PLNT - Investing In Planet Fitness: Wise Move Or Foolish Gamble?

2023-04-20 16:42:50 ET

Summary

- Low insider holdings, vulnerable customer base, unattractive valuation, potential headwind of inflation in 2023.

- Recurrent revenue stream, commendable industry tenacity. Reasonable pricing strategy, and expansion into international markets.

- Planet Fitness faces challenges but its recurrent revenue stream and pricing strategy make it an intriguing stock to watch, with analysts' opinions divided.

Investment Thesis

SA analysts appear to dislike Planet Fitness, Inc. ( PLNT ) while Wall Street analysts rated it an average strong buy. The company's low insider holdings and vulnerable customer base are alarming, and the current valuation is not very attractive. Additionally, the potential headwind of inflation in 2023 is a cause for anxiety.

However, it's important to note that these challenges do not negate the company's strengths, and the industry's overall tenacity is commendable. In fact, there is a surprise silver lining in the fact that Planet Fitness's membership and franchising models provide a relatively stable recurrent revenue stream, allowing the company to generate operating income even in tough times like the COVID situation in 2020. While investors should remain cautious, there is potential for Planet Fitness to continue disrupting the industry with its reasonable pricing strategy and expansion into international markets, making it an intriguing stock to keep an eye on.

We'll advise investors who like this name to buy in, keep their positions small, and add more if the price drops or if we gain additional insight into the macro impact on the company's customers.

Company Profile

Planet Fitness is one of the largest and fastest-growing franchisors and operators of fitness centers in the world, with a highly recognized national brand.

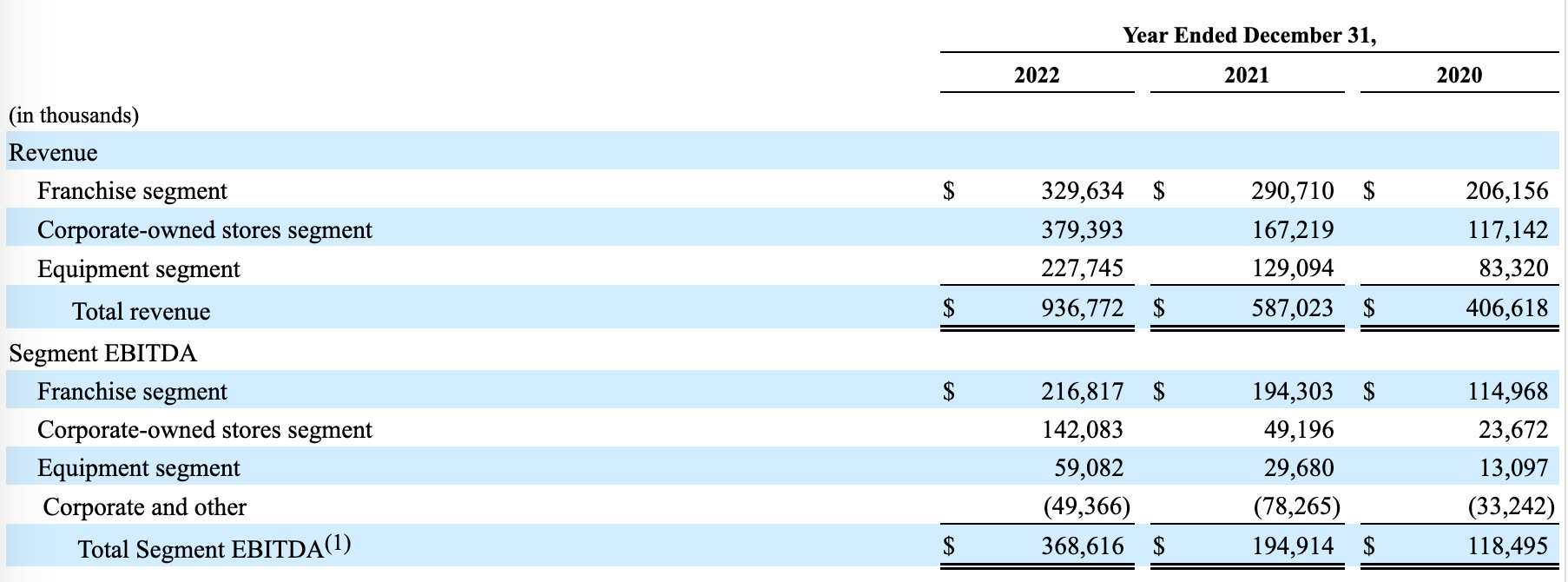

- In 2022 , the company's revenues were $936.8 million and system-wide sales were $3.9 billion.

- The company had approximately 17.0 million members and 2,410 stores in all 50 states, the District of Columbia, Puerto Rico, Canada, Panama, Mexico, and Australia.

- System-wide sales for 2022 included $3.5 billion attributable to franchisee-owned stores and $395.1 million attributable to its corporate-owned stores.

- Of the 2,410 stores, 2,176 were franchised, and 234 were corporate-owned.

Company Fundamentals

{kind=link}

Financials (Company's filing)

Franchise segment revenue:

- Includes royalty, NAF, franchise, placement, online join, and other fees

- Comprised 35%, 50%, and 51% of total revenue for 2022, 2021, and 2020, respectively

- Construction of franchise stores: Averaged approximately 21 weeks in 2022 and 2021 based on US franchisee data

- Franchisees' investment to open a new store: Un-levered investment ranged from approximately $1.7 million to $3.8 million based on samples in 2022

Corporate-owned store segment revenue:

- Includes membership dues, enrollment fees, annual fees, prepaid fees, and retail sales

- Comprised 41%, 28%, and 29% of total revenue for 2022, 2021, and 2020, respectively

- Over 90% of members paid monthly dues by EFT, and the remainder prepaid annually.

-

Corporate-owned stores in 2022:EBITDA margin of 37.5%Average unit volume of $1.8 million Store-level profitability assessment of 42.0%7% royalty rate reducing the four-wall EBITDA margin to 34.8%

Equipment segment revenue:

- Includes equipment revenue for new and replacement equipment for franchisee-owned stores in the US, Canada, and Mexico

- Franchisees are generally required to replace equipment every 5-7 years

- Comprised 24%, 22%, and 20% of total revenue for 2022, 2021, and 2020, respectively.

Growth Drivers

- The exceptional value proposition appeals to a broad member demographic

The company believed its TAM can be as large as 250 million population in U.S. and Canada given its competitive price. It had 20% stores located in "low-income" areas and a 50% female customer base.

Our member base is approximately 50% female and our members come from both high- and low-income households. Approximately 20% of our stores are located in areas that the US government deems “low income,” providing access to improve health and wellness in underserved communities.

The company also had international expansion plans. They operated in Dominican Republic, Panama, Mexico, and Australia. The management was optimistic about Mexico and Australia.

But just to let you know on that, the initial read on Mexico and Australia, they really performed well. I've been really happy also with sales. And the model is actually translating very, very well in the markets outside the US.

- Highly attractive franchise system built for growth. The company stated that its franchise model was performing well and its franchisees continued to open new stores under the partnerships.

Our streamlined model features relatively fixed labor costs, minimal inventory, automatic billing and limited cash transactions.

The attractiveness of our franchise model is further evidenced by the fact that our franchisees re-invest their capital into the brand, with over 90% of our new stores in 2022 opened by our existing franchisee base.

- Increasing the mix of PF Black Card memberships by enhancing value and member experience. The company initially started with a $10 monthly membership program and successfully raised average monthly fees by launching its premium membership program at $24.99 per month. This can act as strong support for its claim on TAM.

Our PF Black Card members as a percentage of total membership has increased from 60% as of December 31, 2018 to 62.5% as of December 31, 2022, and our average monthly dues per member have increased from $16.52 to $18.01 over the same period.

- Increase franchising fee

Typically, the fitness industry charges a franchise fee ranging from 5%-10%. The company had success in raising its franchise fee and might be able to increase the fee in the future.

Continue to expand royalties from increases in average royalty rate and new franchisees. While our current franchise agreement stipulates a monthly royalty rate of 7% of monthly dues and annual membership fees, as of December 31, 2022, only 47% of our stores are paying royalties at the current franchise agreement rate, primarily due to lower rates in historical agreements. As new franchisees enter our system and, generally, as current franchisees open new stores or renew their existing franchise agreements at the current royalty rate, our average system-wide royalty rate will increase. In 2022, our average royalty rate was 6.5% compared to 5.6% in 2018.

Industry

- Wellness services may be recession-proof compared to other Services, according to Survey

In fact, 62 percent of the 2,000 U.S. adults surveyed said they are willing to limit their social life and go to bars and concerts to continue to afford preventative health and wellness activities.

In our piece Under Armour: Finding Joy In The Darkest Of Times, we discussed the resilience of the sports industry and the possibility of increased consumer spending following the traveling cycle.

- Consumer spending may increase following the traveling cycle.

One possible reason for the sluggish consumer spending in the consumer discretionary sector could be attributed to the recent surge in travel trends. Once travel demand slows, it's likely that spending will return to the consumer discretionary sector.

During its Q1 2023 earnings call, Delta Air Lines expected a strong June quarter with capacity and revenue growth and is investing in its global network and technology to support future growth and margin expansion.

Moving forward, we are sunsetting the comparisons to 2019 and returning to year-over-year metrics. Domestically, we are growing our seats mid-single digits over last year with our core hub rebuild beginning to take hold in June and accelerating through the fall. On international, we are excited with the momentum we’re seeing and expect record revenues and profitability for the summer travel season. To meet increasing demand, we are growing our international seats by more than 20% in the June quarter compared to the prior year, and we already have about 75% of our bookings on hand.

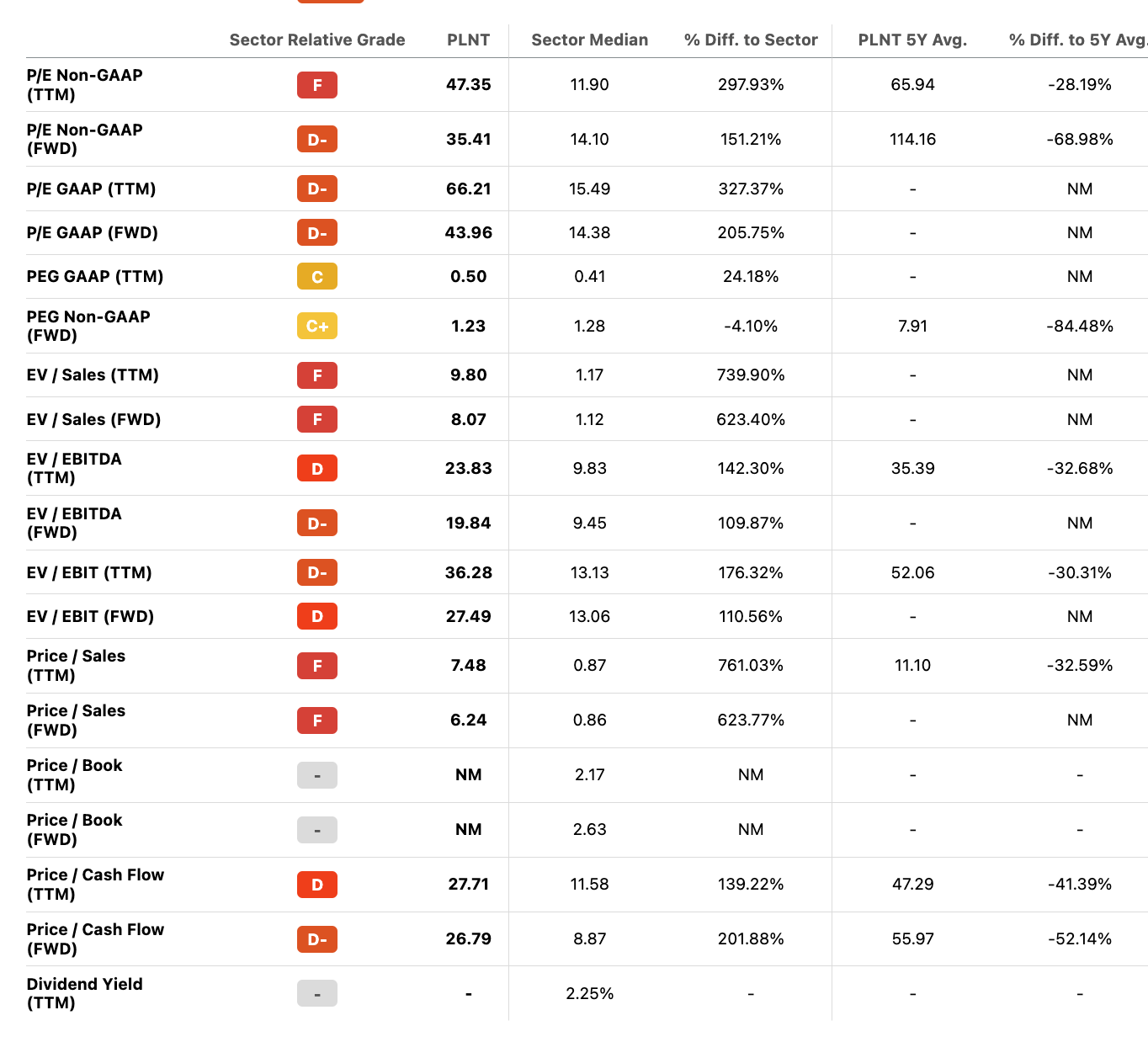

Valuation

Most of its valuation multiples trade below its 5-year average but higher than the sector median.

{kind=link}

Valuation multiple (Seeking Alpha)

The company projected its revenues to increase by 13%-14% and adj EPS to grow by 33%-36% in 2023. This makes its FWD PEG ratio less than 1.5x. Its FWD EV/EBITDA is at 20x.

New equipment placements of approximately 160 in franchisee-owned locations

System-wide same-store sales in the high single-digit percentage range

The following are 2023 growth expectations over the Company’s 2022 results:

Revenue to increase in the 13% to 14% range

Adjusted EBITDA to increase in the 17% to 18% range

Adjusted net income to increase in the 30% to 33% range

Adjusted earnings per share to increase in the 33% to 36% range, based on Adjusted diluted shares outstanding of approximately 89.5 million, inclusive of one million shares repurchased.

The company believed its TAM can be as large as 250 million people given its competitive price.

Due to our unique positioning to a broader demographic, we believe Planet Fitness has an addressable market that is significantly larger than the traditional health club industry. We view our addressable market as approximately 250 million people, representing the U.S. population over 14 years of age.

If we assume the company can grow its member counts by 4.4 times to 75 million, which is a 30% market share of the 250 million population. The valuation under our DCF model is still expensive. The market value suggested scenarios of higher penetration or global expansion.

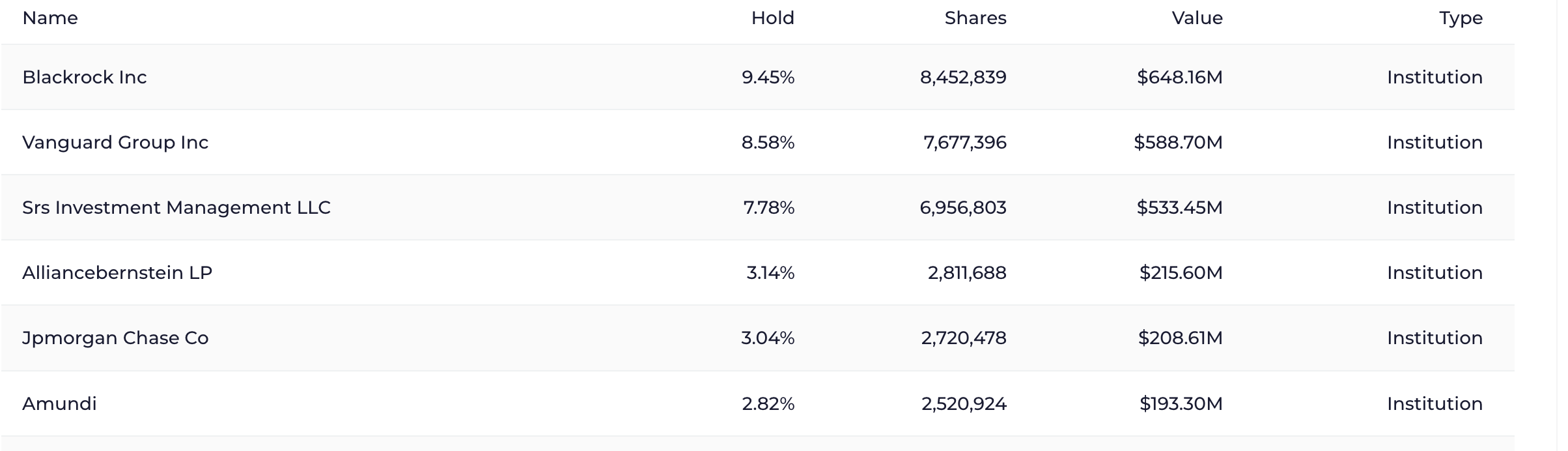

It's worth noting that insiders only hold 0.49% of shares but institutional investors hold 97%.

{kind=link}

Ownership (Wallstreetzen)

{kind=link}

Ownership (Wallstreetzen)

Catalysts

- New store openings

As of December 31, 2022, its franchisees had contractual obligations to open more than 1,000 additional stores, including more than 500 over the next three years. If the expansion plan is executed as planned, it is likely the stock can go higher.

Blackstone -sponsored Nexus Select Trust just announced it planned to double its portfolio of shopping malls in the next 4-5 years to 20 million square feet through acquisition mode. This can signal continued strong consumer spending over the mid-to-long term.

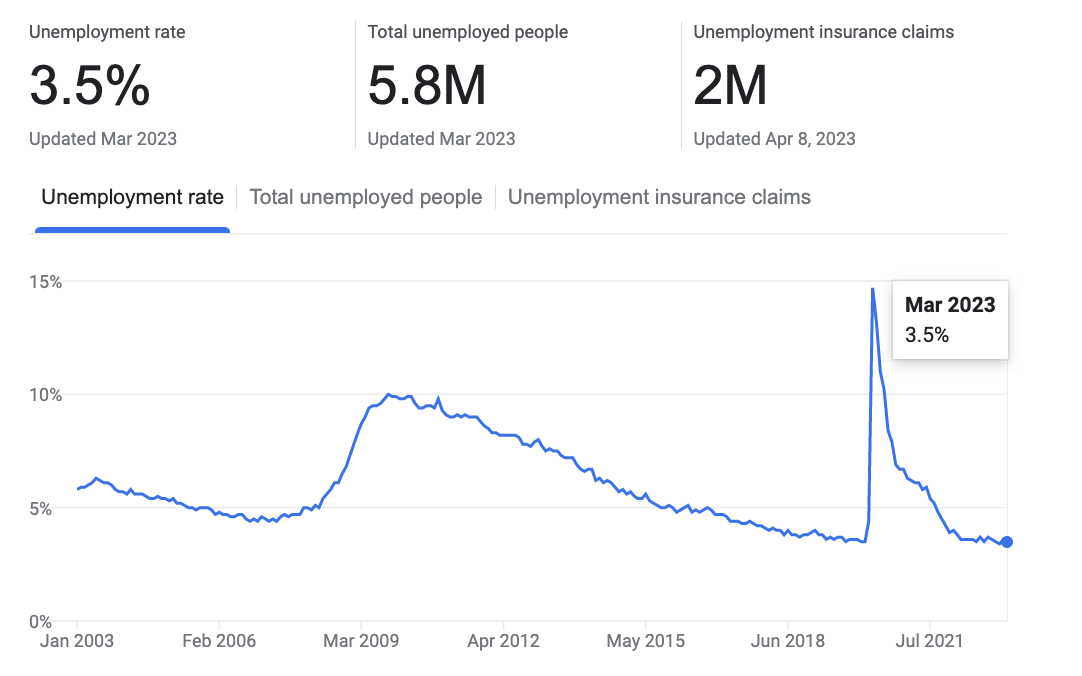

Despite the market worrisome of recession in the U.S., we saw a couple of bankruptcy events and some industries were in trouble but still have not seen any clear sign that the U.S. as a whole is going into recession yet. The unemployment rate was still at a record low in history. This can suggest consumer spending is still strong.

{kind=link}

Unemployment rate (Google)

- 2022 share repurchase program

There is still room to buy back shares. On November 4, 2022, the Company’s board of directors approved a share repurchase program of up to $500.0 million, which replaced the 2019 share repurchase program. In January 2023, the Company purchased 317,599 shares of Class A common stock for a total cost of $25.0 million.

Risks

- Impairment risk

Sunshine Acquisition

Planet Fitness acquired Sunshine Fitness in a cash and stock transaction valued at $824 million, adding 114 clubs to its corporate-owned portfolio, predominantly located in the Southeast United States. This implied an average of $7.2 million per store. Calculating its annual ROI using the company's stats, we arrive at a 10.5% return annually or a payback period of 9.5 years. The return is quite low even considering it was a 50-50 cash and stock deal. If the acquiring stores underperform, there is a cash flow shortfall risk.

- Class Lawsuit

The company is involved in various claims and legal actions that arise in the ordinary course of business. It was and is sued multiple times for over-billing customers and preventing them from canceling their memberships.

These can have a potential financial impact on the company and also can hurt customers' trust long term.

- Macro Impact

Approximately 20% of its stores are located in areas that the US government deems “low income,” providing access to improve health and wellness in underserved communities. This population can be at risk to discontinue the service of the company due to inflation.

Predictable and recurring revenue streams with high cash flow conversion

The company decreased revenue by 40% in 2020 amid the COVID situation. It nevertheless had operating profits of $59 million. The company had about $500 million in cash on hand at the time. It issued a $75 million debt to pay the interest payment and CAEX of $82 million and $52 million. The company was able to survive the COVID situation and didn't close stores attributing to its recurring revenues stream under its long-term franchise contract.

The typical franchise agreement has a 10-year term. In 2022, approximately 90% of both our corporate-owned store and franchise revenues consisted of recurring revenue streams, which include royalties, vendor commissions, monthly dues, and annual fees.

According to IHRSA, from the start of the COVID-19 pandemic in March 2020 through 2022, 25% of all fitness facilities were permanently closed across the United States as a result of COVID-19 pandemic. Over the same period of time, Planet Fitness permanently closed none of its franchisee-owned or corporate-owned stores as a result of the COVID-19 pandemic.

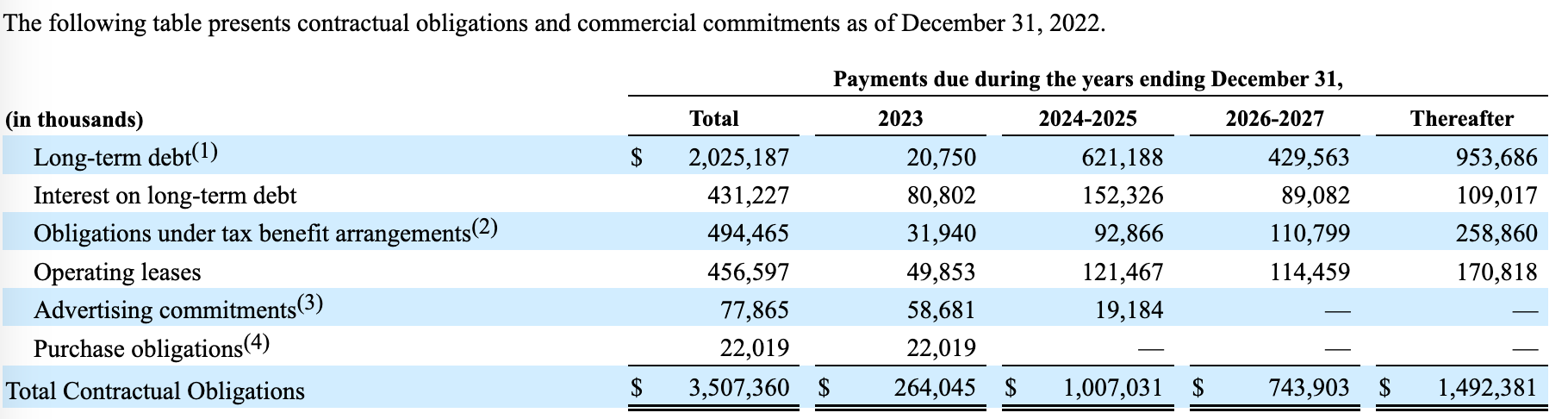

- Debt obligation

{kind=link}

Contractual obligation (Company's filing)

As of Dec 2022, the company had total contractual obligations of $3.5 billion, implying an obligation to EBITDA ratio of 9.5x. Net debt to EBITDA is 4.3x. The company might need to refinance its contractual obligation of around $1 billion in 2024 or beyond.

Recap

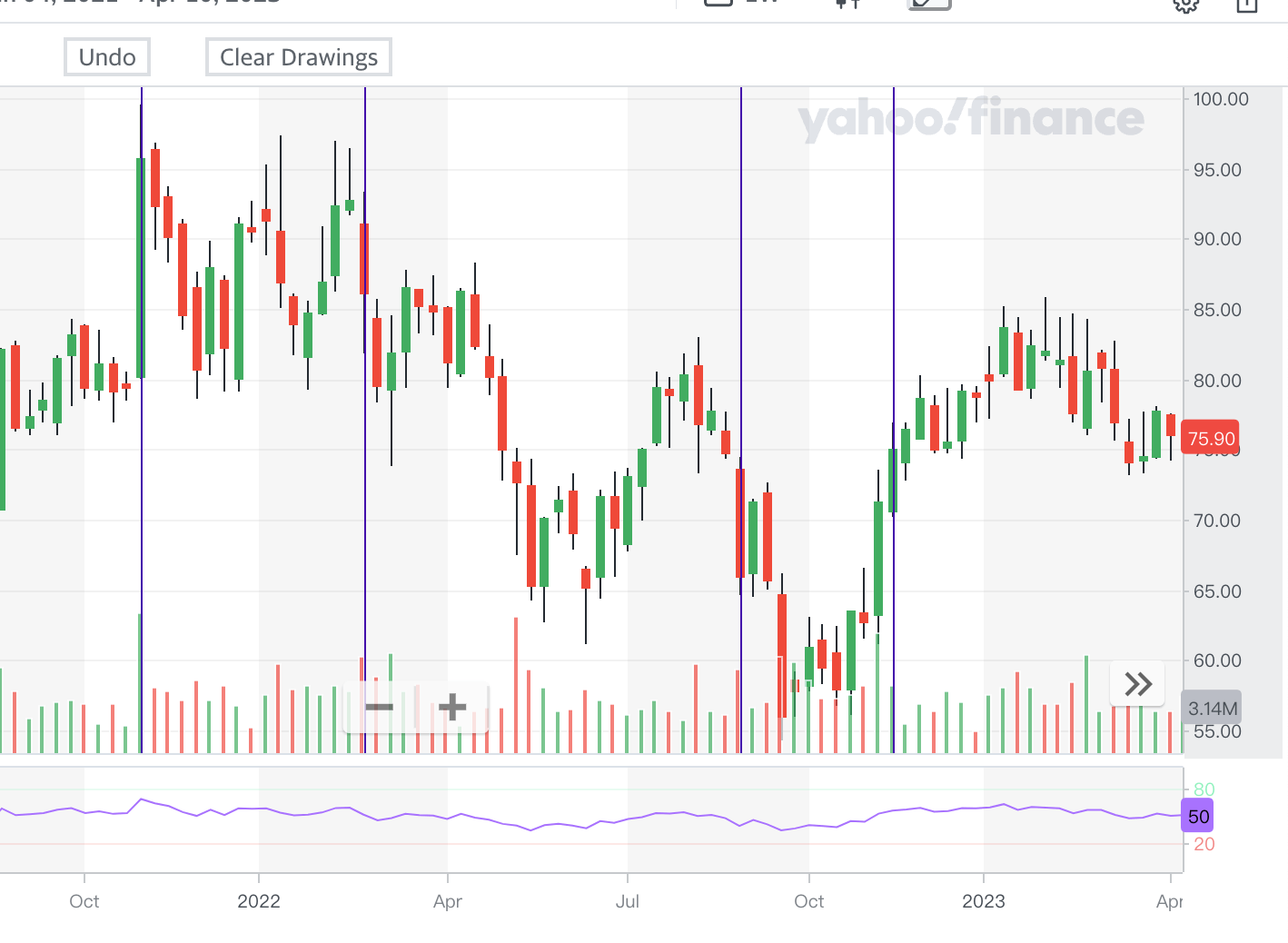

Before we start to introduce the company, we would like to quickly go through the recent history and stock performance of the company.

{kind=link}

Stock chart (Yahoo Finance)

Its stock reached an all-time high of around $95 per share in Nov 2011 while the CEO Rondeau Christopher and President & CFO Lively Dorvin sold shares worth a combined $22 million at the same time. The company announced an $824 million acquisition deal to buy 114 stores from TSG in Jan 2022. Mr. Dorvin left the firm in Aug 2022. The stock dropped from the $90 per share range to $60 per share in 2022. Thereafter, the stock rebounded sharply after the earnings release in 2022.

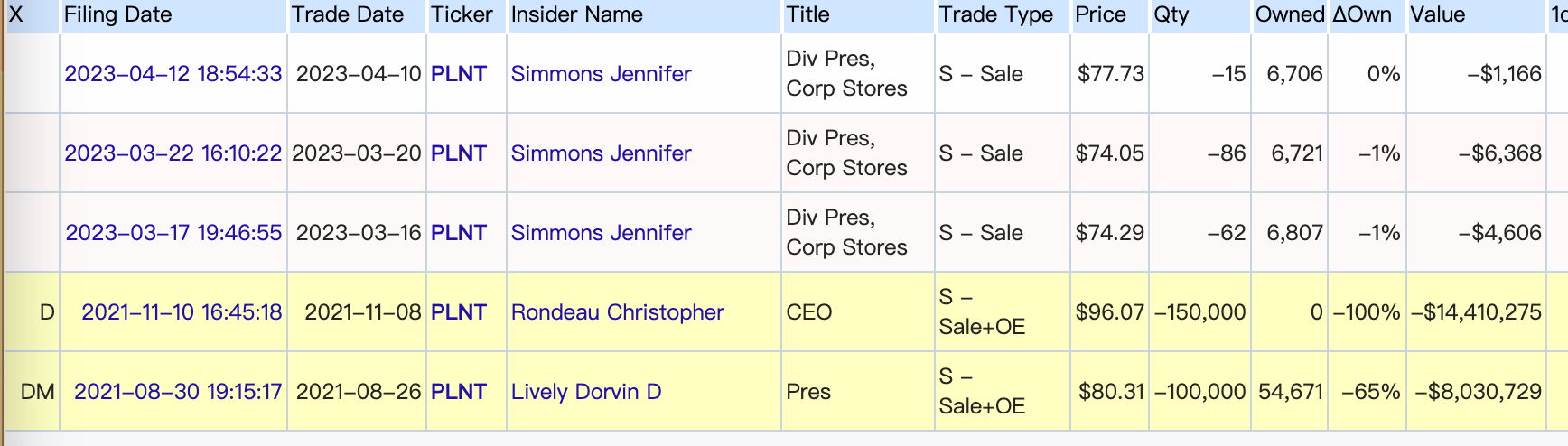

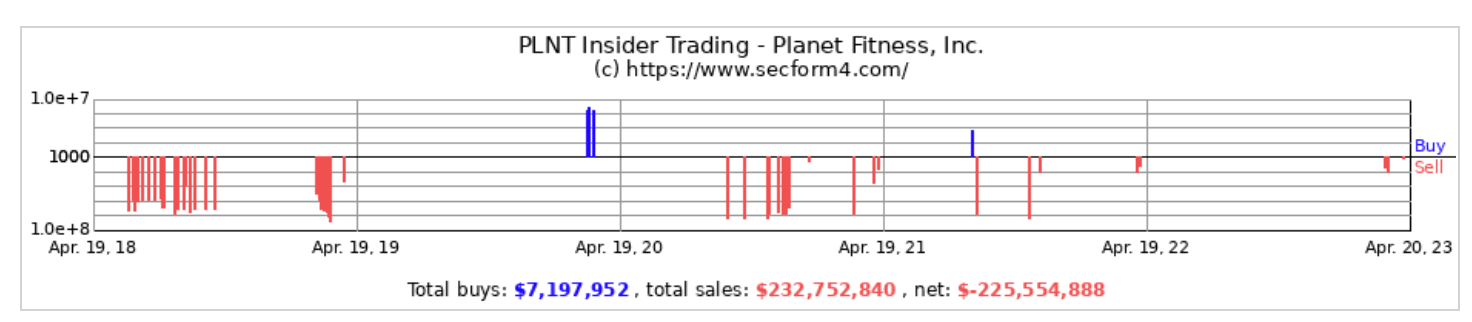

{kind=link}

Insider activity (Openinsider)

{kind=link}

Insider activity (SEC)

Summary

We think low insider holdings and its vulnerable customer base are concerns. Valuation is somewhat not very attractive.

However, we like the fact that the management has a track record of executing its franchising models. CEO Rondeau has been with the firm for 31 years since it was founded in 1992.

The company has the potential to disrupt the industry thanks to its reasonable pricing strategy. We particularly look forward to its expansion into international markets.

The company can face a headwind in 2023 due to inflation. However, we appreciate the sports and fitness industry's tenacity in general. Its recurrent revenue stream is relatively stable because of its membership and franchising models. It still generated operating income in the tough COVID situation in 2020. The company has a number of growth drivers, such as increasing membership spending, opening more stores, and raising franchising prices.

For further details see:

Investing In Planet Fitness: Wise Move Or Foolish Gamble?