SWKS - Investing In Skyworks: A Smart Move For Those Eyeing Growth And Value

2023-11-12 03:42:31 ET

Summary

- Skyworks Solutions is a leading RF manufacturer positioned to take advantage of growth in the 5G market.

- The company's focus on broad markets, including IoT and automotive applications, offers potential for diversification away from the maturing smartphone market.

- While the company's recent earnings report was lackluster, its strong free cash flow and sound balance sheet provide stability and potential for future growth.

When I last wrote an article about the radio frequency ("RF") manufacturer Skyworks Solutions ( SWKS ) on February 05, 2021, I had a thesis that the 5G era had begun. And Skyworks would "live up to its promise as a high growth company that could take advantage of the wireless industry expanding into 5G." I was right in the short term, as the stock hit an all-time high of $189.94 on April 26, 2021. Over the longer term, I was obviously wrong. Between a slowing mobile phone market, inflation, rising interest rates, and a slowing economy, the stock sank 50.53% from its price at my previous article's publication of $178.95 to a price in the high $80s today.

I maintain a buy on this stock. Mobile industry experts project the smartphone phone market to recover in 2024, 5G networks and phones should grow more complex, driving more RF dollar content per phone, and the stock now sells at a far more reasonable valuation compared to early 2021. This article will discuss Skyworks' fiscal fourth quarter 2023 report, growth drivers, and valuation.

The big picture

Skyworks is a long-term innovator in manufacturing RF devices, which mobile phones use to transmit and receive radio waves. According to the company's investor website , it is a "longstanding leader in innovative connectivity solutions with roots going back to 1962." One pattern that has repeated for Skyworks since 2G transitioned to 3G is that revenue has jumped higher with each mobile technology upgrade, with the move from 2G to 3G being the most extreme example. The 3G era began around 2001. As seen in the chart below, year-over-year revenue growth showed a massive jump around that time.

Apple (AAPL) introduced the iPhone in 2007. As one of the most innovative companies in the RF field, it wasn't long before Skyworks became an Apple supplier. Based on iPhone teardowns, it first became part of Apple's supply chain after the company introduced the iPhone 3GS on June 19, 2009. Shortly after that, the 4G era began near the end of 2009 . Between the end of 2009 and March 2019, the start of the 5G era, Skyworks stock rose approximately 520%, around a 20% compound annual growth rate ("CAGR").

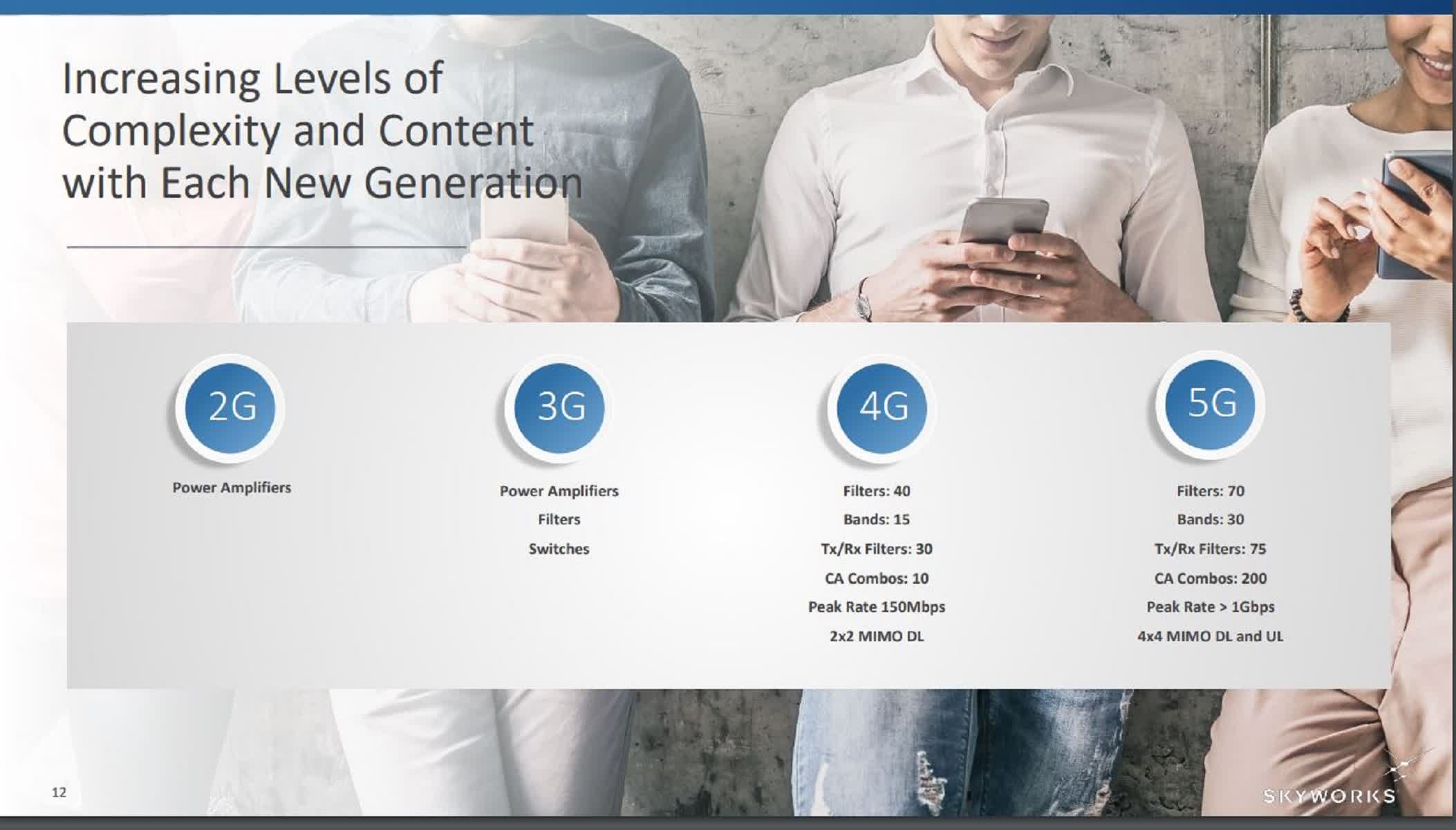

One of the drivers for the stock's rise over these ten years was the increased complexity of 4G over 3G, requiring higher dollar content per phone. The following image shows how each mobile generation requires more complexity and content.

{kind=link}

As a result of the above dynamic, Skyworks' underlying fundamentals like revenue growth, profitability, and free cash flow ("FCF") improved, and investors greatly rewarded the stock in the 2009 to 2019 period. When the transition from 4G to 5G began in 2019, Wall Street expected a growth spurt similar to what had occurred in the transition from 3G to 4G, and initially, that's what happened. Skyworks stock took off in 2020 due to improving fundamentals and the hype surrounding 5G. Still, the stock collapsed in a little over a year as analysts and investors got far less bang than expected due to a worsening macroeconomy and, in part, 5G adoption rates being slower than experts expected. In an article on Deloitte Insights in 2022, the authors cited a poll of 31,600 respondents in 18 countries and stated, "[The poll] suggests that consumers appear indifferent to 5G. Proactive upgrading to a 5G network is not a priority for them. Furthermore, 5G support is only a minor factor when considering new phones."

The excellent news for Skyworks Bulls is that analysts project that 5G adoption should pick up meaningfully moving forward. According to Future Market Insights , 5G should grow at a compound annual growth rate of 48.3% from a projected $19.3 billion at the end of 2023 to $994.8 billion by 2033. As a leading provider of RF devices, the company has positioned itself to take advantage of that growth.

More than just mobile phones

Another factor driving Skyworks' previous growth spurts, aside from increasing phone complexity and more content, was the massive growth of the smartphone market. However, the 5G revolution may not benefit from those same tailwinds. There is evidence that the smartphone market is maturing. According to a chart published by Statista , the year-over-year growth rate for smartphone shipments peaked at around 75% in 2010 and crossed over to negative growth rates in 2017. Smartphone shipments peaked at 1.473 billion in 2016, before the pandemic and the subsequent economic slowdown. So, while the growth of the smartphone market may return in 2024, don't expect blazing-hot growth, as we may be well past peak smartphone.

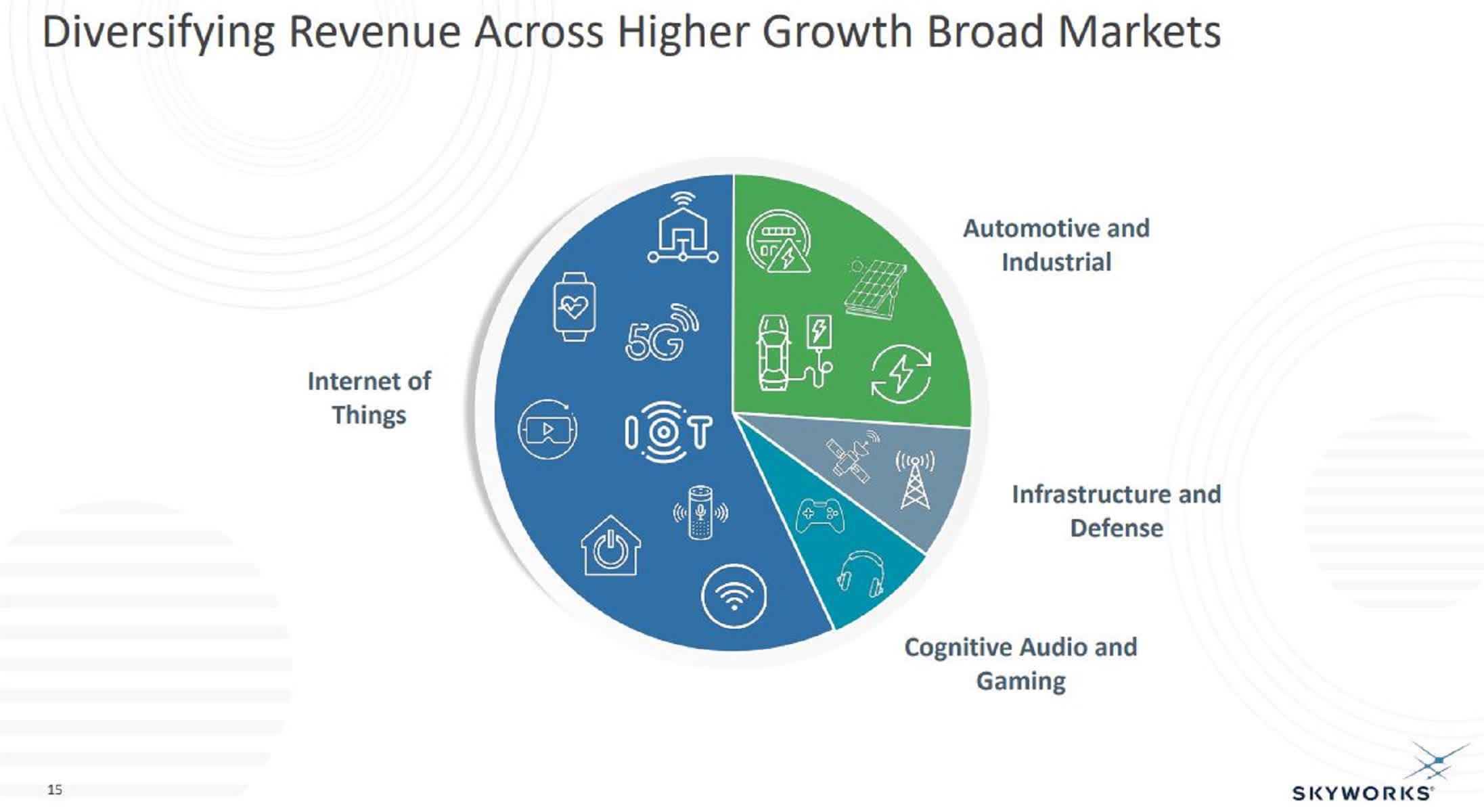

The good news is that the 5G market is more than smartphones and encompasses the Internet of Things ("IoT"), automotive and industrial applications, cellular infrastructure and defense applications, and cognitive audio and gaming. Skyworks refers to these applications as "broad markets."

{kind=link}

Broad markets is growing much faster than the smartphone market. According to Fortune Business Insights , the global IoT market should grow at a CAGR of 26.1% from $662.21 billion in 2023 to $3.35 trillion by 2030 -- explosive growth. Over the last several years, Skyworks has prepared to leave the mobile phone era and has a strategic vision for the IoT era.

{kind=link}

Skyworks bought the Infrastructure and Automotive business of Silicon Laboratories ( SLAB ) in 2021 to expand its business further into broad markets. According to the press release announcing the acquisition, the purchase will help it grow into the following potentially lucrative markets:

- Electric and hybrid vehicles

- industrial and motor control

- power supply

- 5G wireless infrastructure

- optical data communication

- data center

- automotive

- smart home and several other applications

Investors hope its efforts to grow in the faster-growing broad markets will diversify it away from the slower-growing mobile business and Apple. If you decide to invest in Skyworks, monitoring its broad market segment share of total revenue is vital.

Skyworks lackluster earnings report

The company's latest earnings report was lackluster. Although some saw " glimmers of hope ," it was nothing to write home about either. The company's Q4 revenue was down 13% year-over-year to $1.219 billion, in line with analysts' estimates. Management forecasts first-quarter 2024 revenue of between $1.175 billion and $1.225 million. At the mid-point of $1.20 billion, revenue would be down only 20.5% year-over-year in the fiscal first quarter.

The company's gross margins continued a sharp decline in 2023. Management explained during the earnings call, using far more technical language, that Skyworks had temporarily reduced factory production to lower its inventory levels in the wake of a supply glut, negatively impacting gross margins. In the fourth quarter, Skyworks recorded generally accepted accounting principles ("GAAP") gross margins of 39.2% and non-GAAP gross margins of 47.1%, well below its long-term non-GAAP target of 53%. Management forecasts a non-GAAP gross margin of 46% to 47% for the fiscal first quarter of 2024. These numbers are ugly, and investors should not expect the stock to rebound soon.

If you have not paid attention to Skyworks over the last several years, be aware that when mobile phone growth ran into a brick wall in 2021 into 2023, the company suddenly made too many RF devices versus demand, and its inventory ballooned. During the company's earnings call , Chief Executive Officer ("CEO") Liam Griffin said:

While excess supply conditions are modestly improving in the Android market, we continue to under-ship to natural demand as the industry rebalances. Within broad markets, we see softer demand extending from consumer to certain durable sectors as customers adjust to normalize lead times and reduce excess inventory. After two years of unprecedented events due to COVID and historical supply chain shortages, the semiconductor industry is returning to a normal supply and demand balance.

Source: Skyworks Solutions Fiscal Fourth Quarter 2023 Earnings Call

While the good news is that Skyworks is close to finishing burning off inventory in the mobile phone market, the unwelcome news is that some portions of the broad market segment are currently entering a similar inventory correction. However, one thing that Skyworks investors can look forward to is that once the company finishes working off all its excess inventory in mobile and broad markets and ramps up factory production to meet demand, revenue should reaccelerate. Its GAAP gross margins should also rise from its current 39% to more normalized levels of between 48% and 51%. Skyworks Chief Financial Officer ("CFO") said during the earnings call:

Looking ahead, couple quarters, obviously March and June are our seasonally slower quarters in terms of top line. And typically you see a modest reduction of gross margins during those quarters. And then beyond that, you look at the second half of the calendar year, September and December, we will start ramping up again, and you will see gradual improvements of the gross margins.

Source: Skyworks Solutions Fiscal Fourth Quarter 2023 Earnings Call

If the above statement by the CFO holds true, the stock price could start rebounding in the September or December quarter of 2024.

Skyworks' fiscal fourth-quarter 2023 GAAP net income was $244.8 million, and its diluted earnings-per-share was $1.52, both numbers down 19% from last year. Its non-GAAP EPS was $2.20, beating analysts' consensus estimates by $0.10.

While profitability may suffer, the company gushes free cash flow ("FCF"). It grew its trailing 12-month FCF by 76% over the previous year's comparable quarter to reach $1.6 billion of FCF, a 34.5% FCF margin. Its FCF yield was 12% -- an outstanding number for a dividend growth company. The best part is that CFO Kris Sennesael said that it believes its FCF is "sustainable," and the company targets multiple years of a +30% FCF margin.

Skyworks has a sound balance sheet. The chart below shows it still has $1.29 billion of debt on the balance sheet from financing its acquisition of Silicon Labs' infrastructure and automotive business. Cash and short-term investments were $738.50 million.

Because it has a robust FCF flow, it can quickly pay down this debt even in a down market. On the earnings call, the CFO said:

[We] repaid $200 million of our term loan [in fiscal Q4]. In early October, we repaid $150 million of outstanding borrowings under the term loan, and we intend to pay off the remaining $150 million by year end. Entering calendar year 2024, we are comfortable with our capital structure and debt levels of $1 billion, which provide us with superior flexibility and optionality.

Source: Skyworks Fiscal Fourth Quarter 2023 Earnings Call

It also used its cash flow to pay $108 million in dividends in the quarter and declared a $0.68/share quarterly dividend .

It has a few risks

The most significant threat that could ruin the buy thesis for this company is its customer concentration with one company. According to Skyworks 2022 10-K , Apple accounted for 58%, 59%, and 56% of its net revenue for fiscal 2022, 2021, and 2020, respectively. While the company has benefited substantially over the past ten years from being one of Apple's primary suppliers, it comes with massive risk. If Apple ever decides to use another vendor, Skyworks could have its revenue cut in half. Cupertino has also shown a desire to replace all the third-party components in its supply chain with its own technology over the last several years.

Although Skyworks' 5G business with Apple doesn't appear to be under any immediate threat, Apple put out job listings for engineers in 2021 to develop 6G wireless technology. Additionally, Apple opened a new office in late 2021 focused on wireless chip production in Irvine, California. Skyworks headquarters established its headquarters in Irvine in 2020. So, Apple is in a prime position to poach employees. Apple followed up its 2021 office opening by expanding its lease in Irvine in July 2023. If Apple develops its own 6G RF technology and 6G deployment begins in 2030, as expected, Skyworks has maybe four to six years before Apple might cut them out of the picture.

The company must diversify its revenue away from Apple, and Skyworks' best chance to do so is by expanding its rapidly growing broad markets business. In its first-quarter earnings call, the CEO mentioned that broad markets is 37% of total revenue, only up from 36% in the previous year's comparable quarter. The company's efforts to diversify away from Apple using broad markets is currently moving at a snail's pace. Suppose Skyworks fails to pick up the pace in its diversification efforts. In that case, the market may be hesitant to award the stock a higher multiple with the Damocles sword of Apple potentially replacing Skyworks' content hanging over the company.

Up until mid-2020, Skyworks' price-to-earnings (P/E) ratio traded in line with Apple. The chart below shows that the relationship decoupled as the market digests the possibility of Apple replacing Skyworks' RF products.

Another risk that investor should monitor are threats to its Chinese business. As of fiscal 2022, China was its second-largest market, making up around 11% of Skyworks revenue. There are numerous risks to that revenue. For instance, if trade relations between the U.S. and China deteriorate, it could negatively impact its Chinese business. China sometimes takes out its frustrations with the U.S. government on U.S. companies.

A recent example is Chinese curbs on Apple's iPhone , which, by extension, also hurts Skyworks. Competition from Chinese companies is another risk. Citi analysts recently downgraded Skyworks over worries that Huawei's Mate 60 smartphone launch could hurt its business due to Huawei supporting domestic RF suppliers.

Valuation

As seen in the chart below, Skyworks' P/E ratio of 14.38 is well below its median P/E ratio over the last five and ten years. Skyworks' Earnings per Share (Diluted) for the trailing twelve months ("TTM") at the end of the September 2023 quarter was $6.13 . Multiplying $6.13 by its five-year median P/E of $16.55 equals a fair value ("FV") of $101.45, up 17.52% from the November 9, 2023, closing price of 86.50. The FV is $118.43, up 37% if you use the ten-year median P/E.

The company's price-to-earnings-to-growth ("PEG") one-year forward ratio of 0.50 is low -- a sign of undervaluation. Generally, the market considers a PEG ratio of 1.0 fairly valued .

Seeking Alpha quant valuation grades Skyworks as a B. Wall Street rates Skyworks as a buy with a one-year price target of $106, which is around a 20% upside.

Buy, sell, or hold?

This dividend growth stock might interest you if you have a more value mindset. Aggressive growth investors, however, may look at the company's current lack of growth and remain uninterested. If you believe the company's revenue growth and margins will improve in late 2024 or early 2025, now is an excellent time to start dollar cost averaging into Skyworks. I rate the stock a buy.

For further details see:

Investing In Skyworks: A Smart Move For Those Eyeing Growth And Value