CG - Investment AI Indexing Private Equity And Berkshire Hathaway

2023-04-16 08:50:39 ET

Summary

- Investment AI will make the equity market more efficient than it is today.

- Three possible responses from retail investors are suggested:

- Increase/initiate the allocation to the market-weighted index such as S&P 500.

- Complement the index with the private equity stocks.

- Initiate/keep holding Berkshire Hathaway.

What follows is my understanding of the problems facing Joe and Jane putting their money to work in the world of investment AI ("IAI"). One option is to do nothing and keep chasing growth or value or yield the old way. An alternative is to recognize that superior IAIs over there will easily beat you in any strategy and adjust your investing style accordingly.

Some readers may find the last statement contradictory: since adjusting investing style represents just another strategy, it could be as futile as any other strategy. However, I hope to demonstrate that this is not precisely correct, at least for now.

In this article, I will focus only on several practical suggestions - quite a few other options are available. Any statement represents nothing more than my subjective and biased opinion and serves nothing more than a basis for further discussions.

Timing and stages

First of all, IAI is already here. The most successful implementations are probably run in secrecy for now. But due to the common usability of ChatGPT, everybody can become smarter than she/he is. And everybody can easily code now, even a person who has no clue of what coding means.

Let me quote a recent post by Grady Simon:

Yesterday, I watched someone upload a video file to a chat app, ask a language model "Can you extract the first 5 s of the video?", and then wait as the language model wrote a few lines of code and then actually executed that code , resulting in a downloadable video file. Oh, and writing and executing code is only one of the many new capabilities that can be seamlessly stitched together by the language model.

Certainly, a similar technique can be used, at least in principle, for investing as well. Until recently, such tools were hardly available even for advanced companies not to mention an average Joe. These advanced companies, in their turn, may have access to better databases, some advanced IAI training, more sophisticated evaluation tools, etc. And this is something that I guess is happening now and represents the first stage of IAI implementation.

Trading should be the first victim at this stage. The more you trade, the more you lose against IAI. Technical investing may be the next victim, followed by quant investing and fundamental analysis. And so on. All strategies listed are based on quantitative metrics which make them vulnerable to IAI sooner rather than later. Let me use here a chess analogy.

Earlier chess programs, including the ones with superhuman abilities, used primarily quantitative methods. They were superior in tactics but less skilled in making positional or strategic decisions that did not succumb to straightforward calculations. For the same reason, for a long time, programs were losing to humans playing Go which is less tactical but more strategic. Certainly, it has changed since the appearance of AlphaZero several years ago. The latter step represented the next stage of chess AI.

What could be a strategic decision in investing that would not be easily handled by IAI? Several things come to mind and I will start with the simplest one. In 2016-18, Warren Buffett bought Apple ( AAPL ) stock. By itself, the decision was not outstanding. A lot of people knew that Apple was inexpensive, profitable, and promising. But Buffett invested about $35B in AAPL equal roughly to 7% of Berkshire Hathaway's ( BRK.A ) ( BRK.B ) market cap at the time (it took the company half a century to reach this market cap!). As far as know, buying a single stock in such quantities had never happened before. It was something comparable to a brilliant intuitive positional decision in chess when a player relies more on intuition than on accurate calculations. Calculations are still important as a safety tool but not for idea generation.

In retrospect, Buffett's decision may seem obvious but I doubt it was. He neglected diversification rules on a grand scale with a hi-tech stock that was arguably not his area of expertise. Perhaps, this kind of decision cannot be handled by IAI yet.

Another promising path to beating IAI at its current stage could be coming up with a completely new investment idea not represented in any form in the IAI training set. This idea may be either very simple or quite complicated. It does not matter as long as the idea is in uncharted waters outside of the previous experience.

There are many good analogies of it in science. For example, Bohr's postulates for those who are familiar with physics. They came from nowhere and did not represent any logical step that could be somehow derived from what was already known. In math, where almost everything is formally derived from what is already known, I would mention the invention of the Fourier series in the XIX century by a young mathematician based on well-known calculus. The idea that any function could be represented by a sum of sines and cosines was so counterintuitive that some of the greatest math minds of the time refused to believe it even when presented with rigorous proof. Modern AI may not be able to replicate these leaps of human thought yet.

In one of his articles , Stephen Wolfram provided a beautiful illustration of the last statement. He made a neural net to learn a simple step function that was defined for the values of its argument from -1 to 1 and was not defined anywhere else. After ~10M points in the training set, the network learned the function almost perfectly.

However, depending on the training details, there were several different collections of weights (i.e., different solutions for the same network) that learned the function equally well. But these different solutions provided dramatically different results outside the training region. The neural net could perfectly interpolate the function but did not have a clue of how to extrapolate it.

My original article had a picture that I reproduced from Wolfram's article to make the last paragraph easily understandable. Unfortunately, per SA's request, I had to remove the picture because I did not receive authorization to reproduce it. If you are interested, please take a look at the section of Wolfram's article called "Machine Learning, and the Training of Neural Nets" - one glance at the picture will suffice.

Nothing is surprising in this, as the neural net has no idea how the function behaves outside the training region. Humans, however, are different due to their intuition and imagination.

To illustrate this stage in investing, let me use the recent example of the Silicon Valley Bank ( SIVB ) collapse. I'll assume my readers are familiar with what happened and will not retell the story.

The collapse of SIVB was due to the combination of two factors: a mismatch of assets and liabilities and the possibility of a bank run that could happen almost instantly due to mobile banking and modern communication tools. The first factor was a result of greed, gambling, and rather poor management. It seems easily predictable by both humans and AI.

But the second factor, seemingly obvious in retrospect, represented something completely new. Until the SIVB disaster, bank runs were taking much longer being limited by the physical dispensing of cash.

As far as I understand, the Fed's stress scenarios did not foresee this development either. Perhaps, it was not so obvious after all.

Another well-known case of something completely new in finance and investing was mortgage-backed securities vulnerability as the root cause of the Great Financial Crisis. We know that certain outstanding investors predicted it and acted accordingly.

A neural network that could predict the SIVB collapse due to a quick bank run (a rather simple event that had never happened) or the GFC due to an MBS vulnerability (a more complicated event) might not exist yet.

In this post, I will assume that we are currently only at the first stage of IAI implementation. The second and so on stages will follow but, perhaps, not immediately. I might be wrong but this assumption seems the most plausible to me.

Joe and Jane act

Investing involves two separate processes - asset allocation and asset selection. This post is solely about stock selection and will leave everything else, including asset allocation, untouched.

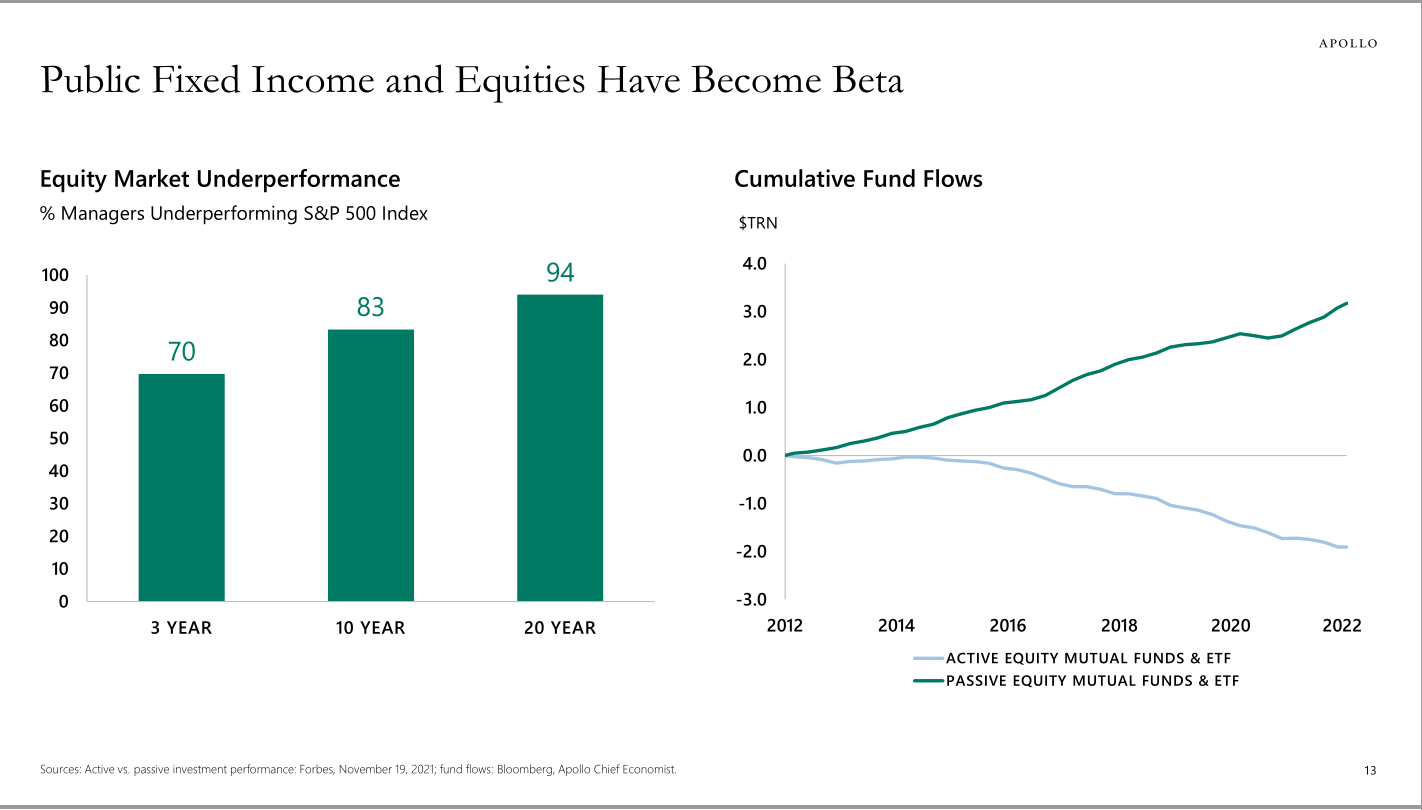

IAI implementations should make the stock market more efficient as more resources are committed to analyzing it. But the stock market is already quite efficient today as is shown on the next slide from Apollo's ( APO ) presentation:

{kind=link}

Since it is difficult to beat index funds, investors have preferred them vs. active strategies as shown on the graph on the right part of the slide. IAI is expected to further support this trend and Joe and Jane should increase their allocation to index funds within their stock holdings.

By indexing I mean S&P 500 mimicking funds such as SPY ( SPY ) or similar instruments or total market funds that are not very different from SPY. I do not mean any type of equal-weight funds or funds designed to replicate specific strategies or industries. Only broad market-weight tools such as SPY allows overweighting the strongest performers. It is the best Joe and Jane can do to reproduce Buffett's move to buy Apple.

SPY is not as diversified as equal-weight indexes. Quite a few people measure diversification by the number of stocks in the portfolio without accounting for their weights. This is wrong as the portfolio consisting of 90% of stock A and 10% of stock B is significantly less diversified than the portfolio of the same two stocks in fifty-fifty proportions.

For a long time, I have used a simple original formula to measure my portfolio's diversification (I published about it several years ago but will reproduce it here). If we have N stocks in the portfolio with their weights denoted as w i , then diversification n can be calculated as follows:

Author

Those who know statistics may figure out that my formula becomes precise (in terms of measuring portfolio volatility) when stocks are uncorrelated and have the same standard deviation. In other cases, it is but a useful proxy.

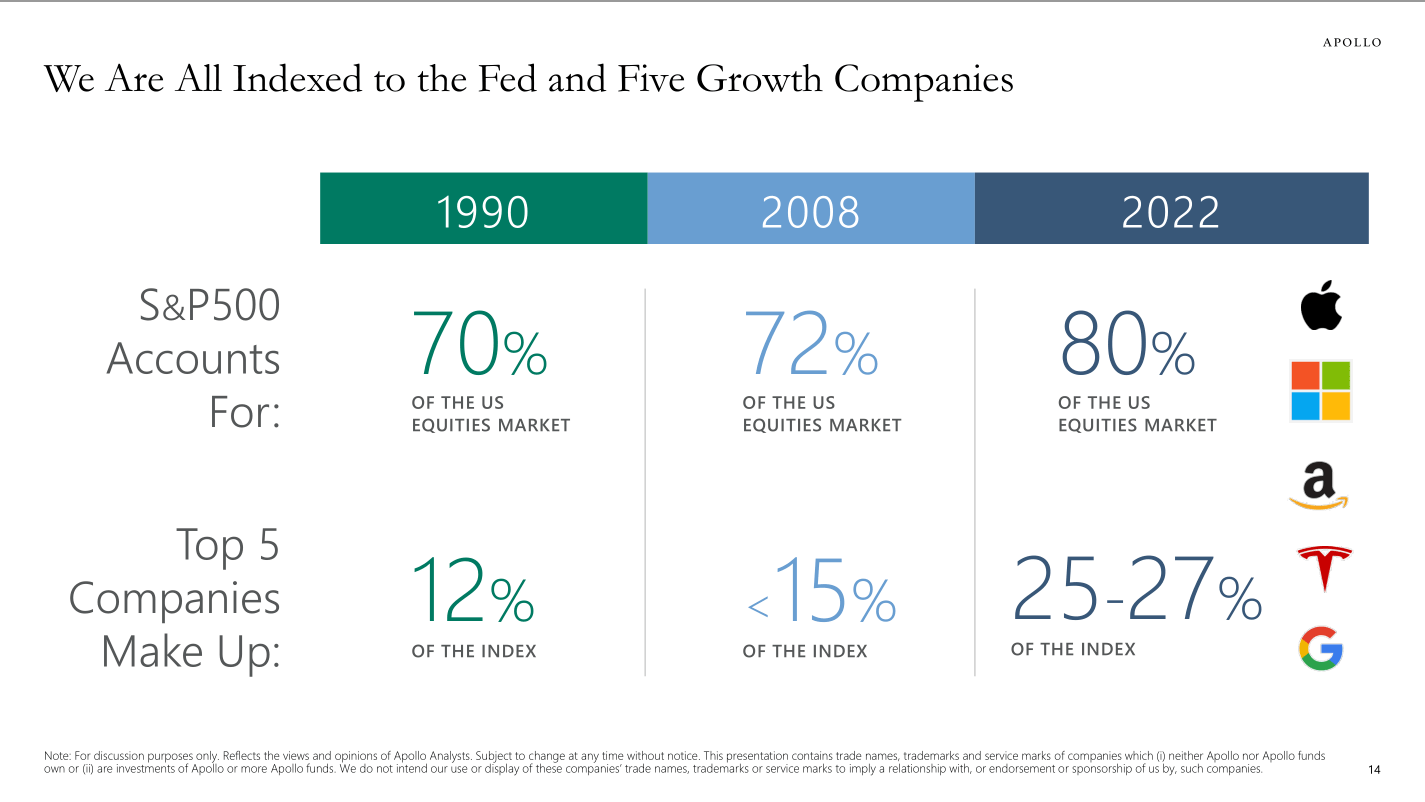

For the S&P 500, my formula typically produces diversification between 60 and 70, way lower than 500 in the name of the index. The real diversification is still much lower due to strong correlations within industries. The same fact is reflected in one of Apollo's slides:

{kind=link}

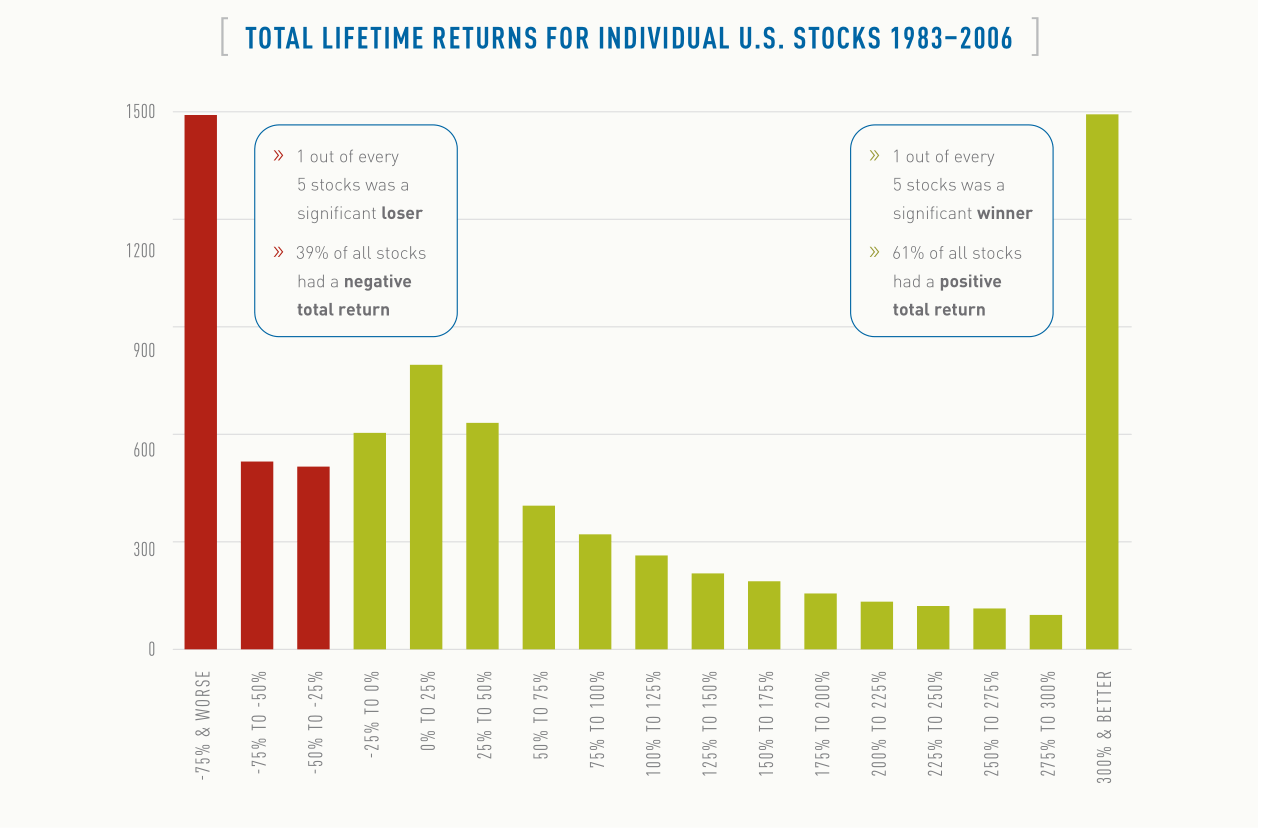

Despite all positivity that people and media ascribe to diversification, I would argue that excessive diversification is a strong negative. It is rather obvious from the graph below. One can achieve better diversification only at the high cost of inferior returns!

{kind=link}

Joe and Jane may pose the next question: "Do we need to invest all our stock allocation in SPY?". Not necessarily, in my opinion, because the target, while investor-specific, is multi-dimensional and the total return alone fails to describe it. To explain it, I will use my personal preferences as an example.

When investing in stocks, I am guided by several partially conflicting requirements that I ranked by their importance to me:

- Increase the total return.

- Reduce risks through reasonable diversification and avoidance of high-risk stocks (such as high-leveraged issues, micro caps, "melting ice cubes", suspicious industries, etc.).

- Reach high tax efficiency.

- Increase income.

- Enjoy the investing process.

Others may disagree with my ranking, and neglect item 5 completely. Many SA readers may pinpoint item 4 as the dominant.

For most rational investors managing their own money, SPY alone cannot match their target. For me, index investing fits the first three requirements but misses the last two. My individual stocks generally hit items 1, 3, 4, and 5. I am trying to combine the index and individual stocks to get a better mix.

Until recently, my split between the index and individual stocks was close to fifty-fifty for many years. However, I started increasing my index allocation once I digested ChatGPT and GPT 4.0 capabilities.

I suggest that Joe and Jane should increase (or initiate) their index allocation as the most obvious and simplest response to the IAI threat.

Private Equity

Different strategies are available to complement SPY with individual stocks or other equity instruments. Income generation is a clear objective for many leading to adding REITs, MLPs, BDCs, etc. to their investment portfolios. There is nothing wrong with it as long as one controls risks and implements strict accounting to make sure that the incremental income does not cost too much in terms of sacrificing total return. In this regard, I am impartial to Enterprise Product Partners ( EPD ). Its results are not related to commodity prices, it is conservatively capitalized and its assets are irreplaceable. The fact that it is often available at an 8% tax-efficient yield with distributions growing at 4-5% annually keeps me puzzled no matter what.

But in this section, I would like to focus on another group of stocks to complement SPY at the time of IAI. I mean alternative ("alt") asset managers aka private equity. Two completely independent lines of thought support this idea.

The first line is straightforward. Big alt managers such as Blackstone ( BX ), Apollo, Brookfield ( BN ) ( BAM ), Ares ( ARES ), KKR ( KKR ), and Carlyle ( CG ) are very influential, control a significant part of the US economy, and employ a lot of people within their holdings. Meanwhile:

- They are not represented in SPY at all even though Apollo has a good chance to be added rather shortly.

- Historically, many of them (if not all) have outperformed SPY since their IPOs.

- Their income today is derived primarily from growing "sticky" management fees rather than capricious carry. Thus, they are not that risky anymore.

- Asset-light companies (such as BX, BAM, ARES) generate high and quickly growing yields of ~4-5% far exceeding SPY's yield and beating many REITs as well. ARES has managed to increase its yield by close to 20% annually over the last several years.

Based on these arguments, alt managers can be a very valuable addition to the index providing better diversification and increasing both income and total return at the same time. But all this seems rather obvious and IAI has to account for it as well (so far, the market has not recognized this opportunity. Either it is illusory or the market is not that efficient).

The second line of thought is more subtle. Over the last several years, alt managers have instituted a quiet revolution. Historically their private funds were available only to institutional investors and the superrich. Today two of them (BX and Blue Owl ( OWL )) made their private funds available to Joe and Jane as well through various distributors - banks, broker-dealers, etc. This practice is still not widely spread but other alt managers are joining the race and within several years private funds (aka "alternative investments" or simply "alts") may become a household name similar to mutual funds.

Yes, Joe and Jane will pay a price for the right to participate. First, their alts will not be as liquid as stocks or mutual funds. Alt managers impose certain restrictions on withdrawals and this has recently led to negative publicity for BX. Secondly, Joe and Jane may pay a fee to a distributor on top of fees charged by the alt manager.

In my opinion, both issues are temporary. Eventually, the public will recognize and come to terms with the limited liquidity of alts similar to how it has recognized the limited liquidity of annuities or other insurance-wrapped investments. At that point, distributors may not be needed either as alts can be sold via the Internet.

The best alt managers have beaten the index over the long run and have a built-in advantage over IAI. Investments by private equity combine rational and numeric assessment of available opportunities, human factors, and leverage. By "human factors", I mean both the unique ambitions and temperament of private equity execs and equally human emotions of owners/managers of private equity investees. Leverage just amplifies what is already there. This is something that IAI cannot do because of the human element. Risks that appear inherent in the model have failed to realize for big alt managers except for isolated cases. To put it plainly, top alt managers have beaten the index for almost all of its flagship funds after fees. IAI may facilitate this activity but can hardly compete in private deals directly.

As of now, Joe and Jane can invest only in alts committed to secured lending and real estate. But in the nearest future, the options will multiply due to the proven creativity of alt managers. The recent AAA fund from Apollo available in retail format is a promising step in this direction.

For Joe and Jane, alts may become an important addition to index funds and other public investments. In the world of more efficient markets, alts from best managers may become a unique opportunity to beat the index.

If alts become that popular, top alt managers will benefit disproportionately. It might be not unlike BlackRock's ( BLK ) or Vanguard's success. Then alt managers' stocks have a good chance to outperform due to the fees that Joe and Jane will pay.

This second line of thought is not so obvious and uses extrapolation. As we already know AI is not so good at it.

So, my second suggestion would be to get exposed to big alt managers in addition to holding the index.

Berkshire Hathaway

Many investors consider Berkshire Hathaway ( BRK.A )( BRK.B ) as the only single-stock alternative to the index. Consequently, Joe and Jane can initiate or increase their Berkshire position in response to IAI.

I have been holding the stock for close to 20 years and its return closely matches the index over the long run. Berkshire has one clear advantage over the index - it is more tax efficient since it does not pay dividends. In one of his letters, Buffett suggested that those who need income can sell the desired amount of stock each year (say, 4% to receive a 4% "yield"). Contrary to real dividends, only part of this artificial "dividend" will be taxed as a long-term capital gain.

Another BRK advantage versus the index is that the stock can be valued, and based on this valuation, bought or sold at an opportune time. This may add a point or so to one's returns.

There are several ways to value the stock and I published the method I prefer. It is simple, so Joe and Jane can use it without any external help. Buffett may have known about the method many years ago - please check my publication for details, it is an interesting story.

As I mentioned earlier, any numerical method is accessible to IAI as well and Joe and Jane can only marginally beat the index (perhaps, on an after-tax basis only) holding BRK. But even this should be a good result in the world of IAI.

Can Berkshire do better than this? Only if it can do something positive that IAI cannot predict. Buying a stock like Apple in humongous quantities shows that such things are possible. Unfortunately, it is not likely that Buffett will run the company for many years longer. What can we expect from Berkshire without Buffett?

From the example of Steve Jobs and Apple, we know that outstanding companies with hand-picked management can outperform long after their creators are not around. I would assume that the insurance business will continue performing well post-Buffett with Ajit Jain (and now also Joseph Brandon from Alleghany) around. Non-insurance businesses should perform well too under Greg Abel - Buffett has never managed them too closely anyway. The critical part will be capital allocation.

From independent sources (see here , for example) and an occasional Buffett comment, Todd Combs and Ted Weschler are slightly underperforming the market but doing better than Buffett himself (the comment was before the Apple investment multiplied). Can Berkshire benefit by replacing them with the index? The answer is no at least because the duo of investment managers needs non-stop market training to produce the right decisions when big opportunities emerge. These major opportunities do not happen often, perhaps once in several years only. And the related decisions may include either a stock investment or an acquisition (of course, it implies the participation of Mr. Abel and, perhaps, other actors). I do not know if Messrs. Weschler and Combs are capable of making these big decisions like Buffett but Buffett himself seems hopeful.

I would not exclude something particularly new in the post-Buffett era either. For example, I wonder if Berkshire can set up a private equity-like internal group. Let me explain what I mean.

The role model would be Brookfield Infrastructure ( BIP ) ( BIPC ). It differs from other private equity groups in several ways. First, almost all its businesses are of the highest quality, rivaling or, in my opinion, exceeding Berkshire's. Secondly, the group often holds businesses much longer than needed for a quick profitable exit. Thirdly, the group has first-class operational skills. As a result, BIP is more of a strategic player than a buyout outlet.

Being a part of an alt manager, BIP has to exit its investments eventually to return funds with profits to institutional investors. Functioning within Berkshire, such a group would not need to exit investments - Berkshire could keep them indefinitely similar to many other businesses within the conglomerate. Berkshire would be the only capital provider for such a group replacing external investors.

All this is nothing more than my speculations. But Berkshire Hathaway Energy ("BHE") already possesses some elements of this group. However, perhaps due to the temperament of its management, BHE does one deal in several years while BIP does several sizable deals a year.

To the best of my knowledge, Buffett and Munger have never tried to hire or acquire such a group. It may be due to their cultural incompatibility with private equity - I remember Munger mentioning private equity negatively. Or perhaps, such activity appears too risky for Buffett and Munger.

The younger generation of Berkshire leaders may be less conservative. Running BHE for many years, Greg Abel may approach the infrastructure and renewable acquisition opportunities more aggressively.

My third suggestion is to hold BRK in response to IAI as it may overperform the index on an after-tax basis. In the worst-case scenario, underperformance compared to the index should not be significant.

For further details see:

Investment AI, Indexing, Private Equity, And Berkshire Hathaway