LQDB - Investment Grade Positioning And 3 Things To Watch Closely

2023-05-24 10:07:00 ET

Summary

- Corporate bonds offer better opportunities than government bonds, in our view, as central banks wind down their monetary tightening cycles.

- The health of regional banks and the debt ceiling are concerns, but we see selective opportunities in the banking sector and expect the debt ceiling standoff to be resolved.

- We expect the economy to experience a soft landing and believe companies are prepared to manage a slowdown.

By Matt Brill, Head of North American Investment Grade and Todd Schomberg, Senior Portfolio Manager

Fixed income markets have seen some dramatic changes in the past few months. As we make asset allocation decisions, we are especially focused on three things. First, all eyes continue to be on the US Federal Reserve (Fed) to determine when its latest hiking cycle will end. Second, regional banks continue to be a source of concern, with PacWest ( PACW ) and Western Alliance ( WAL ) joining First Horizon ( FHN ) in the latest market volatility. And third, the debt ceiling is becoming a bigger focus, with the possibility that the ceiling will be hit as soon as June 1.

This month, Invesco Portfolio Managers Matt Brill and Todd Schomberg discuss the general trends in the investment grade market and their expectations looking ahead.

Q: You mentioned in last month’s commentary that all eyes remain on the Fed. What are your thoughts on the rest of 2023?

Central bank monetary tightening is coming to an end, and economies are likely headed for a soft landing. In our opinion, corporate bonds offer greater opportunities than government bonds. The deep bond market losses in 2022 were caused by interest rate sensitivity and higher yields, not credit losses or fundamental concerns. Ironically, the global economy was too good! But the magnitude of these losses was much greater than expected.

In terms of future monetary policy, the Fed is trying to walk a fine line. Current economic data are still fairly strong, and inflation has been sticky, so the Fed is in a bind regarding how to handle it. Along with watching the economic data intently, it is no doubt watching recent banking sector stress to see how it impacts the economy going forward. The May hike was likely its final hike.

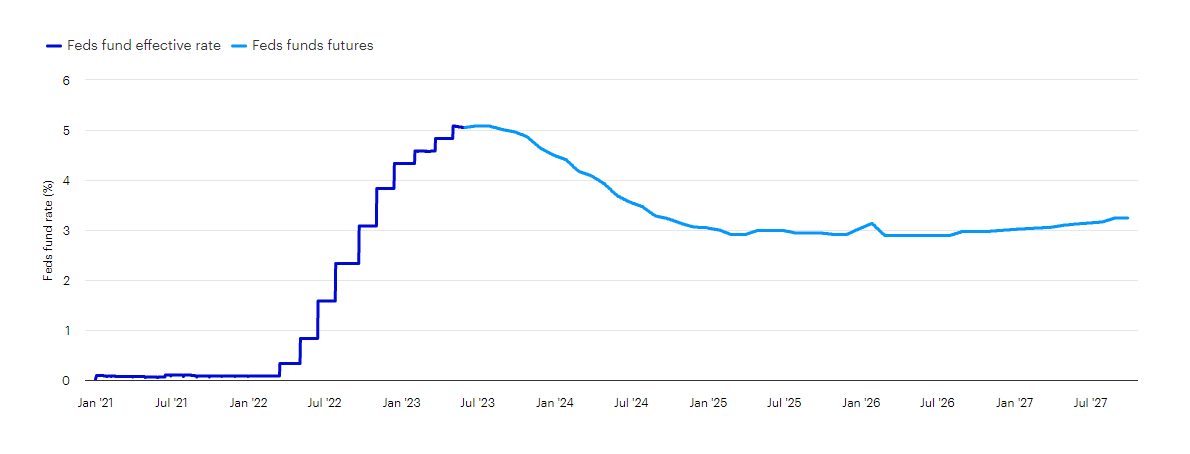

Figure 1: Fed funds effective rate and fed funds futures

{kind=link}

Source: Macrobond. Data as of May 8, 2023

Q: How are you positioning your portfolios to handle the end of the rate-hiking cycle?

We can get high-quality bonds in the 5% range. These yields are attractive, in our view, and may not last too long, because eventually, central banks may start to cut rates. We do not expect to make up for all of 2022’s losses in 2023, but we expect high-single digit returns this year. Most indices within the Bloomberg US Aggregate Bond Index are already up 3% to 4% percent year-to-date, which is a good start 1 . We could see continued good performance in 2024 if we see rate cuts, as we expect.

People have been calling for a recession for 18 months and it’s probably the most anticipated recession in history. We believe the economy will slow down but expect the job market to hold up. And because many companies have been preparing for the worst, we would not expect a recession to blindside them. We would expect them to perform well even if we experience a recession.

If there is a hard landing, we do not expect spreads to widen and markets to fall on the scale of what occurred in 2008-09 or when COVID hit in early 2020. There will likely be pain, but, even in a hard landing scenario, because companies have been preparing, the blow should be mitigated.

We are still generally of the view that a soft landing is possible.

Q: Regional banks have been in the news since early March. How has volatility in the banking sector impacted your outlook?

A few things around the regional banks seem different than in past cycles. First, recent stresses have not been driven by bad loan quality or poor assets, but rather by poor asset-liability management combined with a lack of confidence. We have seen crises of confidence before, but the trigger appears different this time.

In the current situation, restoring confidence will be key, in our view. Quarterly earnings results for regional banks were fairly solid. Most regional banks suffered minimal, if any, outflows from deposits, and loan losses were acceptable. Banks’ earnings and reserves for the future were fairly strong.

But looking forward, the cost for these banks to survive is likely going to be high. Banks will likely focus on shoring up deposits, so staying liquid will likely be costly for them down the road. This isn’t a great equity story, but it's not the worst story from a bondholder perspective if they are able to survive.

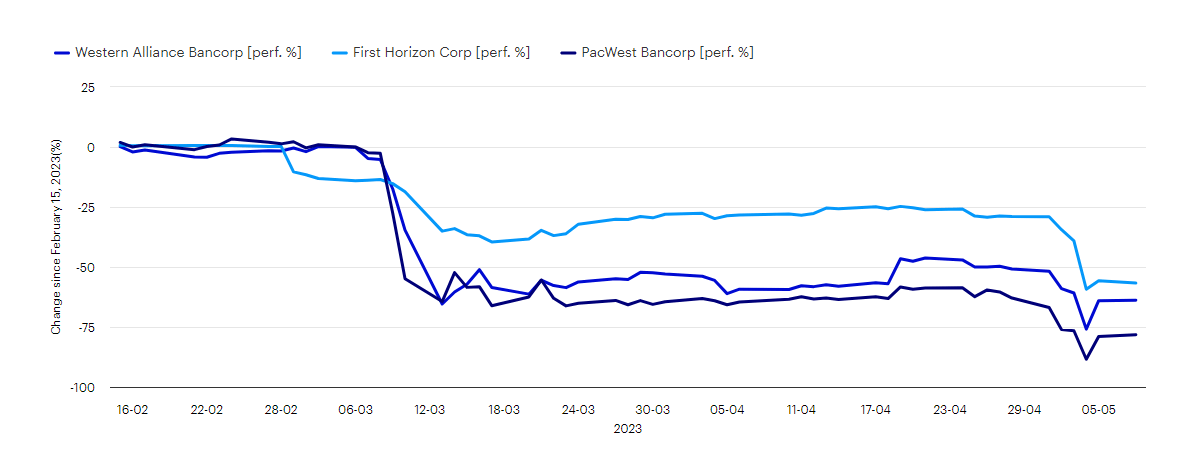

We believe the regional banks will manage through the current situation and that there will be a solution with time. But we may see additional bank failures. First Republic will likely be the largest one, but now we can add PacWest and Western Alliance to the list of banks in the crosshairs.

Figure 2: Hardest-hit regional banks – stock price change since February 15, 2023

{kind=link}

Source: Macrobond, Bloomberg L.P. Data as of May 8, 2023

Once the economy begins to normalize and the yield curve is no longer inverted, we believe banks will be able to lend again and be profitable. If it does appear that spreads could go tighter, we would want to own banks because we would expect them to outperform the market by the largest margin.

Q: Do you have concerns with any of the largest banks?

We are not concerned about the “big six 2 ” banks. We do, of course, favor certain ones over others. But the key thing to point out is that regulatory scrutiny will likely intensify across all banks – especially the regional banks, but even the big banks. That is actually not a bad thing from a debtor standpoint. We want banks to be profitable, but, from a bondholder perspective, the more restraints, the better. Overall, we believe the big six banks are all in good shape and that most of the super-regionals will likely be fine, but we are being extremely choosy.

Q: There has been a lot of news focus on the debt ceiling. What are your concerns?

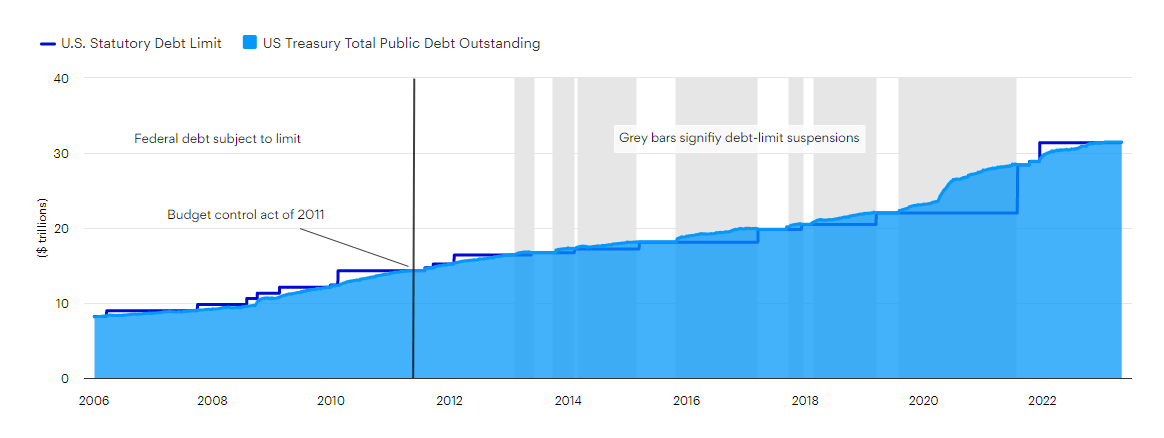

Treasury Secretary Yellen has said that the US could hit the debt ceiling as soon as June 1. Looking back at the 2011 debt ceiling showdown and Standard & Poor’s eventual downgrade of the US, credit spreads widened by nearly 100 basis points in just a few months. 3 Spreads retraced most of that move in only a few months as well, but the volatility was significant.

Most of the spread widening took place after the debt ceiling resolution but also after the downgrade. The downgrade of US debt caused a bigger impact than the debt ceiling problem itself. If the US is downgraded again due to debt ceiling concerns, we would expect credit spreads to widen.

Figure 3: US Treasury total public debt outstanding and the statutory debt limit

{kind=link}

Source: Macrobond, Bloomberg L.P. Data as of May 8, 2023.

Footnotes

1 Source: Bloomberg L.P. Data as of May 4, 2023. US Treasury Index +4.02%, Government-Related Index +4.16%, Corporate Index +3.92%, and Securitized Index +3.50%. The Bloomberg US Aggregate Bond Index, or the Agg, is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. Investors frequently use the index as a stand-in for measuring the performance of the US bond market.

2 Source: The “big six” banks are: Bank of America, Citigroup, Goldman Sachs, JP Morgan, Morgan Stanley, and Wells Fargo.

3 Source: Bloomberg L.P. Bloomberg US Corporate Bond Index Option Adjusted Spread (OAS) to Treasuries. July 29, 2011, +152; October 4, 2011, +250; October 4, 2012, +151. The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility, and financial issuers.

Important information

NA2899993

Header image: Gapikralj / 500px / Getty

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Past performance is not a guarantee of future results.

All investing involves risk, including the risk of loss.

The opinions referenced above are those of the author as of May 12, 2023 . These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

All data as of May 8, 2023, unless otherwise stated. All data is USD, unless otherwise stated.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

This information is intended for US residents.

The information on this site does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional/financial consultant before making any investment decisions.

Invesco Distributors, Inc., is the US distributor for Invesco Ltd.'s Retail Products, Collective Trust Funds and CollegeBound 529.

Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2023 Invesco Ltd. All rights reserved

Investment Grade Positioning And 3 Things To Watch Closely by Invesco US

For further details see:

Investment Grade Positioning And 3 Things To Watch Closely