KHYB - Investment Strategies For Generating Efficient Income

2024-01-05 09:50:00 ET

Summary

- Bond yields are up but secular forces still pose headwinds for inflation-adjusted returns.

- While the power of higher bond yields is certainly a welcome development for income investors, the path forward will likely feature plenty of volatility.

- We think an efficient way to generate income is by carefully assembling mixes of interest-rate and credit building blocks—and incorporating private-market exposure for additional diversification and return potential.

By Brian Resnick, CFA

An Unfriendly Landscape for Income Investors

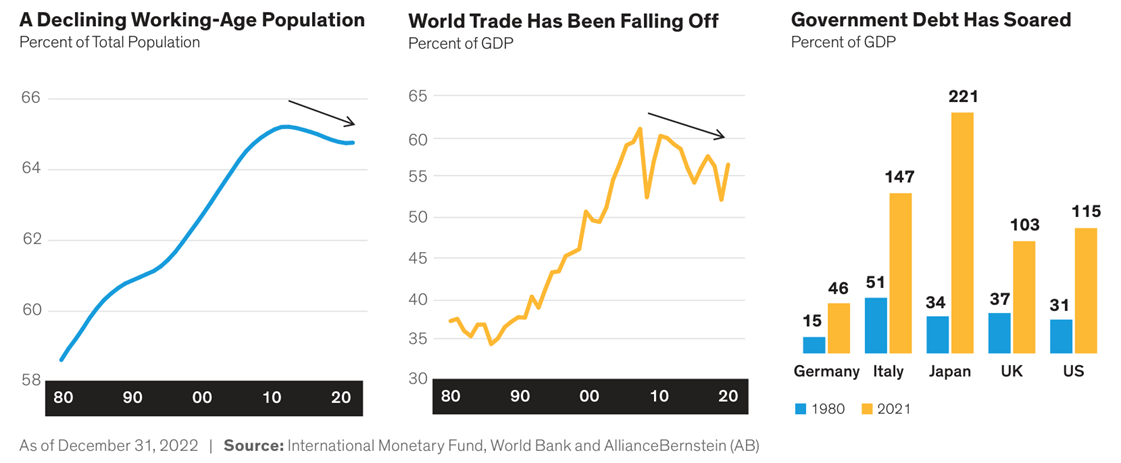

A challenging macro mix is set to make investing a lot more challenging in the years ahead: the share of the world's population that's of working age seems to have peaked.

Growth in world trade, a huge economic tailwind since the mid- 1980s, has flattened. And the global debt burden is nearing 140% of gross domestic product (GDP)-it's well documented that levels above 100% can create economic headwinds.

Collectively, these factors will likely yield lower growth and higher inflation, creating a challenging environment for investors.

Bond Yields Have Come Roaring Back

In the fixed-income world, yields have come a long way from their depths during the COVID-19 pandemic. Back in mid-2020, the 10-year US Treasury yield was only 0.6%, a meager level for income seekers. Then, in early 2022, the Federal Reserve kicked off a sharp cycle of interest-rate hikes in hopes of cooling off red-hot inflation.

By late 2023, the landscape had changed dramatically, with the 10-year Treasury yield well above 4%. While the yield surge inflicted a lot of pain across bond markets, it's also brought renewed energy to traditional core bond strategies and bolstered the income-generating capabilities of sectors from investment- grade corporates to high-yield bonds and emerging-market debt.

Secular Forces Will Challenge Real Returns

While the power of higher bond yields is certainly a welcome development for income investors, the path forward will likely feature plenty of volatility. It will also feature the convergence of three macro headwinds ( Display 1 ) that will pressure inflation- adjusted returns.

First, demographics are changing, with the global working-age population declining. Second, globalization seems to have peaked and pivoted into deglobalization, as evidenced by declining levels of world trade. And third, a growing debt burden is diverting otherwise productive investment in order to cover debt-servicing costs.

Display 1: Macro headwinds-demographics, deglobalization and debt

{kind=link}

Collectively, these three forces are likely to drive economic growth lower and inflation higher, making it harder for investors to generate returns that outpace rising prices. That challenge calls for enhancing yields while bolstering diversification to protect against the inevitable market downturn.

A 2022 Lesson: Don't Get Complacent with Higher Yields

Many investors may be convinced that the higher levels of yield in a traditional core bond portfolio are just the ticket to generate better income. After all, the yield on the Bloomberg US Aggregate Bond Index surged from a meager 1% in mid-2020 to 5.4% by September 2023.

However, one of the lessons from a brutal 2022 was that the traditional notion of portfolio diversification doesn't always work. Granted, it was an uncommon year, with a massive engineered surge in interest rates to stifle growth and cool inflation-not a typical economic cycle. But there's no guarantee that a 2022 couldn't happen again, and even though nominal bond yields are up, so is inflation, so there's a higher hurdle for generating real returns.

How can investors generate high enough income without also facing too much risk?

The key, in our view, is to design portfolios that deliver efficient income-the most income and total return potential for each added unit of risk taken on.

Seen another way, investors should seek to minimize drawdown risk at any income level. The good news? There are plenty of tools to work with.

Efficient Income Building Blocks: Rates and Credit Exposure

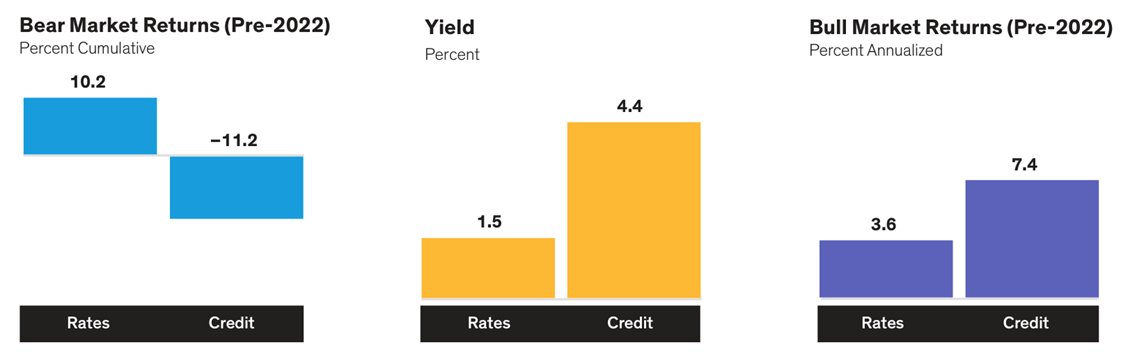

As we see it, the fixed-income universe can be viewed as two distinct asset classes: interest rates, which can be an anchor to windward when risk assets sell off, and credit, a higher-yielding procyclical asset that shines in bull markets.

Both rates and credit play key roles in designing efficient income formulas ( Display 2 ). Rates, represented by US Treasuries, have been an effective counterbalance to declines in risk assets.

Display 2: Fixed income is actually two distinct asset classes

{kind=link}

| Past performance and current analysis do not guarantee future results. Rates yield is calculated using the 10-year US Treasury yield. Rates bull and bear market returns are calculated using the Bloomberg US Intermediate Treasury TR; credit is represented by the ICE BofA US High Yield TR Index . A bear market is defined as a 20% decline or more from peak to trough. Returns are calculated using annualized monthly returns from 1987 through December 2021. As of December 31, 2021 | Source: Bloomberg, ICE Data Indices, Morningstar Direct and AB |

Over the past 20-plus years, they've posted a strong 10.2% annualized return in bear markets when credit, represented by US high yield, declined by 11.2%. In bull markets, on the other hand, higher- yielding credit has easily outpaced rates, by a margin of 7.4% to 3.6%, respectively.

These basic examples help illustrate the value of each income building block. But in practice, there's a lot more investors can do to refine each one-and combine them efficiently to satisfy individual income and risk preferences. Thanks to higher bond yields today, there's more flexibility in those combinations.

Back to Basics: Boost Rate Exposure with Traditional Core Bonds

A healthy allocation to traditional core bonds makes sense now more than ever, with yields at multidecade highs giving investors sizable bang for their buck. The interest-rate exposure of core bonds has historically counterbalanced procyclical risk assets in bear markets.

Going back to the mid-1980s, core bonds have delivered an annualized 9.4% return during periods when equity markets tumbled by 20% or more. The effectiveness of this

counterbalancing is illustrated even more starkly by US Treasuries, the most pure interest-rate segment, which have returned a whopping 13% across those same periods.

The experience of 2022 was a notable exception, as rate exposure inflicted double-digit losses at the same time that credit and equities did. The reason: previous bear markets stemmed from economic slowdowns or recessions, but 2022 was very different. When interest rates rose dramatically from near-zero levels, it revealed a weakness in rates' ability to diversify in times of extreme market stress.

This shortfall highlighted the need to not only diversify across public credit markets but also to identify new sources of income diversification, which we'll cover a bit later.

Embracing Credit Risk-and Managing It Effectively

High-yield bonds are a key cog in the income-generating ability of credit, so it's important to get the design right-and get the most from it over time. Historically, the typical US high-yield strategy has failed to beat a broad high-yield index, quite often because of a common pitfall: not having enough exposure to risk factors that have been rewarded over time, and not managing downside risk.

Just as investors should embrace rate exposure in the rate building block, they should embrace credit risk in the credit building block. And risk should be managed by adapting quality during the credit cycle. That approach translates into favoring higher-quality issuers and reducing beta late in the cycle, while leaning into lower-rated issuers in periods when credit risk has been highly rewarded.

Going Global Expands the Universe and Enhances Return Potential

Investors can make the credit building block even more efficient by diversifying across industries to avoid overconcentration. In 2001 and 2002, a telecom sell-off was a big problem for many investors. In 2008 and 2009, financials were a challenge. In 2016, energy defaults inflicted pain, and in 2020 energy and retail struggled. Industry diversification matters, as does kicking the tires on issuer fundamentals.

Broadening credit exposure to embrace a global, multi-sector approach could also enhance portfolios by incorporating income generators worldwide. The US high-yield market has roughly US$1.7 trillion in assets. Casting a wider net to include global high yield, emerging-market debt, securitized assets and bank loans can expand the opportunity set to about US$7.3 trillion. That's a lot of credit opportunities to choose from.

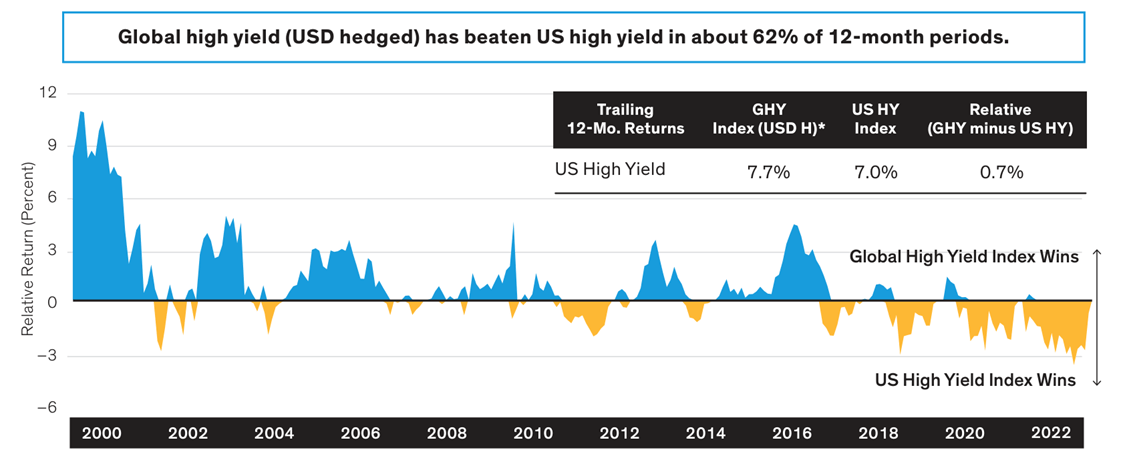

Historically speaking, even a naive passive allocation to global high yield has outpaced US high-yield corporates by about 0.7% annualized, winning in about 62% of one-year periods ( Display 3, page 4 ). Multi-sector credit may also enhance diversification and improve risk-adjusted returns while creating a bigger playing field for active managers to generate alpha. In our view, that's a winning formula for the credit building block, because no one sector wins all the time.

Display 3: Globalizing credit exposure can boost alpha

12-Month Trailing Relative Return of Global High Yield (USD Hedged) vs. US Corporate High Yield

{kind=link}

| Past performance does not guarantee future results. GHY: global high yield; HY: high yield *Global High Yield Index (USD Hedged) is represented by the Bloomberg Global High Yield Index (USD Hedged); US High Yield Index is represented by the Bloomberg US Corporate High Yield Index. From January 1, 2000, through December 31, 2022 Source: Bloomberg, Morningstar Direct and AB |

Balancing Rates and Credit Exposures

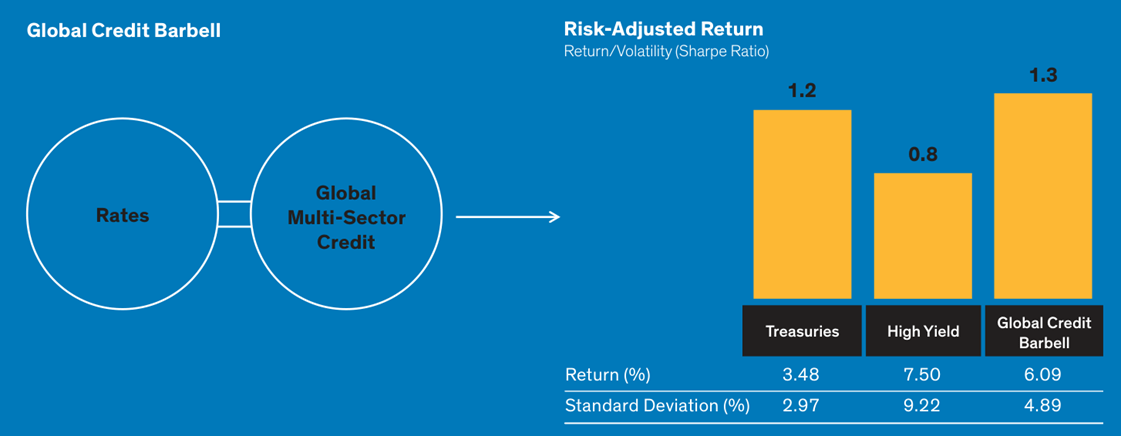

Making the rates and credit building blocks more efficient in themselves may also make them more efficient in combinations such as a "barbell" structure ( Display 4, page 5, left ) that balances high-yielding global multi-sector bonds with high-quality core bonds-bolstered with US Treasuries. Even a simple barbell combination like this, with equal assets budgeted to rates and credit, has been an efficient mix.

We can see this through the Sharpe ratio, a popular measure of the return generated for each unit of risk investors take ( Display 4, page 5, right ). Over the past two decades, the Sharpe ratio for US Treasuries, a basic proxy for the rates building block, has been 1.2. A simple credit allocation to US high yield has produced a Sharpe ratio of 0.8. A global credit barbell has bested both of those building blocks-a Sharpe ratio of 1.3, with returns closer to high yield than to Treasuries and less risk than high yield.

Historically, the global credit/rates barbell has delivered a high level of income to investors efficiently, taking the least amount of risk for each unit of income while reducing downside risk.

Display 4: Rethinking bonds-the rates and diversified credit "barbell"

{kind=link}

| Past performance does not guarantee future results. Treasuries represented by Bloomberg US Intermediate Treasury TR. High yield is represented by the ICE BofA US High Yield Index. Global credit barbell represented by 50% Bloomberg Global High Yield (USD Hedged), 25% Bloomberg US Intermediate Treasury, 25% Bloomberg US Aggregate Bond TR Calculations from January 1, 2001, through December 31, 2021 Source: Bloomberg, ICE Data Indices, Morningstar and AB |

The global credit/rates barbell has delivered a high level of income to investors efficiently, taking the least amount of risk for each unit of income while reducing downside risk.

Another Income Building Block: Private Credit

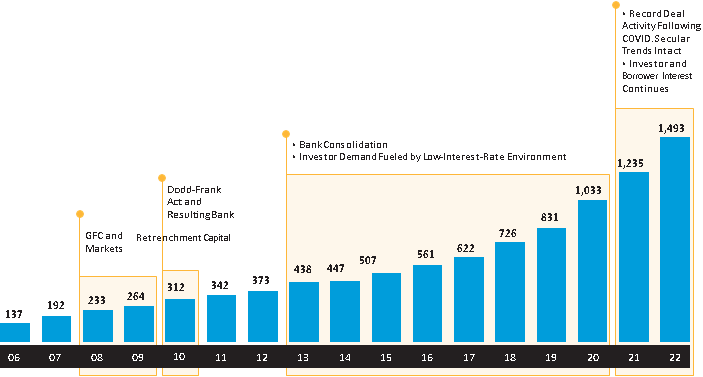

Given the uncommon experience of 2022, with both rates and credit building blocks suffering steep declines, it's important to diversify income strategies even further. Private credit, in our view, offers this potential. This market has grown steadily since the global financial crisis ( GFC ) ( Display 5 ), the worst economic crisis since the Great Depression of 1929. As banks retreated from lending activities, alternative lenders stepped in to provide capital to firms in areas such as direct lending, clean energy and specialty finance.

Display 5: significant post-GFC growth in private credit

Private Debt Assets Under Management (USD Billions)

{kind=link}

| For illustrative purposes only. There can be no assurances that any strategy or investment objective will be met with comparable conditions, or that any investment objectives will be achieved. |

The market grew even faster starting in the mid-2010s, as investors became more broadly aware of this diverse arena's appeal. Private lenders have more influence over deal terms, including loan covenants and business milestones, giving these loans structural advantages over the more uniform public markets. And because private credit is an illiquid asset class, it carries an added yield premium, resulting in generally higher absolute and risk-adjusted yields. That can be a helpful attribute when income investors are seeking to combat low inflation-adjusted yields.

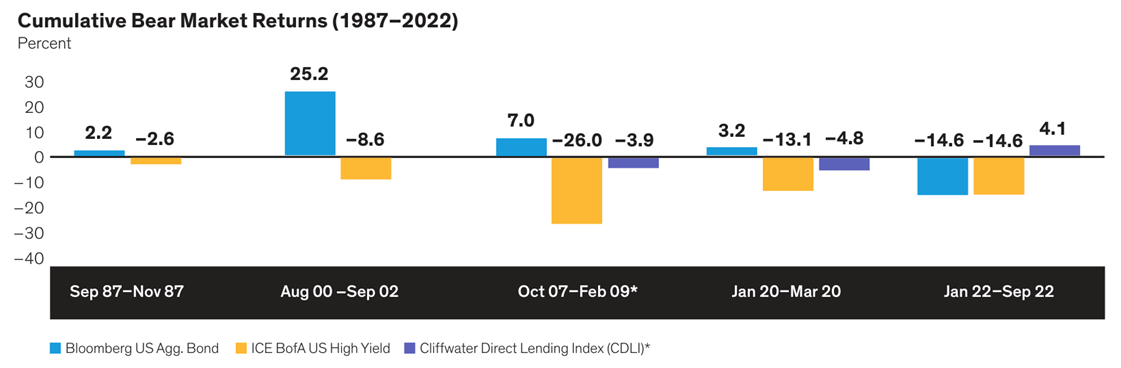

By bringing more asset types, and even a consumer-credit dimension, into the income mix, private credit may enhance returns in strong markets and provide diversification that may serve as a cushion in down markets. The value of that last trait was visible in recent bear markets, with private credit consistently outpacing public credit ( Display 6 ). And in a punishing 2022 for both rates and public credit, private credit posted a positive return.

Display 6: Private credit has been resilient in bear markets

{kind=link}

| Past performance does not guarantee future results. *CDLI calculated over nearest quarterly return As of December 31, 2022 | Source: Morningstar and AB |

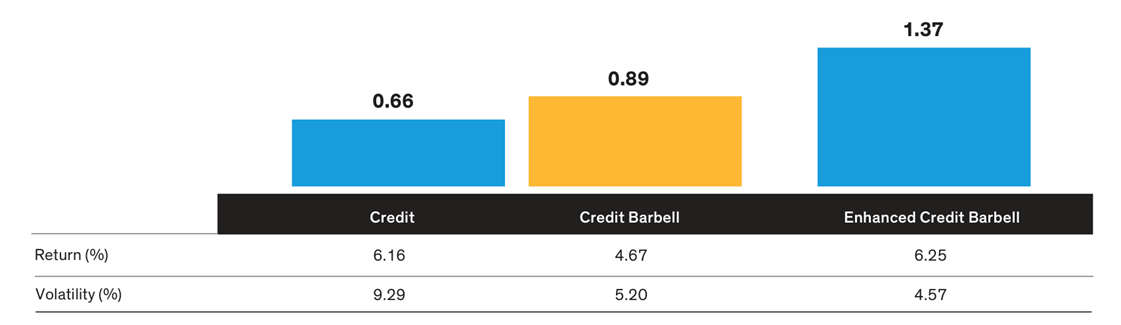

We think this track record makes rethinking fixed income-again- by adding private credit a compelling proposition ( Display 7 ). Since 2004, an enhanced US credit barbell has produced a return to volatility ratio of 1.37, meaning a 1.37% return for every 1% of risk taken. That's even better than the 0.89 ratio of a traditional rates/ credit barbell.

Display 7: Rethinking fixed income…again

Risk-Adjusted Return Ratio (Return/Volatility)

{kind=link}

| Past performance does not guarantee future results. Credit represented by ICE BofA US High Yield Index. Credit barbell represented by 50% Bloomberg Global High Yield (USD Hedged), 25% Bloomberg US Intermediate Treasury, 25% Bloomberg US Aggregate Bond Total Return; enhanced credit barbell represented by 66.7% credit barbell, 33.3% CDLI Returns calculated from September 30, 2004, through June 30, 2023 Source: Bloomberg, Cliffwater, ICE Data Indices, Morningstar and AB |

Of course, investors considering exposure to private credit should carefully assess their tolerance for illiquid assets. As we see it, the delineation isn't really public versus private markets, because some parts of the public markets are illiquid too. Instead, it helps to consider the future barbell pillars as rates, public liquid credit, and private and illiquid credit. Fortunately for investors, certain investment vehicles are democratizing access to illiquid assets, opening new avenues of income potential and diversification.

Looking at the Big Picture

Income investors face a unique challenge in today's landscape. Yields are higher than they've been in a long time, but a trio of macro forces-demographics, deglobalization and debt-will likely depress growth and leave equilibrium inflation higher. That mix will put pressure on real returns, leaving a sticky problem to solve: how can investors boost income without over-risking?

Traditional core bonds continue to provide all-important high-quality interest-rate exposure, but to help offset higher long-run inflation, more diversification is needed. Balancing core rate exposure with higher-yielding globally diversified credit in a barbell structure can generate income more efficiently, and introducing a private-credit dimension may further enhance the mix.

This income approach, which taps both liquid and illiquid credit- may be able to deliver more income while also offering added downside mitigation during the inevitable challenging markets- including the uncommon experience of 2022. This approach also has the flexibility to tap income potential throughout the credit cycle-wherever opportunities might be.

Past performance does not guarantee future results. There can be no assurance that any investment objectives will be achieved.

A word about risk

Interest-Rate Risk: Fixed-income securities may lose value if interest rates rise or fall-long-term securities tend to rise and fall more than short-term securities. The values of mortgage-related and asset-backed securities are particularly sensitive to changes in interest rates due to prepayment risk. Credit Risk: A bond's credit rating reflects the

issuer's ability to make timely payments of interest or principal-the lower the rating, the higher the risk of default. If the issuer's financial strength deteriorates, the issuer's rating may be lowered and the bond's value may decline. Inflation Risk: Prices for goods and services tend to rise over time, which may erode the purchasing power of investments.

Municipal Market Risk: Debt securities issued by state or local governments may be subject to special political, legal, economic and market factors that can have a significant effect on the portfolio's yield or value. Fixed-Income Risk: Investments in fixed-income securities are subject to interest-rate risk-the fluctuation of the interest rate, and credit risk-the issuer's ability to make timely payments of interest or principal. The lower the credit rating, the higher the risk of default. Fixed-income securities with lower ratings (commonly known as "junk bonds") tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

Index examples are presented to illustrate the application of our investment philosophy and are used for comparison purposes only. An investor cannot invest directly in an index.

AllianceBernstein Investments, Inc. ('ABI') is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the manager of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

© 2023 AllianceBernstein L.P., 501 Commerce St., Nashville, TN 37203

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Investment Strategies For Generating Efficient Income