IWM - Investors Ignore A Deeply Inverted Yield Curve At Their Peril

2023-07-13 14:41:48 ET

Summary

- Equities rallied on a better-than-expected CPI report Wednesday and the lowest rise in inflation in some 27 months.

- However, the Federal Reserve is still likely to raise rates again later this month, and the yield curve remains deeply inverted.

- Calm has prevailed in the markets since shortly after three of the biggest bank failures in history a few months ago.

- However, volatility seems overdue to return to the markets.

- How I am positioning my portfolio as a "hard landing" still remains a likely scenario in the quarters ahead is outlined below.

The hawk plays with the pigeon and the pigeon is happy, but not knowing that it is playing with death .”? Amos Tutuola.

I feel like I am starting to sound like a broken record by stating I am extremely cautious around the markets right now. I know that yesterday's CPI report came in a bit lower than expected. The headline reading was of a 3% year-over-year rise in inflation. This was the smallest year-over-year gain in prices in 27 months. " Core inflation" did fall a half a percent from May’s level, but it is still running at 4.8%, significantly above the Fed’s target rate of two percent. This was enough to set off a decent rally in equities in trading Wednesday. For the day, the NASDAQ (COMP.IND) rose one and a quarter percent the S&P 500 (SP500) gained three quarters of one percent, while the Dow (DJI) managed a meager rise of a quarter of a percent.

The current yield curve is one of my top concerns about the market and, or more importantly, the economy. Almost everything on the yield curve is currently inverted. The three-month Treasury yields (US3M) is just over 5.2%, the two year (US2Y) goes for just under five percent and the 10-Year Treasury yield (US10Y) sits at just 3.82% as we sit now

This sort of inverted yield curve holds several negative ramifications for the market. Starting with, this is the first time since the worst of the 2008/2009 Financial Crisis that investors are not confronted with a TINA (There Is No Alternative) market. Excess cash can garner better than five percent rates in short term treasuries. This should hurt the demand for equities, especially if volatility returns to the markets.

Second, historically, an inverted yield curve is a solid sign that a potential recession is on the horizon. Given the current extent of the inversion, I am in the same camp that legendary fund manager Stanley Druckenmiller is right now. This is that a " hard landing " lies ahead and that the economy will be in recession within a year, if not sooner. This reality at some point should trigger a significant selloff in stocks.

Investors continue to get conflicting economic signals on a weekly basis. The manufacturing part of the economy is in contractionary territory, both here and in Europe. The larger services part of the economy is in expansion territory, at least for the time being. However, there are solid signs that harder economic days lie ahead. The June BLS Jobs report last Friday showed the smallest number of jobs created since the country was coming out from under the pandemic lock-downs in the first half of 2020. Here is what the Chief Economist at Raymond James had to say about that jobs report.

This jobs report harbored the first indicator that the U.S. will slow down a lot, and by our forecast enter a recession, in the second half of 2023. "

In addition, the Leading Economic Indicators have fallen for 15 straight months now. The inverted yield curve will also continue to pressure the " hold to maturity" bond portfolios of regional banks. It was the " unrealized losses" on these bond portfolios that helped trigger the events that led to the collapse of Silicon Valley, Signature and First Republic Banks earlier this year. These were three of the top four bank failures by deposit totals in U.S. history, something investors seem to have put in the rearview mirror prematurely over the last couple of months.

In addition, regional banks are facing a potential commercial real estate debacle thanks to rising rates, as this part of the banking system accounts for approximately 70% of loans to the CRE space. There are some $1.5 trillion worth of commercial real estate loans that need to be rolled over during the next few years. This includes some $500 billion on beleaguered office properties. Office vacancy rates have hit all-time highs in Los Angeles and San Francisco and sit around 20% in New York City and D.C. as well. Plunging asset values and refinancing rates will be much higher than the ZIRP glory days, will make rolling over debt a very painful exercise. Like recently with the two largest hotels (by key count) and the biggest mall in San Francisco, more and more property owners will end up " turning in the keys" to lenders. This will put further pressure on asset values and increase losses for the regional banking system.

The delinquency rate for commercial backed mortgage securities hit 4.5% in June, according to Trepp, up substantially from just 1.6% at the beginning of the year. I expect the delinquency rate to at least double from here, before the problems in commercial real estate crest. This will lead to much higher write-offs at regional banks and more stringent credit criteria for their other customers, aka a " credit crunch," which should be particularly impactful on small business.

2024 should be one ugly year for the CRE space. As one of my friends that works at a boutique real estate company recently quipped, his firm has adopted a " Survive Until 2025" motto in recent months.

As noted previously, an inverted yield curve has historically portended a high chance of recession on the horizon. I believe it is no different this time around, and the 500 bps the Federal Reserve has hiked Fed Funds rates since March of 2022 will result in an economic contraction. This should mean significantly lower equity values over the next few quarters.

My portfolio is positioned accordingly. Approximately half of my portfolio is currently in short-term treasuries yielding north of five percent, and another five percent is in cash. The roughly 40% allocation in my long positions are almost all within covered call holdings to mitigate downside. I also have a small but growing percentage of my portfolio targeting overvalued equities like Apple ( AAPL ) via just out of the money bear put spreads , which I detailed in this recent article .

{kind=link}

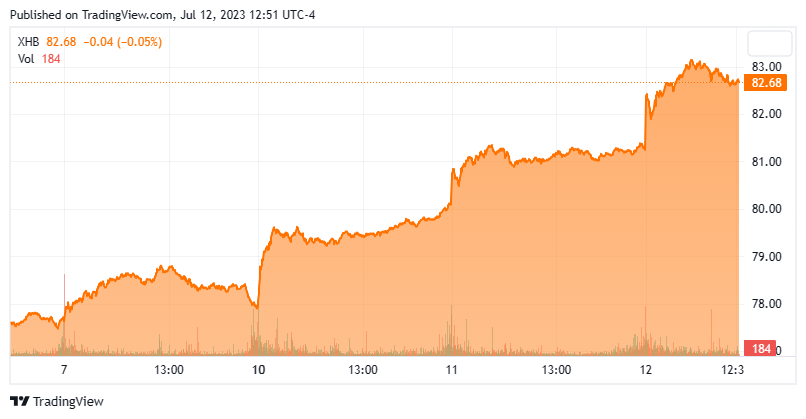

Yesterday I started a new short position via this type of bear put spreads in the SPDR® S&P Homebuilders ETF ( XHB ) which is up some 35% in 2023 despite an increasingly challenged housing sector as average mortgage rates approach seven percent and housing affordability is near historical lows.

In conclusion, it definitely feels discretion is the better part of valor with the market at current trading levels. Investors should position themselves accordingly.

Desperation is the road to depravity .”? Abigail Owen.

For further details see:

Investors Ignore A Deeply Inverted Yield Curve At Their Peril