IONQ - Ionq: No Scaling Out Of A Unprofitability Problem

2023-10-18 08:30:00 ET

Summary

- Ionq's technology cannot scale fast enough to keep up with growing costs, leading to doubts about its profitability.

- Quantum computing hardware is currently limited by high error rates and lacks the breakthroughs needed to overcome these challenges.

- Ionq's financials are dominated by R&D expenditures and investment income, with little real revenue from services rendered.

- Ionq cannot scale their way off this problem; expect linear growth in revenue and quantum computing systems, not exponential growth.

I believe that Ionq (IONQ) is a strong sell - their technology cannot scale faster enough to keep up with growing costs, and there is no clear path to profitability. I will outline first the technical challenges facing the company, and then focus on the financials of the company in the latter half of my report.

The Laws of Physics: Scaling is Hard!

To begin with, quantum computing hardware currently is in the "noisy intermediate-scale quantum" (NISQ) computing regime ( as defined by John Preskill in 2018 ), with ? 100 qubits and no complete error-correction schemes. Unless the problem of high error rates can be overcome, NISQ devices will not be able to scale to tackle useful problems that are not solvable by classical computers. Ionq has not been able to bring a profitable product to market via their "quantum-computing as a service" (QCaaS), and their financials are dominated by large R&D expenditures and investment income, not real revenue from services rendered. Let's dive in.

Tackling noise is a core challenge of scaling quantum computing, as error correction is necessary to carry out complex quantum algorithms. This challenge defines the current NISQ paradigm for all of the current quantum computing players. Despite the pomp and circumstance around public announcements of recent quantum computing efforts by Ionq and its peers Rigetti, Google, Microsoft, the trend in peer-reviewed journal articles in the field is steady improvements, but not the breakthroughs required to overcome the NISQ paradigm. For example, in 2020, Google highlighted that tackling complicated simulations in quantum chemistry is not achievable with their 12-qubit system ( source ).

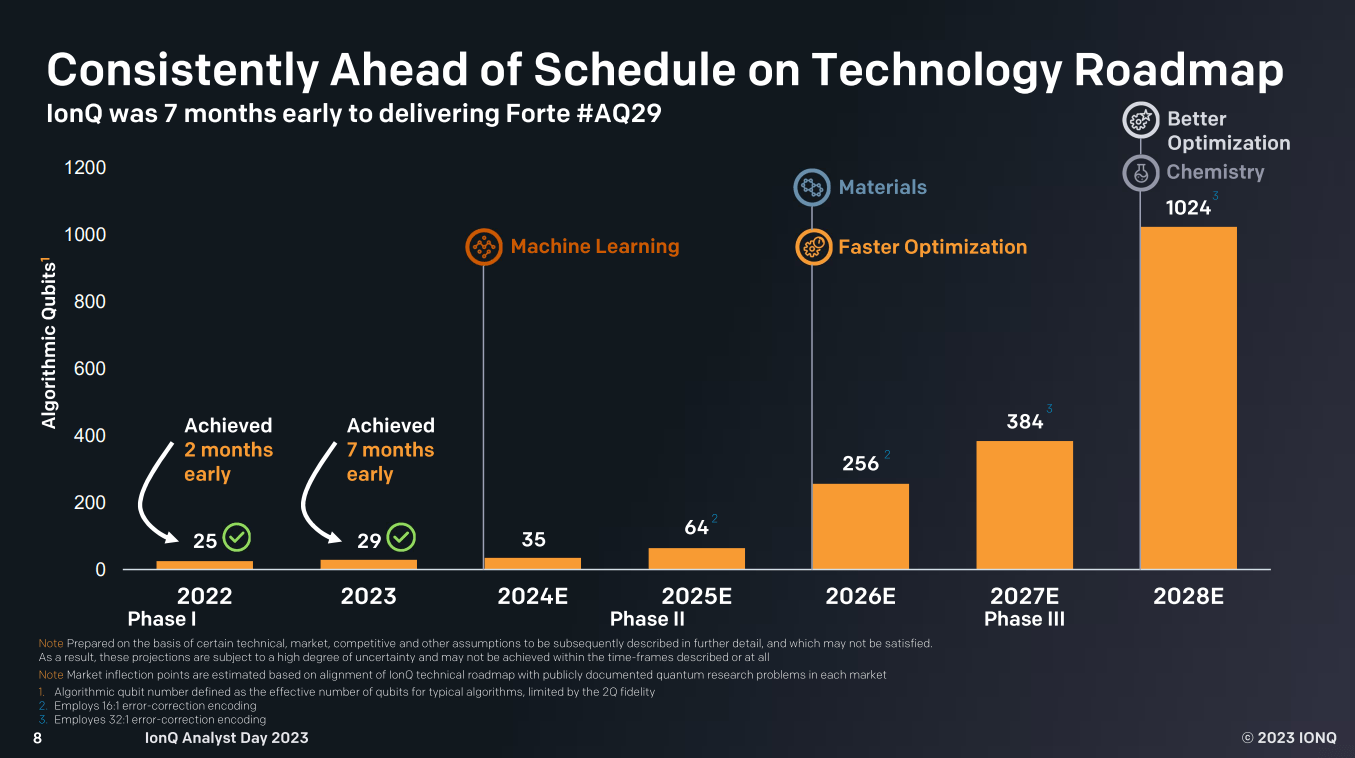

Ionq's pathway to increasing qubit count (Ionq Analyst Day 2023)

{kind=link}

Key to all quantum computing companies is the need to scale the number of qubits, enabling more error-correction and more complicated algorithms. Ionq uses the language of "algorithmic qubits" ((AQ)) as their figure of merit for their qubit numbers. From Ionq's 2023 Investor Day, their current roadmap outlines their goal of reaching a 29-AQ system in 2023, and their expected qubit count going out to 2028. Despite their rosy projection of exponential growth over the next five years, it is important to have a basic understanding of the difficulties of scaling qubit counts for Ionq's trapped ion technology. Currently, the ion traps utilize a 1D geometry, with all the qubits in a row. Scaling to 64 or 256 qubits would require a more complicated design, either using a longer 1D chains, some kind of 2D array or a photonic interconnect ( see this review article on challenges in trapped-ion computing from 2019 ). However, these methods have not been proven experimentally at the scale that Ionq wants to roll out in their commercial quantum computers.

Sandia National Lab's new ion trap, dubbed the "Enchilada Trap". (Sandia National Lab)

{kind=link}

Technical issues aside, Ionq is unlikely to achieve exponential qubit scaling due to the complexity of ion-trap fabrication. While Ionq uses a chip-scale ion trap, these are complicated devices that are extremely difficult to fabricate; Sandia recently announced the development of a new ion trap supporting up to 200 qubits ( source ), requiring complex lithography and nanofabrication techniques. Until the technology matures to the point where the scalability of the semiconductor industry can be utilized, the expense in time and manpower will relegate Ionq's qubit count growth to the linear regime, not the exponential trend that their leadership hopes for. This has a large impact on the financials and highlights the company's inability to scale itself up to profitability.

The Financials: Plenty of R&D Spending, but No Product Growth?

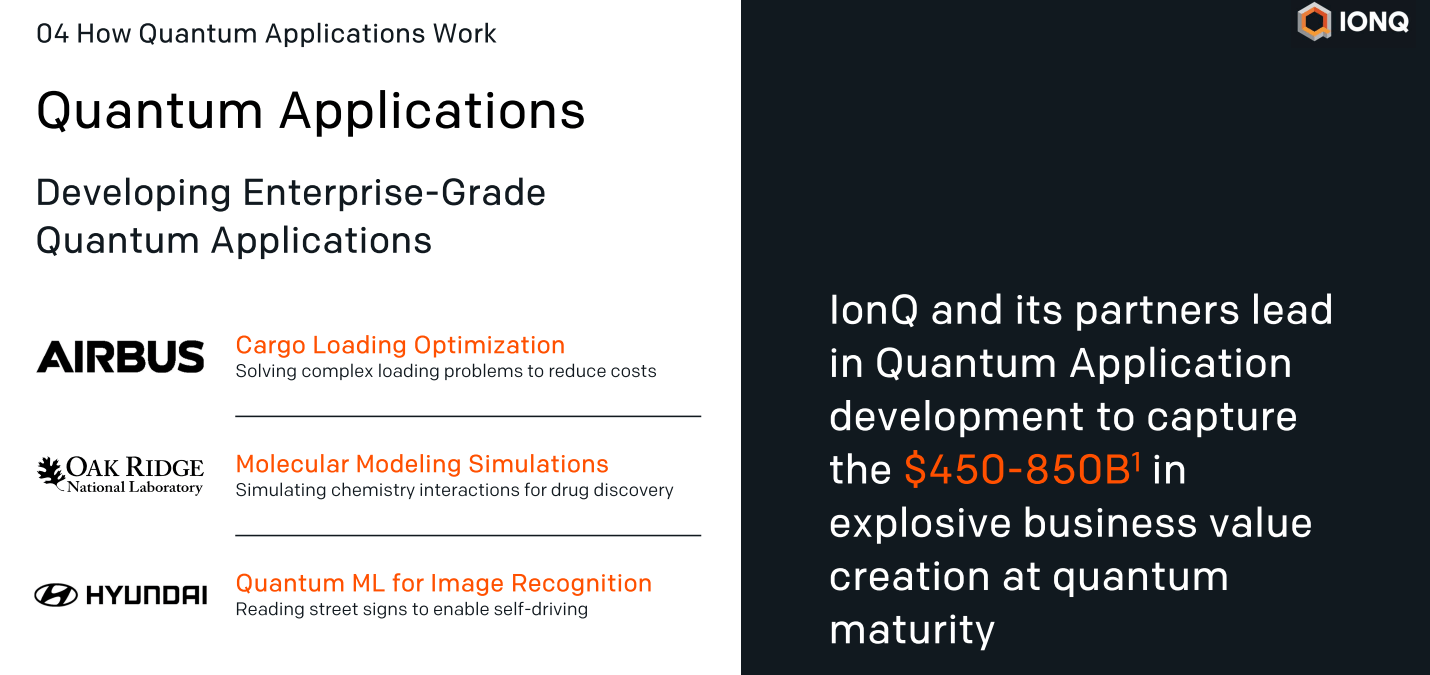

Now, let us shift gears and take a deeper look at the financials of Ionq. Their three customer profiles are government, commercial or academic, with revenue from deals and partnerships broken down between access agreements (based on fixed-amounts), service period-based, usage-based or completion-based. Ionq advertises its systems for tackling complex problems, such as solving logistics optimizations, finding new drugs, and advancing "quantum machine learning. However, there is no market for quantum applications that cannot be solved via classical computing methods. A recent paper by IBM in 2023 on their 127 qubit processor ( source ) claimed to have "demonstrated [a] realization of near-term quantum applications"; however, within a few weeks, researchers at the Flatiron Institute and Caltech released pre-print journal articles highlighting the same result achieved with classical computers ( source ).

Ionq's enterprise customers (Ionq Aug 2023 Quarterly Report)

{kind=link}

The Fine Print: 10-Q Details

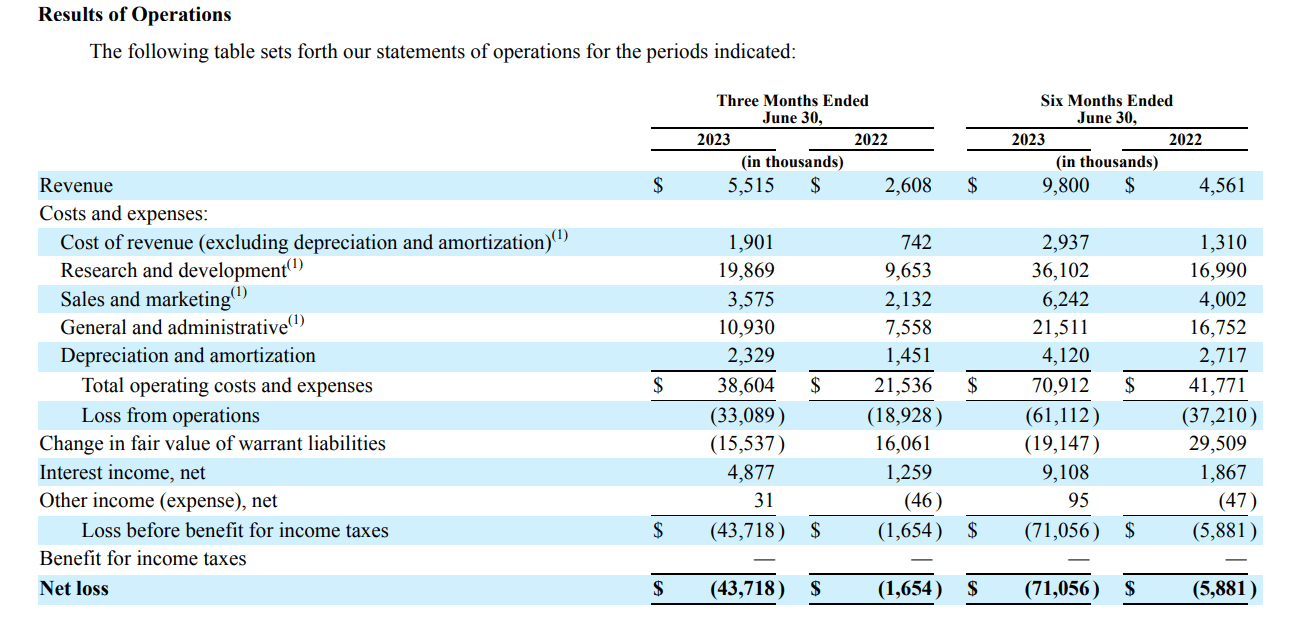

Ionq's first half of 2023 revenue and costs, resulting in a net loss (Ionq Q2 2023 10-Q)

{kind=link}

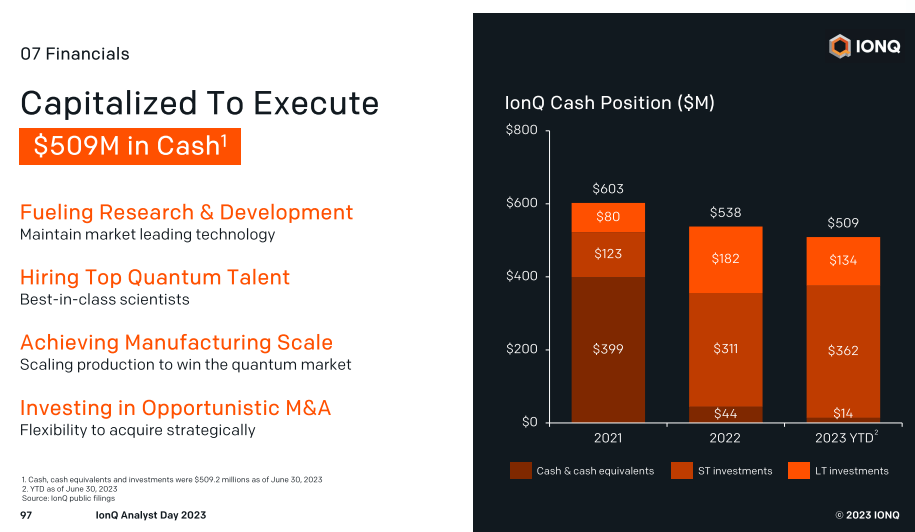

The current state of applications notwithstanding, Ionq continues to highlight its growing customer base to support its claim for exponential growth. However, the financials as filed in their most recent 10-Q report show otherwise. Ionq realized $5.5M of revenue from the first half of 2023, dwarfed by the R&D spending and additional costs in bringing up sites in Washington and Basel. Interestingly, the interest income generated by the cash and other assets held by the company is only slightly less than the revenue generated by Ionq's QCaaS obligations. Digging into this further, we find that the company has shifted away from cash and cash equivalents into various short/long-term investments.

Ionq's Cash Reserves - note the shift into short/long-term investments (Analyst Day 2023)

{kind=link}

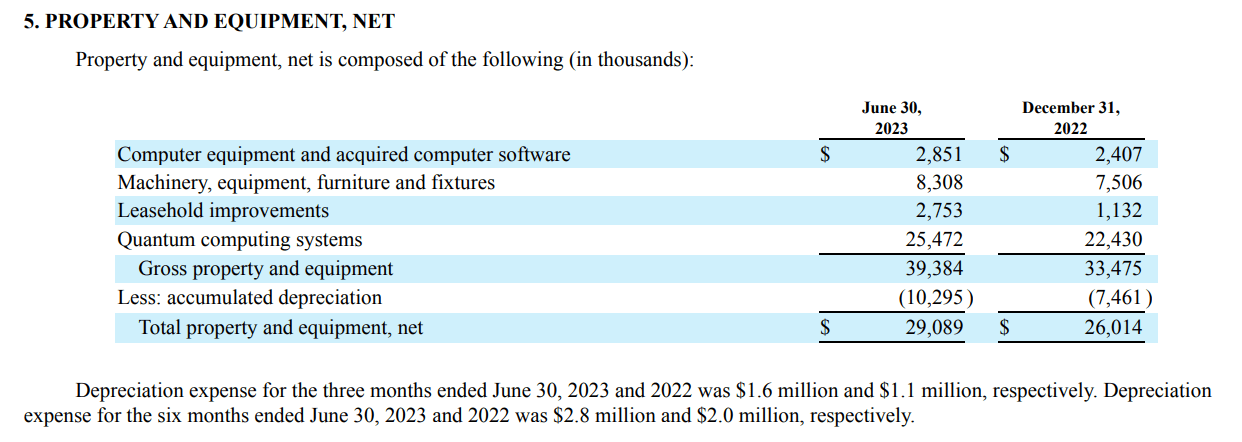

Additionally, for a company touting exponential growth, their most recent 10-Q filing reveals that the growth in physical quantum computing systems as measured by their property and equipment filing has only grown about 10% over the last 6 months. While this would be a significant build-up for any company, this highlights the growing discrepancy between the growth that the company is advertising and the ground truth,

Property holdings for Ionq (Ionq Q2 2023 10-Q)

{kind=link}

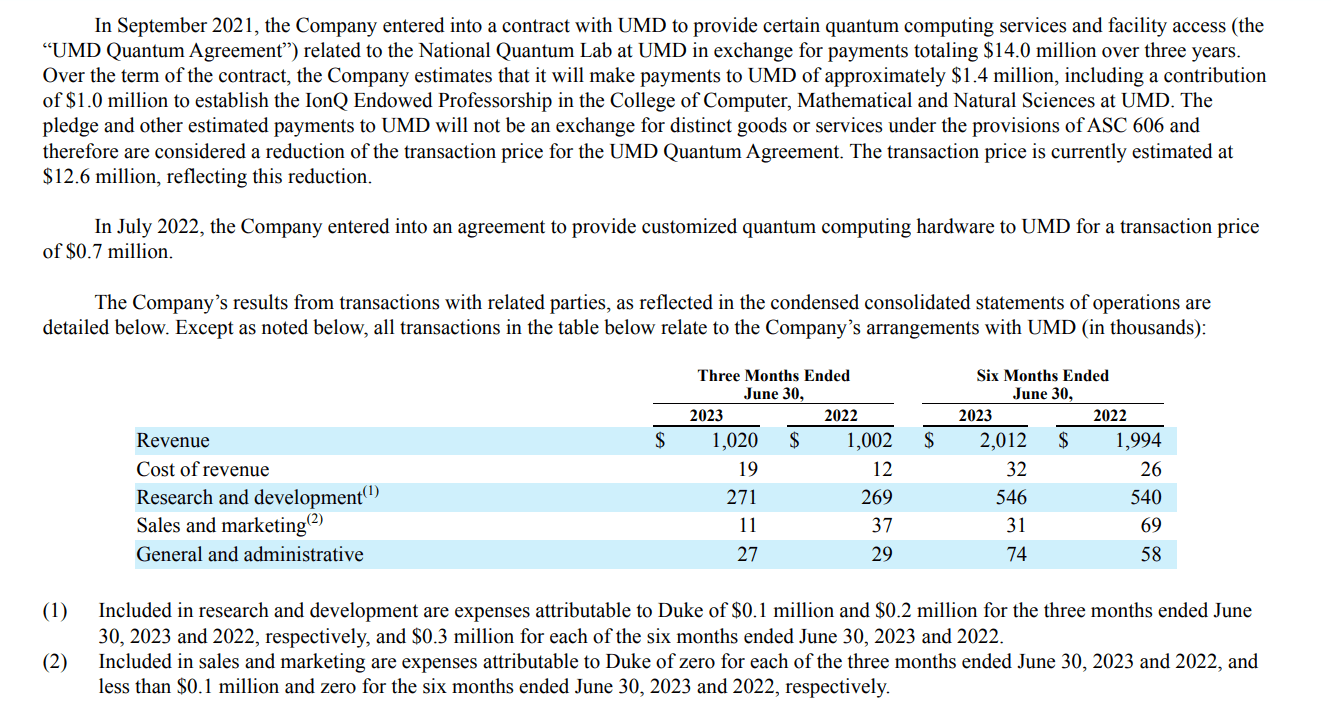

So where does the bulk of their revenue from? Although Ionq does not give us a breakdown of their revenue streams by sector, if we assume each of the mentioned customers (Airbus, Hyundai, and Oak Ridge National Lab) all have a similar contract for around $1M quarterly, the remainder of the revenue can be explained by Ionq's ongoing partnership with UMD. This deal nets Ionq $12.6M over three years by providing quantum computing services and facility access to the university. This represents a significant portion of the operating revenue generated by the company.

Breakdown of Ionq's deal with UMD, generating a large fraction of their revenue (Ionq Q2 2023 10-Q)

{kind=link}

Risks and Valuation

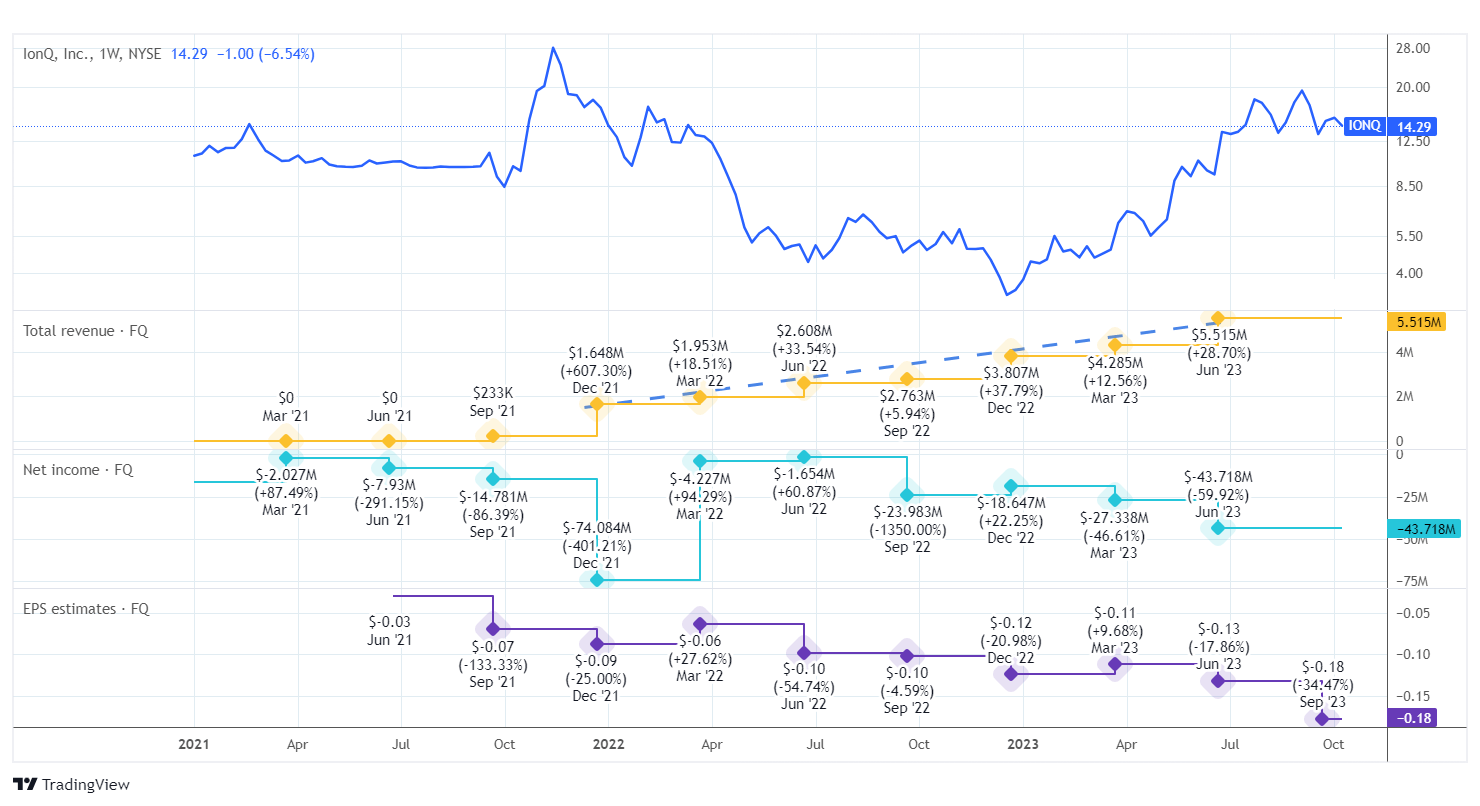

Ionq's stock price with revenue, income and EPS for the last two years (TradingView)

{kind=link}

It is important to remember the adage that "the market can stay irrational longer than I can stay solvent" when taking a contrarian position. Ionq has done an excellent job shoring up support from large industrial customers with deep pockets and lofty promises. I am not alone in sharing the sentiment that the company has little in the way of a real product or a pathway to profitability. From the price chart with quarterly revenue, income and EPS metrics, we can see that the company's stock price has little connection with its current financials. The valuation appears to be correlated with the revenues coming in, but as alluded to previously, the revenue seems to be detached from actual services rendered and more likely due to fixed-revenue access agreements. With a surprisingly low growth in inventoried quantum computing systems, it appears that the revenue growth will only remain most modest on a QoQ or YoY basis. If the current linear trend continues, I would expect revenues to reach $6.7M by the end of FY 2023. However, with R&D spending greater than the revenue by a factor of 3-4 on a quarter basis, linear growth in revenue will not be sufficient to reach profitability. As the company tries to scale production and continues to hire more talent to push the boundaries of what is possible, I expect the net losses to continue to mount.

Conclusion

In conclusion, I believe Ionq went public too early without a viable product or pathway to profitability. While the promise of quantum computing is extremely appealing and continues to drive the rapid pace of R&D in the field, Ionq continues to suffer the same technological barriers as its peers. Addressing scaling challenges for trapped-ion quantum computing will remain a costly and time-intensive process, and the scaling processes are likely going to be more linear than exponential. Based on this combination of factors, I believe that Ionq is a strong sell; it does not matter how cutting-edge the technology is if the company cannot generate a profit now or in the future.

For further details see:

Ionq: No Scaling Out Of A Unprofitability Problem