IPX - IperionX: Promising Potential But It's Still Early Days

2023-09-11 10:09:04 ET

Summary

- Titanium producer IperionX has done decently in the stock market, with a 23% price rise since its listing in June 2022. It's still pre-production but holds much promise.

- With its innovative processes, it sees lower production costs and reduced carbon emissions associated with titanium production. Titanium has lagged aluminum and steel in usage for these reasons.

- If the company is able to achieve lower cost production, I believe there's a significant market opportunity for it. But for now, it's better to wait until it becomes fully operational.

Titanium producer IperionX ( IPX ), which has been publicly listed since June 2022, has had a decent run in the stock market, with a 23% price rise since listing. It might not be runaway growth, but I think there’s something to be said for its relative stability, especially as a pre-revenue company. Its Beta value of 0.69 since listing is a quantitative reflection of this aspect.

This is a good place to start, in my view. But there’s a whole lot more to unpack in the IperionX story to assess whether it’s a good buy for investors right now or not.

The market opportunity

IperionX sees an opportunity to lower production costs and reduce carbon emissions associated with titanium, which have held it back despite its notable superiority to other industrial metals like steel and aluminum in terms of strength and weight.

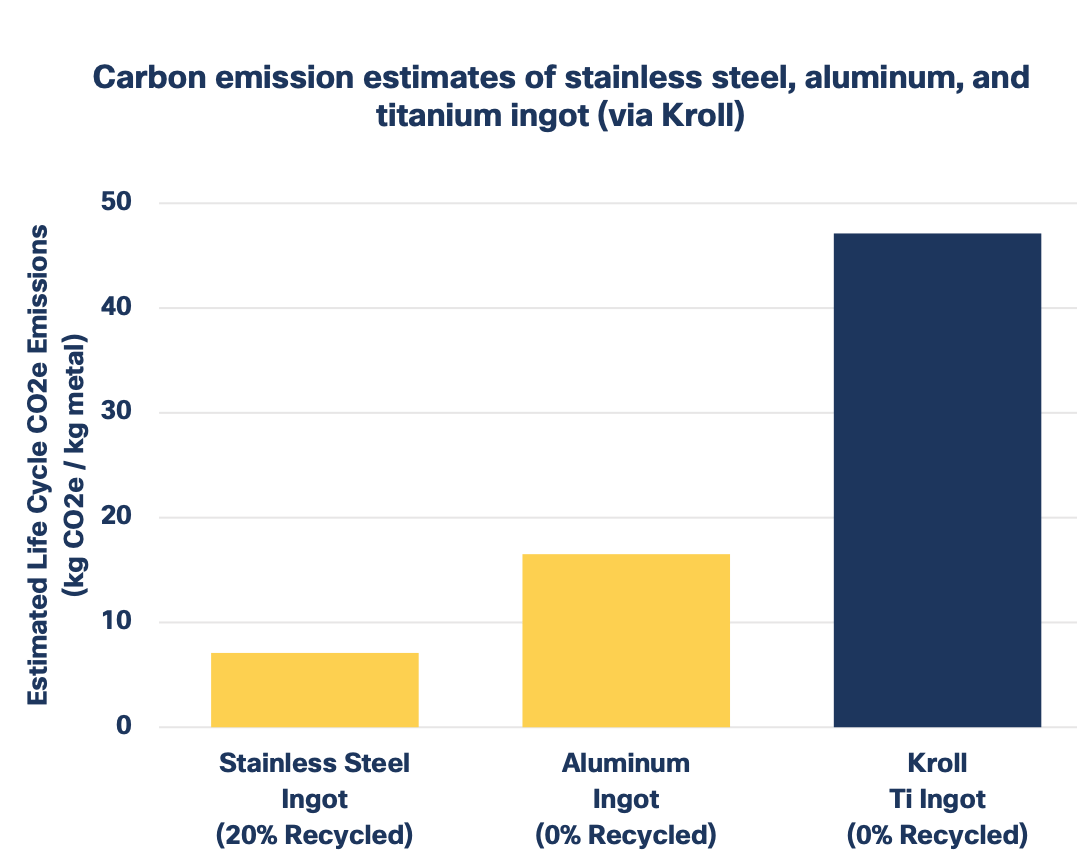

The titanium ingot spot price, for example, in the first quarter of 2023 was at $ 27,000/t , which is over 11x the aluminum coil price and almost 5x higher than stainless steel hot rolled coil price as per the company's data (see slide 7 of the link). It also faces the challenge of far higher carbon emissions over its life cycle compared to other metals, when the traditional Kroll process is used (see chart below).

{kind=link}

If the company is able to disrupt the titanium market with its innovations, there can be significant potential for it in my view, considering that the stainless steel market is 50x the size of the $4 billion titanium market and the aluminum market is over 40x its size.

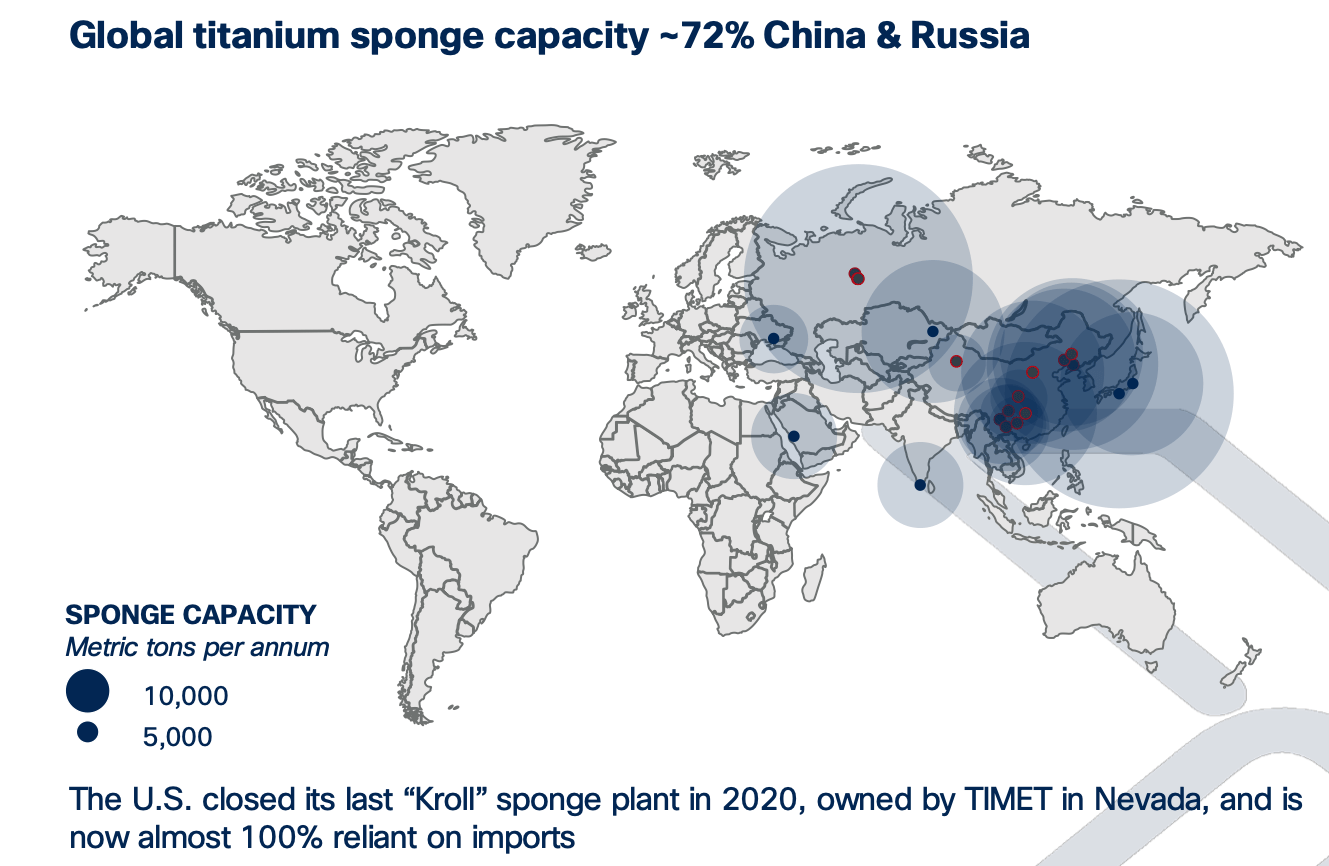

In any case, there’s presently a case to restart titanium production in the US, after its last remaining titanium processing plant was closed down in 2020. With 72% of the global capacity for titanium sponge, an intermediate product used in the production of finished products, with China and Russia right now, the present geopolitical situation would be in the current spirit of securing domestic production.

{kind=link}

What it does

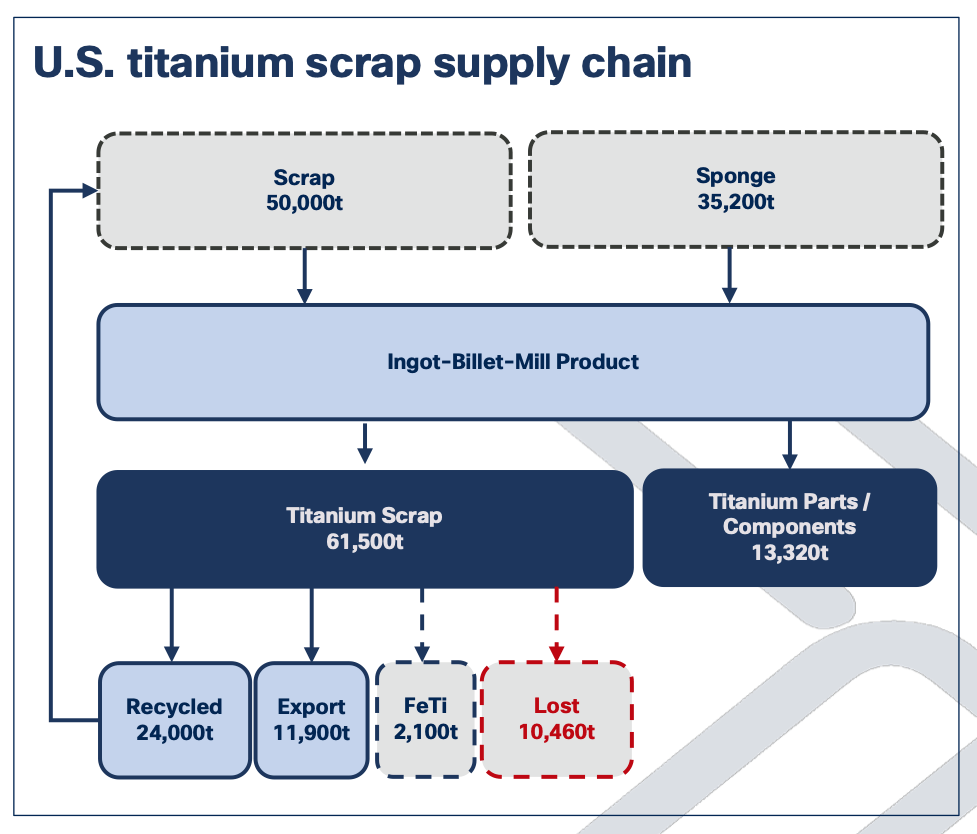

Founded in 2017, the Charlotte, North Carolina headquartered company has innovative production processes underway that are superior to the traditional Kroll process. Since the Kroll process limits the ability for recycled titanium usage (see chart below), there are higher costs associated with production and a fully circular economy is inhibited.

{kind=link}

Titanium processing

IperionX’s production processes, however, have multiple advantages over the existing process. For one, they are energy efficient, allowing for lower costs. They also generate lower greenhouse gas emissions and can use scrap metal instead of mined titanium.

It has three production processes in place called the Hydrogen Assisted Metallothermic Reduction [HAMR] process, Granulation-Sintering-Deoxygenation [GSD] process and Synthetic Rutile.

The first two are thermochemical processes, commonly used for the conversion of raw substances into fuels and other useful products. Both of them have the advantage of being low cost, while the HAMR process is also low in emission generation. Synthetic Rutile converts titanium feedstocks into high-grade versions, without using carbon-generating fuel sources.

The Titan project

The company also owns the Titan project, a big titanium, zirconium and rare earth minerals deposit in west Tennessee, US. It received all the permits required to develop it last month, which is a positive considering that the project is amenable to low-cost and sustainable mineral extraction, which are running themes for the company.

Progress so far

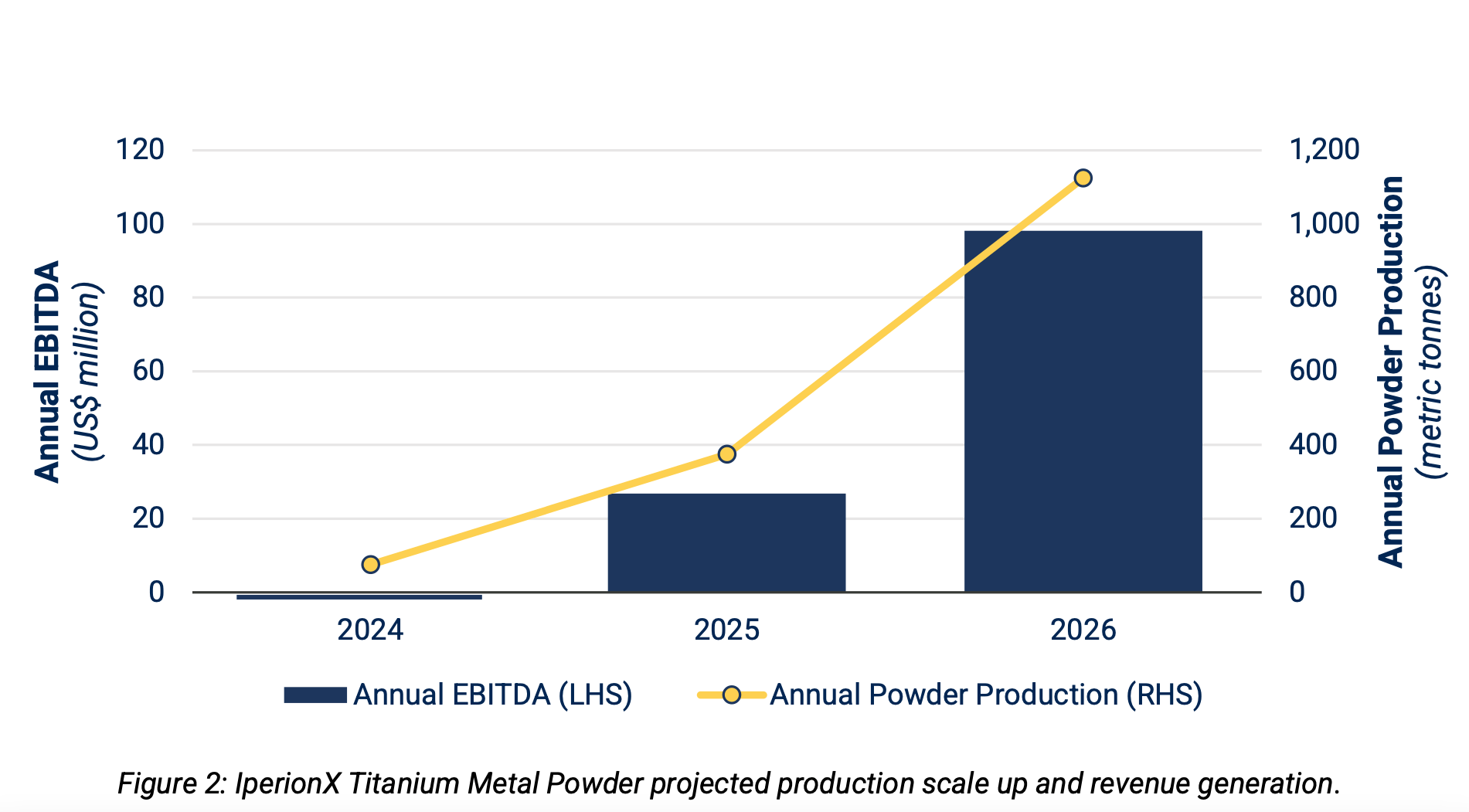

The company expects to start production to start full-scale commercial production in 2025 using the HAMR process. Significantly lower production costs of around $42/kg compared to other producers’ costs of $200/kg are forecast. It also expects to be EBITDA positive from the start, with is estimated to be at $100 million by 2026 (see chart below).

{kind=link}

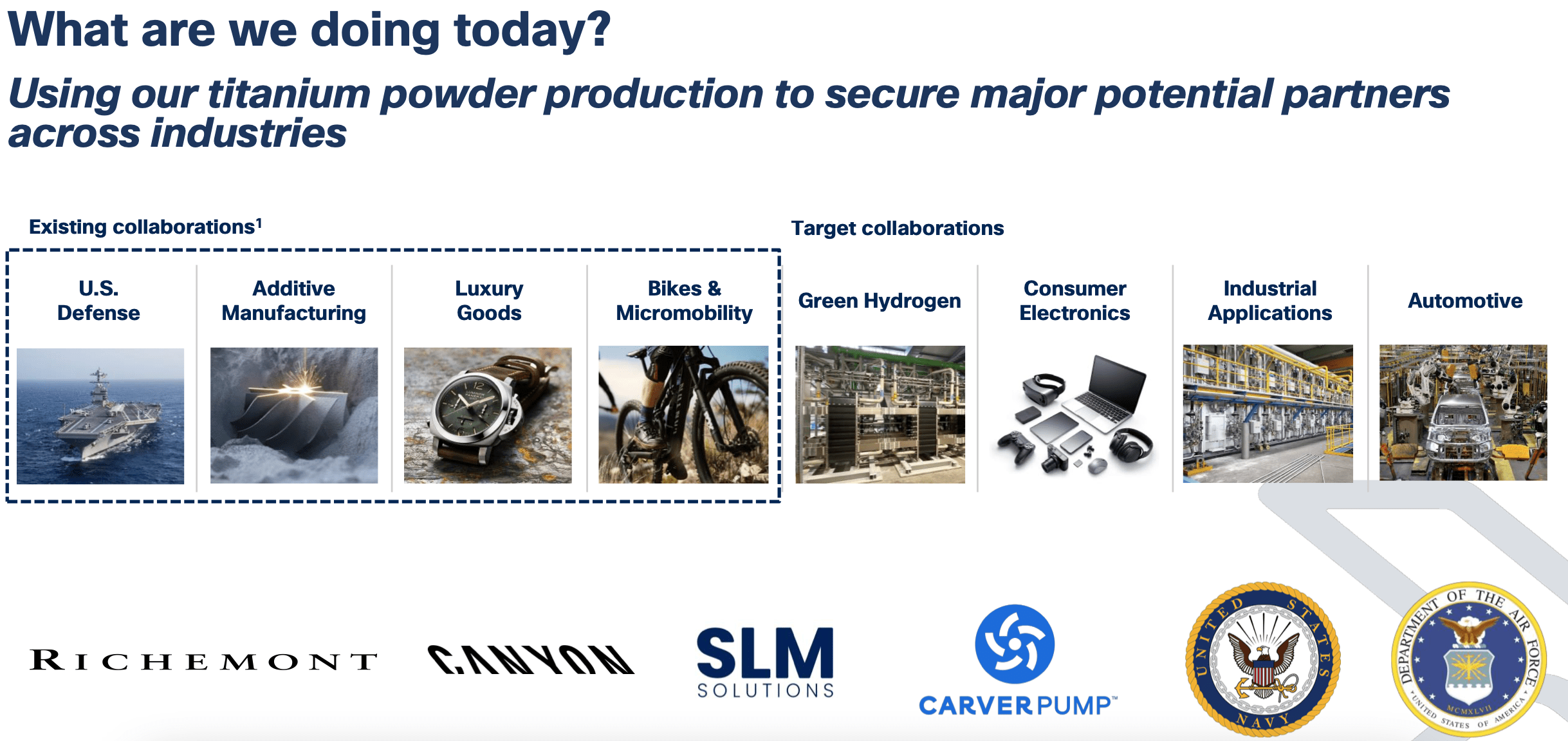

The company already has collaborations with customers in multiple sectors and is now targeting collaboration in newer sectors as well (see chart below). Notable among the target sectors is the green hydrogen market, whose production is forecast to increase by 1000x by 2030 (see Page 7 of the link). Titanium is used in electrolyzers required for green hydrogen production and also in hydrogen fuel cells. Hydrogen production ramp-up may well be witnessed shortly, as the Inflation Reduction Act [IRA] provides both a hydrogen production tax credit and a capital expenditure tax credit.

{kind=link}

Financials and market multiples

The company’s balance sheet looks alright to me, with its current ratio for December 2022 (the latest half year for which numbers are available), was at 6.5x. Its assets-to-liabilities ratio at 6.9x is also healthy, with limited debt on its books.

For pre-production companies, I also like to consider the working capital to operating expenses ratio since it gives a sense of how long the company can go on without needing additional funding for its expenses. Its working capital in December 2022 was $10 million, which is 2.3x the operating expenses. This indicates that it had enough to last for over a year. This isn’t ideal, but considering that it starts initial production in early 2024, it isn’t the worst-case scenario either.

The company’s price-to-book (P/B) ratio is rather high at 9.2x compared to 1.6x for the materials sector. This is of course related to IperionX’s potential, but at the same time, it also makes the stock less of a sure buy.

What next?

IperionX sure sounds promising in that it can disrupt the titanium market by slashing costs and reducing emissions. If all goes according to plan, titanium may well be a competitor to lower cost metals like aluminum and steel.

It has also made much headway, with full-scale commercial production due to start in 2025, the financial estimates for which look appealing in that the company expects to be EBITDA positive from the get go. Its balance sheet also looks healthy, though a higher cover for operating expenses would have been better.

Investors are clearly bullish about it going by the market multiples. But we will know for certain how things turn out for it when it starts production. Until then, I think it's still too early to buy it. I’m going with a Hold on IperionX.

For further details see:

IperionX: Promising Potential But It's Still Early Days