IPSEY - Ipsen: Positive On Bylvay But Uncertain About 2028/2029 Expiries

2023-04-19 11:56:38 ET

Summary

- The addition of Bylvay to its portfolio is expected to have a positive impact on the company's medium-term growth prospects.

- The threat of competition from Livmarli could curb Bylvay's potential.

- The looming patent expiry of Onivyde/Cabometyx in 2028 and 2029 may continue to weigh on the company's valuation.

Investment thesis

Ipsen (IPSEY) develops, produces, and sells pharmaceuticals for a variety of medical conditions, including oncology, endocrinology, and neuromuscular diseases. This article discusses IPSEY's business after acquiring Albireo , with a special emphasis on the drug Bylvay and the market for it in the conditions of Progressive Familial Intrahepatic Cholestasis [PFIC], Alagille Syndrome [ALGS], and Biliary Atresia [BA]. To put it simply, I think Ipsen will do well in the medium term after adding Bylvay's sales. However, in my opinion, the looming Onivyde/Cabometyx patent expiry in 2028 and 2029 will continue to weigh on Ipsen's valuation despite the addition of Bylvay, and until this factor is resolved, a hold rating is warranted. However, the elafibranor 2L PBC readout at the end of 2Q23 has the potential to further improve IPSEY's outlook, so I think this could become a special situation investment opportunity. Please note that I am not a medical professional or student, and that any medical analysis presented below is based solely on my own research.

Bylvay

{kind=link}

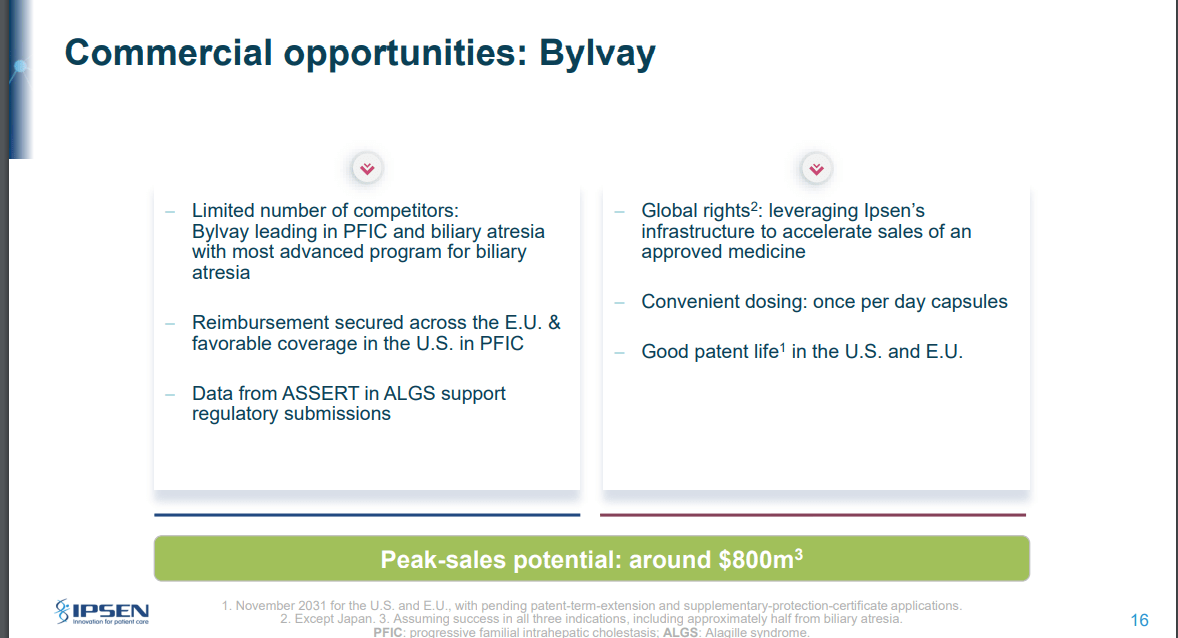

The threat of competition from Livmarli (owned by Mirum Pharma), in my opinion, could curb Bylvay's potential. In my opinion, Bylvay and Livmarli are both well-positioned to capitalize on the growing market for treatments for rare orphan diseases like PFIC, ALGS, and BA, with Bylvay's time-to-market advantage in BA and PFIC as well as its more convenient dosing potentially offsetting Livmarli's slightly higher efficacy. IPSEY may, in fact, face severe competition from Livmarli and end up splitting the market in half. Therefore, I anticipate Bylvay's peak sales to be significantly below the €800 million projected by management. Nonetheless, I think it will help improve IPSEY's medium-term growth prospects significantly.

{kind=link}

The competing products in the PFIC market, ALGS and BA, have similar enough profiles that I don't see much room for differentiation between them. That said, I believe that Livmarli may have a slightly better effectiveness profile compared to Bylvay. However, due to the limited number of patients and the use of slightly different endpoints, it is challenging to determine the relative effectiveness accurately. However, an inherent advantage that Bylvay has, I think, is the lower rate of Diarrhea . IPSEY has a slight advantage over competing therapies because Bylvay is more convenient to take (a once-daily oral capsule rather than a twice-daily oral solution) and because it has been on the market for at least two years longer than Livmarli's PFIC and BA and ALGS in the United States.

My hypothesis is that Bylvay and Livmarli will split the IBAT opportunity evenly across all metrics (50% each at peak). In particular, while I expect Bylvay to have the time to market advantage in BA, I don't think sales will hit €800 million (that management expected), as it's hard for me to say with much confidence (based on what I know) that Bylvay is noticeably different from Livmarli. As such, I would take the safer path of being conservative (which I think is what many investors that do not have deep medical knowledge should do as well).

Future M&A

In the FY22 report, management restated its commitment to bolstering its capacity for external innovation. I think management is getting better at closing deals, and I'm a fan of the Albireo deal (it helps IPSEY's medium-term prospects despite some concerns about increased competition). IPSEY has executed several multibillion-dollar deals since its new CEO took over in July 2020, and due to the advantageous terms of these deals, capital outlays are often deferred. Take the €120 million upfront payment made to Elafibranor, for instance; this was 25% of the total purchase price. The Albireo acquisition has given IPSEY a healthy balance sheet with about €1.5 billion in available capital, and I anticipate that this will grow in the coming years. If management can continue finding attractive assets to acquire, it could eventually cover the Onivyde/Cabometyx patent expiry in 2028 and 2029.

Catalyst

Even though the earnings story is cloudy, there is still good news on the horizon. Upside potential may exist for elafibranor stock if the Phase III ELATIVE study readout in 2Q23 demonstrates a clinically meaningful benefit on ALP and pruritus compared to the current standard of care Ocaliva. However, when the Phase III RESPONSE study results are published in 3Q23, there is a possibility that seladelpar, a key competitor, will report statistically superior efficacy to elafibranor. Any potential benefit would be nullified by this action.

Conclusion

The IPSEY acquisition of Albireo and the addition of Bylvay to its portfolio are expected to have a positive impact on the company's medium-term growth prospects. However, the looming patent expiry of Onivyde/Cabometyx in 2028 and 2029 may continue to weigh on the company's valuation, and a hold rating is recommended until this issue is resolved. Despite the potential threat of competition from Livmarli, Bylvay's time-to-market advantage and more convenient dosing make it well-positioned to capitalize on the growing market for treatments for rare orphan diseases. I also think management commitment to external innovation and successful execution of recent multibillion-dollar deals bode well for its future M&A prospects. Overall, my hold rating is stemmed from the uncertainties in the company's earnings story.

For further details see:

Ipsen: Positive On Bylvay But Uncertain About 2028/2029 Expiries