IRDEY - Iren: Tough Winter Would Be Bad

2023-08-03 07:58:01 ET

Summary

- Iren is pretty exposed to high gas prices which can affect their spark spread. While they do hedge, difficulties in gas prices affect their large CCGT capacity.

- Iren is behind on the renewable transition relative to the other Italian players who've generally been very progressive.

- While Iren has strengths in regulated concessions which are long-dated businesses, the CAPEX burdens to catch-up in renewable make them uncompelling at current valuations.

Iren ( OTCPK:IRDEF ) is an Italian energy player that would be known to a lot of people who pay energy bills in Italy. They have quite a lot of regulated businesses, and they're doing well on that front as new concessions become consolidated. Those businesses are long-dated. The greater concern is in the energy generation business and how it relates to the multiple. They are quite behind on renewables and that investment is expensive. For now they are reliant on thermoelectric power. Iren doesn't stand out as a great investment.

Discussing H1 2023

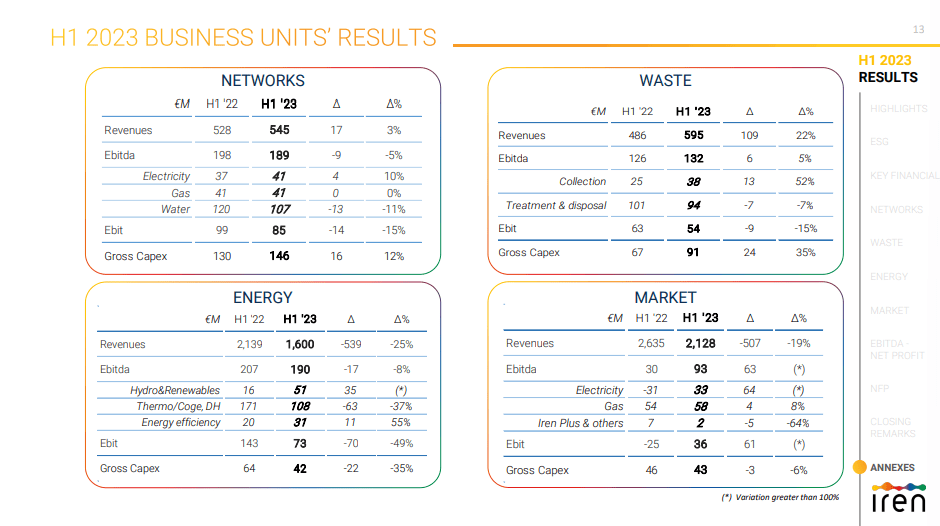

Let's have a quick look at some of the high-level results .

{kind=link}

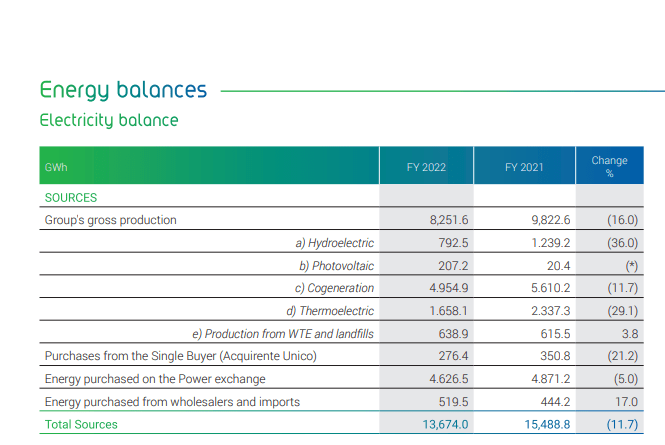

Energy includes heat generation but also power. A lot of the energy they generate is from cogeneration and from thermoelectric plants. Thermoelectric power is at more than 2x the power generated by hydropower, then there are the cogeneration plants that produce both electricity and heat which further eclipse the renewable contribution. Photovoltaic investments in 2022 is why the renewable EBITDA has grown so much, where capacity 10xed. Currently there is about 6x more power generated from CCGT than renewable sources.

{kind=link}

While Iren actively manages hedging activity in order to avoid major margin compression, the large thermoelectric exposure means a bad and cold winter that seriously draws down on reserves of LNG in Europe will eventually affect gas prices for Iren which is an input to their spark spread. Since there is quite a lot of regulation regarding how these prices can be passed on, especially in Italy, the impacts could be pretty severe on thermo margins which have already been meaningfully hit YoY. Providing heating which would be in higher demand in a cold winter would also potentially crimp the company margins if they got stuck buying expensive gas that's getting hoarded at spot prices. However, there is an extent to which the provision of heat will benefit from higher prices, as margins were better in heating last year, and also there was more heating demand.

Waste and networks are both government concessions. A Tuscan concession being recently consolidated results in a pretty great H1 jump in waste, although this consolidation effect will disappear next quarter. In networks, the deal is the same as always, which is that companies are responsible for operating regulated utilities and carry the OPEX burden. By making investments and improving the scale of the regulated utility they can earn higher remuneration from the government. While rates of the regulated tariff are also indexed to rates and, therefore, indirectly to inflation, OPEX inflation is outrunning revenue effects currently. The end of inflation would be a good thing for Iren's regulated businesses.

Bottom Line

Iren is mainly a CCGT company. It's not the best considering the war in Ukraine continues to go on with no obvious end in sight, at least not before winter. Europe has not dealt with a cold winter post-Ukraine invasion, but this may be the year. Things could get bad and Iren's margins are likely going to suffer even after hedging if Italy gets cold.

The other issue is the renewable transition. Italy is very progressive in terms of its companies making investments in renewables. Even other more far behind comps that have big retail businesses like Iren are still further ahead . Iren trades in line with them after considering some of the CAPEX burden at around a 9x PE, but in order to roll out new production more investments will be needed and they take a lot out of the cash flows. FCF was negative in 2022, and it will continue to be compressed for a while longer, likely for some more years. While they trade at a first glance discount to some competitors, CAPEX burden as well as uncertainty around gas prices in the coming winter have us looking elsewhere since the economic returns aren't great right now as they scramble on the renewable front.

For further details see:

Iren: Tough Winter Would Be Bad