IRTC - iRhythm: Fairly Priced At Current Multiples No Need To Size Up

Summary

- iRhythm Technologies continues to offer long-term value for seasoned healthcare investors who can hedge around portfolio variance.

- For current owners, we currently don't recommend "sizing up" an already existing IRTC position.

- However, shares appear fairly priced, and new buyers are buying exposure to defensive and niche credentials in IRTC.

- We value IRTC a hold and expect further commentary in the coming months with reimbursement updates from Novitas.

Investment Summary

As owners of iRhythm Technologies, Inc. ( IRTC ) shares, we constantly review the weight of the position and evaluate its portion of the equity risk budget. Note we are underweight global equities as an asset class in favor of the short end of the curve and alternatives.

Alas, we have trimmed the IRTC position down substantially and are long-term holders with tactical exposure to the sub-industry and IRTC's niche credentials. However, we are right now neutral on the shares and don't envision sizing up the position any time soon. Looking ahead, IRTC looks to have moved more defensive and may offer these characteristics in a weakening economic climate. Alas, valuations are supportive of a hold at a price objective of $153-$157.

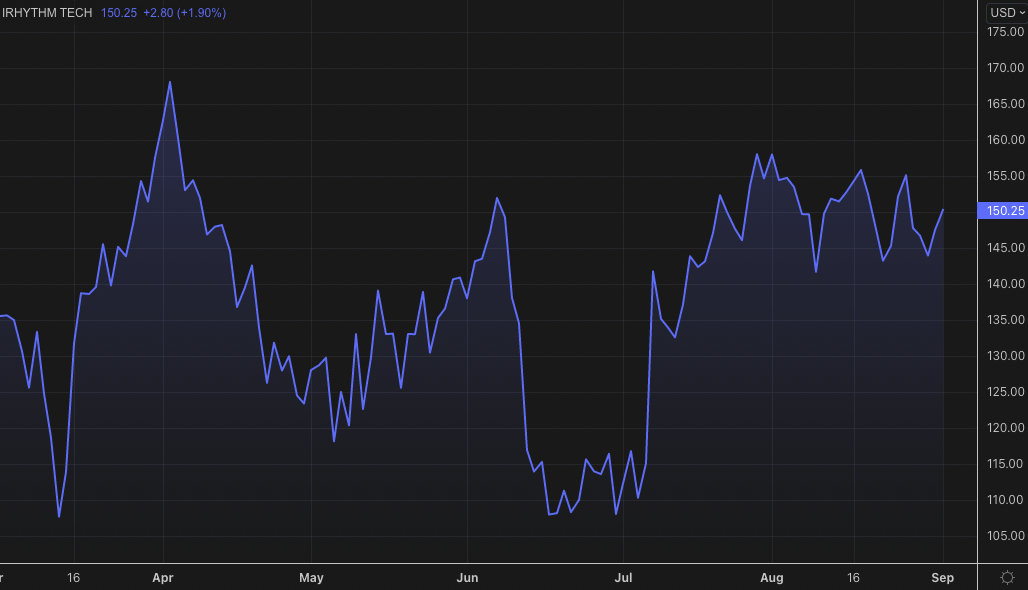

Exhibit 1. IRTC 6-month price action

{kind=link}

Reimbursement overhang not a risk, but don't ignore

Good news flowed back in January FY22 when Novitas Solutions updated rates for CPT codes 93243 and 93247 to $223 and $233 respectively. Novitas is the MAC that covers IRTC's independent diagnostic testing facility ("IDTF") in Houston, Texas. The updated rates were an improvement from FY21 but are well below historical rates for Zio XT. So we still need to see these stretch back up somewhat in order to get back to the frenzy of FY20.

Yet, in Illinois, the MAC covering its IDTF in Illinois, NGS, updated the codes to $335 and $247 respectively, retroactive to January 2022. These rates are higher than historical Medicare reimbursement rates for Zio XT. So the company is seeing regulatory tailwinds in that regard.

Importantly, CMS has proposed national payment rates for Zio XT's category of CPT code, effective for FY23. It proposes a so-called conversion factor, which the company estimates to be between $215-$204 for the 93247 and 93243 codes, respectively. With the conversion factor in place on a 2023 Geographic Practice Cost Index ("GPCI"), it believes that rates could range from $218 to $295 for CPT code 93247 and $207 to $280 for CPT code 93243.

It's understood the 2023 final rule is expected to be announced by November 2022 for implementation on January 1, 2023. Regarding changes that took effect in FY21, per the company's Q2 FY22 10-Q:

"As a result of the CPT code changes that took effect January 1, 2021, the number of claims from the first half of 2021, which contained differences between the submitted price and reimbursement rate and overall denials, increased significantly compared to the Company's historical experience as a result of CPT code transition issues with the payors.

The Company continues to work with the payors to collect on these claims, however, the collection cycle for these claims is significantly longer than usual and may lead to higher write-offs of doubtful accounts for those periods and negatively impact the Company's results of operations".

The reimbursement picture is critical in understanding IRTC's forward earnings momentum and predicting the company's future cash flows. In that vein, as in similar companies who rely on rebates and reimbursement to book revenue, much of the upside is capped on the reimbursement variable. It is therefore paramount IRTC succeeds from a volume perspective to overcome this. These are key risks to consider looking ahead.

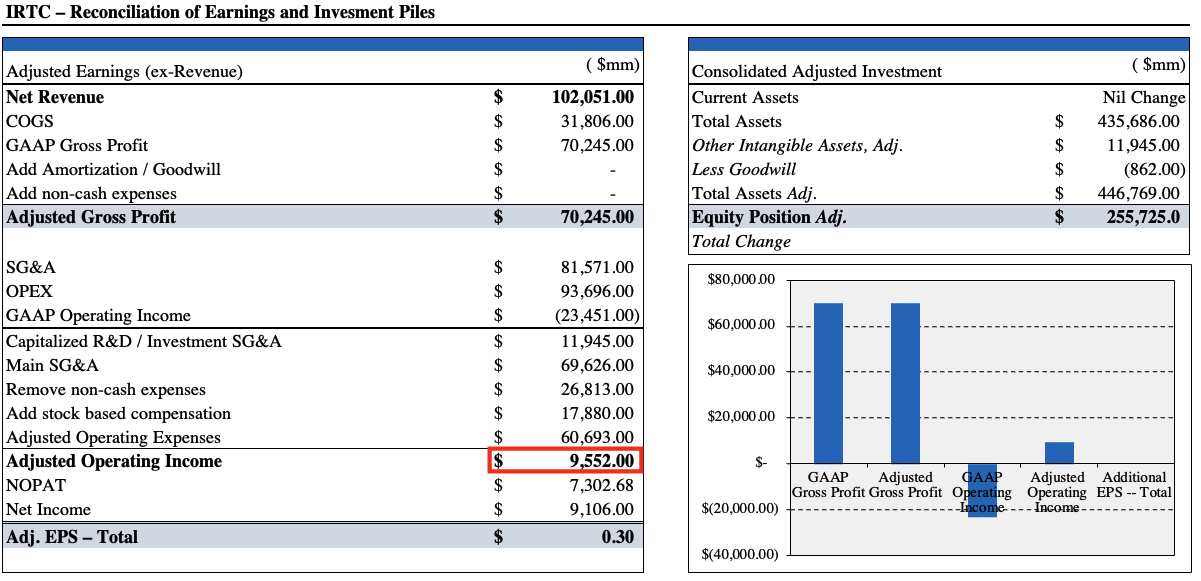

Accounting adjustments for valuation

Forensics on IRTC's financial statements reveal that several reconciliations must be made in order to extract a measure of true corporate value. As noted in Exhibit 2, we've capitalized $11.9 million ("mm") in R&D expenditure to the balance sheet, and this includes $17.8mm of stock-based compensation to OPEX. Doing so has significant impacts to earnings and investment value. With that, we see an adjusted earnings of $0.30 per share, up from a loss of $0.80 per share in the quarter. Meanwhile, we also back out ~$826K from the balance sheet and after post-adjustments shareholder value increases to $255.7mm.

Exhibit 2. IRTC adjustments to GAAP earnings

{kind=link}

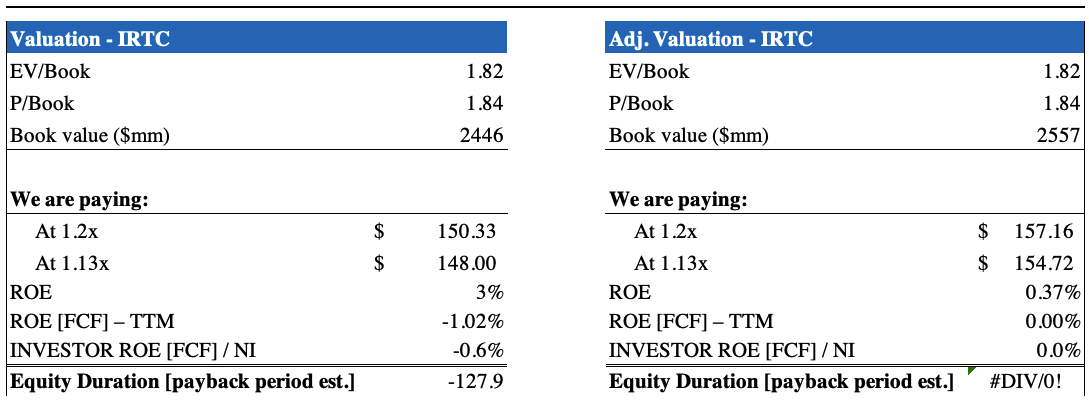

Valuation

Shares are trading at 12.3x sales and are also priced at 1.8x book value and enterprise value ("EV") to book value of equity. On face value, these appear to be respective multiples, but we have to first gauge a) what it is we are buying with IRTC and, b) if these multiples do represent a value proposition.

As seen in Exhibit 3, both pre and post-adjustment, at the above multiples we'd be paying a relative premium, or at least fair value for the stock. That could be fine if the valuation is worth what's on offer. Recall that an investment is typically worth it if the payoff - the present value of the future cash flows - is greater than the cost. In other words, if the rate of return is greater than the implied cost.

Exhibit 3.

{kind=link}

Factoring these points into the equation, we see that shares are likely to be priced fairly at the current market capitalization. The below model bakes in a breadth of valuation inputs that look at the spectrum of continuing value, i.e., earnings. All else considered, we feel shares could be fairly priced at an objective of $153.50, as seen in Exhibit 4.

Another way to think of it is that we're paying $154-$157 [post-adjustment] for a price objective of $153. On GAAP earnings, it's a similar differential. This valuation, therefore, supports a neutral view.

Exhibit 4.

Data: HB Insights Estimates

With the above points in mind, IRTC doesn't appear to be at any inflection point just yet. Rates/reimbursement still presents with imminent challenges but isn't the dark cloud on the company's numbers it once was. Nevertheless, it remains integral to the IRTC story heading forward.

However, looking at numbers and not narrative, and understanding what we're buying today in IRTC, there appears to be a lack of compelling value on offer. Valuations are supportive of a neutral view, alongside other measures of corporate value as well - in particular, profitability and return on investment. Alas, with this in mind, we rate IRTC a hold with a $153-$157 valuation.

For further details see:

iRhythm: Fairly Priced At Current Multiples, No Need To Size Up