IRS - IRSA Inversiones: A Call Option On Premium Estates Without An Expiration Date

2023-09-07 06:21:55 ET

Summary

- Argentina represents a rare opportunity for adventurous investors. The runaway inflation will push the depositors to seek shelter in equities and tangible assets. Turkey is a prime example.

- IRSA Inversiones is a two-fold bet on that dynamics. The company manages a portfolio of shopping malls and office buildings in prime locations in Buenos Aires and other cities.

- The company owns a hidden gem: Costa Urbana is the most significant development project in Buenos Aires. Its value might exceed significantly the current market cap of IRSA.

- IRSA offers exposure simultaneity to the rising equity market and growing real estate prices for prices lower than its NAV.

- IRSA has been a significant part of my portfolio for the last 12 months for the reasons mentioned. Said that I give the stock a strong buy rating.

Thesis

IRSA Inversiones (IRS) owns a portfolio of high-quality real estate in Argentina. Among them is Costa Urbana, the most significant development project in Buenos Aires. Its value might exceed the company's market cap without being too generous. IRSA significantly improved its standing after merging with its sister company, IRCP. Before, both companies were in messy relationships, and researching them was an analyst nightmare.

The company's financials are in order. IRSA reduced its debts despite the COVID lockdown that severely affected its business. The primary revenue source is the shopping malls. They recovered successfully from the pandemic lows; that year, TTM EBITDA exceeded 2019 numbers.

Mr. Market values IRSA assets well below its NAV. I have been a shareholder for 12 months and am planning to hold the position. That said, I give IRSA a strong buy rating.

Demography, Runaway Inflation, and Parabolic Markets Moves

My focus as an investor is the overlooked corners of the market. The middle of the distribution curve is too crowded. On the other hand, on both sides of the bell curve resides Alpha, where the markets cannot price the business efficiently. Latin America offers such opportunities. LATAM real estate markets are an exciting proposition for adventurous investors. It offers enormous upside potential, and we pay cents on the dollar.

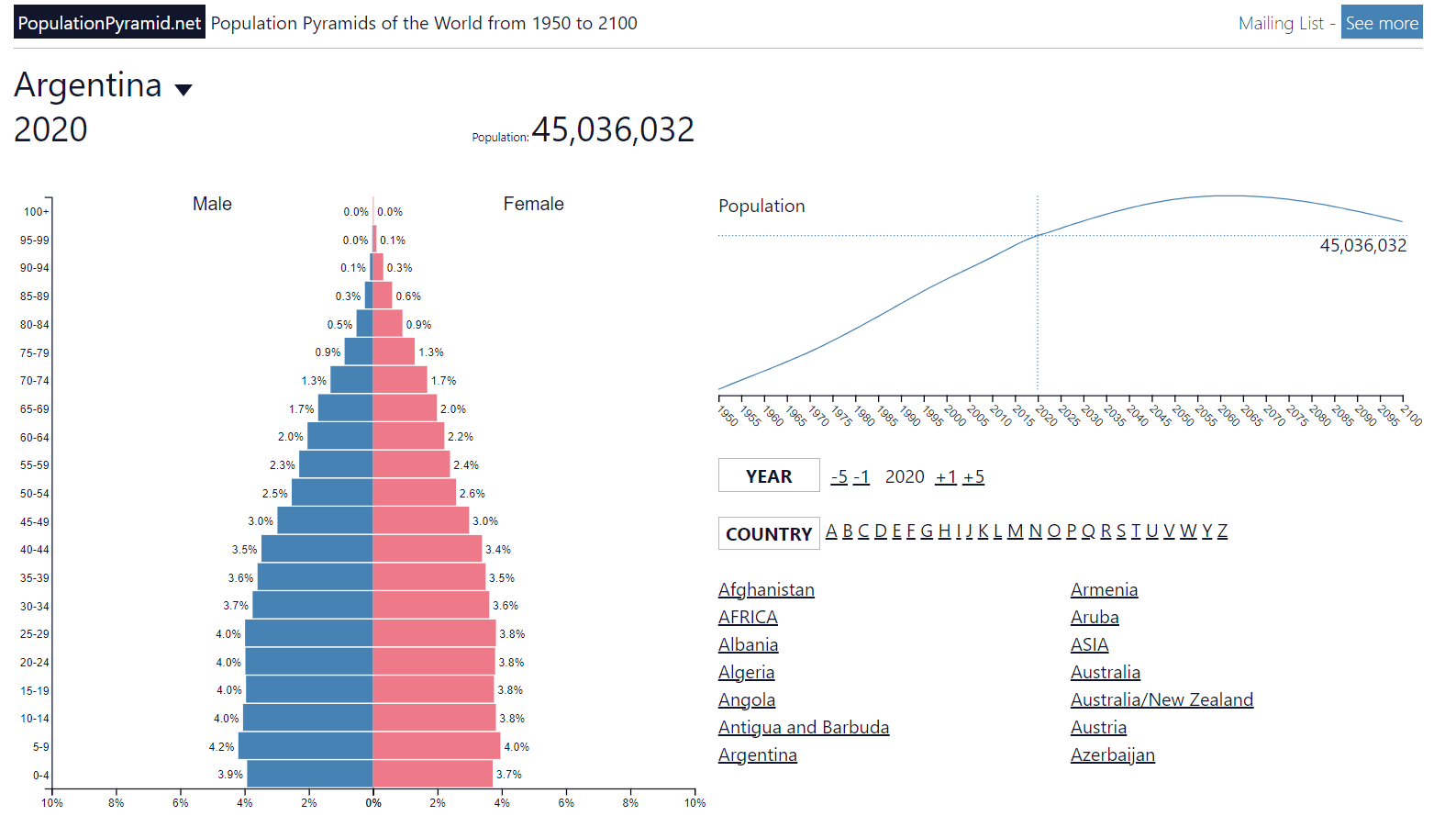

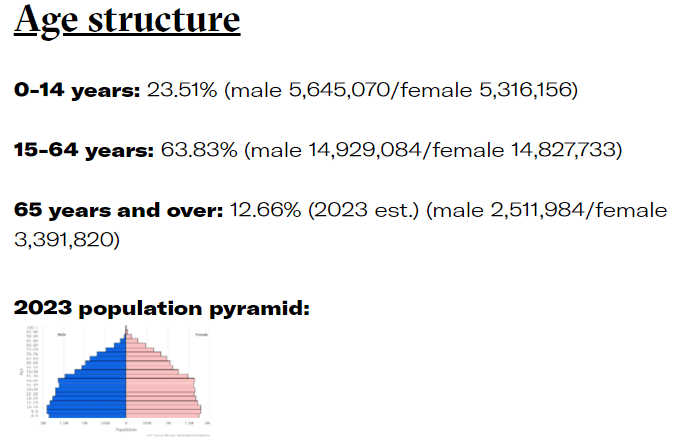

Real Estate business depends long term on demography. Argentina's population pyramid is still good. That means more people are in productive age and fewer are retired. The chart below shows Argentina's population structure:

{kind=link}

The importance of those charts could not be overstated. Demography is destiny. Investing in real estate means knowing the population dynamics in the region. A growing number of people will create demand for your company's real estate and vice versa. Regardless of how exclusive your properties are, no one will be interested in renting if there are no people. Going deeper in detail, below is the Buenos Aires population data from the CIA fact book :

{kind=link}

The working population represents 63.8 % of the total, while the youngster 0-14 years 23 %. Those numbers favor the city's development in the next decade.

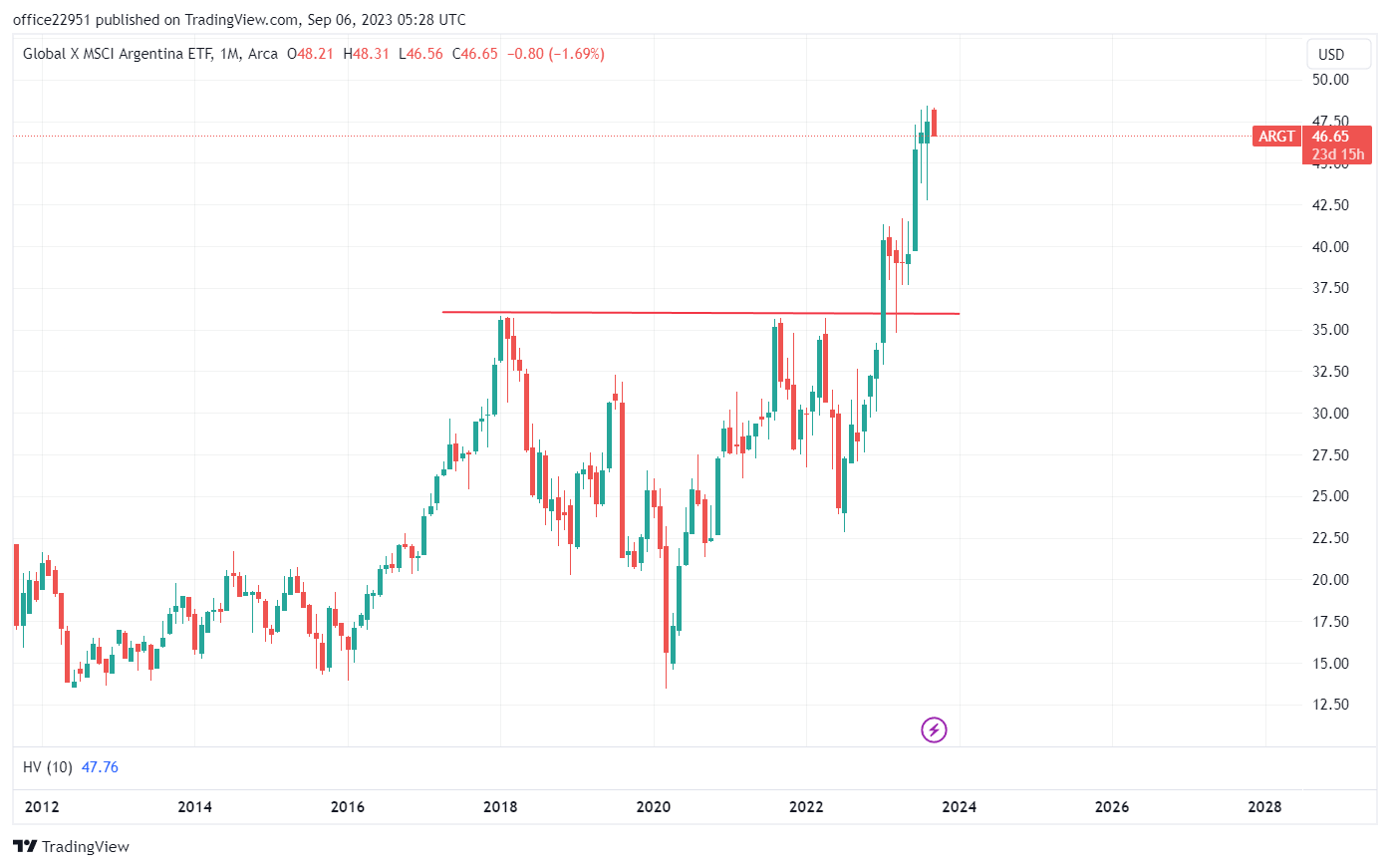

Despite the great demography, Argentina is a synonym for economic turmoil. Recommending investing there puts my sanity under question. However, avoiding crowded positions might create extraordinary gains. The latter are hidden in unexpected places. The chart below is such an example; it shows the performance of Global X Argentina (ARGT):

Trading View Global X Argentina

{kind=link}

ARGT is among the best-performing indexes for the 12 months. Bear in mind next month, Argentina will hold presidential elections. The winner of PASO Milei is a strong contender for the office. He is proposing market-oriented reforms to stimulate investors and entrepreneurs. The other competitors for Casa Rosada are market-oriented, too, to a different degree. The political pendulum will accomplish its swing from left to right and ignite another bull run on Argentinean equities.

On top of that, the ever-rising inflation and plummeting peso will push the locals to allocate their capital to the stock and real estate markets. Examples of such dynamics are Turkey and Iran . The latter deserves special mention:

{kind=link}

Iran's TEDPIX index realized x5 for a few years due to runaway inflation that pushed the depositors to invest in equities instead of holding its evaporating cash.

After the brief primer in demography and runaway inflation-market parabolic moves correlations, it's time to move to the next chapter: IRSA Inversiones as a call option on prime real estate without expiration.

Company Overview

IRSA is part of the business empire of Alejandro Elsztain , who is CEO of IRSA and CRESUD S.A.C.I.F y.a. (CRESY). CRESY is the largest shareholder in IRSA's 58.1 % stake. In December 2021, IRSA merged with IRCP. The latter was another company, part of Elzstain's holdings. Before the merger, IRSA was an analyst nightmare due to its complicated structure. The company invested in IDB Israeli diversified holding: IDB-owned airlines, pharmacies, telecoms, and more. IRSA divested its stake in IDB after the merger. Since then, the corporate structure has been simple and easy to understand.

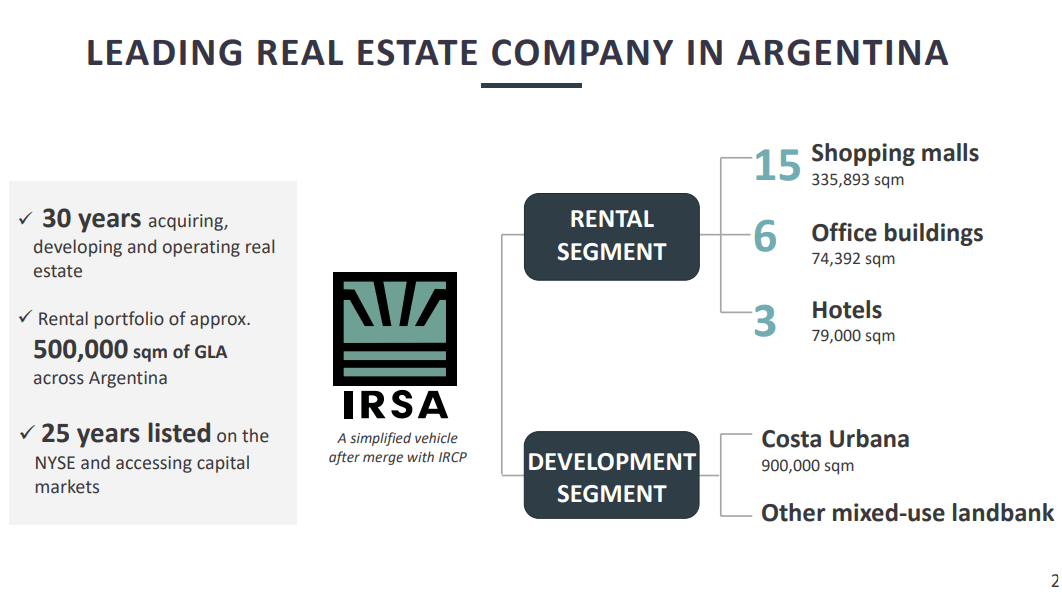

IRSA Inversiones runs a portfolio of commercial real estate. Currently owns 15 shopping malls, six office buildings, and three hotels. The table below from the last company presentation shows IRSA at a glance:

{kind=link}

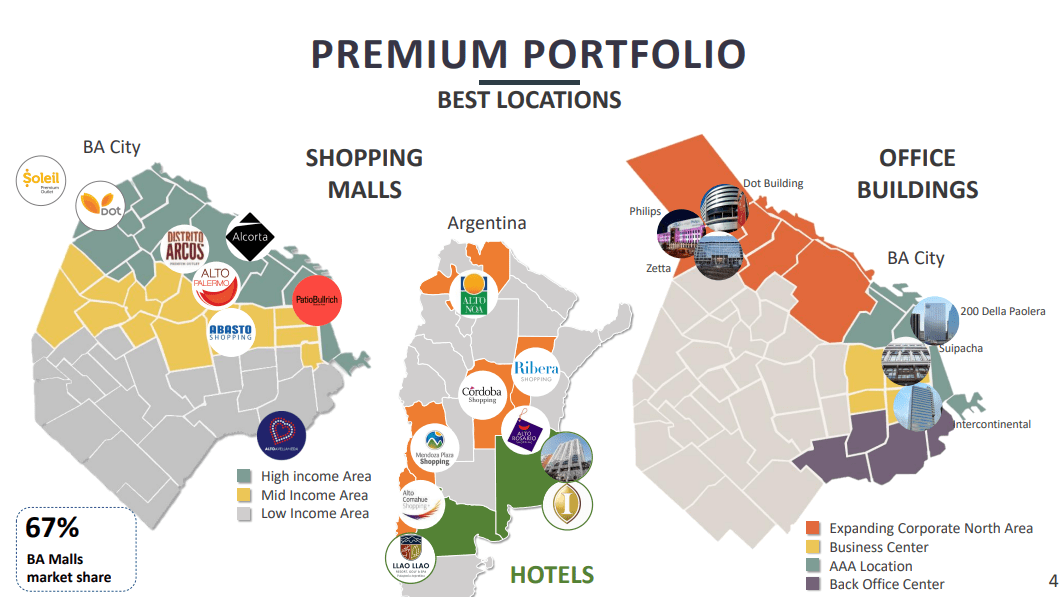

The shopping centers are located in premium districts of Buenos Aires, Mendoza, Cordoba, and Salta. However, the company's primary assets are in Buenos Aires. IRSA assets are shown on the map below:

{kind=link}

IRSA office buildings are concentrated in high-income areas such as Puerto Madero, Retiro, and Recoleta.

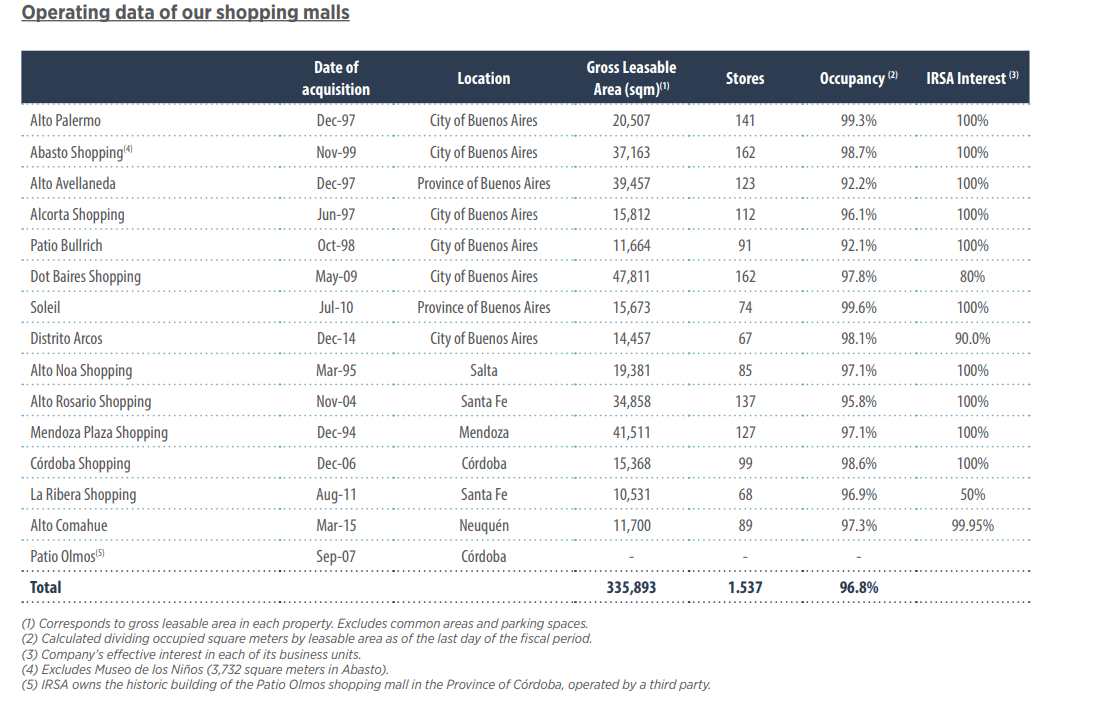

The company's most significant source of revenue is the shopping malls. The table below shows their performance:

{kind=link}

The occupancy rate has recovered from the COVID-19 lows, translating into EBITDA growth. The structure of shopping mall revenue is divided between rental 74 % and others (brokerage fees, parking, and advertising). The rent is divided into base rent and % of tenant's sales. The rents are paid ARS, and its value is linked to the inflation.

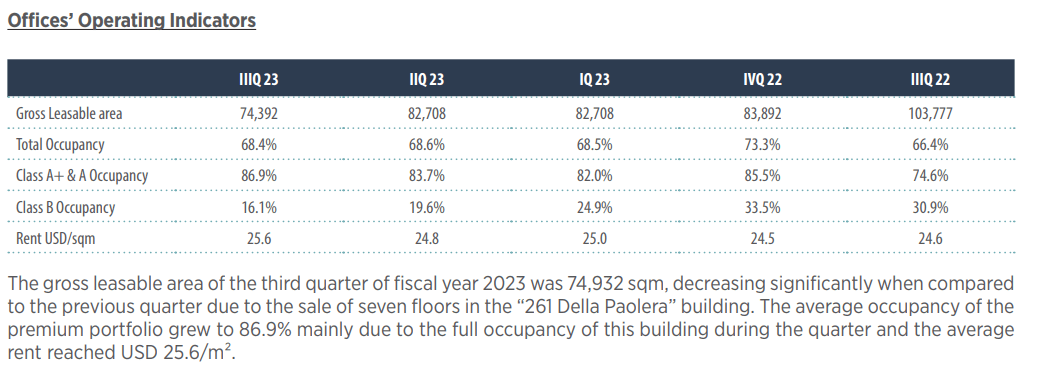

The office buildings generate 11 % of the revenues. They are profitability decline despite the post-COVID recovery. The table below illustrates the segment parameters:

{kind=link}

The occupancy rate has been stagnant for the last two years. The declining CRE occupancy is not endemic to IRSA or Argentina. The transition to home office due to the pandemic lockdowns drastically impacted the profitability of the office segment.

Among the company's hidden gems is the Costa Urbana project. In December 2021, the Buenos Aires City Congress approved the project and published a law grant, "U73 Public Parks and Costa Urbana Urbanization". This is a green light for IRSA after more than 20 years. The quote below from the company's CEO illustrates the importance of the project:

After more than 20 years, it is a significant milestone to have the approval of the company's largest project that will boost its future growth. We hope to contribute to employment creation and the city's development with an innovative, modern, and sustainable project, which implies a great opportunity and, at the same time, a responsibility. We are convinced of the potential of the real estate industry and its role in the economic reactivation of the country.

- Eduardo Elsztain, President and CEO of IRSA.

Company Financials

IRSA has a robust balance sheet, providing the company with sufficient liquidity. The table below shows IRSA liquidity metrics. The data is from the company's last report .

| Debt Service Coverage Ratio |

| 2.01 |

| Quick ratio |

| 2.01 |

| Current ratio |

| 1.43 |

| Net debt/AFFO |

| 3.7 |

| Long-term debt/Equity |

| 17 % |

| Total debt/Equity |

| 25 % |

| Total liabilities/Total assets |

| 45 % |

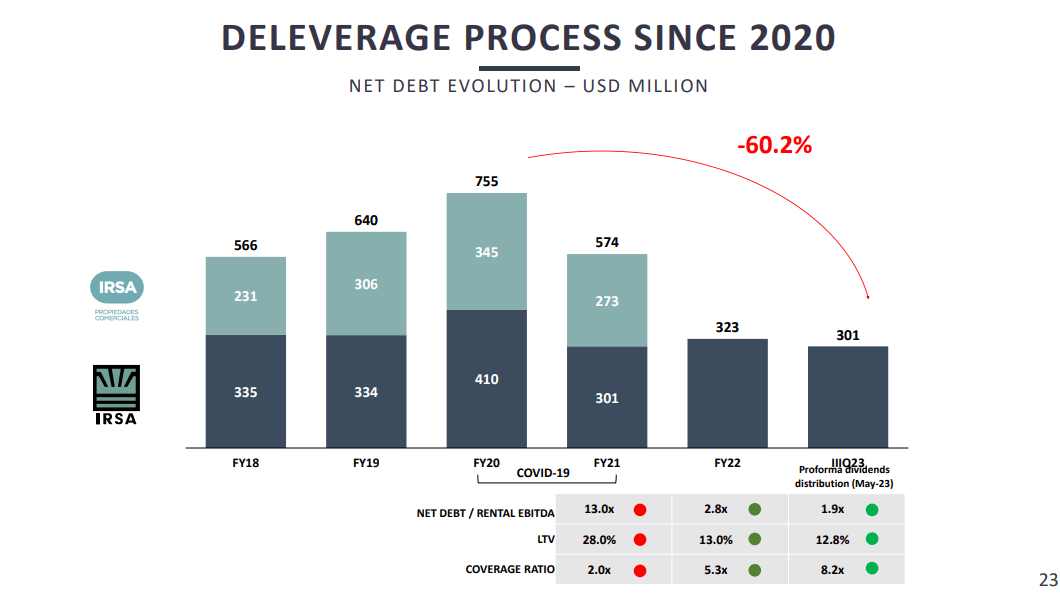

One crucial aspect is the successful deleverage. Despite the draconian lockdowns, IRSA weathered the storm and reduced its debts. Loan to value dropped significantly after the merger between IRSA and IRCP in 2021. IRSA held 21.7 % of Condor Hospitality Trust (CDOR), which liquidated to reduce its debts. The image below shows the deleveraging process since 2020:

{kind=link}

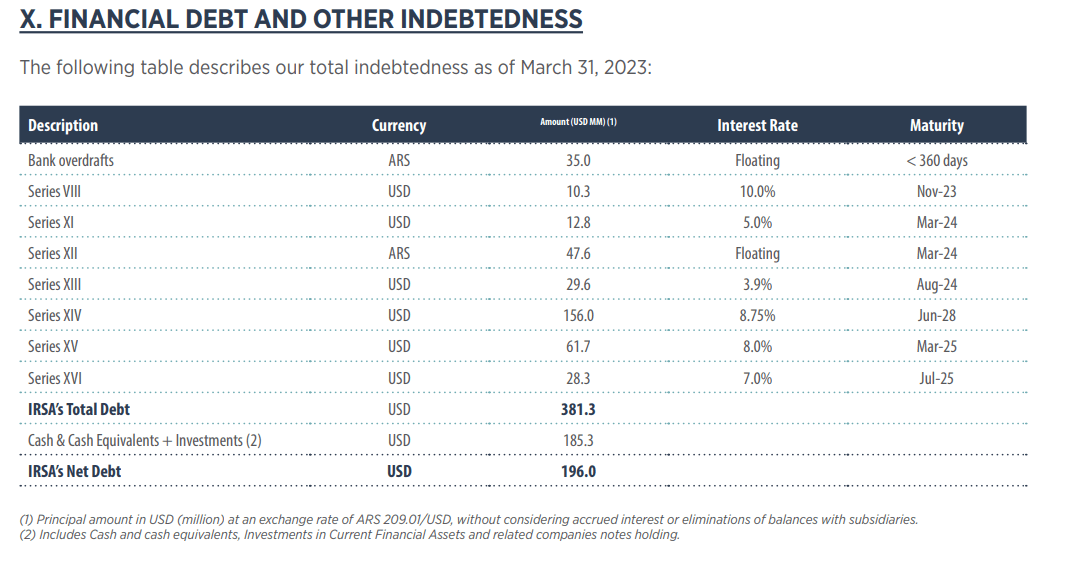

The company's debt maturity is well distributed in the next five years. The table below from the last corporate presentation shows the current debt structure:

{kind=link}

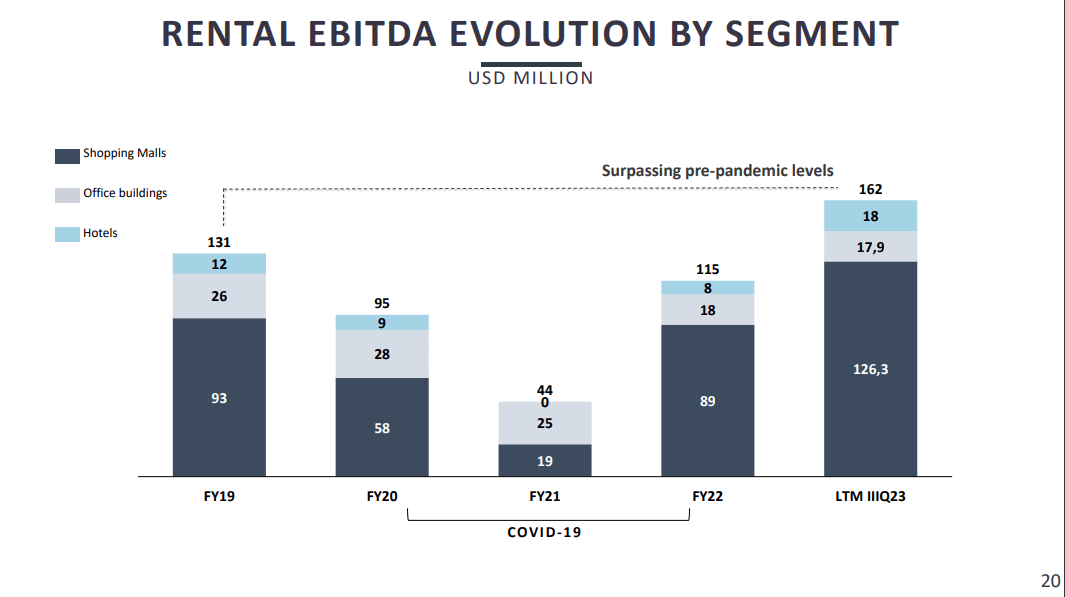

In five years, IRSA must repay less than $ 50 million annually. This is less than 30% of the company's EBITDA. In 2028, it is due $ 156 million in debt. I expect the company to repay it earlier because of its growing profitability. The image below is showing the company's EBITDA for the last four years:

{kind=link}

The company's EBITDA exceeds the levels from 2019 measured in USD. Only the office segment is stagnant.

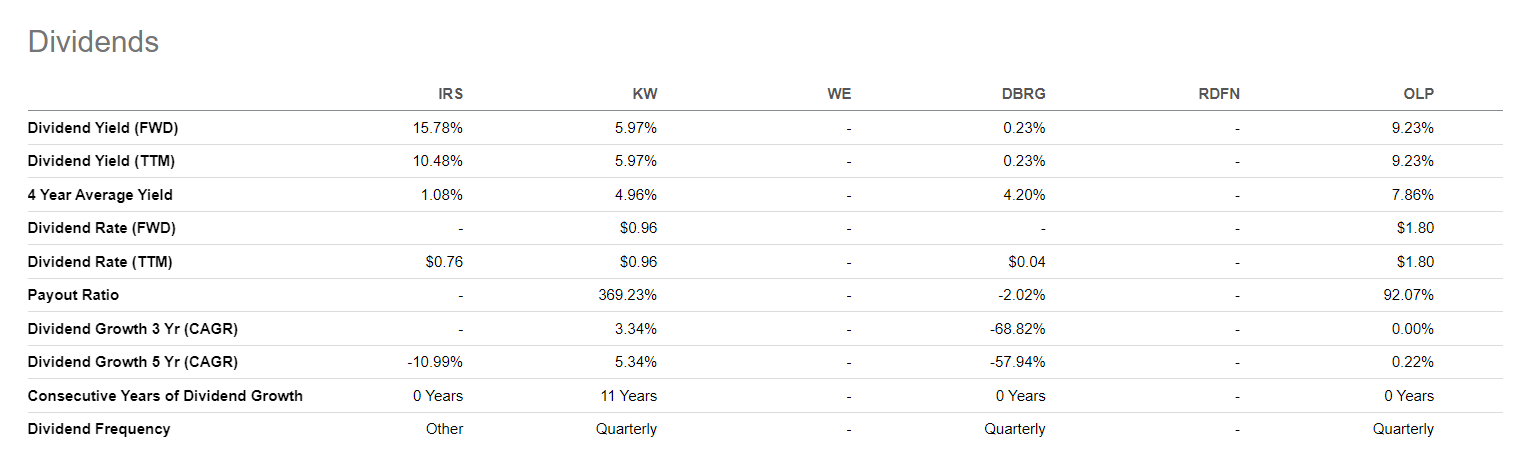

IRSA distributes dividends. Like the other Argentinean companies, the yield is higher than its US peers. The table below compares IRSA dividend metrics with other REITS:

{kind=link}

The drawback is the dividend frequency. IRSA had in the past periods without paying dividends.

Valuation

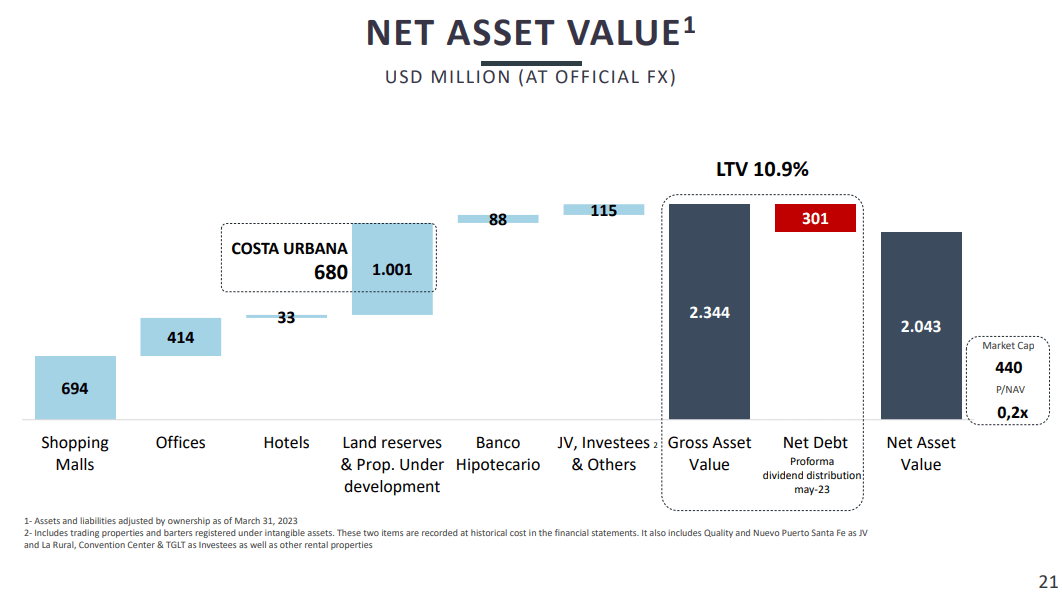

I usually use an AFFO 2-stage discounted cash flow model to estimate REIT value. IRSA is a different case due to the company's portfolio and Argentinean economic anomalies. I return to the basics in such cases, measuring the company's NAV. The image below is from the Q2 company's presentation.

{kind=link}

Based on the above calculations, IRSA NAV is $ 2.04 billion, while the company's market cap is $ 1.27 billion. Let's now use my approach to NAV.

The value of Costa Urbana is understated at $ 680 million. Assuming a price of $ 1000 per sqm of buildable land, the value of Costa Urbana would rise to $ 900 million. IRSA owns a 37.7 % stake in Banco de Credito y Securitization and 29.91 % in Banco Hipotecario; the latter owns 62.3 % of the former. That adds another 18 % equity stake for IRSA. I use total company liabilities in NAV because if I subtract only the debt obligations, I might ignore another heavy drawback. In IRSA's case, deferred taxes are valued at $ 728 million.

To summarize:

- Shopping Malls $ 694 million

- Offices $ 414 million

- Hotels $ 33 million

- Land reserves (ex Costa Urbana) $ 320 million

- Costa Urbana $ 900 million

- Banco Hipotecario stake $ 53 million

- BACS stake $ 424 million

- Cash $ 72 million

- Total receivables: $ 108 million

- Total Liabilities: $ 1.26 billion

IRSA Inversiones NAV = $ 1.758 billion

Market Capitalization = $ 1.27 billion (on Sept 06 2023)

I used the book values of IRSA's stakes in Banco Hipotecario and BACS from last quarter's reports. I have been conservative in valuing other company assets, such as malls and office buildings. However, IRSA is an excellent offer, even at the current price.

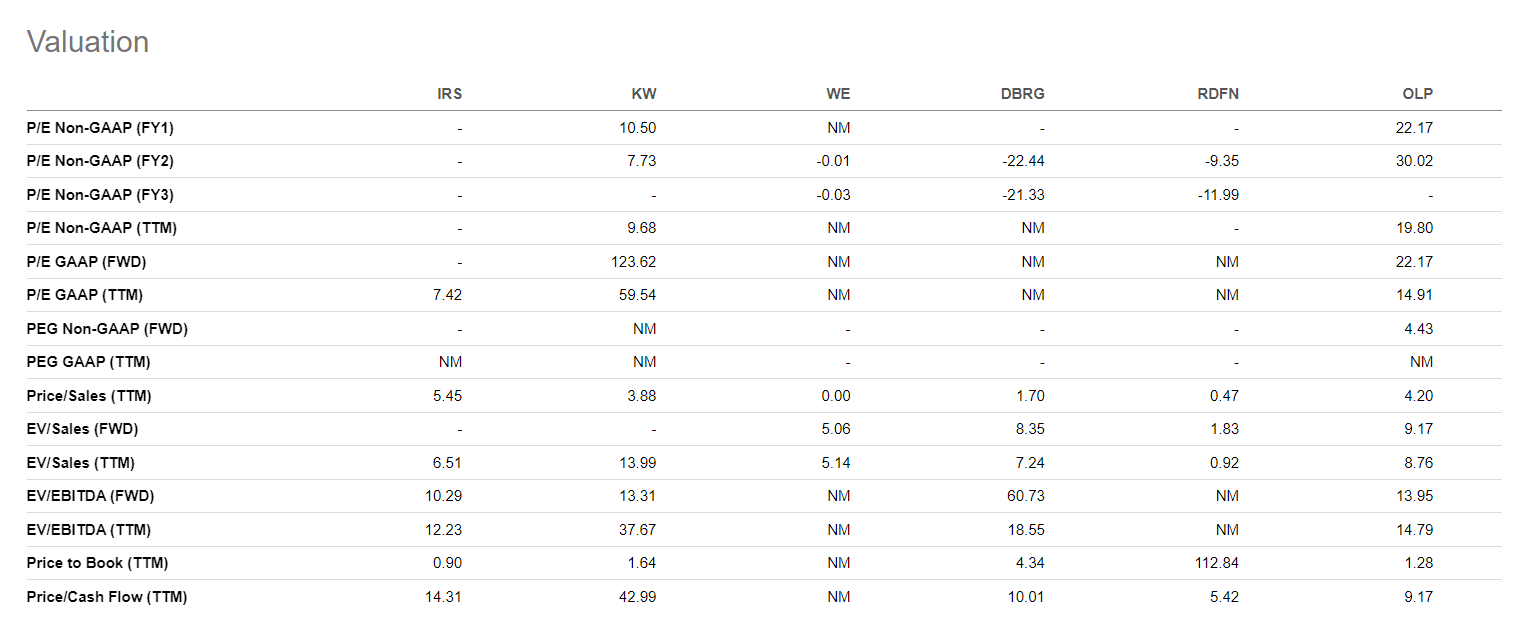

The table below shows how the company compares against its peers:

{kind=link}

To weigh up IRSA against similar companies is a difficult task due to the lack of Argentinean or LATAM REITS listed in US exchanges. They said comparing IRSA against WeWork (WE) is like apples to oranges. Based on the Price to Book, the company is cheaper, but EV/Sales stand in the middle.

Risks

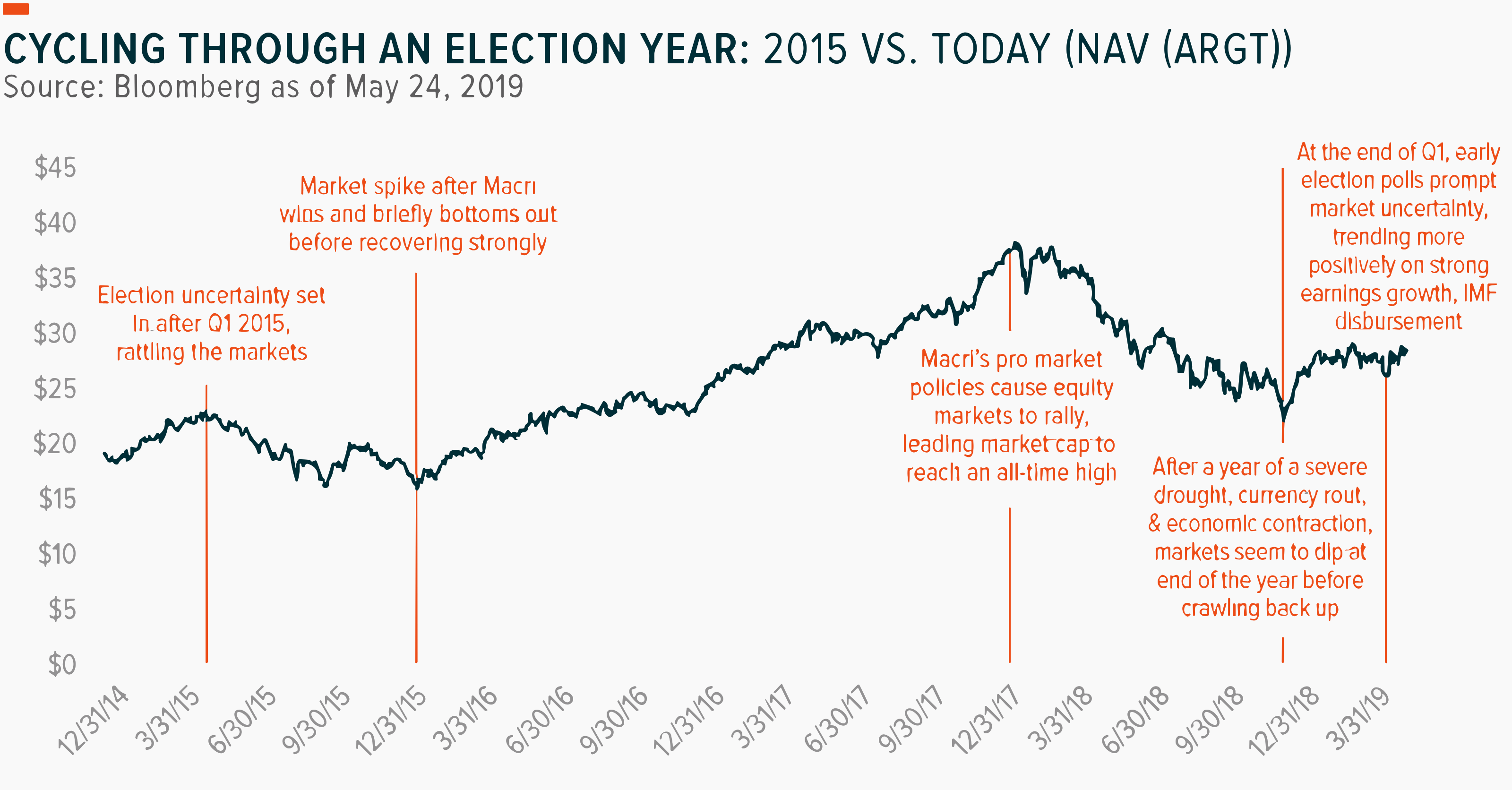

IRSA's primary risk is an Argentinean company operating in Argentina. The latter, for curious investors, is a blessing. The risk brings volatility. As common wisdom says, volatility is the investor's prime enemy; however, if you seek high returns, the volatility is the admission fee to the party. The Argentinean stocks represent a rare opportunity. We are still at the beginning of the new potential boom cycle. The chart below from Global X represents the correlation between Argentinean equities and presidential elections:

{kind=link}

We were in a similar situation as in 2015, just before Mauricio Macri's win . Milei's success on PASO adds credibility to my expectations for pro-market political change in Argentina. Hence, the downside risk is still present but is relatively limited.

The other risks are interest rate changes, poor economic growth, and demographic issues. Changes in interest rates are the most variable parameter that directly impacts property prices and, hence, REITS' share prices. Interest rates determine the cost of capital and the company's profit margins. Often, even with cheap money (low-interest rates), if the region and city are going through a period of stagnation - high unemployment and low or zero economic growth, property prices will decline, and demand for rental space will stagnate.

The demographics of the region determine long-term trends. However, the devil is in the details - ethnicity and age structure decide which properties will be most in demand in a particular area. High numbers of young and working people create economic growth accompanied by increasing business activity. This, in turn, stimulates demand for real estate.

From all the mentioned risks, IRSA is highly dependent on economic growth or lack of such. In the short term, demography and interest rates can not compensate for economic stagnation.

Conclusion

IRSA is a strong buy because it offers the asymmetry of an option but without an expiration date. I have been a shareholder for the last 12 months. I plan to keep the position if the pro-market president wins the elections in October. That scenario carries a lot of credibility after Milei's PASO win. IRSA is well positioned to benefit from Buenos Aires' demography and Argentinean economic peculiarities. Runaway inflation pushes the depositors to seek shelter in equity markets and real estate. The company has a robust balance sheet with well-distributed debt maturity. The current price based on NAV is an excellent opportunity to buy prime real estate for cents on dollars.

For further details see:

IRSA Inversiones: A Call Option On Premium Estates Without An Expiration Date