OKE - Is 6%-Yielding ONEOK An Unbeatable S&P 500 Income Play?

2023-10-24 15:00:46 ET

Summary

- ONEOK, Inc. is making the case that it's the best high-yield stock in the S&P 500 based on several criteria.

- The company has a solid financial track record, with a dividend that hasn't been cut in over 25 years and a projected 9% free cash flow yield in 2025.

- ONEOK's merger with Magellan Midstream Partners makes it one of the best-diversified midstream players in North America, offering growth and stability.

Introduction

Earlier this week, the 10-year government bond yielded 5.0%, the highest number since 2007!

Bloomberg

While rates have come down a bit since then, it shouldn't surprise anyone when I say that we're in an environment of elevated rates.

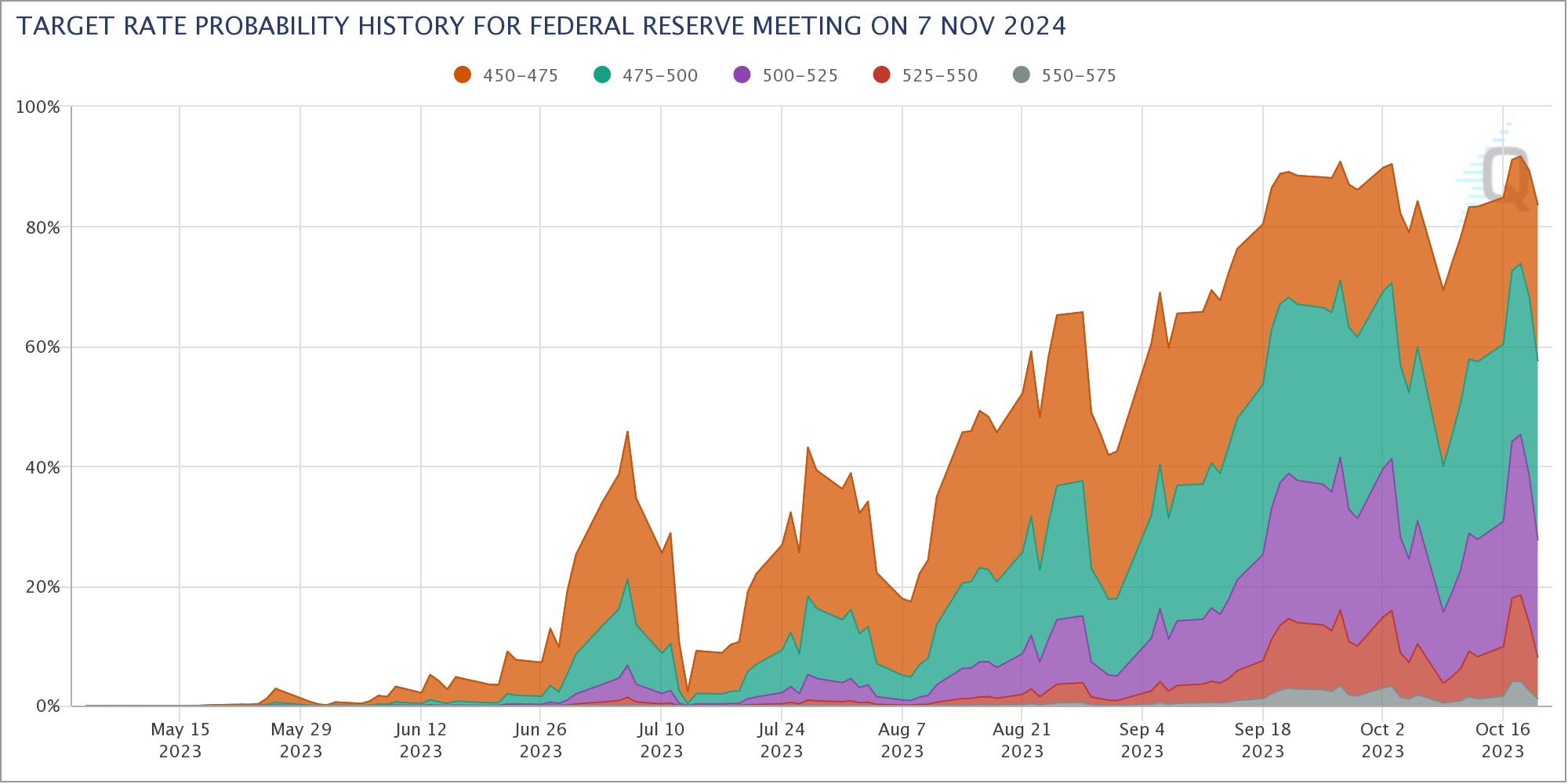

Even worse, as I discussed in a recent article , the market expects rates to remain elevated. The implied chances that the Federal Reserve funds rate is above 4.50% on November 7, 2024, has risen to more than 80%. During the summer, that number was roughly 0%.

{kind=link}

When adding elevated inflation, it makes sense that people are seeking higher yields on their investments.

Although it's tough to compare dividend growth stocks to bonds (one has a steadily growing payout, the other hasn't), I cannot disagree with investors who make the case that they require a higher yield in this environment.

The bottom line is that cash flow-dependent investors need a higher yield.

That's where ONEOK, Inc. (OKE) comes in, one of the few midstream companies that is a C-Corp, meaning investors do not have to deal with K-1 forms.

The company makes the case that it's the most attractive high-yield stock in the S&P 500, which we will discuss in greater detail in this article.

So, let's get to it!

The Best High-Yield Stock In The S&P 500?

Making the case that ONEOK is the best high-yielding S&P 500 stock is quite a statement.

ONEOK has done it.

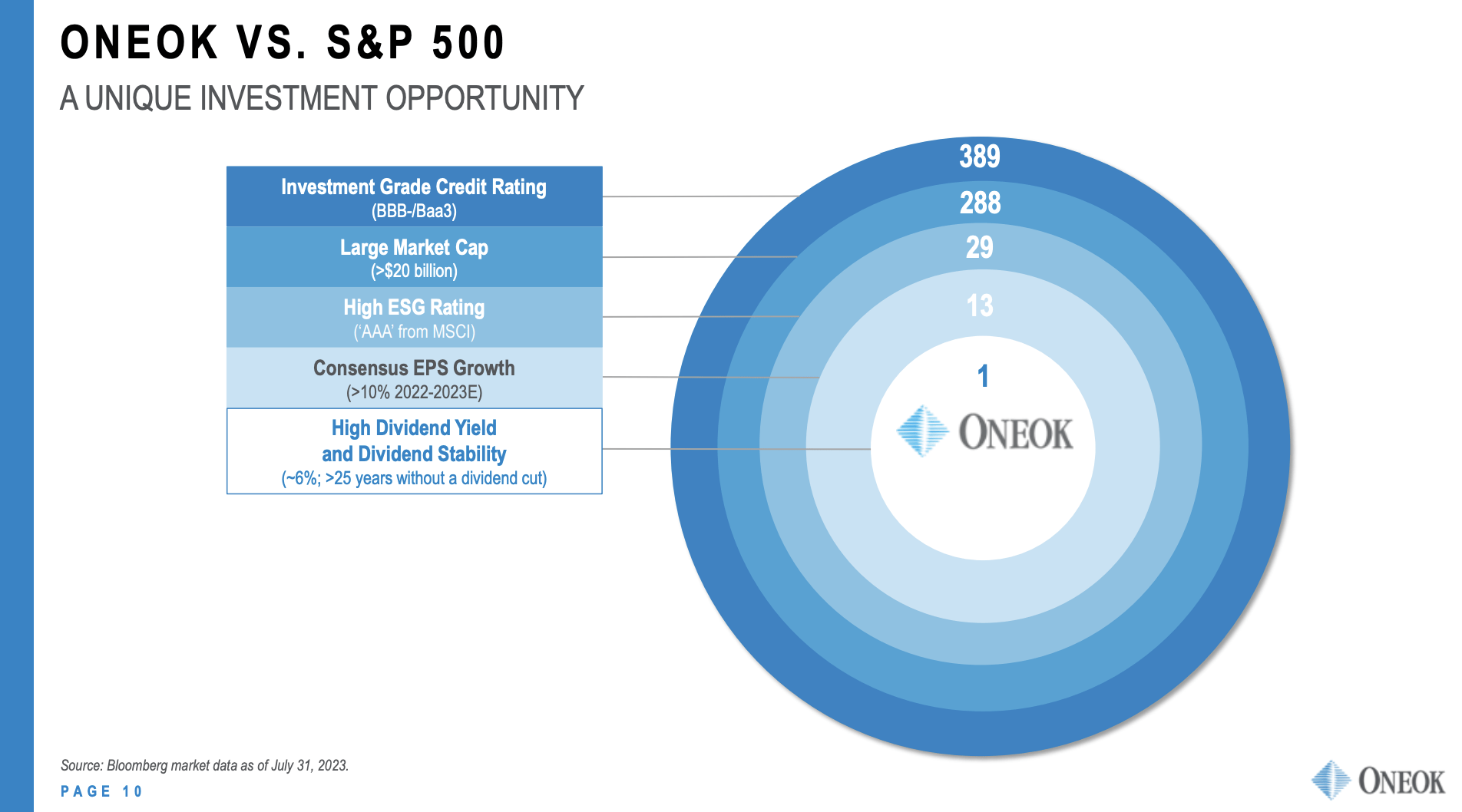

In a recent investor presentation, the company made the case that it's the best high-yield stock in the S&P 500 based on a number of criteria.

- The company has an investment-grade rating. This reduces 500 companies to 389 - as of July 31, 2022.

- The company has a market cap of over $20 billion, which erases another 100 companies. In other words, we're filtering out smaller companies.

- An AAA ESG rating. Bear in mind, this is an environmental, social, and governance rating, NOT a credit rating! Personally, I'm not a fan of including this rating, as it's very hard to assess how "ESG" a company is. Anyway, it reduced the company basket to just 29 companies.

- OKE is expected to grow its earnings per share by more than 10%. In this environment, not a lot of companies can compete with that. Hence, we're now left with just 13 companies.

- Of these 13 companies, just one company has a yield of 6% or more. That company is OKE.

{kind=link}

What the company has done here is fully legit. However, I'm not a fan of including the ESG score in this process. I also don't like excluding companies smaller than $20 billion. I would have gone with a $5 to $10 billion cutoff, but that's my preference.

Nonetheless, the company isn't deceiving us.

I also made a screener to prove that.

Here are the criteria that I used:

- The company needs to be an S&P 500 member.

- It needs a market cap of at least $10 billion.

- The dividend yield needs to exceed 5%.

- At least 10% year-on-year EPS growth.

My findings showed five companies. Three of them are REITs, where the focus is NOT on earnings due to the importance of depreciation of assets and other factors.

- ONEOK

- Alexandria Real Estate ( ARE )

- Kimco Realty Corporation ( KIM )

- Prudential Financial ( PRU )

- VICI Properties ( VICI ).

So, yes. It is fair to say that based on a few key criteria, OKE is indeed one of the best high-yield plays on the market.

The problem is that a lot depends on year-on-year EPS growth. That's a very specific number. It excludes all companies that are seeing temporary dips. It includes companies that might benefit from a temporary improvement.

What we need are players with consistent growth, which is why we need to take a closer look.

Consistent Dividend Growth Opportunities

OKE's stock price returns are not very consistent. The company has been through a number of very volatile cycles.

Over the past ten years, OKE shares have returned 161%, including dividends. This performance beats the Vanguard High Dividend Yield ETF ( VYM ) and the energy sector ( XLE ).

Unfortunately, investors have been through two massive sell-offs. In 2014-2016, slower growth expectations caused investors to flee the midstream industry, as mass defaults were feared. These fears did not materialize.

In 2020, the stock sold off as demand for fossil fuels imploded due to lockdowns.

Since then, the company has made a strong comeback, supported by demand, growth, and increasing safety and stability.

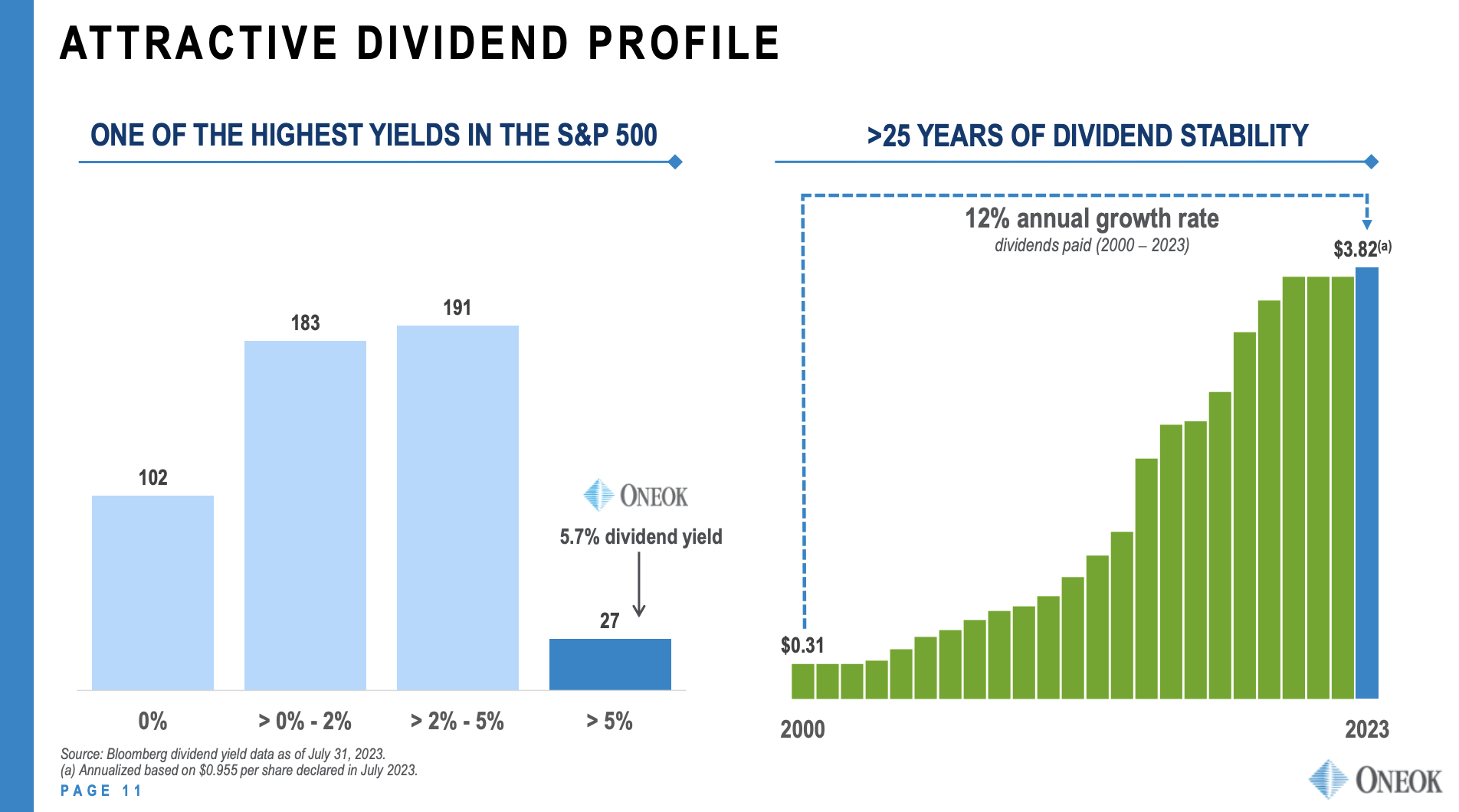

The good news is that, despite stock price volatility, the OKE dividend hasn't been cut in more than 25 years. Since 2000, the dividend has been raised by 12% per year, making it one of the few companies in the S&P 500 that offers a yield over 5%.

{kind=link}

OKE currently pays a $0.955 dividend per share per quarter. This translates to a 5.7% yield. It's protected by a 70% payout ratio.

In 2025, the company is expected to generate $3.5 billion in free cash flow, which would translate to a 9% free cash flow yield, paving the road to consistent dividend growth with support from buybacks.

Furthermore, the company benefits from the stability that comes with the midstream industry. Unlike oil and gas producers, OKE relies on volumes, not necessarily commodity pricing.

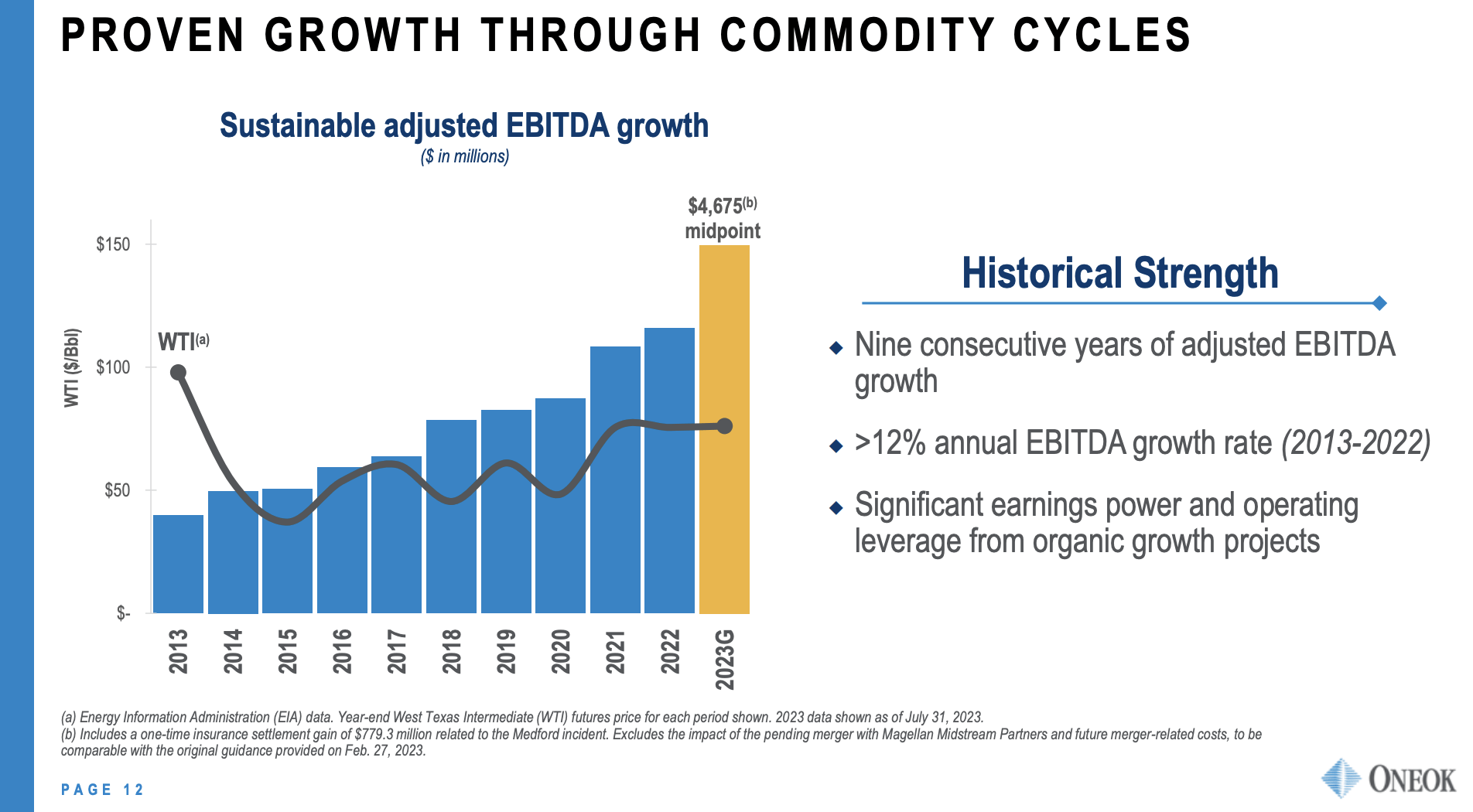

It allowed the company to consistently grow its EBITDA despite severe oil price volatility over the past ten years. EBITDA has grown by 12% per year in the 2013-2022 period. Please note that 2023 expectations exclude the merger with Magellan Midstream Partners.

{kind=link}

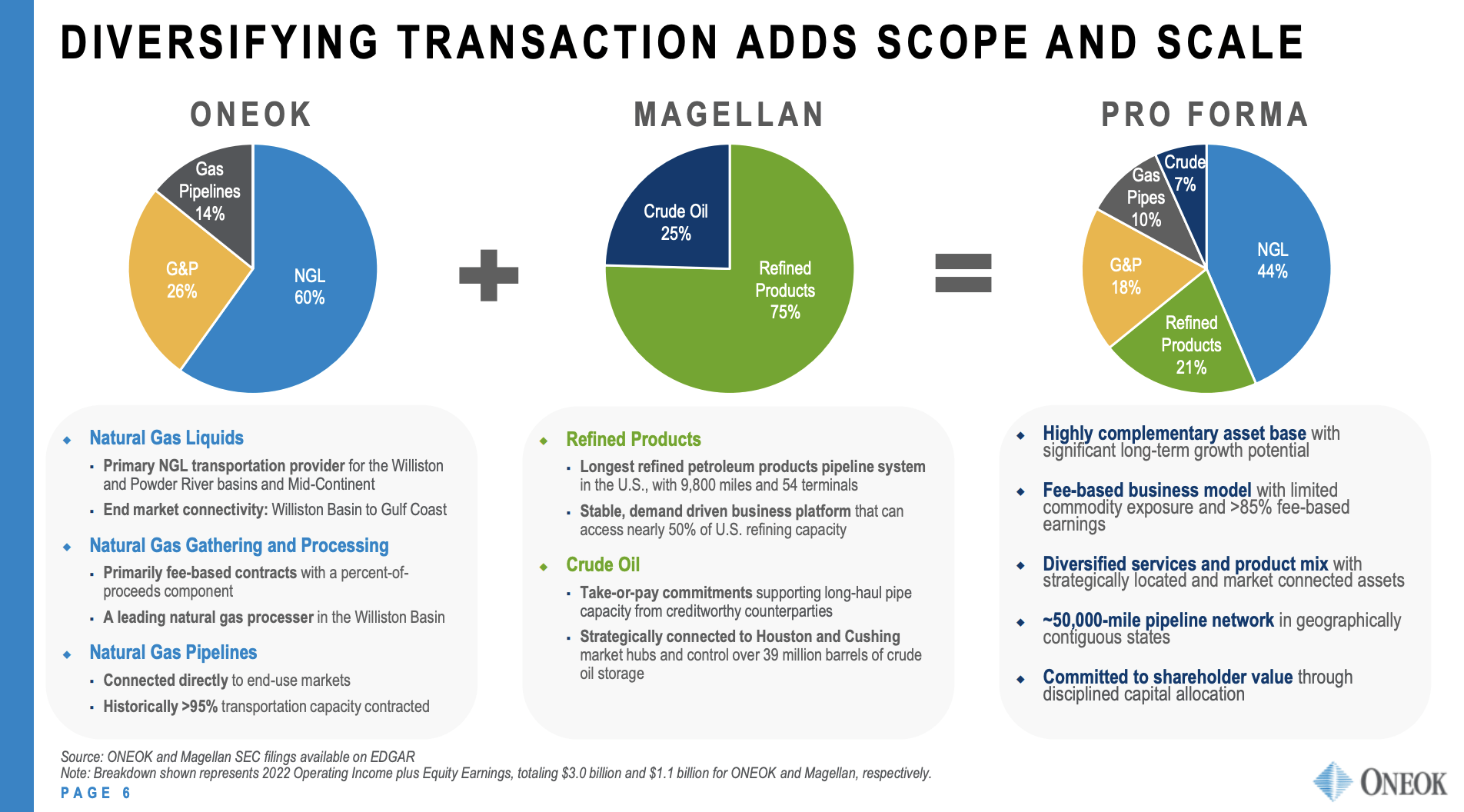

When adding the recently-approved merger with Magellan, the company turns into one of the best-diversified midstream players in North America.

The combined company has a 50-thousand-mile network with 44% natural gas liquids exposure. It has 21% exposure in refined products, 18% gathering and processing exposure, and 7% crude oil exposure.

{kind=link}

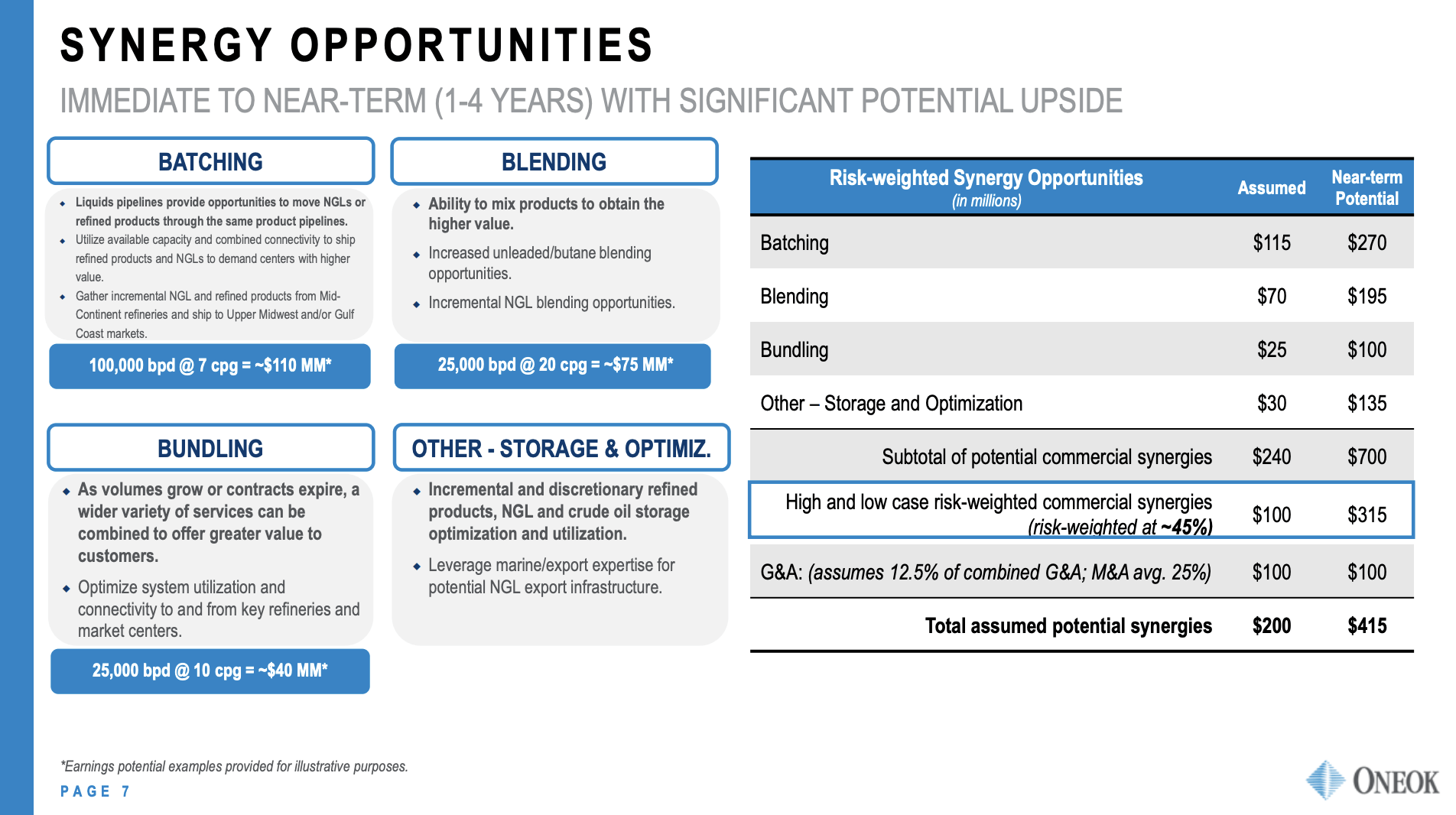

Furthermore, ONEOK and Magellan are actively exploring opportunities in batching, blending, and bundling.

- Batching involves mixing products like propane and unleaded fuels within their pipelines, optimizing efficiency.

- Blending focuses on cost-effective transportation, reducing the need for trucking.

- Bundling combines various services, such as transporting natural gas, NGLs, and crude oil for producers, creating portfolios of opportunities and contracts.

{kind=link}

These strategies aim to optimize the use of existing assets, with the potential for considerable operational synergies.

Furthermore, ONEOK anticipates minimal capital needs in the short term to capture the outlined synergies, with some projects requiring little to no investment.

As they progress, they might explore low-return projects, followed by higher-return projects for expanding and extending their systems into new markets.

The synergy-driven capital allocation strategy aligns with their goal of achieving quality scale and high returns.

An Attractive Valuation

OKE, which has an investment-grade balance sheet with a BBB rating and a sub-4x 2024E EBITDA net leverage ratio, is attractively valued.

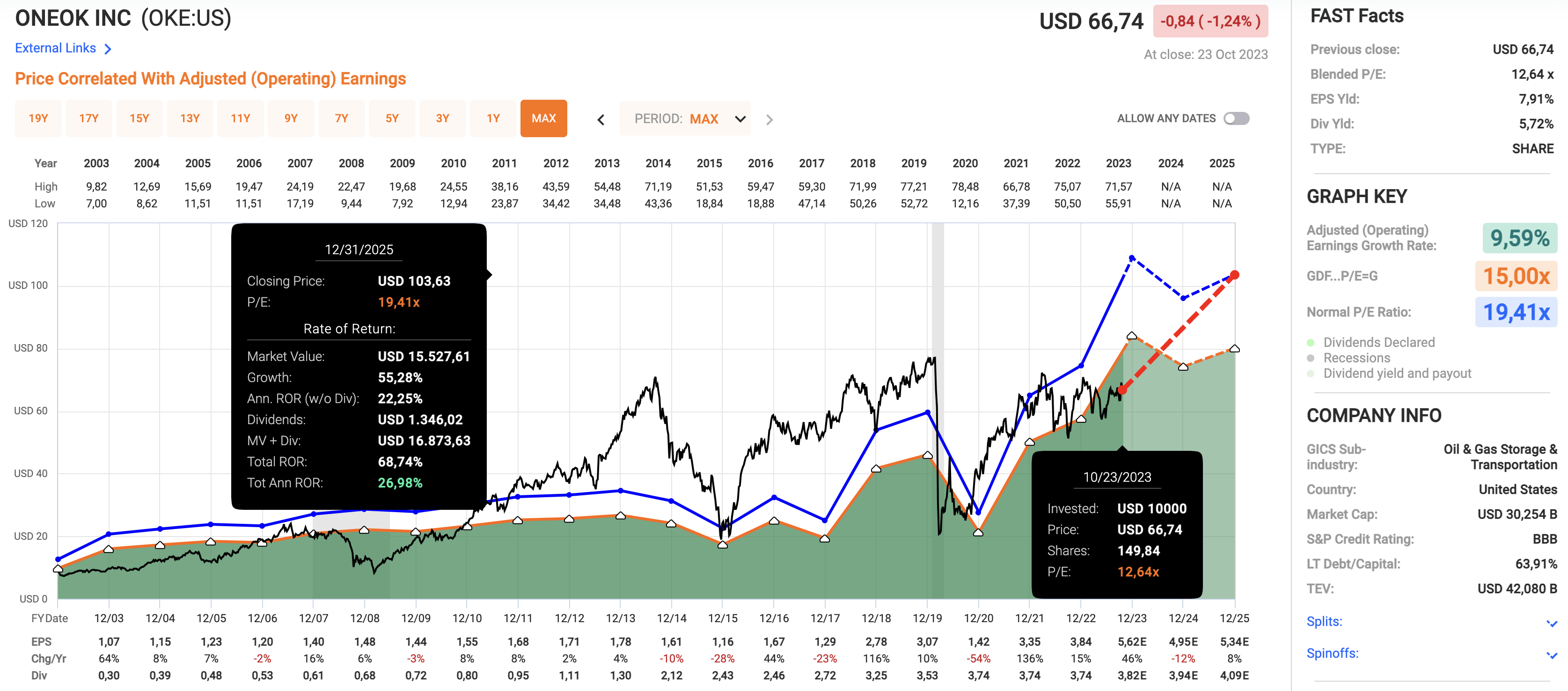

OKE is trading at just 12.6x adjusted earnings. Its longer-term valuation is 19.4x earnings (that's the blue line). The company has consistently traded at a premium before the pandemic, as earnings were low and the market was betting on better results down the road.

That has happened. Now, OKE is trading at a discount.

{kind=link}

If the company returns to its valuation, it has the potential to return 26% per year through 2025. That's not necessarily a prediction, just a theoretical assessment based on a fair valuation multiple and expected growth rates (seen in the lower part of the chart above).

Even a 15x multiple would, technically speaking, lead to a 15% annual return over the next three years.

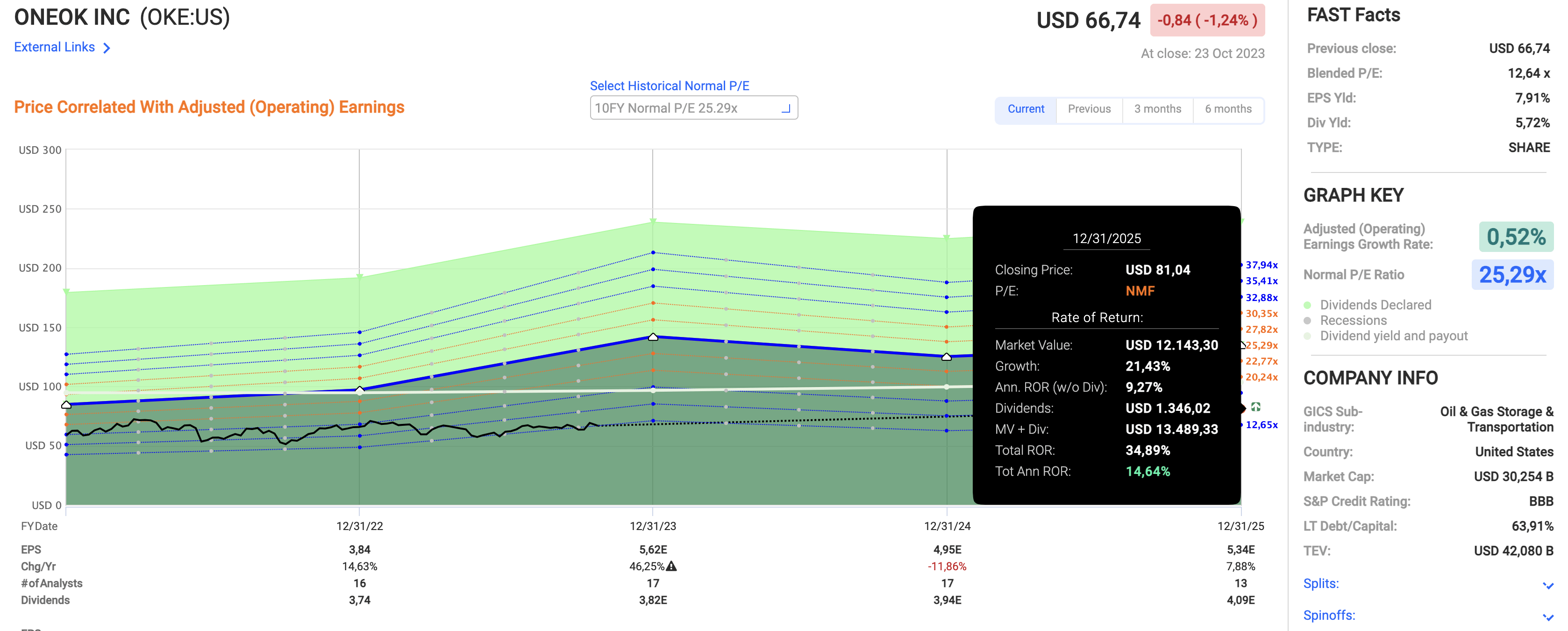

{kind=link}

The current consensus price target is $69, which is 4% above the current price.

With these numbers in mind, we need to take them with a grain of salt. I believe that a fair price target of $75 (12% above the current price) is warranted. In the years ahead, I expect the company to return at least 10% to 12%, including its dividend.

Investors looking for midstream exposure without having to invest in companies with an MLP structure may benefit from buying OKE. It has a great yield, a stellar business with synergy opportunities, and a high probability of more-than-decent returns over the next few years.

The only thing investors need to keep in mind is that OKE (like all of its peers) is volatile. Be aware of these risks when assessing a suitable position size.

Takeaway

In today's environment of rising bond yields and persistent inflation, ONEOK shines as a high-yield investment option.

With a dividend yield of 5.7% and a solid financial track record, OKE offers compelling reasons to be considered one of the best high-yield stocks in the S&P 500.

OKE's strengths include its investment-grade rating, substantial market cap, and an AAA ESG rating, although the latter may be subjective.

What sets OKE apart is its remarkable consistency. The company hasn't cut its dividend in over 25 years, and with a 70% payout ratio and projected 9% free cash flow yield in 2025, it's well-positioned for sustained dividend growth.

Moreover, OKE's diversification and merger with Magellan make it one of the best-diversified midstream players in North America, poised for growth and stability. The stock appears attractively valued, potentially offering substantial returns.

For investors seeking high yields and exposure to the midstream sector, OKE is a strong candidate. Just remember, it's not without volatility, so consider your risk tolerance when determining your position size.

For further details see:

Is 6%-Yielding ONEOK An Unbeatable S&P 500 Income Play?