SPTS - Is A Soft Landing Becoming More Or Less Likely?

Summary

- Falling inflation makes a soft landing seem more plausible.

- But strong employment growth makes it seem less plausible.

- Markets are desperate to corral or create a 'good news' outlook.

- But risk remain two sided; the Fed is serious and it is not bluffing.

Badda Boom - Badda bust?

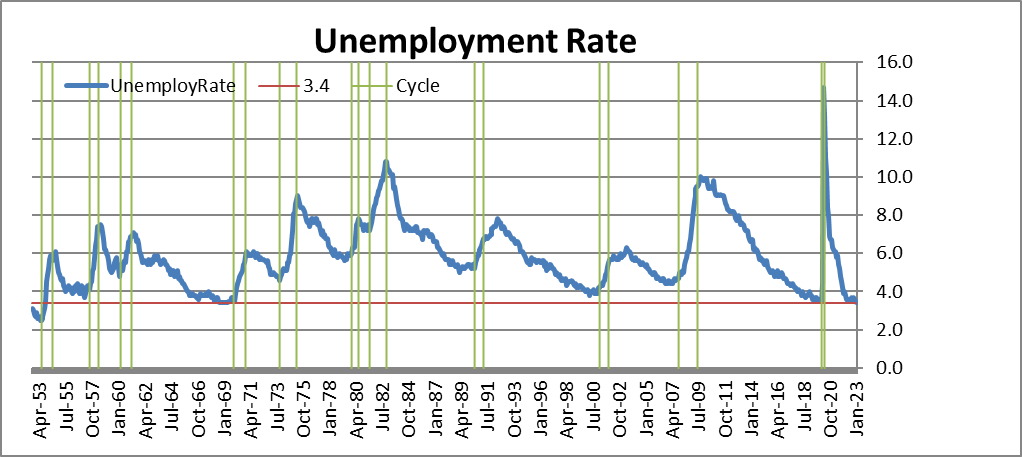

Here we go again. The debate is heating up over the prospects for a soft landing. Inflation has come down and job growth has turned out to be exceptionally durable with the unemployment rate, in the teeth of a Fed tightening cycle, ticking down slightly lower to reach a 50 year low. Under Trump the unemployment rate had gotten to 3.5% then COVID struck and the unemployment rate surged. Now, in this recovery, we have returned the unemployment rate to 3.5% and last month it just ticked down to 3.4% even in the midst of this Fed tightening cycle! To find a lower rate of unemployment you have to turn the calendar back nearly 70 years (to October of 1953). Can that level of unemployment be sustained without causing inflation? So far it never has…

{kind=link}

Note that when unemployment reaches its cycle low…it usually does not stay there for very long…So, is shooting for a soft-landing here folly?

Inflation is cooling - will it continue?

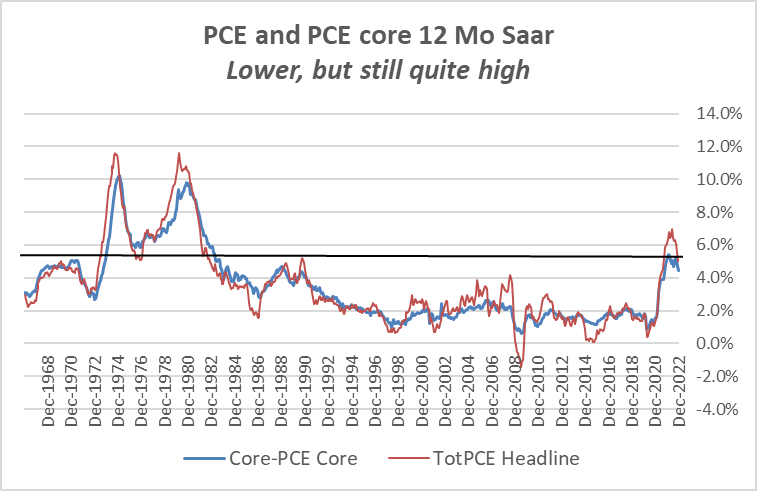

Meanwhile, inflation has broken lower. The Fed targets the PCE deflator. Core PCE peaked in this cycle at 5.4% and in December of the 2022 the year-over-year rate has fallen to 4.4%. The headline for PCE peaked at 7% but in December it's running at a 5% annual rate. The headline has seen a drop in inflation of two percentage points from its peak while the core has seen a drop of one percentage point. By comparison the core CPI peaked at 6.7% and in December it's running at a 5.7% pace, also a deceleration of one percentage point. The CPI headline at its highest pace reached 9% and in December is running at a 6.4% annual rate - that's a drop in inflation of 2.6 percentage points, more than for the PCE headline. But the CPI still runs hotter than the PCE. Will inflation keep falling?

Is this enough progress for the Fed to slow down?

{kind=link}

On balance both the inflation reports show inflation is falling; both show that there's a bigger decline for the headline than for the core. This clearly traces back to the role of energy prices. That conclusion is somewhat less reassuring since oil remains 'in-play' in the Russia-Ukraine war and in other geopolitical matters. Oil prices have stopped falling and have started to rise slightly. The strong dollar weakened commodity prices generally.

What 2% compliance looks like for the core

Inflation will fall...but how much? (Haver Analytics and FAO Economics)

{kind=link}

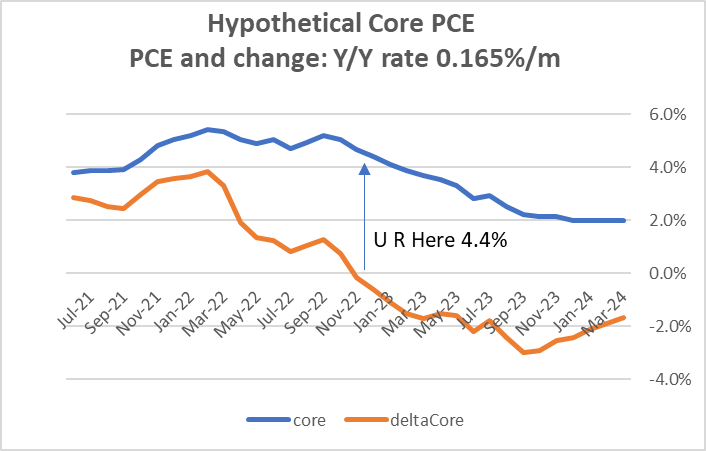

Blind man's bluff- This chart imposes monthly increases of 0.165% on core PCE for every month after Dec 2002 (last hard data point). That puts the annualized PCE Core at a 2% pace monthly. The chart then plots the resulting Yr/Yr inflation rates by month on actual and hypothetical data through March of 2024. The last three-months are at 2% by the assumption of 0.165% per month. The chart shows how the loss of historic excess inflation data would play though the Yr/Yr PCE calculations if we instantly got to 2% inflation in January (not remotely likely). Note that in the last 23 months only two months have had core PCE gains that are this low. The PCE is hardly on the brink of doing this. Extrapolating the downtrend is a bad idea. The chart demonstrates where the historic inflation rates are highest and lowest by showing where their dropping out of the Yr/Yr calculation has the most impact. For example, on these assumptions year-on-year core inflation is at 2.8% in June and 2.9% in July of 2023. It falls to 2.5% in August then to 2.2% in September. This means that by September the historic inflation bubble is essentially gone. From Sept on, we will be measuring inflation based on what monthly news breaks without the baggage of excess historic inflation boosting the index. With the job market so tight, does anyone believe that inflation would be so easily controlled in 2023 and beyond?

Jettisoning history is beneficial...but not enough - Running the calculations forward to eliminate historically high monthly inflation numbers will bring inflation down - and it already has- as this exercise demonstrates. But to hit 2% the economy must also generate persistently low new monthly numbers- right now that seems unlikely. Averaging a gain of 0.25% each month is a 3% annual rate. Another way to think of it is that each quarter needs two monthly gains of 0.2% and one gain of 0.1% to hit a 2% annual rate. Still, many cite low recent inflation numbers. They are in fact better than the older historic figures. But over three-months the core PCE is gaining at a 2.9% annual rate and over four-months it is gaining at a 3.6% annual rate. And this is during a period of commodity price weakness - and that is not good enough. When you think of the Fed bluffing, keep these calculations in mind. Who do you think is bluffing?

Embrace, or rebuff, the bluff?

The markets have begun to question Fed policy. Some in markets claim that the Fed is bluffing. This is a curious position because in all my years of Fed-watching - and I've had quite a few of them - I've never had occasion to think that the Fed was bluffing. This allegation is something new. In fact, bluffing is one thing that I think central banks generally do not do; central banks do make mistakes. They make bad forecasts. They sometimes make bad policy. But all of that is different from bluffing. To say that the central bank is bluffing is to say that it does not intend to do what it says it is going to do. Typically, that would generate a credibility problem. In this case, I think the allegation is a device used by the markets to try to make their own position and their own forecasts seem more viable. The point is this: if the Fed were bluffing, that would imply that the Fed doesn't think it really needs to raise rates as much as it has said. It would also imply that the Fed may, in some sense, even have the same forecast as the markets. This is an interpretation that the markets would like to foster to reinforce their own view of what the economy needs and what the Fed will do. What's not clear to me is what the markets think that the Fed gains from bluffing. If the markets are right and if the Fed's not going to raise rates as much as it plans, and if the Fed thinks inflation really is going to fall faster, why shouldn't the Fed just say that?

Mr Softie… or not?

The two developments have put the notion of a soft landing back on the table are (1) the unexpectedly sharp and continuing drop in inflation coupled with (2) resilience in the labor market. Janet Yellen, former Fed Chair, and current Treasury Secretary in the Biden Administration, has said that the labor market this strong we don't need to have a recession. Frankly I don't see the logic in that. If the Fed is not able to slow the economy and slow job gains, then it's unlikely to be able to slow wage growth. If it can't slow wage growth, it's unlikely to be able to contain inflation. In my view the more resilient labor market makes recession seem more likely because that means the Fed will have to raise rates higher and possibly keep rates higher, longer. That's not a recipe for a soft landing.

The soft-landing view comes with baggage

Yellen's soft-landing position is joined by a separate series of arguments that contend that inflation is not a labor market phenomenon. Accordingly, slowing the labor market isn't necessary. This view is confused. I would compare it to the role of firemen. Firemen generally do not start the fire, but they are the ones who put it out. Just because the labor market did not start the inflation, doesn't mean that the job market will not continue to maintain or extend the inflation rate unless wages are controlled. In fact, we've already seen indexed Social Security payments go up relatively sharply this year. Labor is aware there was a rise in inflation and that labor's real wage has been eroded. While it's true that wage gains have been rising faster than they had in previous years, they continue to trail inflation and so even if inflation stabilizes or if the pace is reduced to some extent there may continue to be lingering wage pressures unless something causes labor to feel like it is less in control. And there's nothing like a rising unemployment rate to do that. The hotter the labor market, the more in-control of working conditions labor will be. It does not matter that inflation did not begin in the labor market- that assertion is a red herring.

The real worry is Boom Vs Bust…Badda boom?

The labor market has proved resilient to this point; there's no telling when that resilience will break down or how it will break down. One of the things that continues to bother me is that we are in a strange business cycle. During COVID, policy created the strongest money supply growth that we've had since at least the 1960s and, about a year and a half after that, we are now posting the weakest money supply growth we've had since the 1960s. This includes the first decline in year-over-year M2 that we've experienced over this considerable span. I am concerned that a boom-bust in money supply growth could create a boom-bust in economic activity as well.

Take it easy federales

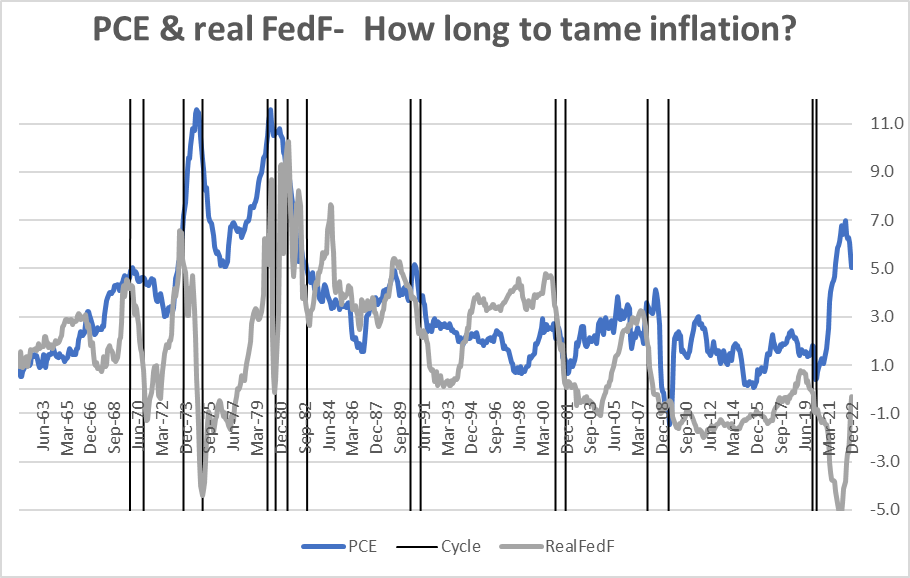

As for those who caution the Fed not to overdo it, in some sense, given the risk that I outline, that may seem to be good advice. But the inflation rate is still running hot. Looking at real interest rates monetary policy really isn't restrictive (yet) despite all the increases in the nominal fed funds rate! So, what's all the fuss about overdoing it? This situation should raise questions about whether rates have been raised enough to continue to push inflation down. Just because the inflation rate has gone down relatively sharply for the headline, and more modestly for the core, isn't to say that is going to continue, as we demonstrate above. Alan Blinder, former Fed vice-chair, has another Op-Ed piece in the WSJ warning the Fed on overdoing it. But the low level of real interest rates should make us wary of whether the Fed has done enough, not too much.

Real rates are still low and inflation is still high... (Haver Analytics and FAO Economics )

{kind=link}

Money growth and the fear factor

The boom-bust cycle in money growth should have us somewhat back on our heels and uncertain about what happens next. Could the recent bust in money growth cause the bottom to drop out? It could. Yet, the sheer strength in job growth has to impress us and make us wonder what policy has to do to slow the growth rate of jobs and assure containment of wage pressures. So, the Fed faces risk on both sides.

As a further matter we should note that we're doing this in the wake of an unusual Covid-inspired recession and with a significant war going on in Europe. And while the Chinese balloon incident may seem somewhat comical, it's also a serious reminder that US-China relations are not in the best of shape and the China is seriously concerned about U.S. policy toward Taiwan. There is a lot to be distracted by on the geopolitical front as well as real and significant effects especially given the restrictions on trade with Russia and on sending technology products to China. Geopolitics have a tangible impact.

Monetary policy stew

Having thrown a lot of stuff in the pot I suppose it's still possible to stir it up and create a soft landing. However, given all these tensions and the unknowns and given all the forces that are in train, including contrary forces and monetary signals that seem to be at odds with one another, the question is whether one really wants to bet that policy can avoid making the big mistake in this confusing situation.

What is the biggest mistake?

The biggest mistake that the Fed could make would be to let inflation get away from it again. However, I'm sure there is my 'opposite number' out there ready to say 'No, recession would be the big mistake.' That's an argument I don't fear. The Fed must make sure that it does enough and must err on the side of doing too much and if that flies in the face of people urging the Fed to take steps to create a soft landing - too bad. Soft landings are the result of soft policies and soft policies are the source of inflation which is what we already have and what we are trying to dispel. That's a mistake the Fed cannot afford to make again so soon. Here and now, recession is the lesser evil.

'Easy' and 'obvious' need not apply

In this process, there are no easy or obvious answers. But, remember, monetary policy has always been about risk management. Central banks always make policy without knowing what the future is going to be. Policy is always about protecting against making a bigger mistake or patching up a past mistake - or both. Sometimes it's clear that direction policy should be and sometimes it's clear the strength that policy must use to lean. In this period, we have a controversy because while the simple economic case is clear 'that the Fed must make sure that inflation is controlled and not restarted' there has developed a strong political lobby for a soft landing even though shooting for that is the much more dangerous strategy.

Key questions

The key questions for policymakers are going to be: (1) Whether they think that this decline in inflation will continue. (2) How they view the strength in the job market as a determining factor for wage determination at a time that the Fed wishes to prevent the wage price spiral. (3) The treatment of mixed signals: the economy is already giving off mixed signals with various signs of weakness in terms of consumer spending and consumer confidence and the housing market vs job strength. (4) The role of the job market…if job and wage growth remain strong that will support income growth which in turn will support spending. And that sort of progression could prevent inflation from continuing to fall.

In conclusion

Although inflation has fallen and even three-month annualized inflation rates now seem to be within a stone's throw the Fed's targets, there is a long way to go before the Fed gets a steady diet of the kind of monthly numbers that would create 2% inflation- both overall as well as for the core. Once inflation has been high it's not that hard to bring it down to a lower level, but it could be very difficult to bring it back down to the targeted level of 2%. Since the start of inflation, the Fed has been arguing it would be temporary and now inflation is falling on its own. But this is not a cartoon; it's real-life; inflation is not going to come skidding down and come to stop at 2% like the roadrunner stopping at the edge of the mesa - beep, beep! So, what risk will the Fed 'manage' and which risk will the Fed 'tolerate?' That is the ultimate question that is still in play.

For further details see:

Is A Soft Landing Becoming More Or Less Likely?