BDRBF - Is Bombardier Stock Still A Big Buy?

2023-08-10 13:23:40 ET

Summary

- Bombardier stock has seen an impressive 173.4% return since June 2022.

- Revenues for Q2 2023 increased by 8%, with a focus on business jets leading to improved margins and reduced debt.

- Despite slower debt reduction in the coming months, the long-term outlook for Bombardier remains positive, with the stock currently undervalued by 23%-53%.

Bombardier ( OTCQX:BDRAF ) is one of the companies I have been following for years. And while previous turnaround plans failed ultimately, the current management is executing a strong and realistic turnaround plan with realistic targets. While I'm not a fan of investing or recommending to invest in turnarounds, the buy rating on Bombardier stock has certainly paid off. In this report, I will be discussing the Q2 2023 results for Bombardier and provide a valuation of the stock.

Bombardier Stock: Impressive Share Price Return

Since June last year I have a buy rating on the stock and that paid off with a 173.4% return. Probably the only thing I regret is not being a shareholder, but sometimes analysts are better at analyzing than investing. Once Bombardier realized that it had to focus its business rather than being diversified in all directions and failing in all of them, the task was easy: Focus on one area, sell the other segments and take the associated debt out of the business and use the proceeds to pay off debt, R&D and business optimization. That has worked. With a focus on business jets we don't only see the business jet manufacturing and service revenues improving, we also see the margins improving and the debt going down.

{kind=link}

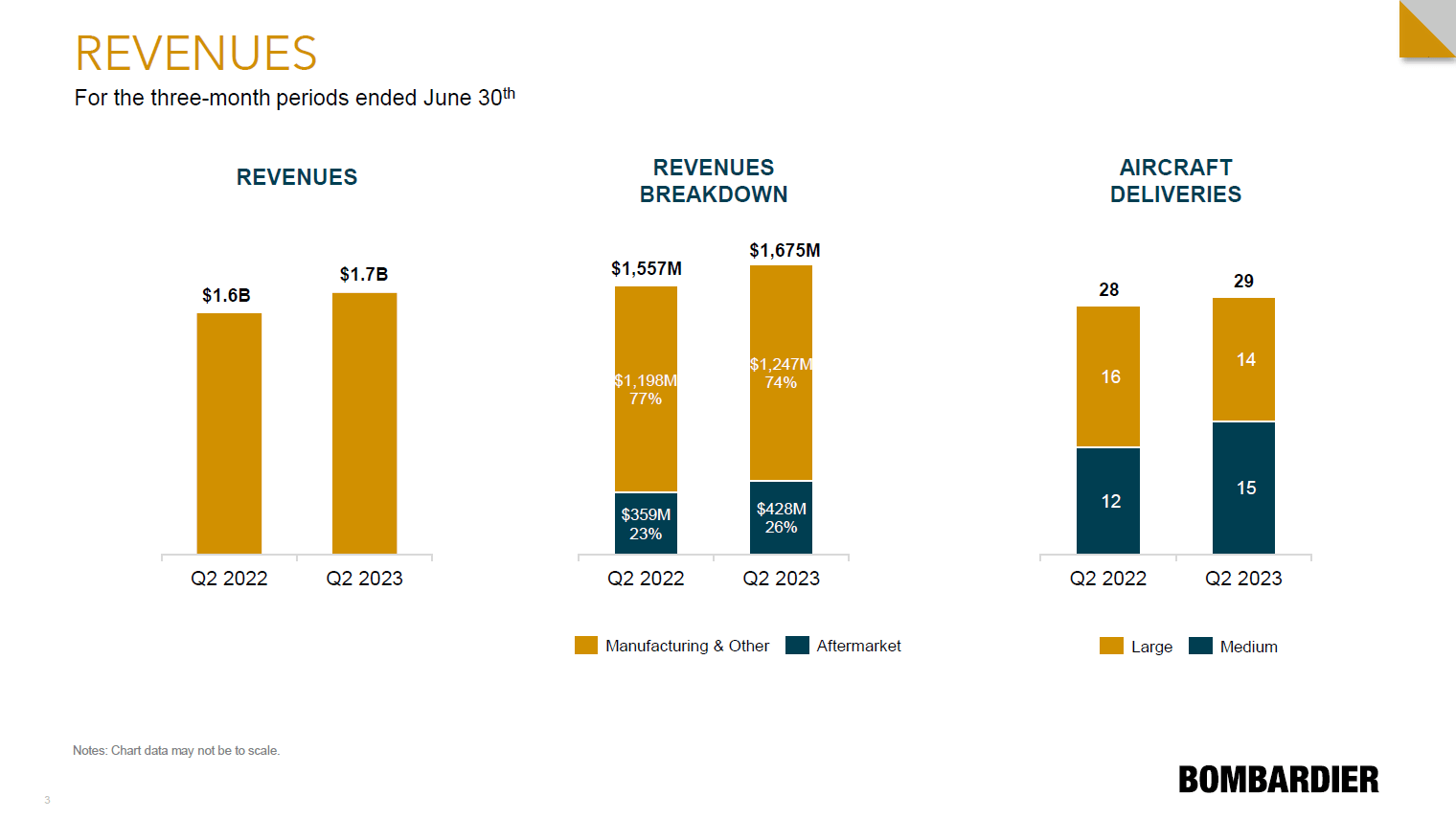

Revenues were up 8% during the quarter to $1.675 billion with the mix between services and manufacturing expanding by 3 percentage points toward aftermarket. Over the past year growing aftermarket sales was driven by improving flight activity, but Bombardier also will at some point reach an asymptote on flight utilization driving the aftermarket sales growth. So, it will need to continue expanding its services footprint, which it already has been doing with new service centers coming online and more service center such as in Abu Dhabi opening in the future. Services revenues grew 19.2% while manufacturing grew 4.6% driven by marginally higher aircraft deliveries, but lower large business jet deliveries.

{kind=link}

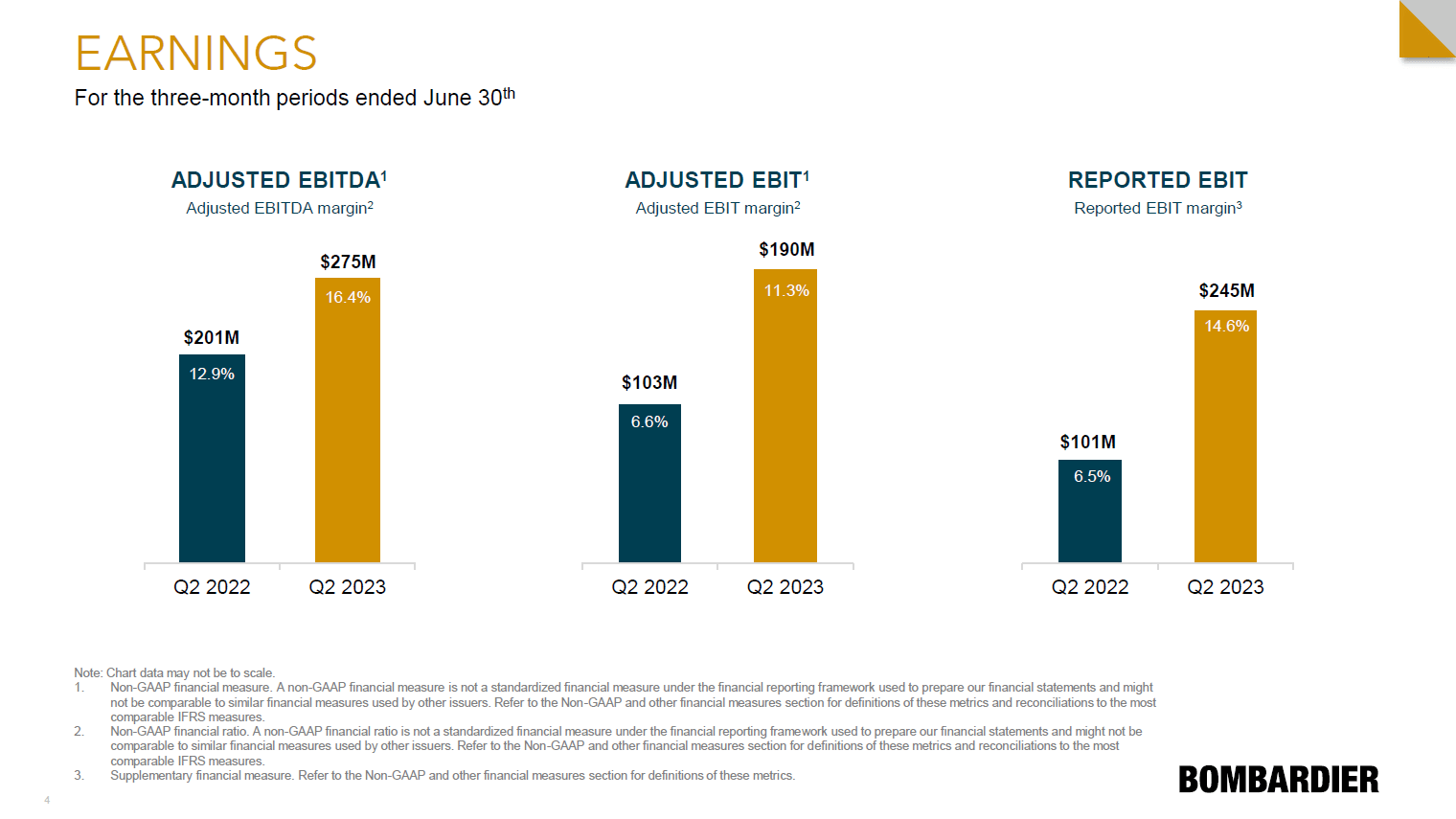

Adjusted EBITDA grew by 37% driven by 8% higher revenues and a 3.5 percentage point margin expansion. Adjusted EBIT grew by nearly 85% and reported EBIT grew by more than 140%. So, we're really seeing the combination of higher revenues and optimizing the business coming along nicely. While the $222 million negative free cash flow compared to a positive free cash flow of $341 million in the same quarter last year suggests otherwise, the better margins and top line give Bombardier a free cash flow tailwind.

During the quarter Bombardier had the last significant residual value guarantee payment related to its divested commercial aviation business, which pressured free cash flow by $104 million. These RVGs have been a liability as Bombardier provided residual value guarantees to customers requiring to protect customers against residual value shortfalls.

Furthermore, there is some capex as the company prepares to transition production to Toronto Pearson Airport while it has higher working capital in preparation for a significant increase in deliveries in the second half of the year.

Putting Cash To Good Use

{kind=link}

Year-to-date, available liquidity went down by $324 million, but I don't consider it a bad thing at all. $878 million went into building the inventory for a higher production, there was $173 million in capex, residual value guarantee payments and net long-term debt reduction of $424 million.

Bombardier

The debt maturity profile shows that Bombardier has no debt maturing in 2023 and 2024 and with its current cash balance it can already take out the 2025 debt as well as a significant portion of the 2026 debt. For the year, Bombardier has maintained its guidance of 138 deliveries with an adjusted EBITDA of more than $1.125 billion and more than $250 million in cash flow. With a $469 million cash burn in H1 that leaves at least $720 million in cash to be generated in the balance of 2023.

Quarter-over-quarter, the net debt to adjusted EBITDA decreased to 4.5x, but even if the cash balance does not improve which is a more than conservative assumption we will see the multiple go to 4x showing further improvement in the metrics, and with cash improvements I could see this going to 3.5x at least. In fact, Bombardier is so bullish on the future that it has increased its targets for 2025 as it was tracking ahead of the objectives. So, there's a lot of room to further deleverage with an even better target on net debt to EBITDA. With an upgrade from Moody's, refinancing also is a realistic tool that we will be seeing most likely to refinance some of the 2027 debt. A significant part of the deleveraging was driven by the ability of Bombardier to retire debt early. In the balance of the year, that space is somewhat constrained due to the cash flow negative first half of the year, but we could see Bombardier retiring debt earlier than maturity into the next year.

With improving financial metrics, Bombardier also is looking at beyond 2025 aiming for $1 billion in defense related sales and that's really what the current management has achieved. Bombardier went from being a company not able to look ahead one maybe two quarters to being able to plan and invest for the future with new business centers and defense penetration as it rolls out its business jets.

Is Bombardier Stock Still A Buy?

{kind=link}

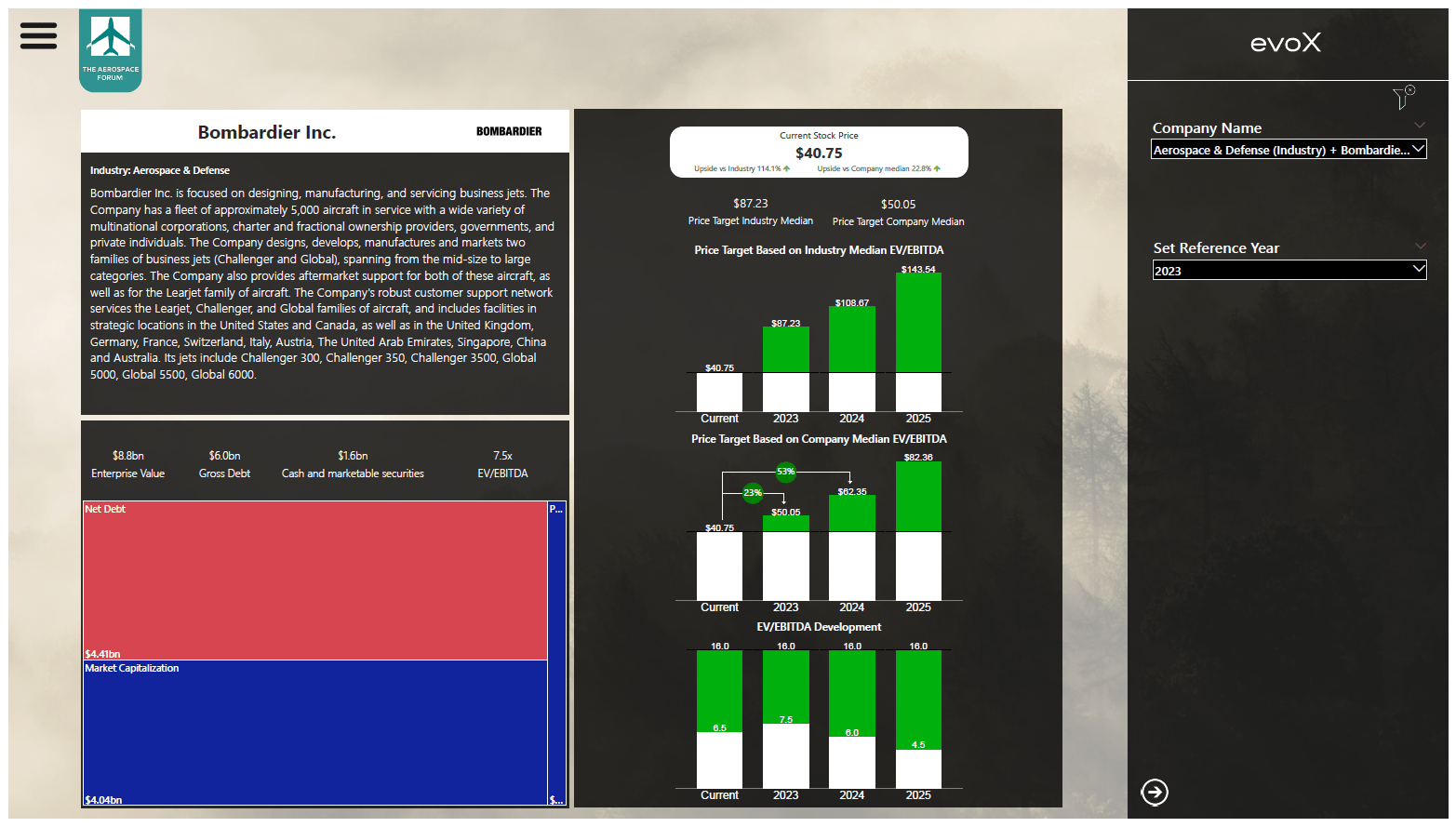

Following the release of its second quarter results, Bombardier stock sold off giving away most of its year-to-date gains. The financial results were not bad, but really failed to inspire as the big boost to free cash flow will be in the second half of the year and space to retire debt early is somewhat limited for the remainder of the year. So, the deleveraging trajectory will be somewhat slower for the coming six months as the first half of the year saw a reduction in liquidity for the Canadian business jet manufacturer. The long-term execution path, however, remains bright, and using the evoX Financial Analytics tool I believe that based on the 2023 expected results Bombardier stock is currently 23% undervalued and even 53% undervalued when pulling 2024 financial results into the stock price all while Bombardier trades at a lower EV-to-EBITDA ratio compared to its peers.

Conclusion: The Growth Story Is Not Over Yet

The second quarter results continued to show topline growth as well as margin expansion. Perhaps when viewing the quarter results in isolation, the free cash flow and debt reduction were not quite as strong as one would have hoped for, but over the longer term, we do see that the execution is fitting with the objectives set by the company. As a result, I maintain my buy rating for the stock even though I do not expect significant debt reductions for this year.

For further details see:

Is Bombardier Stock Still A Big Buy?