CMRE - Is Costamare A Buy Or A Sell After Its 22% Post-Earnings Rally?

2023-07-31 14:00:00 ET

Summary

- Costamare surged 22% after posting strong Q2 results, driven by robust revenues and earnings, share buybacks, and the stock's undervaluation.

- The containership segment continues to provide high-margin cash flows, while the CBI platform and the owned dry bulk vessels show potential for earnings growth.

- I continue to view Costamare's stock as undervalued, which, coupled with the company's strong liquidity position, justifies my urge to keep holding the stock.

Some Context

In early July, I shared an analysis explaining why selling Costamare's ( CMRE ) preferred shares to buy the company's common stock offered a considerably more appealing risk/reward ratio.

The preferreds were (and are) trading near par values, leaving no room for upside other than their high-single-digit yield, which honestly didn't seem like a great opportunity given interest rates being on the rise. That said, at 3.2X earnings at the time, the common stock seemed quite attractive, especially when considering the company's financial position and excellent liquidity.

Fast-forward almost a month later, buying Costamare proved to be the right decision, as shares soared by an impressive 22% on Friday following the company's Q2 report .

Now, the pressing question arises: Does Costamare still present a buying opportunity after such a strong rally, or might selling the stock be a more prudent and sensible course of action?

Why Did Costamare Stock Surge After Its Q2 Results?

To answer our main question, we first need to examine why Costamare surged by this much following its Q2 results. In my view, the rally can be attributed to three factors:

- Robust revenues and earnings despite industry challenges,

- The ramp-up of share repurchases, and

- The stock's undervaluation in the face of a potentially improving dry bulk environment along with excellent liquidity.

Let's break them down!

1) Robust revenues and earnings despite industry challenges

To begin with, Costamare's revenues and earnings remained robust in Q2, despite both the containership and dry bulk industries facing significant headwinds.

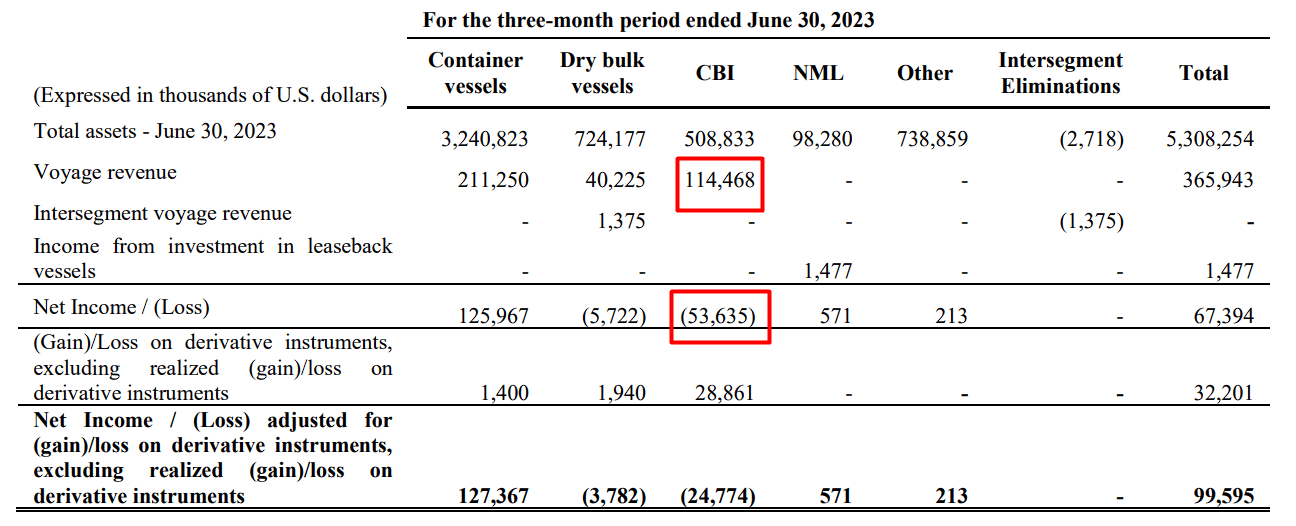

Specifically, for the quarter, total voyage revenues rose by 25.8% to $365.9 million, driven by (i) revenue earned by CBI, which was fully operational in Q2 of 2023, and (ii) higher charter rates in some of Costamare's container vessels, partly offset by lower charter rates in some of its dry bulk vessels and by revenue not collected by five container vessels and four dry bulk vessels that were sold during 2022 and H1-2023.

My previous analysis discussed the company's containership and dry bulk divisions. You can hence check my prior commentary since not much has changed. In short, containerships continue to provide robust, high-margin cash flows, currently boasting a backlog of about $2.9 billion with a TEU-weighted duration of 3.9 years. The dry bulk market remains relatively weak.

Regarding CBI, this is Costamare's brand new platform utilized to charter in and charter out dry bulk vessels, enter into contracts of affreightment and forward freight agreements (FFAs), and utilize hedging solutions.

As you can see, the CBI segment brought in $114.5 million in revenues, in stark contrast to the previous year, when no revenues were posted from CBI.

Costamare's Q2 Revenue Breakdown (Costamare's Q2 Earnings Report)

{kind=link}

Note that the CBI platform actually lost $53.6 million. While this loss can be partially attributed to a weak, dry bulk market (hence the $5.7 million loss the company recorded from its own dry bulk vessels), the majority of losses can be attributed to the CBI platform being in its very early stages and thus incurring one-off costs for its initial set up and the rollover of a new business. This was confirmed by Costamare's CFO, Gregory Zikos, during the company's post-earnings conference call .

Despite both the losses from owned dry bulk vessels and the CBI platform, the containership segment's monster high-margin backlog more than absorbed these flops, allowing the company to post a reduced but still relatively robust net income of $67.4 million.

2) The ramp-up of share buybacks

The primary driving force behind Costamare's post-earnings rally was clearly the substantial ramp-up in share buybacks. In my previous post, I expressed some concern about the underwhelming capital returns from Costamare, especially considering its impressive profitability and discounted valuation.

Costamare's surge in share buybacks during Q2 didn't only address those concerns but also impressed investors, playing a pivotal role in propelling the company's stock performance. Specifically, during the quarter, the company repurchased $50 million worth of stock, or 5,385,492 shares, a notable chunk of its weighted average number of shares of 124,228,628 in Q2.

Costamare paid just over $9/share, on average, for these shares, which I find to be an excellent price from multiple points of view (forward earnings, book value, etc.). In retrospect, these repurchases also appear very smart, with the stock now trading at roughly $11.60.

Looking ahead, Costamare's share buyback program has a remaining capacity of $40.0 million for the common shares and $150 million for preferred shares. Whether the company chooses to start retiring its costly preferreds or resumes repurchasing the common stock, the market should react positively. This is particularly true given that the shares are currently undervalued, which brings me to my final point...

3) The stock's undervaluation in the face of a potentially improving dry bulk environment, along with excellent liquidity

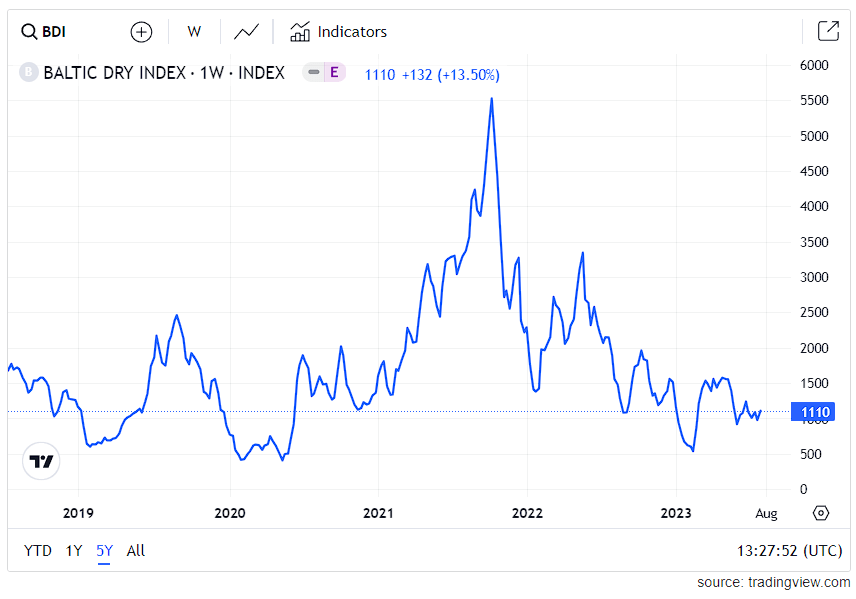

In my view, the final catalyst that bolstered Costamare's remarkable rally was the stock's undervaluation against a promising upturn in the dry bulk space, as well as the company's liquidity position remaining at exceptional levels.

During Costamare's earnings call, Mr. Zikos stated the following regarding the stock's valuation:

I do consider that the stock is undervalued, whether someone looks in terms of NAV, in terms of profitability, in terms of the prospects, in terms of track record, however, you look at it, it's undervalued and this is the reason we bought those common stock shares of $50 million worth over the last quarter.

This comment basically mirrors my thoughts regarding the stock's valuation made in my previous article. In the meantime, Mr. Zikos commented that management has a long-term commitment to the dry bulk space, whose fundamentals they view positively.

Given that it was Costamare's dry bulk assets that weighted earnings lower, Costamare's profitability could see a significant boost following a recovery in dry bulk rates, which currently hover at below-average levels.

Baltic Exchange Dry Index (Trading Economics)

{kind=link}

Combine this upside potential with the fact that Costamare's liquidity remains at a massive $1.06 billion (76% of its market cap even after the post-earnings rally), and you can see why the market loved Costamare's results overall.

So...Is Costamare a Buy or a Sell?

Analyzing the catalysts behind Costamare's post-earnings rally provides valuable insights into the question of whether the stock is a Buy or Sell. In essence, although the post-earnings rally might have taken away some of Costamare's "easy upside" potential, the stock, in my view, remains notably undervalued.

The containership segment's results are set to remain incredibly strong for several quarters ahead, while the dry bulk vessels and the dry bulk platform offer significant potential for an uptick in earnings if rates in the space were even modestly to improve.

As you can see, one-off costs in the CBI platform and lower dry bulk rates are going to result in a notable earnings decline this year. However, not only are this year's projected earnings still exceptional from a historical point of view, but you can see how the absence of this year's CBI set-up costs and the possibility of higher dry bulk rates next year can lead to a swift rebound in EPS (buybacks should also assist in that regard).

Costamare's EPS Projections (Seeking Alpha)

{kind=link}

With Costamare still trading close to 4 times its "normalized" earnings, management acknowledging the stock's undervaluation and responding meaningfully (buybacks), as well as the dry bulk platform offering significant upside potential in the possibility that rates in the industry recovery, I remain bullish on Costamare.

In the meantime, though not extravagant, the 4% dividend yield graciously contributes to a steady income, further bolstering my conviction to keep holding my shares.

For further details see:

Is Costamare A Buy Or A Sell After Its 22% Post-Earnings Rally?