OXY - Is Denbury Undervalued Or Overvalued? It Depends On What You Make Of Its Carbon Capture Business

2023-05-01 10:00:00 ET

Summary

- Denbury is an oil company that also develops a carbon capture, utilization and sequestration business.

- The government's backing makes carbon capture a promising business model, but the more sizeable cash flows may be years away.

- In the short run, cash flow that could be returned to the shareholders will instead fund the carbon capture capex.

- Heading into a likely recession, the valuation looks to be a risk.

Denbury Inc. ( DEN ) has done quite well since emerging from bankruptcy two years ago, when it was known as Denbury Resources:

DEN also outperformed relatively other energy stocks ( XOP ) by a big margin, so this probably isn't just an artifact of the strong oil prices ( CL1:COM ).

The question of course is whether this performance can be sustained - or if Denbury's valuation premium may revert to the mean. The presence of a sizable 10% short interest indeed shows that there is some disagreement in the market on where DEN is headed.

What Is Denbury's Business Model?

One important way in which Denbury differs from its peer group is the emphasis on its carbon capture, utilization and storage (or CCUS) business. While "CCUS" or "carbon capture", just like "hydrogen", has quickly become one of the energy transition's buzzwords, the reality is that it is usually larger companies seeking to develop these projects; not many small oil players are active in this space.

In Denbury's case, though, CCUS may have presented itself as an opportunity naturally rather than through active efforts to realign the company's business to the ESG trend.

At the risk of oversimplifying the engineering nuances of the related processes, DEN's oil production has been relying on "enhanced oil recovery" (or EOR) through the injection of CO2 into its reservoirs since the 1990s:

EOR using CO2 is one of the most efficient tertiary recovery mechanisms for producing crude oil. When injected under pressure into underground, oil-bearing rock formations, CO2 acts somewhat like a solvent as it travels through the reservoir rock, mixing with and modifying the characteristics of the oil so it can be produced and sold.

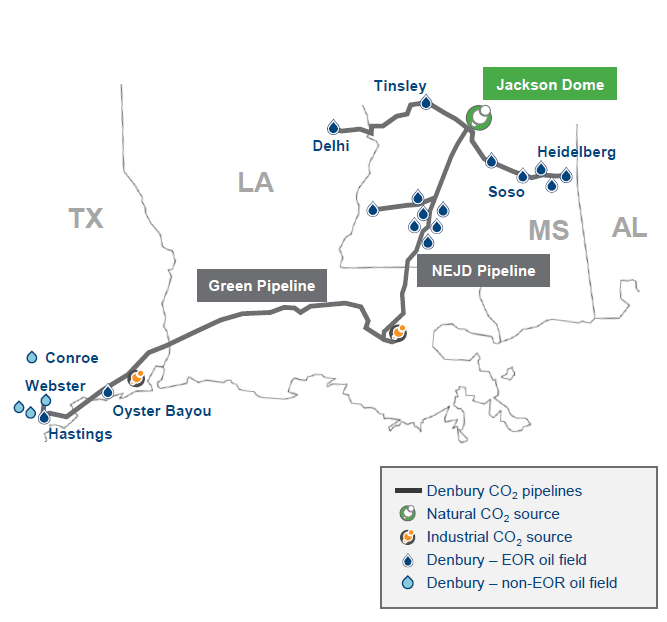

Historically, Denbury has sourced CO2 from naturally occurring reserves like its Jackson Dome asset in Mississippi and relied on a pipeline network to transport the CO2 to its oil producing fields:

{kind=link}

Now fast forward to the 2020s when capturing and sequestering carbon has become an official government objective and is rewarded with the Section 45Q tax credit of up to $85 per ton.

Denbury likely quickly realized that it can reposition its CO2 infrastructure to source industrially generated carbon from companies like Nutrien ( NTR ). It is a win-win because Nutrien and DEN can claim the credit, and DEN also gets to say that its oil production has a negative carbon footprint!

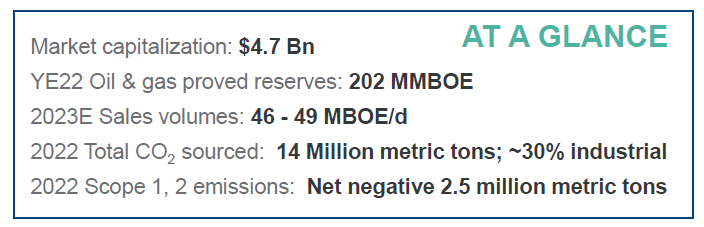

Meanwhile, of course, Denbury will continue to monetize its hydrocarbons production, which is very oil-weighted and has a decent reserve life index of about 11 years:

{kind=link}

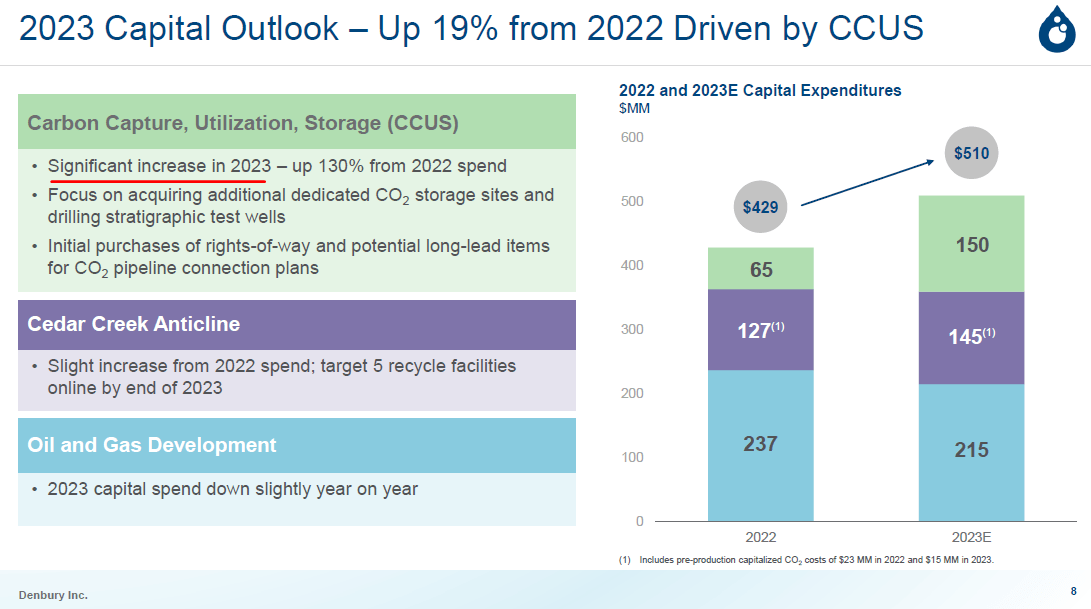

The downside, in Denbury's case, is that the major revenues from sequestering industrial carbon are years away, and in the meanwhile much of the cash flow from oil production flows back into CCUS capex.

{kind=link}

Denbury's management is not shy to highlight the "significant increase" of CCUS capex. So coming back to the valuation question, while many oil companies are nowadays considered "value stocks", DEN should be seen perhaps more as a "growth stock." The valuation then ultimately depends on how much you want to pay for the expected growth.

DEN Stock Key Metrics

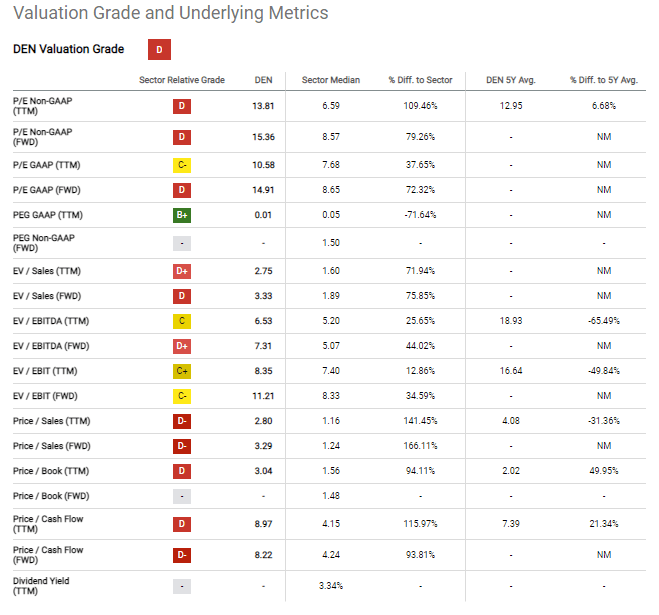

At the current stock price, DEN isn't cheap:

{kind=link}

Moreover, DEN is among the smaller market caps in the sector which generally trade on lower multiples. The short interest is high:

For a company with very little debt like DEN (most of the debt is asset retirement obligations), the short interest probably suggests disagreement with the valuation.

Why Has DEN Stock Been Raising?

As oil prices recovered from the COVID lows, earnings have certainly been improving. However, much of stock price growth over the last year has been helped by the multiple expansion:

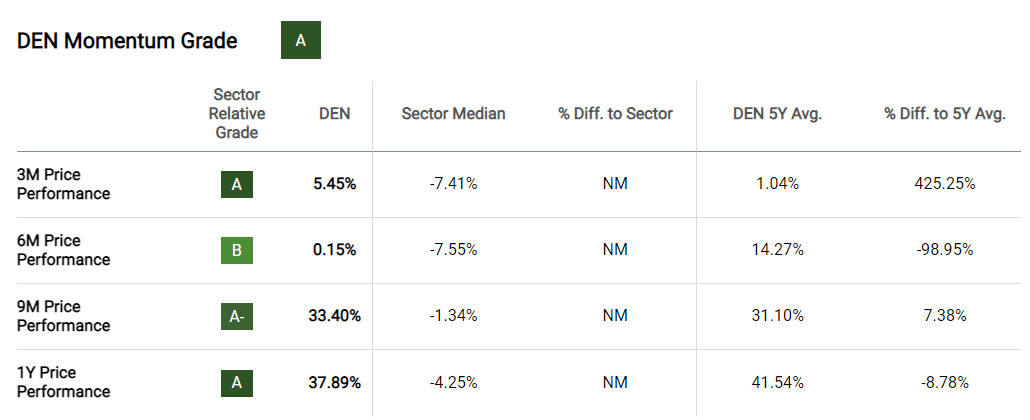

So the short answer to why DEN went up is "momentum":

{kind=link}

Note that Seeking Alpha scores Denbury "A" on momentum while the valuation grade is only "D."

How Does The Current Valuation Compare To Peers?

Not very well. In addition to Seeking Alpha's valuation score, I compared DEN to Occidental ( OXY ):

I chose Occidental on purpose, not just because it is one of the largest independents but also because it too develops a CCUS business. Supposedly, carbon capture was one of Warren Buffett's motivations to acquire a significant stake in the company.

Well, OXY's valuation is more discounted that DEN, which makes little sense given the order of magnitude difference in market cap and footprint diversification. I am sorry, Denbury, but you're no OXY.

Is DEN Overvalued Or Undervalued?

It depends how much value you want to ascribe to the CCUS business. But as a quick thought experiment, let's assume the traditional oil business merits a 9x forward P/E multiple consistent with the sector median. Forward EPS are projected at $6:

{kind=link}

That implies $6 x 9x = $54 per share. The balance $93 - $54 = $39 per share, or a total of $2 billion at 50 million shares outstanding, is what the market ascribes to the CCUS enterprise.

Is $2 billion a lot? I don't know, but for the latest financial year Denbury booked $60 million revenue from CCUS:

{kind=link}

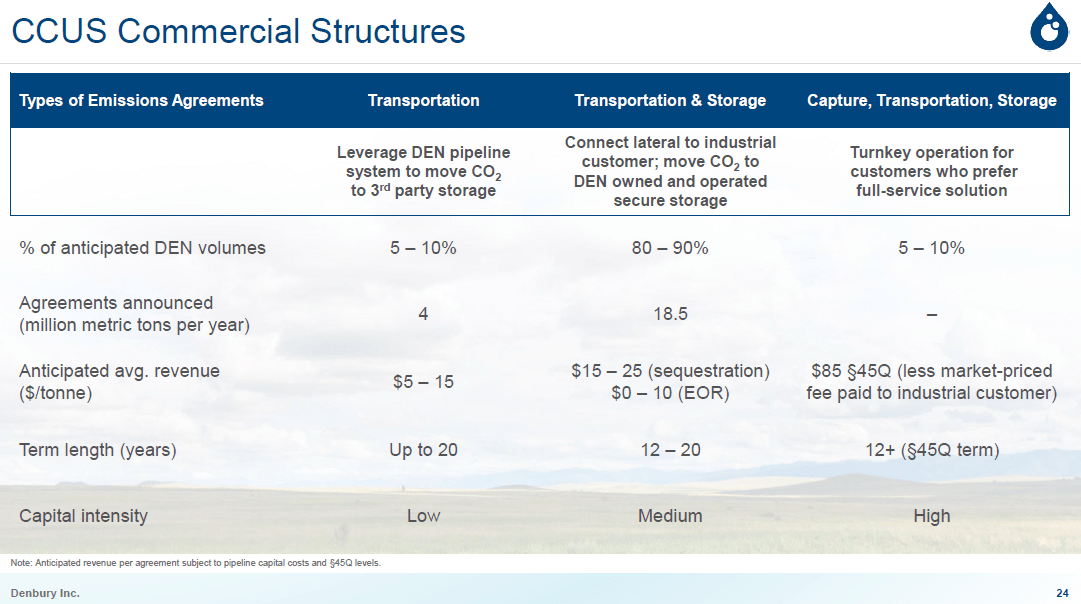

Call me skeptical, but I would prefer to see more definite projections for the CCUS piece. At this early stage, the company isn't offering much specifics:

{kind=link}

No "capture, transportation and storage" contracts are announced yet (those are the ones that would get the full $85 per ton credit). For the "transportation and storage" category, we have 18.5 million metric tons subject to long-term agreements; let's use $25 per ton. That's about $460 million revenue per year, so much better than 2022, but still difficult for me to recommend this business at $2 billion valuation.

What Is The Long-Term Outlook?

The increase of the CCUS credit to $85 per ton under the Inflation Reduction Act is definitely a boost. However, in Denbury's case, the implied valuation for its CCUS activities seems quite rich.

Moreover, Denbury is hardly a monopolist in this emerging field. Much bigger independents like Oxy are also competitors, and the majors Exxon ( XOM ) and Chevron ( CVX ) would also be a competitive threat.

Right now, the market rewards Denbury with a generous multiple, but I am not confident that would continue for much longer. An Exxon comes with certain stability, for which investors are ready to pay premium; bigger companies can also get away even if they prioritize capex over shareholder returns.

However, a small cap company that pours much of its free cash flow into CCUS capex may be a different story. I personally think in Denbury's league cash returns is the name of the game, especially when we're heading into difficult macroeconomic conditions.

During the oil bonanza 2022 year, Denbury spent $100 million on buybacks to buy 1.6 million shares, or about 3% of the outstanding share count. This isn't much compared to companies like Marathon ( MRO ) that reduced share count by a double-digit percentage.

Is DEN Stock A Buy, Sell, Or Hold?

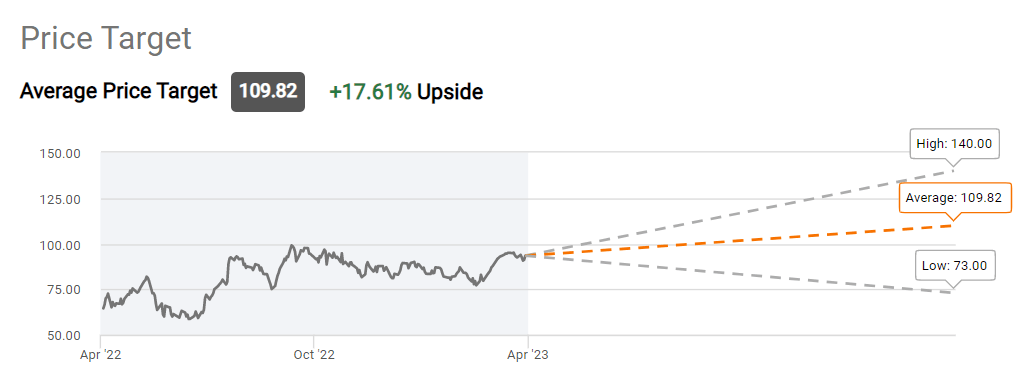

Wall Street's average price target is $109, but I see the low range of the street targets as more likely:

{kind=link}

The company should be announcing earnings very soon, so investors should watch closely for the market's reaction. I don't really expect any earth-shattering announcements on the CCUS side, as that business is a long-term endeavor that will take years to build out. However, if Denbury beats EPS estimates and the stock goes up further, I would at least consider taking some profits.

For further details see:

Is Denbury Undervalued Or Overvalued? It Depends On What You Make Of Its Carbon Capture Business