META - Is It Worth Investing In Oil And Gas Companies In 2023

Summary

- Brent futures and WTI crude have fallen over 8.5% since my article “What Awaits The Oil And Gas Industry In 2023” was published.

- Following the results of an excellent year for the oil and gas industry in 2022, Exxon Mobil plans to send up to $50 billion in a share repurchase program.

- After reducing total debt by $11.231 billion in 2022, Chevron said it would triple its share buyback program to $75 billion, an enormous amount in the industry.

- The US natural gas price is currently $2.327 per MMBTU and has declined in recent quarters due to abnormally high temperatures and reduced risks of shortages in the coming months.

- According to the EIA report, US crude oil inventories stood at 843 million barrels, up 16.3 million from the previous week, shocking many market participants.

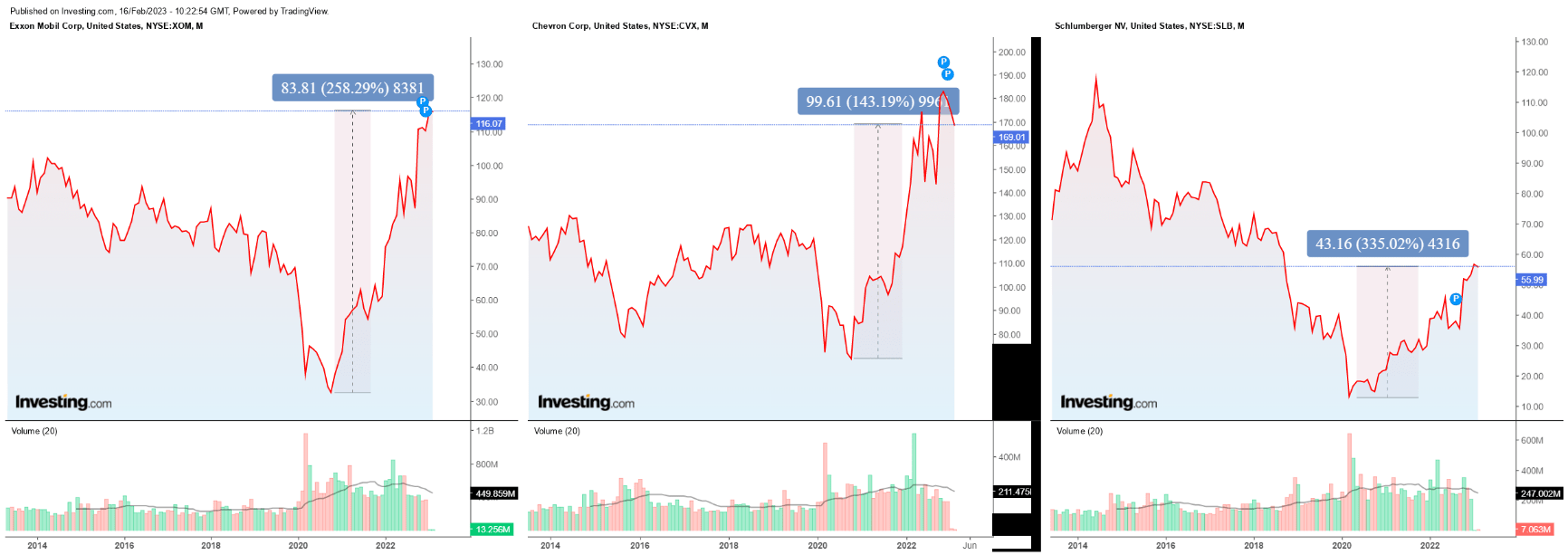

Brent futures ( CO1:COM ) and WTI crude ( CL1:COM ) have fallen over 7.5% since my article “What Awaits The Oil And Gas Industry In 2023” was published, but share prices of gas and oil industry leaders Schlumberger ( SLB ), Exxon Mobil ( XOM ) and Chevron Corporation ( CVX ), three of the main assets in the Energy Select Sector SPDR ETF ( XLE ), continue to reach new heights. From 2020, when the COVID-19 pandemic began, to the present day, these mastodon stocks have shown excellent returns ranging from 143% to 335%, as in the case of Schlumberger, which may not please investors and attract the attention of many Wall Street participants.

{kind=link}

Author's elaboration, based on Investing.com

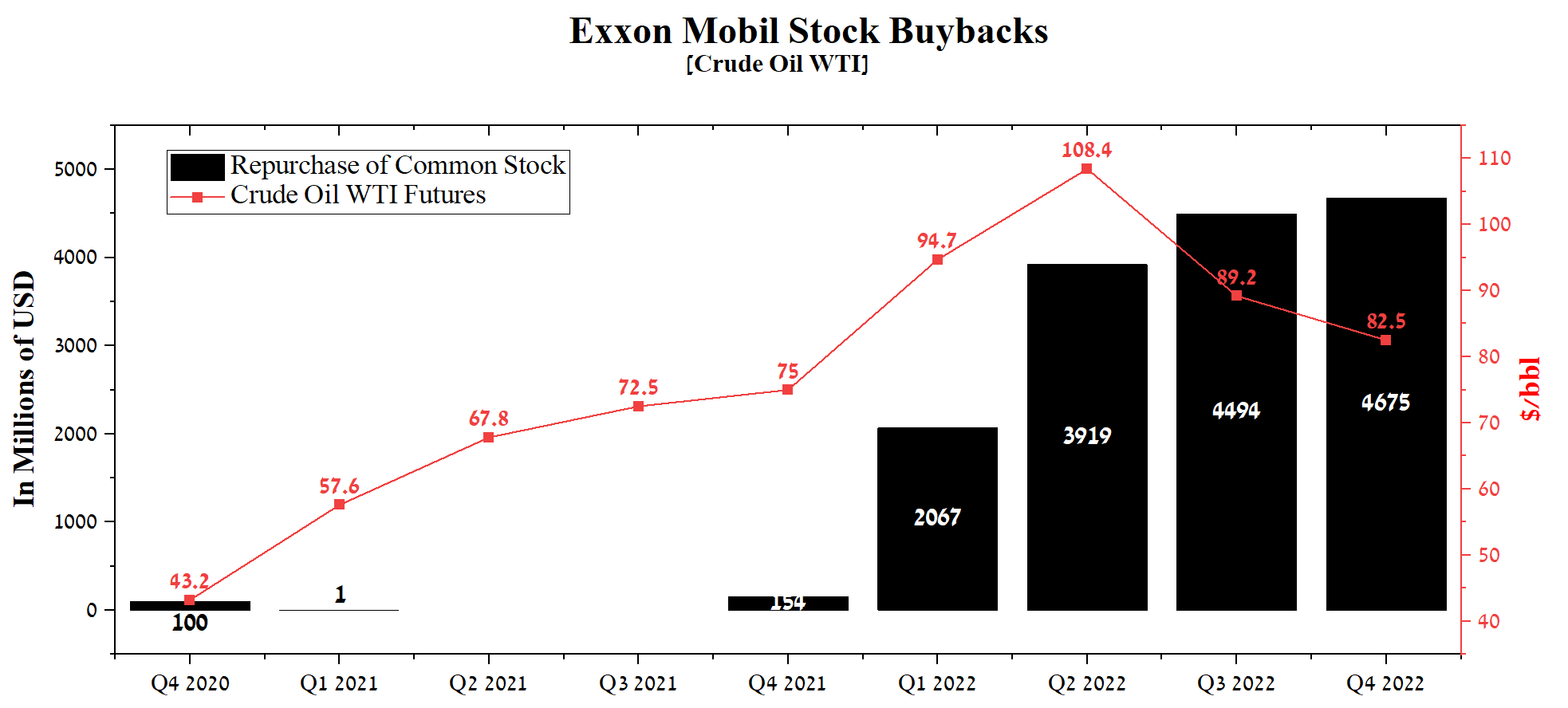

At the beginning of this article, I would like to highlight three key factors that help keep oil and gas stock prices in an upward price range. Significantly higher energy prices since the second half of 2021 due to the outbreak of military conflict in Eastern Europe, rising inflation, and supply chain disruption due to anti-COVID measures in China have contributed to the authorization of tens of billions of dollars of share buyback programs. In Q4 2022, Exxon Mobil repurchased $4.675 billion in the company's stock, up slightly from the previous quarter. The main reasons for the slowdown in Exxon Mobil's share repurchase program may be the need to allocate cash for capital expenditures and debt repayment, the priority of management, and the board of directors in paying dividends over share buybacks to attract long-term investors. In addition, the company's share price is currently at multi-year highs, and as a result, an increase in share buyback spending in the current environment is less attractive. Following the results of an excellent year for the oil and gas industry in 2022, Exxon Mobil plans to send up to $50 billion in a share repurchase program through 2024. This does not mean that the entire amount will be spent, as it will depend on many factors affecting the company and its shareholders.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

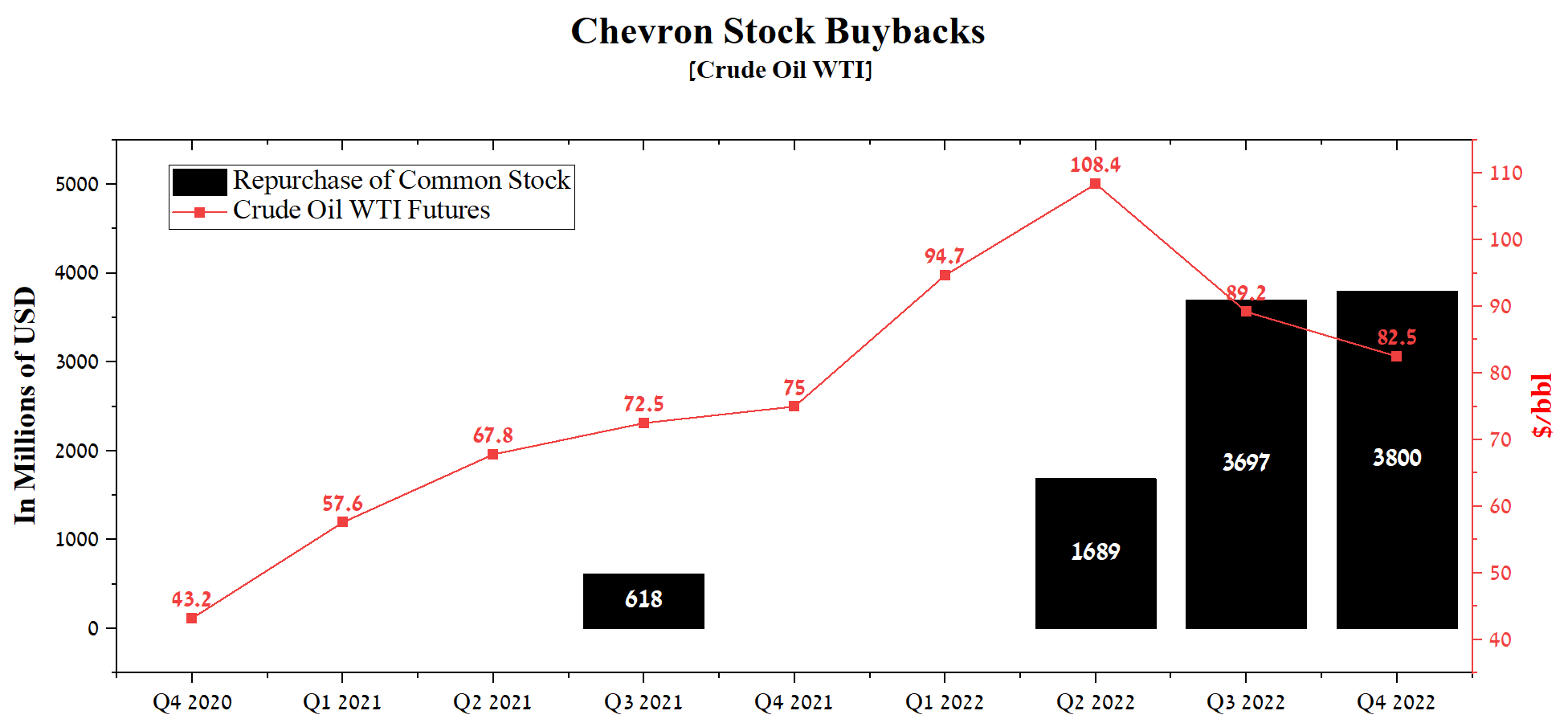

In Q4 2022, Chevron Corporation bought back $3.8 billion of the company's shares, up $103 million from the previous quarter. Unlike Exxon Mobil, the company's management directs a significant part of the cash flow to repay the debt, which in my opinion, is the right decision during the period of rising interest rates, taking advantage of the period of increased energy and oil prices. Historically, we had seen long periods when, after the end of the commodity cycle, many companies painfully endured low oil and gas prices while having high capital expenditures. As a result, Chevron management's top priority is to mitigate the risks associated with debt service before using the remaining operating income to buy back the company's shares. After reducing total debt by $11.231 billion in 2022, the company said on January 25 that it would triple its share buyback program to $75 billion, an enormous amount in the industry currently.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

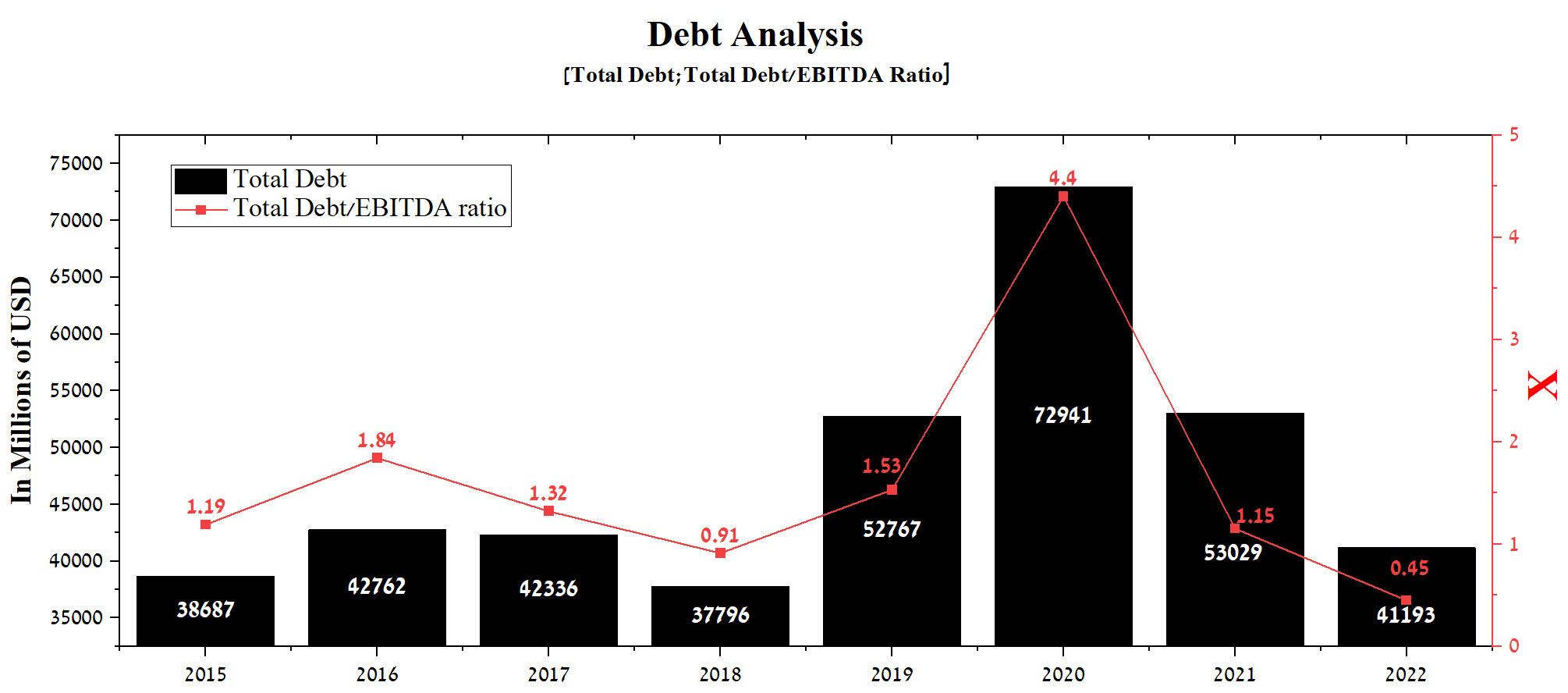

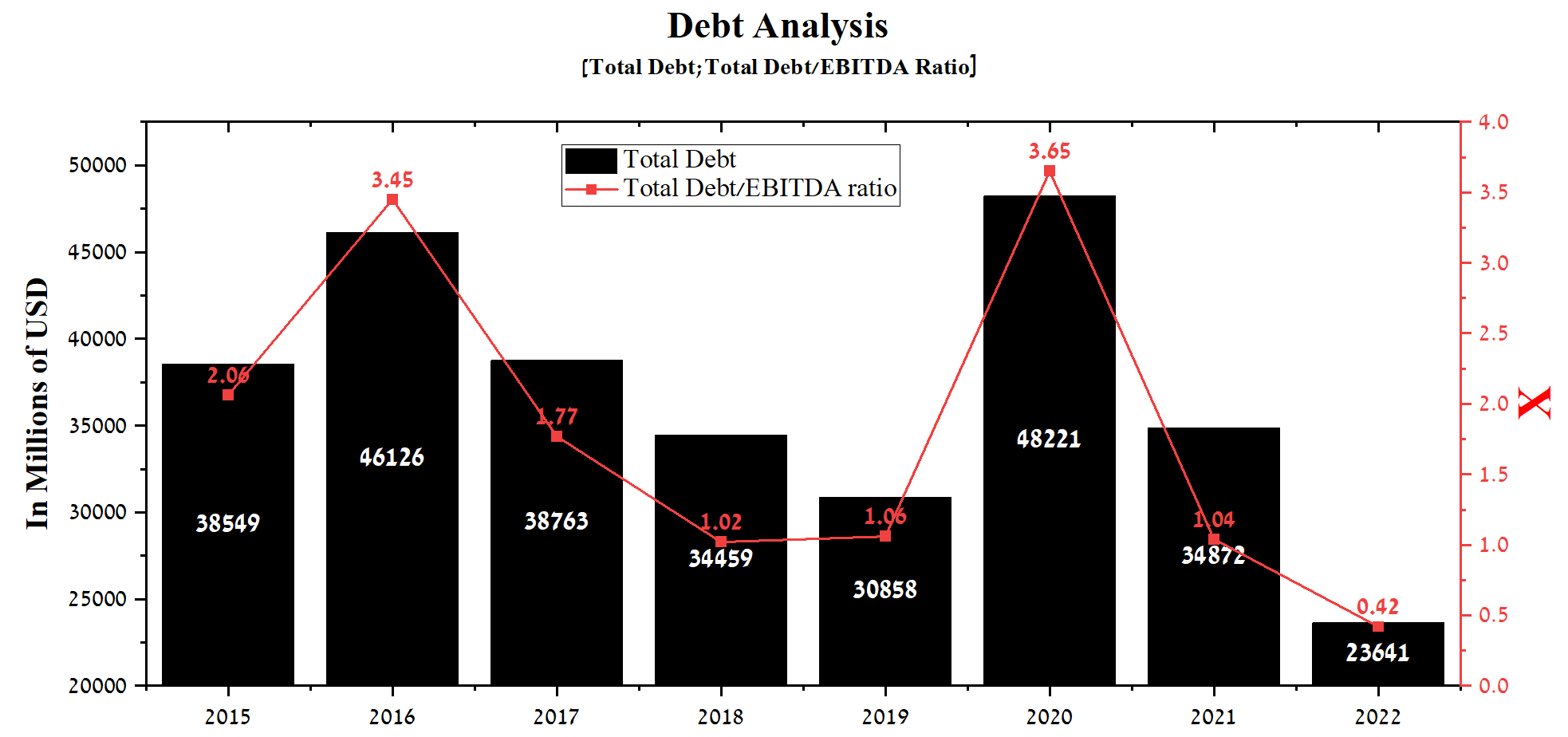

The second factor in the high share price of the SPDR Energy Select Sector ETF is the reduction in the debt of the companies included in it and also the maintenance of a relatively high dividend yield. Both companies' de-leveraging policies are starting to pay off, with Exxon Mobil's total debt at $41,193 million at the end of 2022, down 22.3% from 2021 and 43.5% from peaks in 2020. Moreover, thanks to continued high business margins, Exxon Mobil's Total Debt/EBITDA ratio continues to decline QoQ year-on-year to 0.45x at the end of Q4 2022.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

While Chevron Corporation's Total Debt/EBITDA ratio was marginally better at 0.43x, down 59.6% from 2021.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

A low Total Debt/EBITDA ratio attracts investors looking for stable and less risky investments, as it indicates the company's ability to be flexible in the face of macroeconomic instability, continuing to invest in growth opportunities, and pay dividends to shareholders. In addition, the low total debt/EBITDA ratio allows it to have high credit ratings assigned by S&P Global (NYSE: SPGI ) and Moody's Corporation (NYSE: MCO ) and therefore receive financing on more favorable terms even in a downturn in the business cycle.

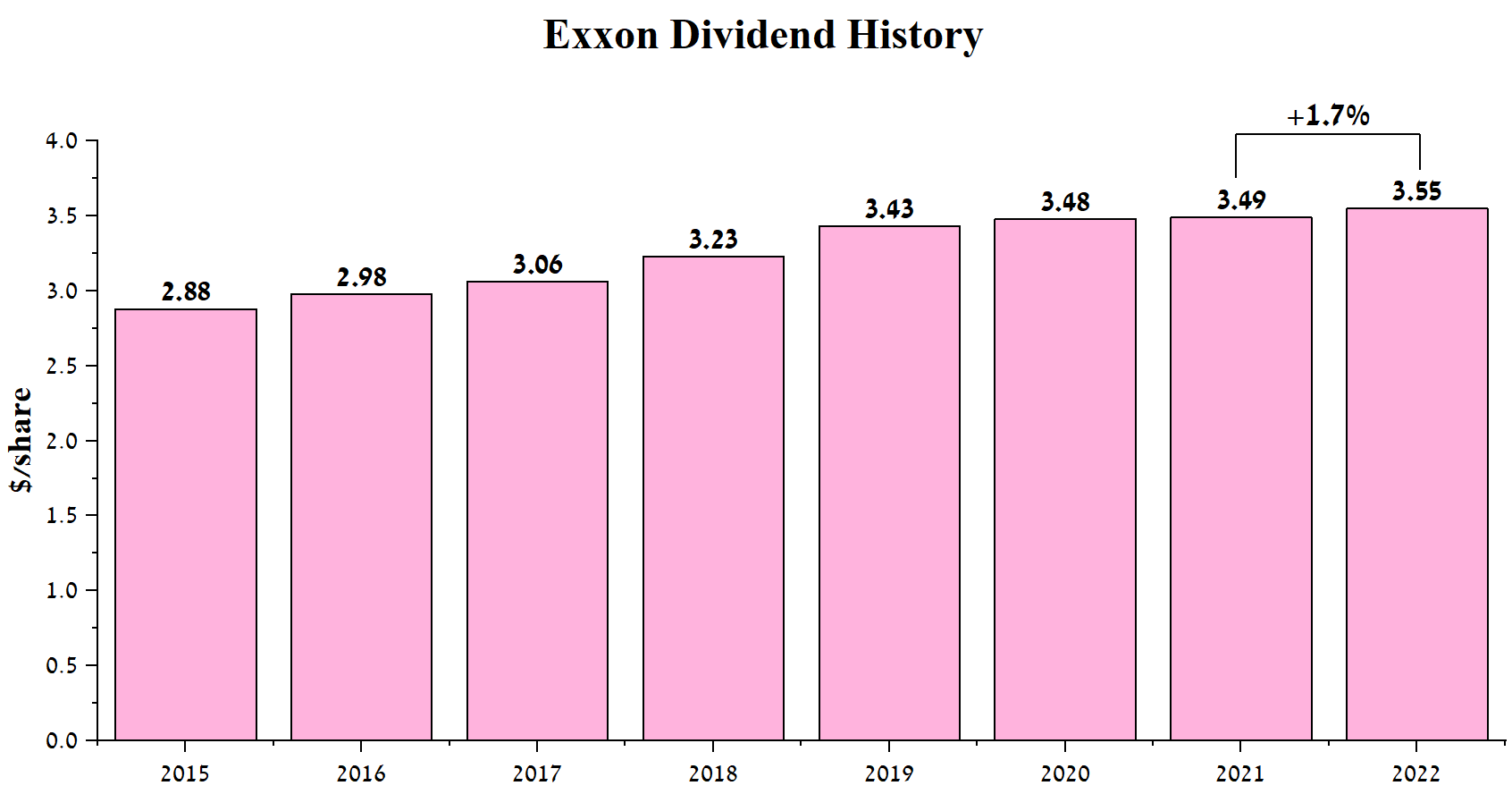

As of February 17, Exxon Mobil's dividend yield is 3.15%, slightly higher than the energy sector average. At the same time, only from the end of 2021, dividend payments began to grow again after a long period from Q2 2019 to Q4 2021, during which the company's management did not seek to increase cash flow spending for this purpose and the Board of Directors decided to pay $0.87 per share in the quarterly dividend.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

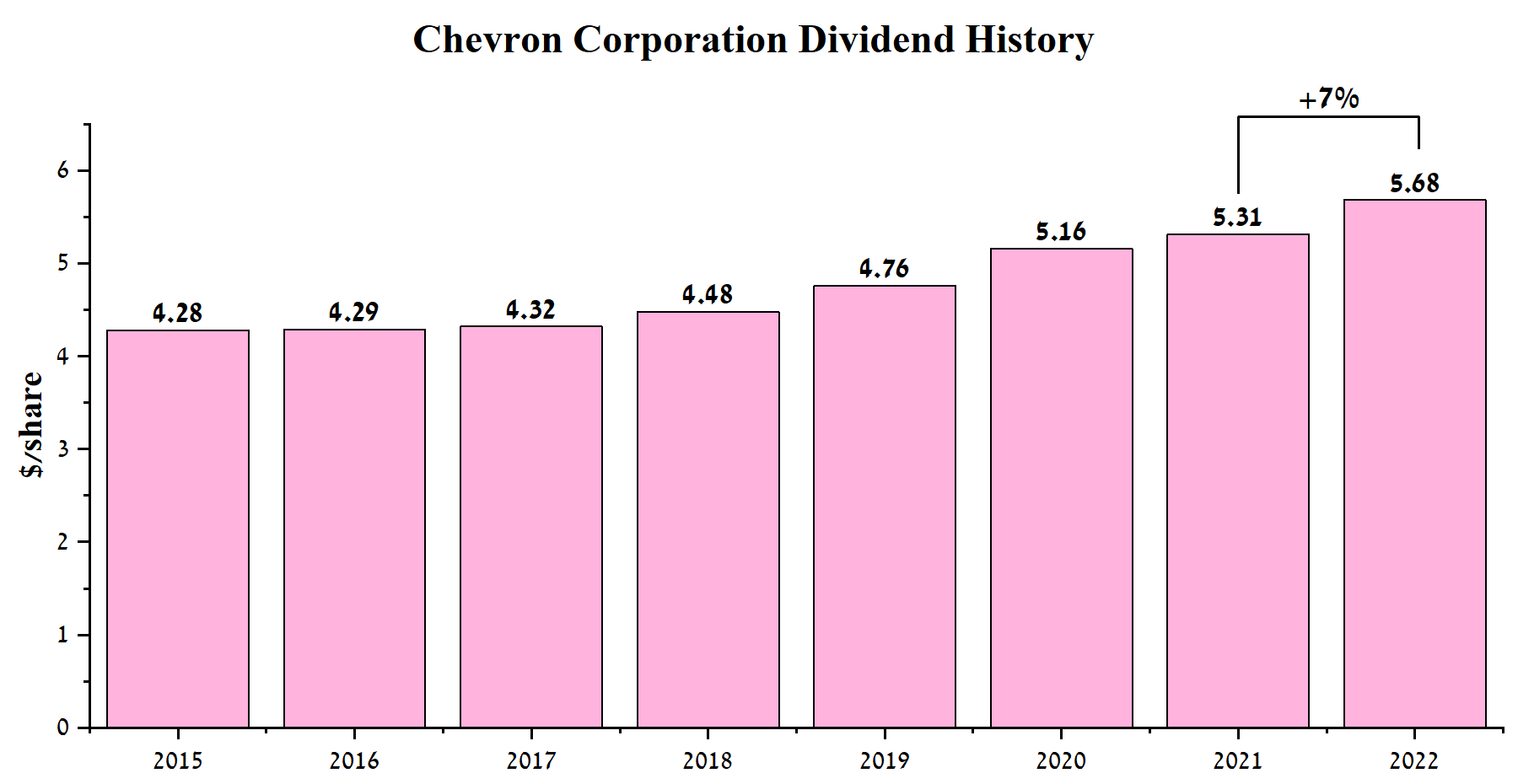

As of February 17, Chevron Corporation's dividend yield is 3.63%, higher than the average for the energy sector and Exxon Mobil. At the same time, the company's management seeks to increase dividend payments more often, making it more attractive compared to Exxon Mobil.

{kind=link}

Source: Author's elaboration, based on Seeking Alpha

The third factor in maintaining high stock prices for Exxon Mobil and Chevron relative to the pre-COVID times is the military conflict in Eastern Europe, which led, among other things, to the imposition of sanctions by the United States and Europe on the oil and gas industry of Russia, followed by an increase in demand for services and goods of American and European companies. On February 5, 2023, the European Union banned tanker deliveries of oil products from Russia, and at the beginning of last year, the United States and the United Kingdom refused to import oil produced in the aggressor country, thereby reducing the cash flow of such Russian companies as PSJC Lukoil (LUKOY), Gazprom (OGZPY), and Rosneft (RNFTF). In response to the imposed sanctions, on December 27, 2022, President Putin signed a decree according to which, from February 1, 2023, a ban on the supply of Russian oil to countries using a price ceiling began to operate.

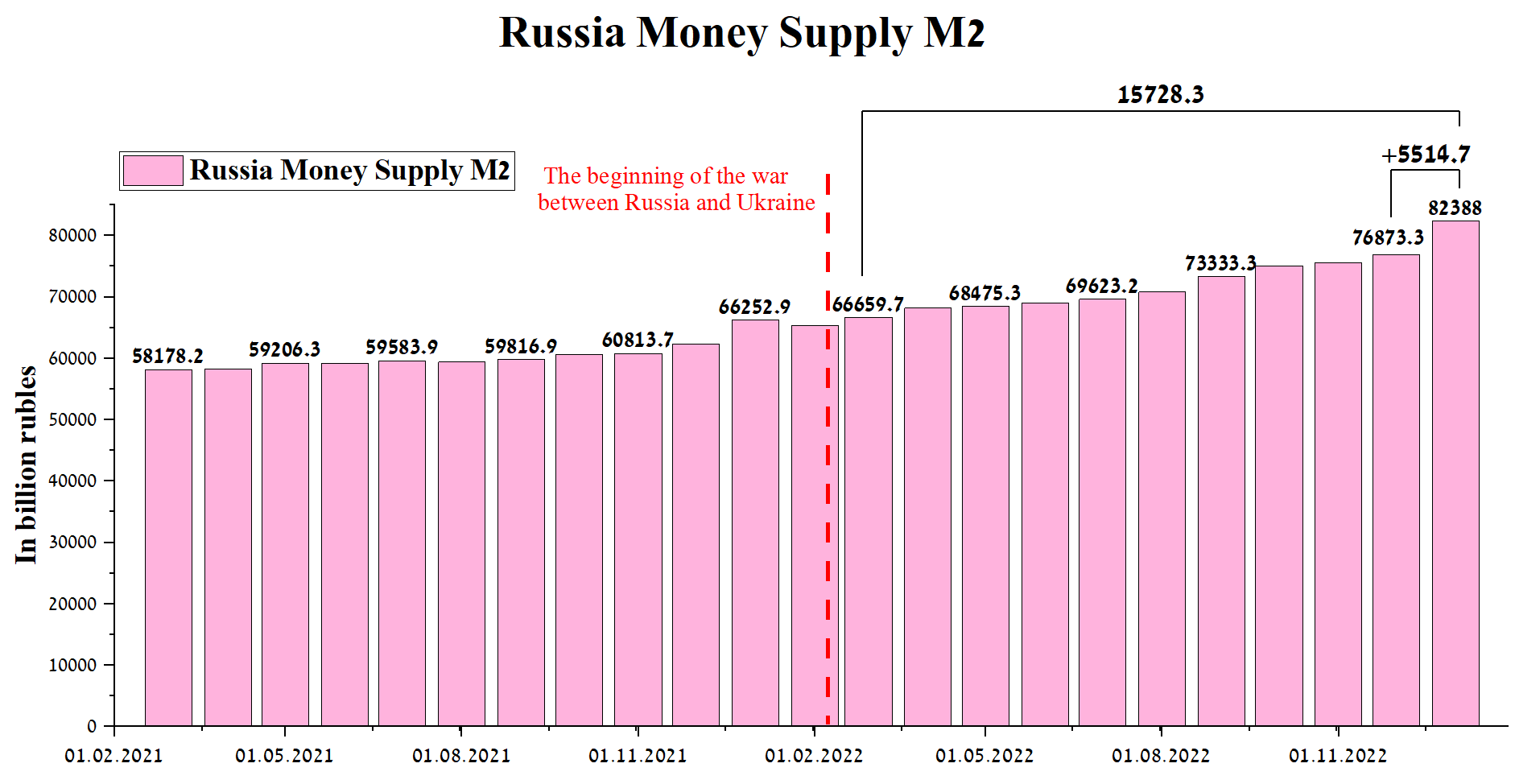

In my assessment, Russia will continue to supply oil and petroleum products in increased volumes to China and India, where economic activity has resumed growth after the COVID-19 pandemic was brought under control and domestic demand for hydrocarbons recovered. Even though the Kremlin claims in its statements that the sanctions will not harm the country's economy, this is not the case. Already one can see an increase in Russia's dependence on Asian countries that take advantage of the aggressor country's deplorable situation and a significant increase in the M2 money supply by about 5.5 trillion rubles in just one month.

{kind=link}

Author's elaboration, based on the Central Bank of the Russian Federation

Given the development of hostilities in the eastern part of Ukraine, it is unlikely that the military conflict will end in the coming months, and thus this will support the demand for oil products produced by companies that are part of the ETF SPDR Energy Select Sector.

Let's move on to the three main factors contributing to the continued downward pressure on prices of petroleum products from Q3 2022 and why investing in oil and gas companies in 2023 is far from the best idea.

Factors exerting downward pressure on shares of oil and gas companies

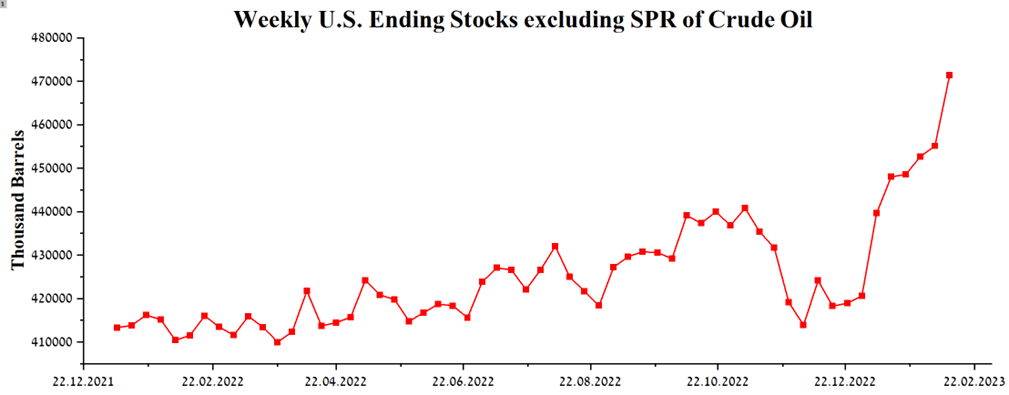

According to the EIA report , US crude oil inventories stood at 843 million barrels, up 16.3 million from the previous week, shocking many market participants. The significant increase was driven by the rise in commercial crude oil inventories of 471.4 million barrels, up 9.6 million from a year earlier. Moreover, as you can see in the chart below, oil inventories continue to rise from month to month, thus contributing to the decline in the price of crude oil.

{kind=link}

Author's elaboration, based on the EIA report

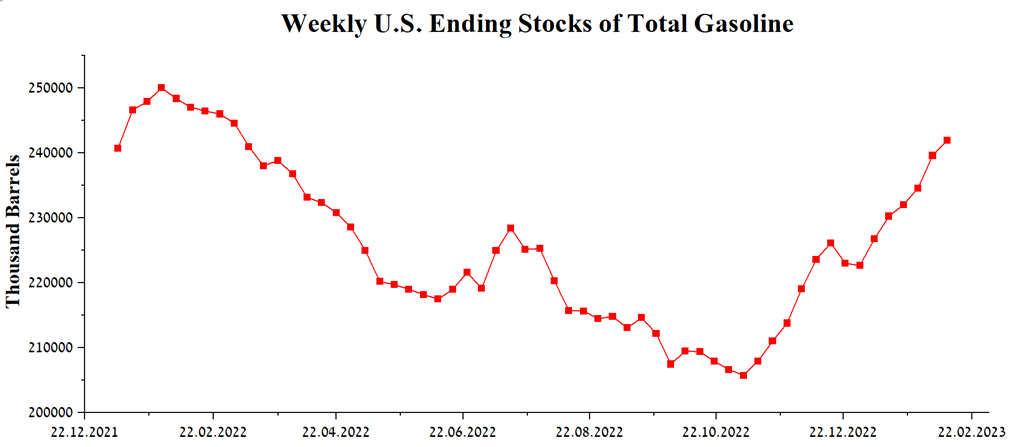

Positive dynamics are shown by stocks of total motor gasoline, which amounted to 241.9 million barrels, an increase of 2.3 million barrels compared to last week. Despite the positive dynamics since the beginning of the fourth quarter of 2022, this indicator is still below 2021.

{kind=link}

Author's elaboration, based on the EIA report

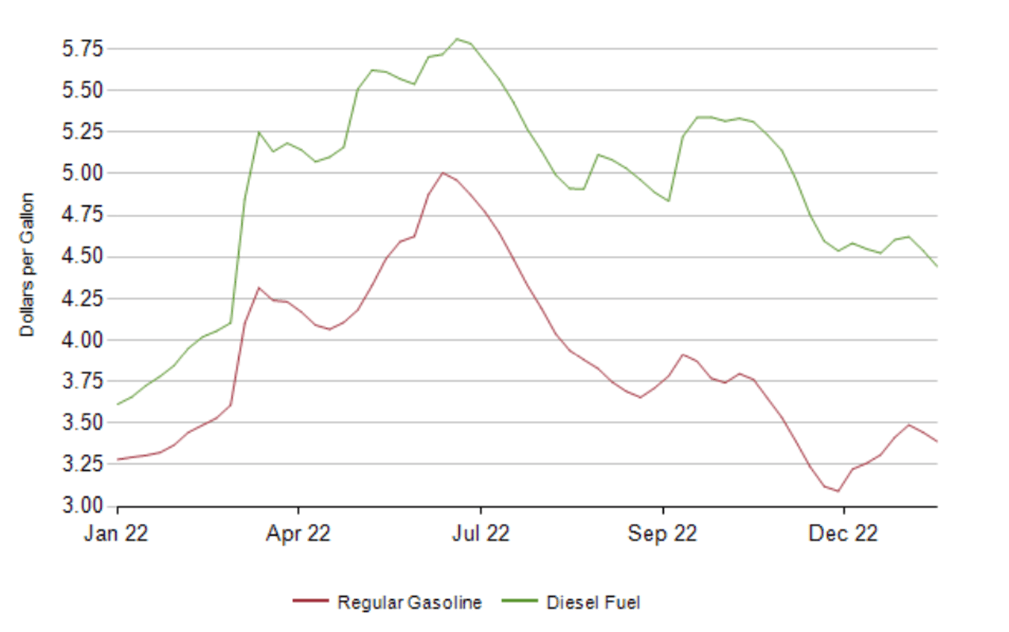

As a result, gasoline and diesel fuel prices remain on a downward trend, which not only helps to reduce inflation in the US, but also reduces the revenue of Exxon Mobil and Chevron Corporation in recent quarters.

{kind=link}

EIA report

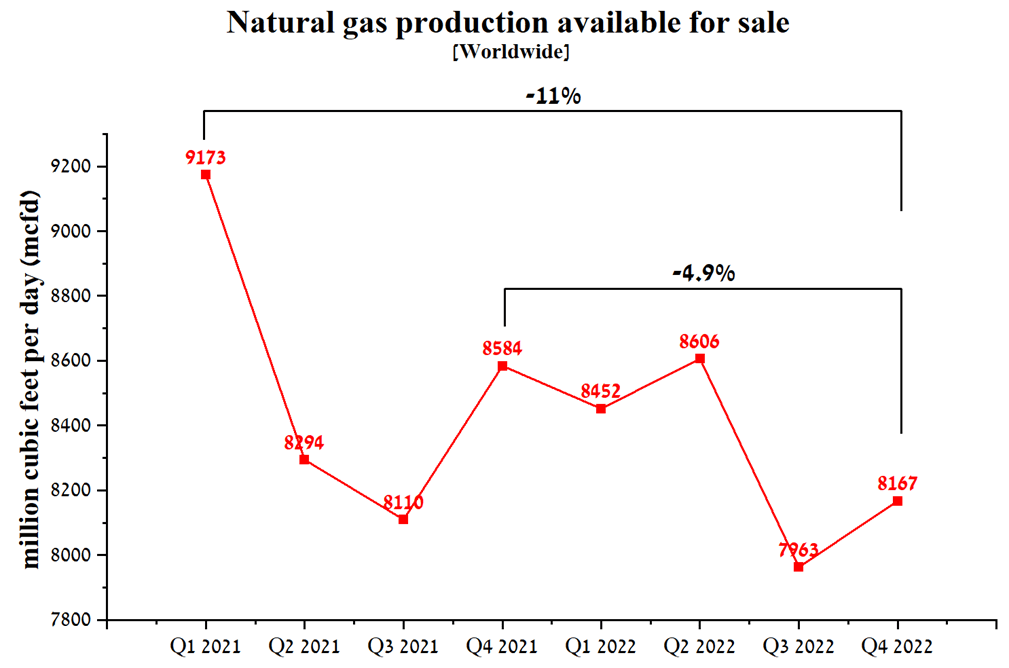

The second factor contributing to the decline in operating profits for Exxon Mobil and Chevron Corporation is the decline in natural gas prices ( NG1:COM ) in both the US and Europe. The sale of natural gas is one of the primary sources of income for both Exxon Mobil and Chevron. Natural gas volumes available for sale by Exxon Mobil were 8,167 million cubic feet per day in Q4 2022, down 4.9% from Q4 2021, with a more severe decline from the first three months of 2021.

{kind=link}

Author's elaboration, based on quarterly securities reports

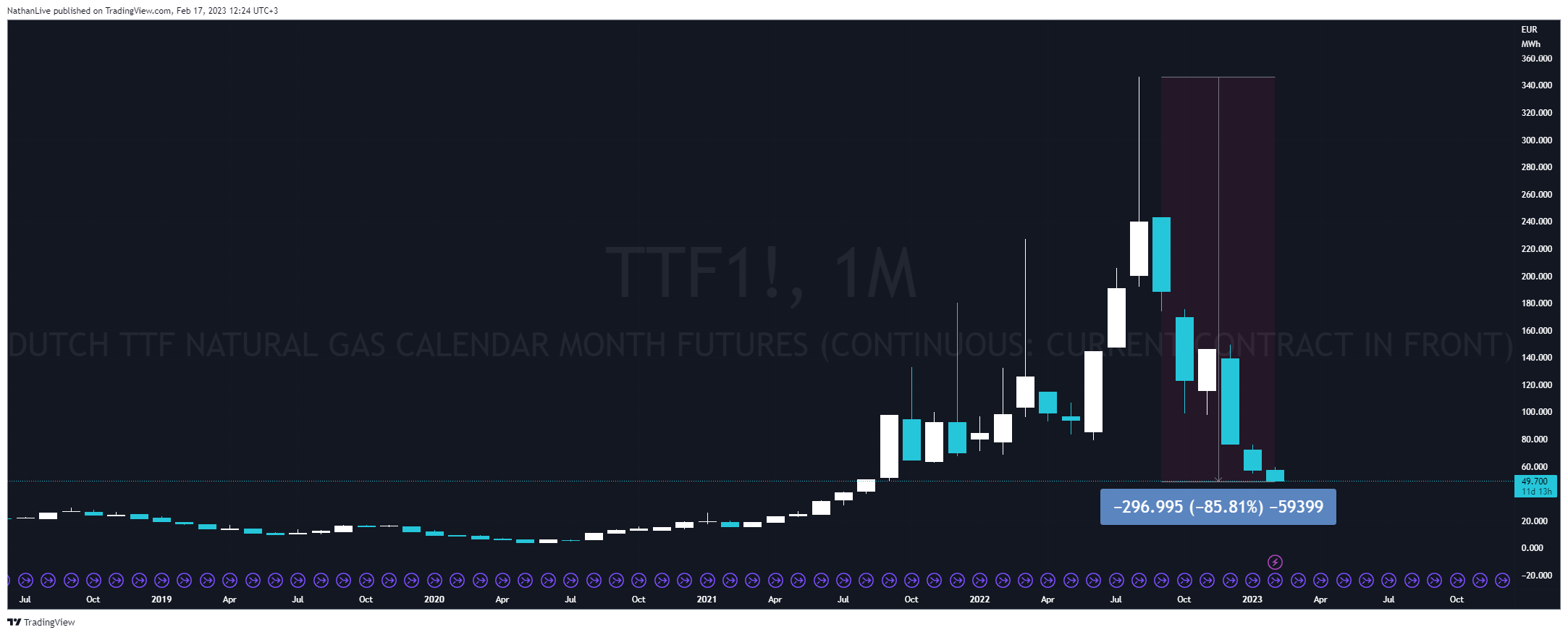

The US natural gas price is currently $2.327 per MMBTU and has declined in recent quarters due to abnormally high temperatures and reduced risks of shortages in the coming months. Moreover, the price of natural gas in the US had almost reached the levels of 2019, when Exxon Mobil's share price was $72-$74. At the same time, the price of European natural gas (TTF1) shows a downward trend, which fell below 50 euros per MWh, reaching mid-2021 levels and falling by 85.8% from peak values.

{kind=link}

Source: N_Aisenstadt — TradingView

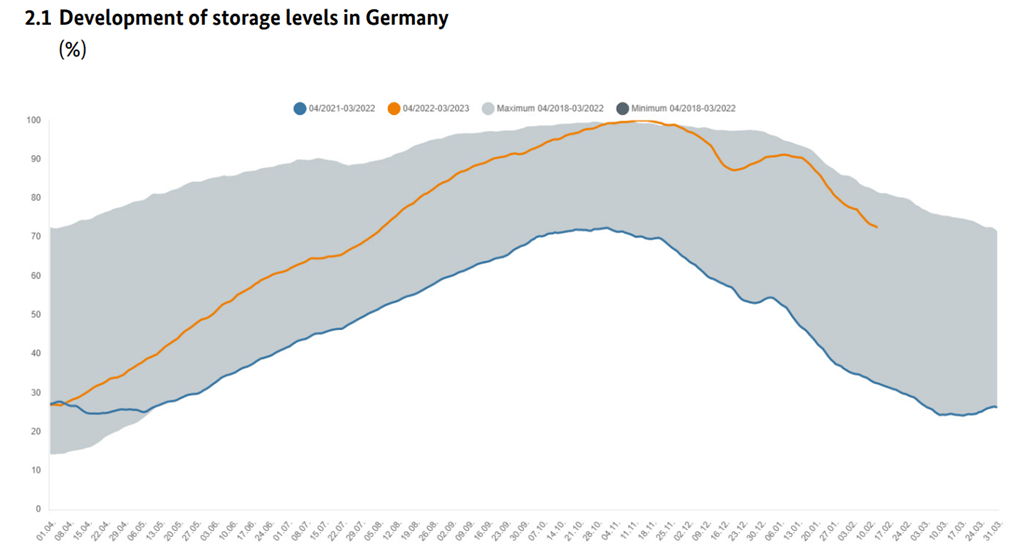

The main reasons for this are the continued mild winter and the maintenance of high levels of natural gas reserves due to improved supply chains. So, for example, in Germany, about 74% of the storage capacity is filled with a vital energy source, which is significantly higher compared to 2021-2022.

{kind=link}

Source: Bundesnetzagentur

According to my calculations, the price of European and American natural gas will remain in the current price ranges and be of low volatility, considering the existing reserves in the reservoirs. Moreover, in the long term, I expect European countries to find long-term and stable suppliers both in the Middle East and the US, thereby increasing downward pressure on the price of natural gas and significantly reducing dependence on Russian supplies.

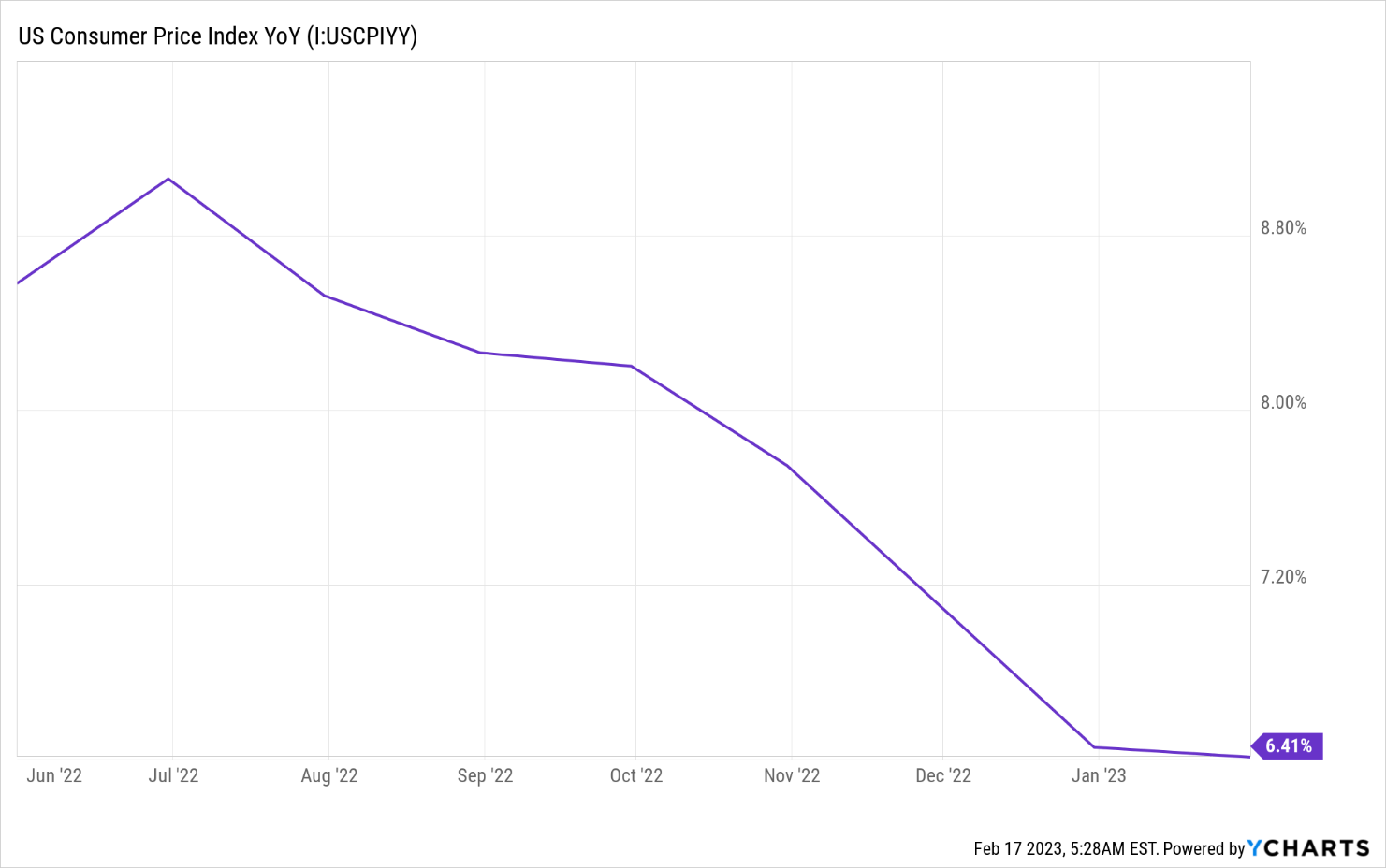

The third factor that will put pressure not only on the share price of the Energy Select Sector SPDR ETF but also on many other market participants like BP ( BP ), Occidental Petroleum Corporation ( OXY ), and Shell ( SHEL ) is lower inflation. CPI inflation rose by 6.4% in January 2023 from 6.5% in the previous month, indicating the effectiveness of the Fed's price containment policy.

{kind=link}

Source: YCharts

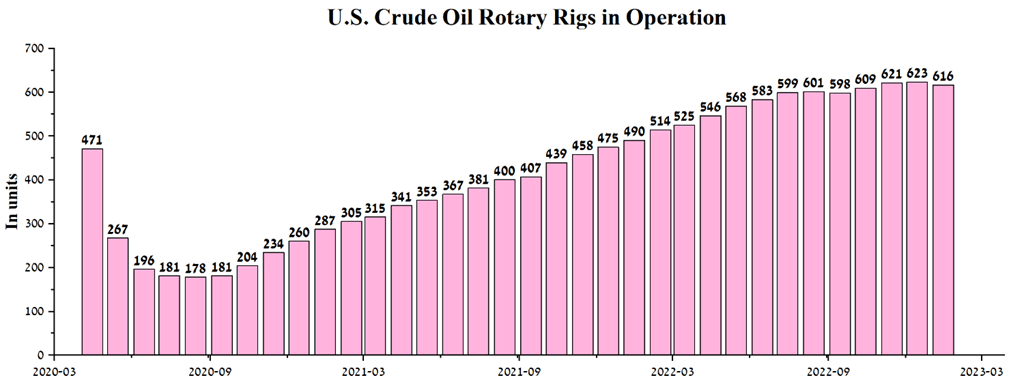

A decrease in inflation will slow down the pace of interest rate hikes by the Fed. According to my calculations, I expect another 0.5% increase in 2023, after which the Fed will again stimulate borrowing and investment, forcing the U.S. economy to grow significantly. As the Fed cuts interest rates, this will drive down borrowing costs, prompting oil and gas companies to invest in expanding oil production and building refineries, thereby lowering fuel prices and replenishing the U.S. Strategic Petroleum Reserve. Even under current conditions, the number of operating oil rigs in the U.S. in January 2023 was 616, up 126 from January 2022.

{kind=link}

Author's elaboration, based on the EIA report

As a result, I expect average US oil production to reach 12.51 million bpd in 2023, up 610,000 bpd from 2022. While according to the results of 2024, this value will increase to 12.7 million barrels as the situation with hiring workers improves and labor costs stabilize.

Conclusion

The oil and gas industry has continued to be under pressure in recent months. Thus, natural gas prices reach multi-month lows despite the war in Eastern Europe, and WTI oil remains in a downward price range and trades at $76.70 per barrel, moving further and further away from the peaks reached in March 2022. Despite the decline in revenue and margins of most companies included in the Energy Select Sector SPDR Fund over the past two quarters, the value of their shares remained near multi-year highs.

In the short term, I expect billions of dollars of buybacks in Exxon Mobil and Chevron Corporation, a recovery in economic activity in China and India, and the expectation by many market participants of replenishing the U.S. Strategic Petroleum Reserve to support non-renewable energy prices. However, a significant increase in U.S. stocks of oil, gasoline, and other fuels, declining inflation, and the expected reduction in interest rates will contribute to an increase in oil and gas drilling rigs, thereby increasing supply in the market, which will ultimately increase pressure on the share price of the Energy Select Sector SPDR fund.

Already, one can observe the emergence of a trend among investment funds to reduce investment in the energy sector, preferring technology and pharmaceutical companies instead of oil and gas companies, which are less dependent on raw material prices. For example, Tesla's share price (NASDAQ: TSLA ) has risen by about 100% in less than a month, and Meta Platforms' share price (NASDAQ: META ) by 108% since October 2022, while the share prices of both Chevron Corporation and Exxon Mobil have not been able to show the same agility.

For further details see:

Is It Worth Investing In Oil And Gas Companies In 2023