PSA - Is My 'KISS' On Your List?

Summary

- I’ve used the term KISS before, and I’m hardly responsible for coining it.

- For those of you who are new to my page, it stands for “keep it simple, sweetheart.”.

- The message is clear: Don’t complicate what doesn’t have to be complicated.

- In this article, I will reveal the first four picks for my mother's brand-new income portfolio.

'Tis the season to buy chocolates, roses, and expensive jewelry. And by that, I of course mean that it's February. And Valentine's Day is right around the corner.

Normally, I stress out a little bit about remembering the date. But perhaps I was especially alert this year, since I thought it was this week and not next.

I guess better early than late, right?

My wife is very much into the holiday, you see. Honestly, I always assumed that most women were, but apparently that's not entirely true. Alliant Credit Union wrote last year that:

"Ninety-four percent of Americans believe in true love, according to Statista. So it's no surprise to see that 52% of Americans plan to celebrate Valentine's Day in some way with family members, friends, etc."

That's quite the difference between 94% and 52%, to say the least. Especially when you consider the "some way" part of the statement above. That could include simply saying "Happy Valentine's Day" for all we know. Or making a meal together at home.

In which case, there are definitely men (and women) out there who spend less money than I do on the event.

Speaking of spending, the Alliant writeup continues with these 2021 statistics from the National Retail Federation:

"… the majority of [those surveyed] said they planned to spend money on candy. Forty-four percent said they would spend money on Valentine's Day cards. Thirty-six percent on flowers and 24% on an evening out."

Only 18% were going to buy jewelry.

It's the Giver and Givee That Counts

Here's the thing about the jewelry-buying crowd though… They were the big spenders, racking up $4.1 billion in total.

They say that love hurts. And clearly, sometimes it's our wallets that feel the pain.

Then again, when it's the right person, he or she is worth the cost. Because you know he or she will be there for you even if those gifts and the money behind them dries up.

The presents, you know, are appreciated. But you also know you're appreciated even more.

In short, some people are worth falling in love with - one of the many ways they differ from stocks. You can fall "in like" with the companies you consider and ultimately own.

But buyers beware! These are businesses you're putting money into. They might be made up of people, but those people probably don't know you. You're a concept to them.

A number.

One very small part of a whole.

And while they may - and hopefully do - consider all that very important, they're still not in love with you. They're not going to die for you, and woe to the investor who forgets that fact.

Fortunately for Will104, he hasn't. This wise man commented on one of my recent iREIT on Alpha articles that:

"Shouldn't fall in love with stocks, but if I did break that rule, ARCC would be the one.

"However, have rotated recently some of my position to OCSL and BXSL, as they have higher concentrations of first lien/senior loans and a bit of a yield pick up."

To which I replied:

"Ha. I will likely put this in the new KISS (Valentine's appropriate) portfolio…. All the best. Brad."

That's what this article is all about: keeping my word and debuting a bouquet of stocks that will outlast roses any day.

Keep It Simple… Sweetheart

I've used the term KISS before - and I'm hardly responsible for coining it - but for those of you who are new to my page, it stands for "keep it simple, sweetheart." Or, if you're feeling less charitable and/or have a more sardonic sense of humor, it could stand for "keep it simple, stupid."

Either way, the message is clear: Don't complicate what doesn't have to be complicated.

We have a bad tendency to do the exact opposite, unfortunately. I know it. You know it. The global population knows it.

And if you think otherwise, you're either insane, an absolute inspiration… or simply old enough with enough experience to know better.

I'm not trying to step on any of my fellow expert analysts' toes here, but all of those theories and models and predictive logarithms are unnecessary. It's not that they do or don't work.

You just don't need them to. Not when all you need is a properly diversified portfolio full of quality, dividend-paying companies.

(Warren Buffett would argue that you don't even need the "properly diversified" part. But I just can't completely get on board with that advice - even from the Oracle of Omaha.)

Again, no company is worth falling in love with. Even the most "qualitiest" company can potentially let you down.

But that "properly diversified portfolio full of quality companies" I just mentioned has very little chance of failing you… if you hold it over time instead of letting the market's often volatile temperament dictate your investing actions.

I stand by all of my portfolios, mind you. But I think this one especially will offer a whole lot to like (not love), starting with these real estate investment trusts (REITs)…

Hard To Beat this Fortress REIT

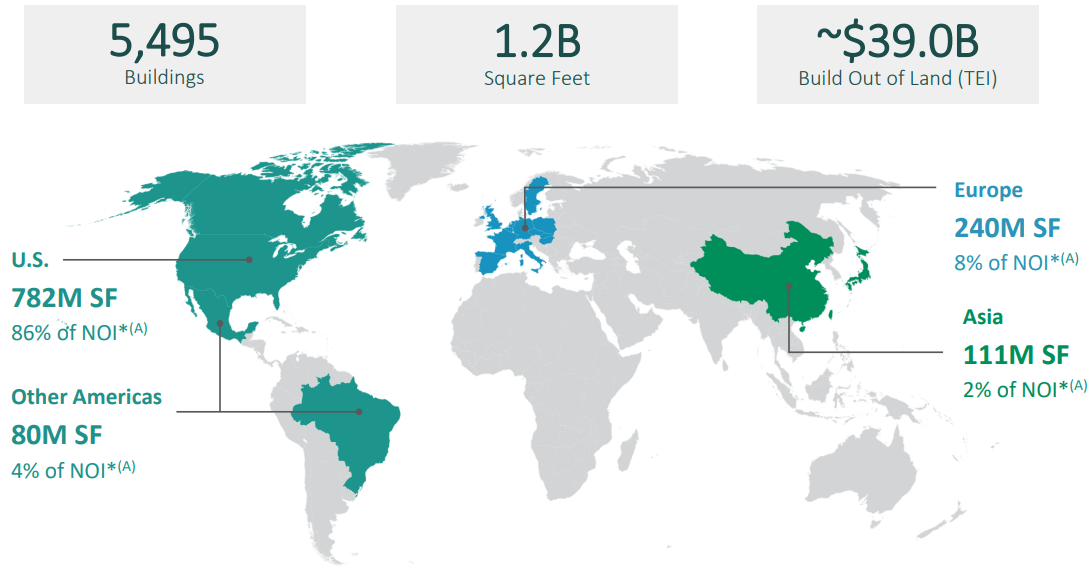

Prologis, Inc. ( PLD ) is a REIT that specializes in industrial properties and has the largest market capitalization of any REIT.

Prologis has an established international footprint with 5,495 properties spread across 19 countries that serve 6,300 customers and process 2.5% of global GDP through their distribution centers. In all, they have 1.2 billion square feet of real estate and have $39 billion invested in land banks for future expansion.

{kind=link}

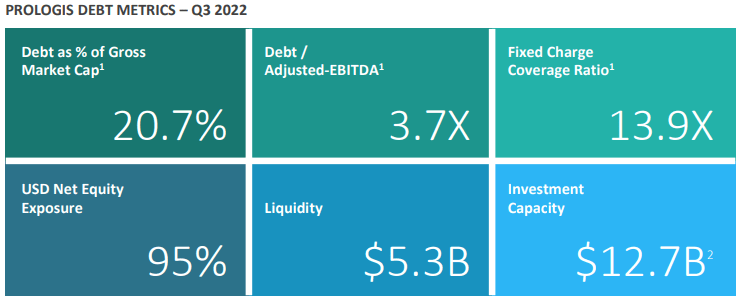

Prologis has some of the best debt metrics in the REIT sector with a Debt to Adjusted EBITDA of 3.7x, a Fixed Charge Coverage ratio of 13.9x and debt as a percentage of market capitalization of 20.7%. They have an A credit rating and 5.3 billion in liquidity as of the third quarter in 2022.

{kind=link}

Prologis has an average funds from operations ("FFO") growth rate of 11.11% and a 10-year average dividend growth rate of 11.13% and currently pay a 2.43% dividend yield. The dividend is secure with a 2022 AFFO payout ratio of 72.31%.

{kind=link}

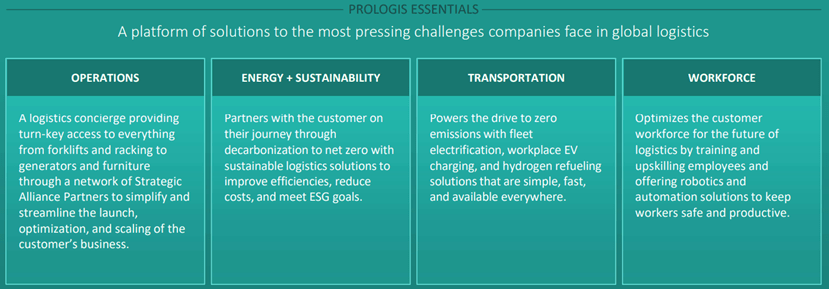

Prologis more than a real estate company that collects rent checks. They have built-up multiple sources of ancillary income streams that complement their real estate business.

Prologis Essentials is a platform of solutions offered to clients to help them navigate the challenges involved in global logistics. Through a network of strategic partners, the Essentials Platform offers turn-key access to racking, forklifts, overhead lighting, generators and even furniture to help streamline and optimize their client's business.

They also offer moving and relocating services to help dismantle, transport and re-install equipment in the new location, whether it's a warehouse owned by Prologis or not. Additionally, the Essentials Platform aids in workforce training and offers robotics and automation to increase workforce productivity.

{kind=link}

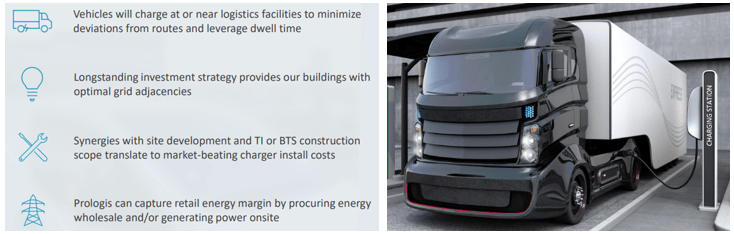

One of the more intriguing aspects of the Essentials Platform is the installation of solar panels and electric vehicle ("EV") charging stations. As of 11/29/2022, Prologis ranked 2nd in the U.S. for on-site solar rooftops.

Prologis - Press Release

As vehicle fleets increasingly become electrified, Prologis has the capability to harness energy at the wholesale level and capture retail energy margin through its EV charging stations and by providing power onsite.

{kind=link}

Prologis is one of the highest quality REITs you can own. It is currently trading at a premium to its 10-year blended P/FFO average of 22.98x with a current FFO multiple of 25.07x, but Prologis' growth has accelerated since the pandemic and their average FFO multiple over the last 3 years has been 28.89x.

I believe the continuing evolution of e-commerce, along with Essentials Platform and the potential in EV charging will continue the recent growth acceleration. At iREIT, we rate Prologis a BUY.

{kind=link}

O, O, O, It's Magic

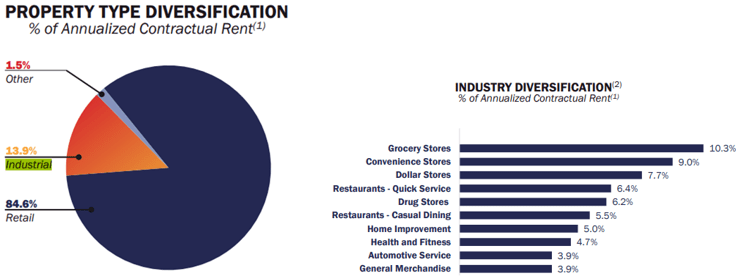

Realty Income Corporation ( O ) is a Real Estate Investment Trust with a primary focus on single-tenant freestanding net lease properties. They are well diversified by industry with Grocery, Convenience, and Dollar Stores making up their top 3 industries as a percentage of contractual rent.

While Realty Income has a primary focus on retail properties, they also have exposure to industrial properties. As of the 3rd quarter of 2022, Realty Income received 13.9% of their contractual rent from industrial properties.

{kind=link}

Realty Income has approximately 11,733 properties in all 50 States and an international presence with properties in the UK and Spain.

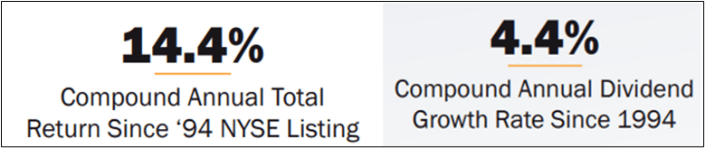

The company was founded in 1969 and went public in 1994. Since going public, Realty Income has delivered a 14.4% compound annual total return as well as a 4.4% compound annual dividend growth rate.

{kind=link}

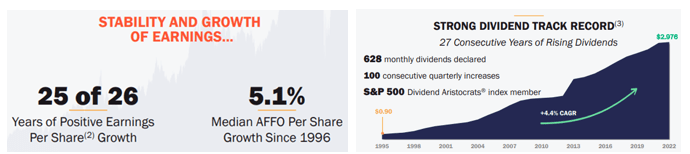

Realty Income is one of the few REITs that qualifies as an S&P 500 Dividend Aristocrat, with 27 consecutive years of dividend growth. The dividend is paid monthly and currently yields 4.43% on an annual basis.

The dividend is well covered with an estimated Adjusted Funds from Operations ("AFFO") payout ratio of 76.17% in 2022. They have shown solid earnings growth with 25 out of 26 years of positive AFFO growth and a median AFFO growth rate of 5.1% since 1996.

{kind=link}

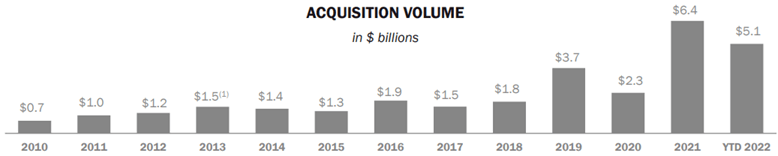

Realty Income shows no signs of slowing down, either, with $5.1 billion in Acquisitions in 2022. Their acquisition volume in 2022 was more than any other year in the last decade, with the exception of 2021, when they acquired VEREIT.

{kind=link}

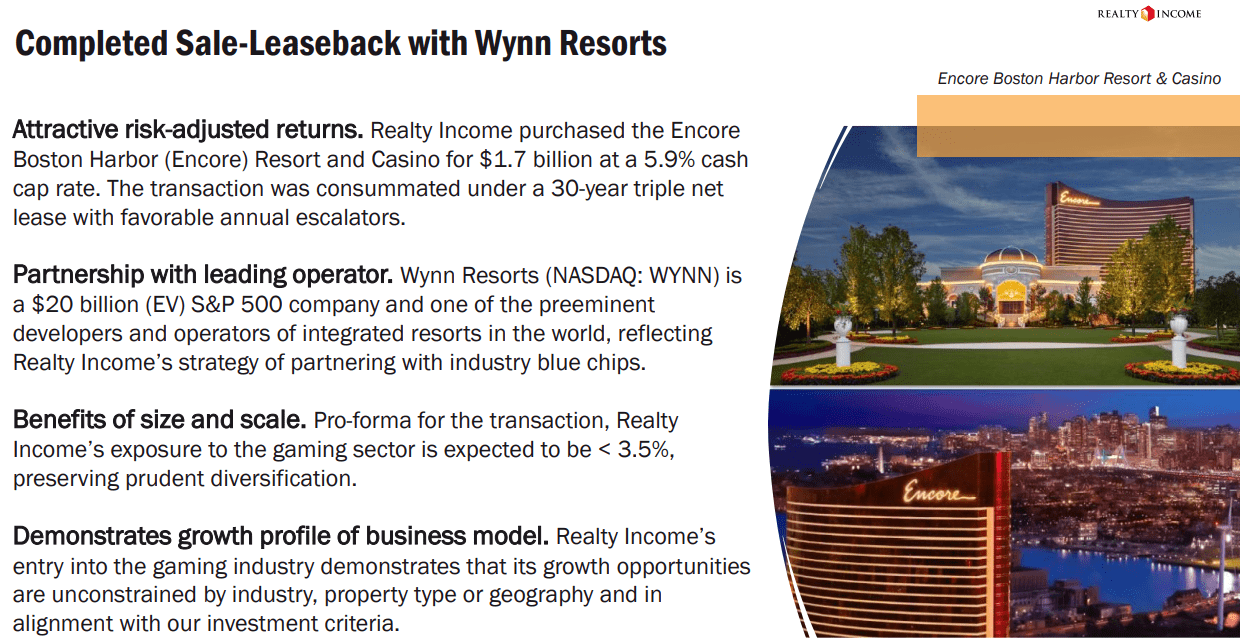

One of their largest deals recently was the sale-leaseback with Wynn Resorts (WYNN) for $1.7 billion at a 5.9% cash cap rate. The sale-leaseback is structured as a 30-year triple net lease with built-in annual escalators. After the transaction, Realty Income expects its exposure to the gaming sector to be around 3.5%, further diversifying their portfolio of properties.

{kind=link}

In another acquisition in late 2022, Realty Income announced that they were acquiring up to 185 single-tenant properties from CIM Real Estate for $894 million at a 7.1% Cash Cap Rate with a weighted average remaining lease term of approximately 9.2 years. The robust acquisition pipeline should continue to fuel AFFO growth, which in turn should continue to fuel dividend growth.

Realty Income has good credit metrics with a Net Debt to Pro Forma Adj EBITDAre of 5.2x and a Fixed Charge Coverage ratio of 5.5x. Their debt as a percentage of total market capitalization is 31% and 88% of their debt is at a fixed rate. Additionally, 95% of their debt is unsecured and they have a weighted average term to maturity of 6.3 years.

Realty Income - Investor Presentation

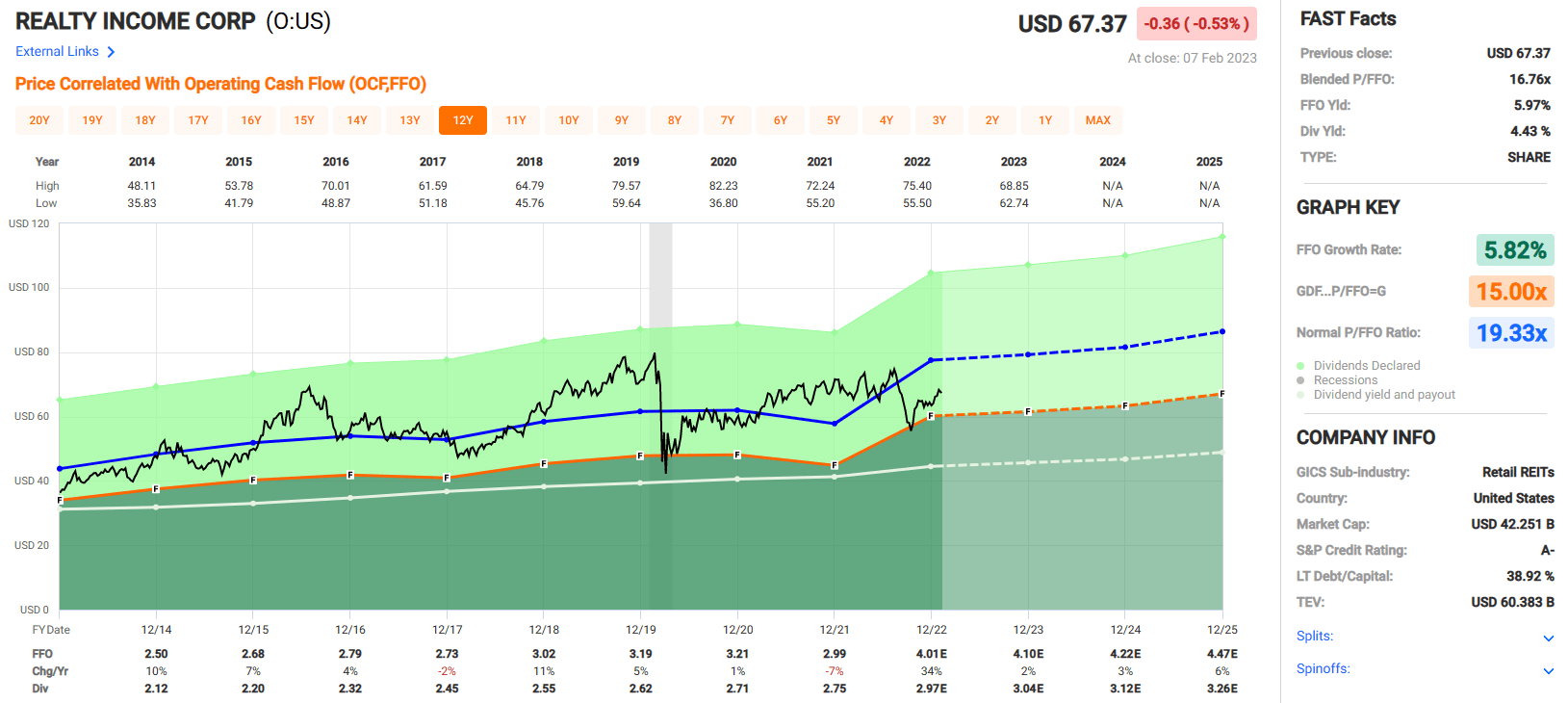

Currently Realty Income trades at a blended FFO multiple of 16.76x which is well below their normal P/FFO ratio of 19.33x. Realty income is one of the most reliable REITs for consistent earnings and dividend growth.

Their acquisition pipeline is robust which should continue to fuel growth. They have grown earnings through multiple recessions and have continued to pay and increase the dividend without interruption. At iREIT, we rate Realty Income a BUY.

{kind=link}

A Healthy Healthcare REIT

Healthcare Realty Trust Incorporated ( HR ) is a healthcare REIT that specializes in ownership, development, and management of Medical Office Buildings ((MOB)).

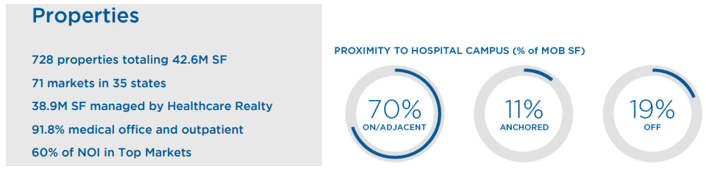

As of the third quarter of 2022, HR's portfolio consisted of 728 properties, serving 71 markets, located in 35 states and covering a total of 42.6 million square feet. In July 2022 Healthcare Realty merged with Healthcare Trust of America to become the largest MOB REIT in America.

Healthcare Realty's properties are well diversified by geography, tenant size, and physician focus. For more than two decades Healthcare Realty Trust has established connections with leading health organizations and has developed its portfolio of properties towards multi-tenant, on-campus medical office buildings that provide stable occupancy and high retention. As of the third quarter 2022, HR had an occupancy rate of 87.7%.

The proximity of HR's medical office buildings to hospitals and other health systems is critical to the physician-hospital relationship. Most of HR's properties are either on campus or adjacent to these health centers and provide outpatient services that include imaging, surgery, cancer treatment, and medical offices for physicians.

{kind=link}

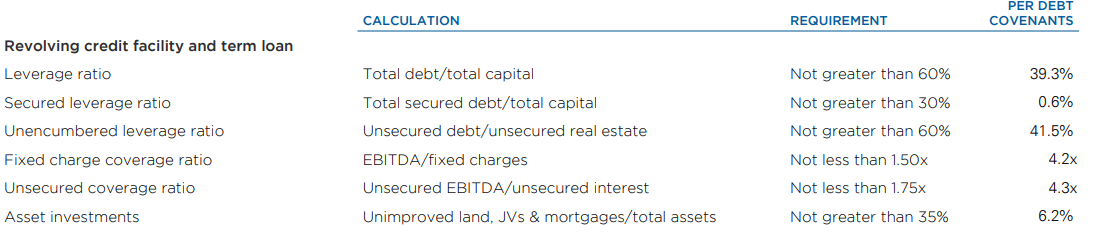

Healthcare Realty has reasonable debt metrics with a Net Debt to adjusted EBITDA of 6.3x and a Fixed Charge Coverage of 4.2x. Their total debt as a percentage of total capital is 39.3% and they have a BBB credit rating.

HR - Supplemental

{kind=link}

Healthcare Realty has ample liquidity with $57.5 million in cash and $1.3 billion available under their unsecured credit facility. Additionally, they list $14.2 billion in unencumbered assets that could be sold to raise cash if necessary.

HR - Supplemental (dollars in thousands)

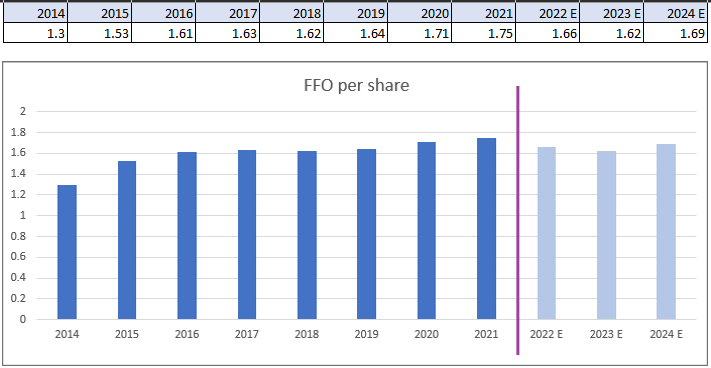

Since 2014, HR's Funds from Operations has seen reasonable growth with an FFO growth rate of 2.87%. Between 2014 and 2021, there was only one year where there was a decline in FFO (2018). Analyst project 2022 FFO to come in at $1.66 per share which would be a decline of 5% from their 2021 FFO of $1.75. Healthcare Realty is set to report fourth quarter results for 2022 on March 1, 2023.

{kind=link}

HR's dividend growth since 2014 has been modest with a compound annual growth rate of 1.51%. This does not include the dividend paid in 2022 which was $6.24, for an increase of approximately 385%.

The large payout in 2022 was the result of a special dividend paid in July 2022 in connection with the HR / HTA merger and does not reflect the normal dividend growth trend since 2014.

{kind=link}

Similarly, the high 2022 AFFO payout ratio of 474.75% is due to the special dividend and does not reflect HR's normal AFFO payout ratio. However, even if we exclude the special dividend, HR has had a high AFFO payout over the last couple of years. In 2021 the AFFO payout ratio was 100.39% and came in at 95.83% in 2020.

The high payout is concerning but should improve in 2023, according to analyst estimates that project AFFO in 2023 to come in at $1.32 per share and a dividend payment of $1.25 for an estimated AFFO payout of ~95% in 2023. This is still a high payout but shows improvement over the 2022 and 2021 levels.

{kind=link}

Currently HR has a dividend yield of 5.9% and is trading at a P/FFO multiple of 12.71x, which is a discount to its normal P/FFO multiple of 17.38x. Although historically HR has not been a high growth REIT, it pays a high yield and is heavily discounted when compared to its normal FFO multiple. We rate Healthcare Realty a Spec BUY.

{kind=link}

I Love These Orange Doors

Public Storage ( PSA ) is a self-storage real estate investment trust. Their first self-storage facility was opened in 1972, and since that time they have grown to become the largest owner, operator and developer of self-storage properties.

They have 2,836 owned properties in 40 states and serve 1.8 million customers. They have been in business for 50 years and currently own 202 million rentable square feet of real estate.

{kind=link}

Public Storage has excellent debt metrics with a Debt to EBITDA of 2.2x, a Net Debt + Preferred to EBITDA of 3.3x, and a Fixed Charge Coverage of 9.3x as of the third quarter of 2022. Additionally, they have a credit rating of A2 / A by Moody's and S&P.

PSA - Financial Statement

In recent years PSA has expanded its portfolio far more than its closest competitors. Since 2019 PSA has invested $8.0 billion in acquisitions and development and has added 42 million square feet of real estate for a 26% increase in portfolio size.

{kind=link}

In a recent news, PSA made a $11 billion hostile bid for Life Storage ( LSI ) in an attempt to buy its smaller competitor after its earlier takeover attempts were rejected. The proposal is for an all-stock deal where Life Storage shareholders would receive 0.4192 shares of Public Storage for each share of Life Storage.

PSA decided to make the takeover public after Life Storage had rejected a previous offer with similar terms. If the deal goes through, it will further consolidate a fragmented industry and save costs and increase efficiencies for the company. The deal should be moderately accretive (estimated 3% growth in 2023) based on a cap rate in the 5% arena.

Life Storage has 1,172 stores in 37 states with over 675,000 customers so the acquisition would complement PSA's operations well. Currently PSA has a total market cap of 53.04 billion, while Life Storage has a market cap of 10.37 billion.

PSA - News Release

In other recent news, PSA announced a 50% increase in its quarterly dividend from $2.00 to $3.00 per share. The increase works out to an annual dividend of 12.00 per share vs its previous rate of $8.00 per share.

PSA - News Release

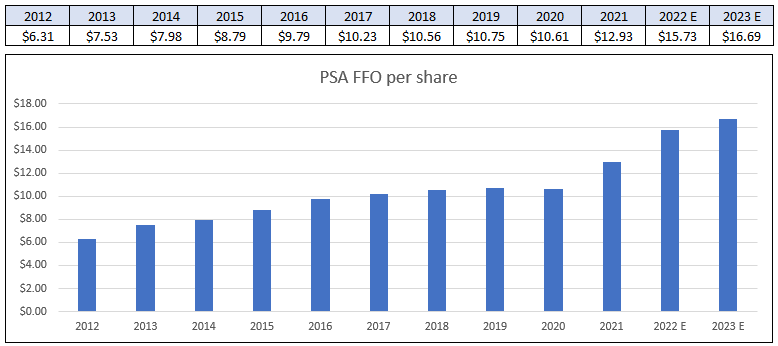

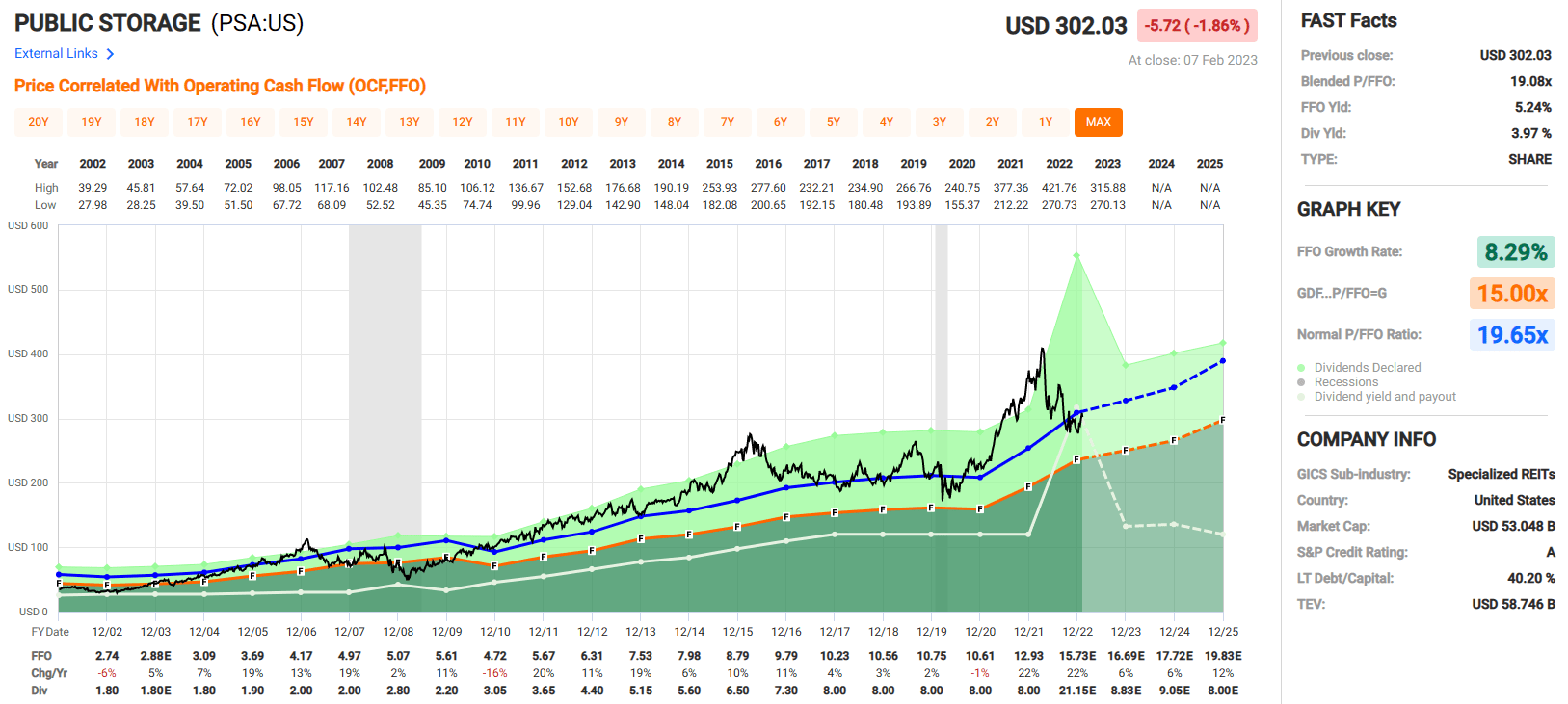

Public Storage has delivered strong growth in its Funds from Operations over the last several decades. Going back to 2003, PSA has a blended FFO growth rate of 8.29% and from 2012 until 2022 PSA averaged an FFO growth rate of 9.72%.

{kind=link}

PSA pays a 3.97% dividend yield which is well covered with a typical AFFO payout ratio ranging between 72% to 82% since 2012. The 2022 AFFO payout is 164.37% but that is due to a one-time special dividend of $13.15 per share in connection with the PS Business Parks merger. Excluding the special dividend, PSA has an expected AFFO payout of 58.86% in 2022.

{kind=link}

Currently PSA is trading at a blended P/FFO of 19.08x which is a slight discount to their normal P/FFO multiple of 19.65x. The company has great debt metrics and has been very active in acquisitions recently which should fuel continued growth in their FFO. They pay a high yield at almost 4% that is very secure with a low AFFO payout. This is a very high-quality company that trades at fair value. At iREIT, we rate Public Storage a BUY.

{kind=link}

Mother Knows Best

In recently returned from a trip to Florida and I took my mother with me to celebrate her birthday. Here's a picture below of me and my mom (just after we are a delicious Baked Alaskan at The Breakers in West Palm Beach).

Twitter (@rbradthomas)

My mom has been in the real estate industry for over four decades, and she inspired me to obtain my real estate license when I was just 17 years old. I watched her sell homes for many regional and national homebuilders and she taught me the concept of buying low and selling high.

Of course, in the stock market we call the "investing with a margin of safety," and that is precisely what I decided that I would do with my mom's brand-new KISS portfolio…buy high-quality REITs when they're on sale.

Tomorrow morning, I will be helping my mom set up a new account modeled after all of my new trades in the KISS portfolio. I'll track these results with members at iREIT on Alpha and hopefully I can get my mom to begin chatting with us in the active chat room (at iREIT on Alpha ).

As always, thank you for reading and commenting…

...let me know if my KISS is on your REIT list?

Happy SWAN Investing!

For further details see:

Is My 'KISS' On Your List?