OGN - Is There Anything Organic Or Interesting About Organon?

Summary

- Organon is a business I own - but only due to being awarded a significant number of shares, some of which I actually sold early on. I kept a stake.

- In this article, I'm going to follow a subscriber request and dive into what Organon might do for its shareholders, if you did not sell, or may be interested.

- My first article on Organon establishes the base case here, and it's as follows.

Dear readers/followers,

In this article, I will be taking a look at Organon ( OGN ), a company in the pharma space. Organon has a bit of a complex history, which we will go through here. Its roots go back to the early 1920s, but its current iteration was founded in 2020.

The company is a pharma stock with annual revenues of around $6.5B on an annual basis, employing roughly 9,000 people across the world. It's not a small company, nor is it one that should be overlooked for what it does in terms of its operating segments.

Let me show you what I mean.

The appeal of Organon

The company's original roots go back to the Netherlands when it was founded as a separate part of a meat factory. In the end, it started producing insulin and began producing estrogens in the 1930s. The company acquired several new businesses during the '40s and '60s and merged to become AKZO, later Akzo Nobel (AKZOF). In fact, Organon was the human health care business of Akzo Nobel.

The company has multiple milestones under its belt, including the M&A of Diosynth in -04. The company was acquired in -07 by Schering-Plough as part of a package deal with Akzo Nobel, which also included the vet pharma business Intervet. This also meant that Organon moved to New Jersey. This was short-lived, because Schering-Plough ended up merging with Merck & Co (MRK), known as Merck Sharp & Dohme or MSD outside the United States and Canada.

{kind=link}

Again, this was also to be relatively short-lived. No more than 10 years later, Merck & Co. announced that Organon & Co will be the name of a potential spin-off in the following categories.

{kind=link}

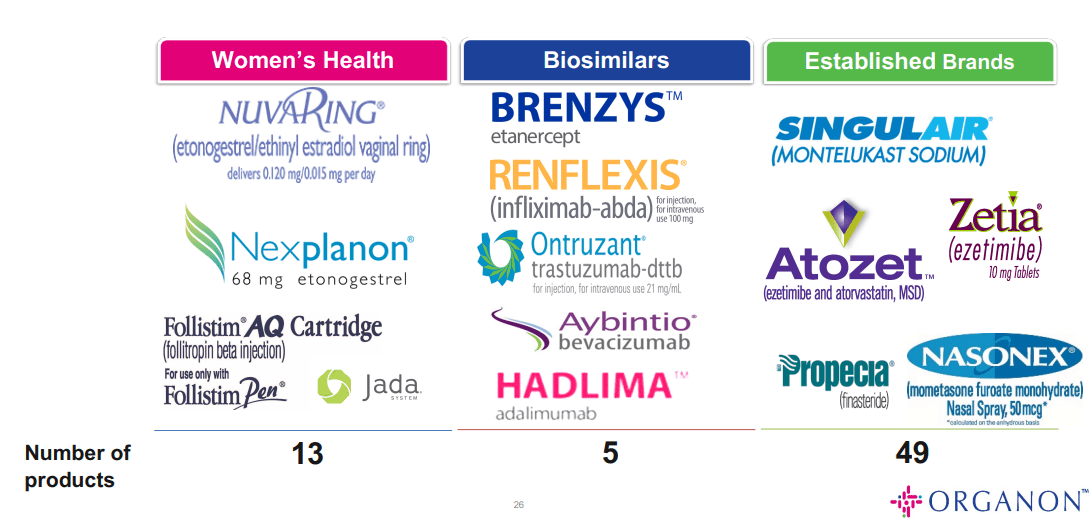

So that's essentially where Organon ended up. As a pharma company in the theoretically attractive fields of Women's Health, Biosimilar, and legacy brands. This is also the company's ambition, its goal. To build a portfolio rich in Women's Health brands, in solid biosimilars, while making sure that the company's established brands, which do represent most of the company's revenues (over $4B in 2021, out of a total of $6B, with Women's health at around $1.6B and Biosimilars at less than $450M), remain stable earners.

This isn't an unattractive prospect as such. Some of the company's larger brands include:

- Nexplanon, the biggest brand in Women's Health for Organon, which is a birth control implant that goes into the arm of the patient. This was close to 50% of 2021 sales in the segment.

- Follistim is a product designed to induce ovulation and pregnancy in functionally infertile patients (not due to ovarian failure).

- NuvaRing, birth control/contraceptive product.

- Renflexis, a biosimilar for Remicade used to treat RA.

- Ontruzant , a biosimilar to Herceptin for treating breast cancer

As well as a host of established legacy brands, with the majority of sales in Cardiovascular, Respiratory, Non-Opioid Pain, and other segments. Since the company was spun off, the company has increased its available cash and reduced its debt whenever possible. In less than 6 months, the company lowered its net debt by $600M, and reported very decent constant currency growth, despite some very significant 2021A headwinds.

3Q22 is the latest results we do have that are relevant here - and since 2021A, the company has seen good revenue growth in single digits - the third consecutive quarter of relevant revenue growth, as it happens, with solid EBITDA on an adjusted basis of Half a billion, meaning close to 33% adjusted EBITDA margins.

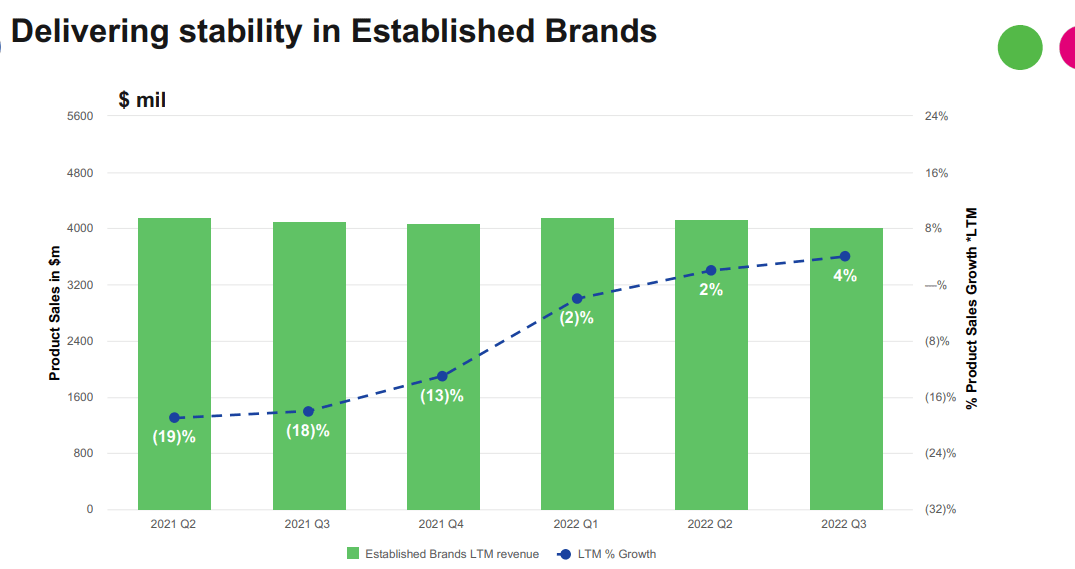

And take a look at what happens in the company's most unstable segment, the legacy brands one.

{kind=link}

Good development, isn't it? In terms of geographical development, APJ and US are where the growth currently is, with 6% YoY for the US and only 1% negative in APJ. That's better than the 11% decline in EU/CA, and 4% in China. Organon has a very attractive overall volume and sales mix on a geographical basis.

OGN IR (OGN IR)

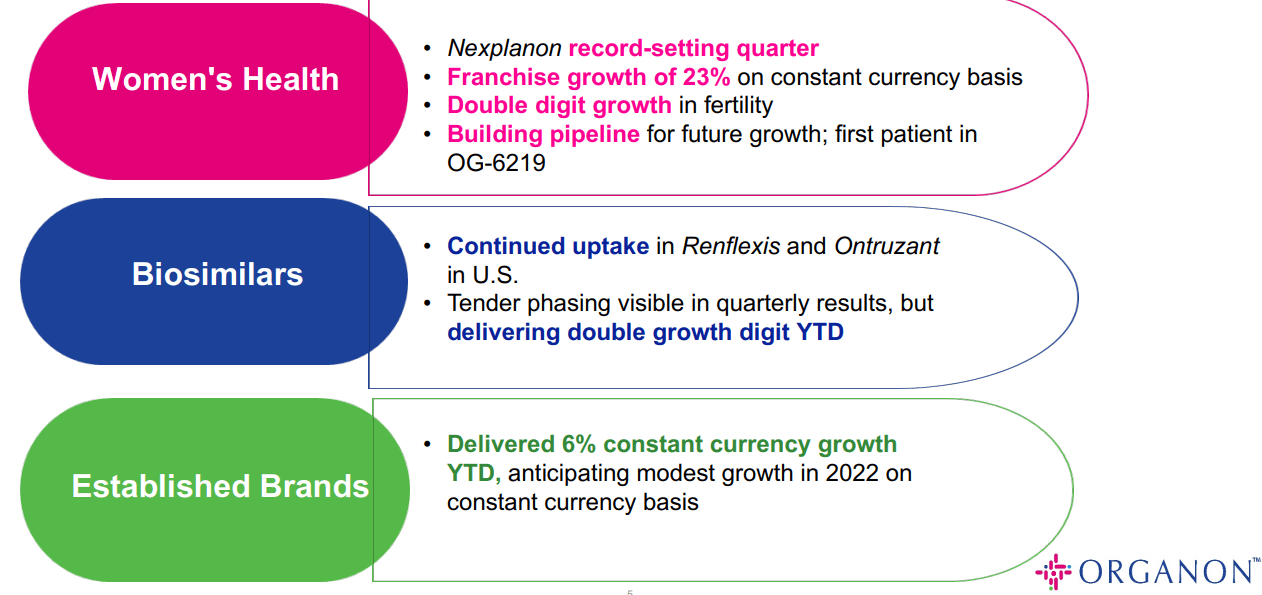

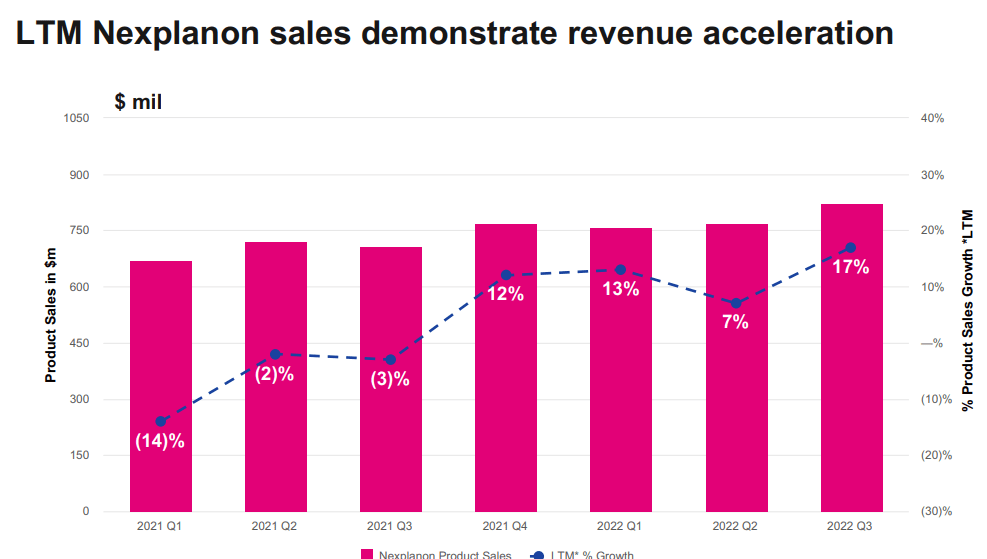

The company's growth vectors, including Women's health with Nexplanon, saw its best quarters, with a double-digit YTD growth in fertility. 10%, to be specific, with a 1% growth in Follistim. Biosimilars had an amazing quarter as well, with Renflexis up 22%, Brenzys up 48%, and Hadlima up 51% - though that last one was from single digits, so not really all that relevant to the bigger picture.

{kind=link}

Looking at OGN at this time is focusing on the stability of legacy. If legacy goes volatile or goes away, OGN is in big trouble. Thankfully, we have a good development here, with only a 1% decline for the year. Respiratory was even up 7%, and the company expects a modest constant currency revenue growth, despite what's happening in 4Q22.

Company P&Ls are solid. Compared to a 2022 YTD on a YoY basis, the Cost of sales is down, the gross profit is up 2%, and the company is pushing its R&D further - up 44% here.

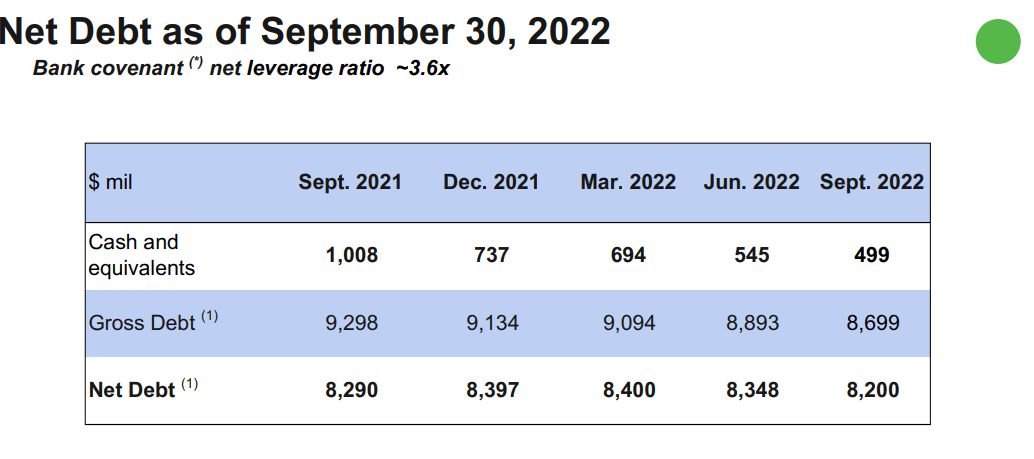

Net debt is one of the more important parts - unfortunately, not much has happened on that front since late 2021.

{kind=link}

The overarching high-level picture for Organon as of this quarter is a good quarter, but heavily impacted by FX. The company's significant, half-billion volume growth is almost completely hidden by a $400M FX and $70M SCM impact. The company has updated 2022E guidance, expecting a significant 5-6% FX impact, but calling for around $6.2B in annual revenues, down around $100M on the high end compared to 2Q22.

I don't see any high-level worries about the company's near-term sales. Organon's pipeline is under construction, and Organon is adding licensing agreements for several candidates and agents, as well as M&As, including the 2021 one of Forendo Pharma.

I believe Organon is building an attractive portfolio of very solid drugs in appealing fields. The one I am least certain about is actually its legacy products - but as far as Women's health and biosimilars go, I believe these are very solid segments with proven, future growth potential.

However, Organon does not have IG rating. It's at a flat BB. Organon does have a dividend, and that dividend is actually fairly solid at 3.76% at current pricing. Its limited history makes traditional valuation approaches somewhat difficult, but we'll find a way to properly evaluate this business in the valuation section.

It has a current market capitalization of roughly $7.7B. I'm not much worried about the company debt - I believe that the company can easily pay this down given time.

Now, I sold most of my assigned Organon on the first trading day. Why did I do this? Because I did not like the headwinds in terms of margins, in terms of initial lack of growth, in terms of where the valuation was implied to be. This proved to be the right choice because Organon has delivered negative growth since its spinning off, and that money was invested into far more profitable ventures.

However, since selling all but a small watchlist position, Organon has sort of stabilized. We now have some idea of where the company might go, how the risks are looking, and how bad the expected margin pressures actually are (they're pretty bad). That's the bearish case.

The bullish one focuses on the new licensing deals, the M&A growth potential, and where the company goes from a dirt-cheap valuation, which Organon is actually at.

Let me clarify.

Organon's Valuation

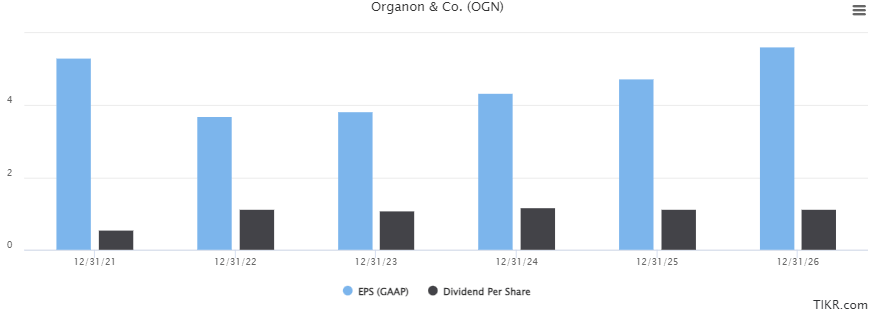

2022 is expected to be the real trough for the company. After that, Organon is expected to significantly improve over time, to 2026E when earnings are close to the 2021 levels on a GAAP EPS level.

The dividends are expected to mostly move in line with this.

{kind=link}

I personally forecast an EBITDA/sales growth of around the same level - 4-8% depending on how well some of the company's ambitions, licensing, and other deals work out. EBITDA margins are expected to go nowhere, still sub-32% in EBITDA in 2026E.

S&P Global gives the company a range of targets starting at a low of $24, and a high of $43 - quite a wide spread. 9 Analysts follow the company, with an average of $33.5/share. 6 out of 9 of them are either at a "BUY" or an "Outperform". The general view is that Organon, at sub-$30/share, is undervalued. Generally speaking, I would agree with this assessment. OGN trades at less than 7x P/E on an NTM normalized basis.

One big flaw I've seen other analysts do is liken OGN to businesses like Bristol Myers ( BMY ), AbbVie ( ABBV ), or Merck ( MRK ). However, this is flawed. There's too little overlap in sectors for this to be a comparable thesis or multiples, and in terms of size and history, there isn't enough to go on here either. By that logic, because the company trades at less than 7x, and closer to 6x normalized, it's massively undervalued to MRK, which is at 14x.

The problem with Organon really is EBITDA growth and margins, which despite many moves the company is making, is seeing significant pressure with a strong FX from the dollar, and less success in offensive pricing strategies. Net debt is flat because the company's cash flow conversion is poor, and this is making investors cautious.

I actually believe this to be wrong at this time.

The mix of negative FX pressures, net debt being unchanged, and sales pressures have created an opportunity for value-conscious investors. Organon's true qualities and potential longer-term upsides are "hidden" by these momentary challenges, and coupled with a 3.5%+ yield, this is making Organon start standing out on my list.

I would much rather have started buying close to $25/share, but at the time I was focused on other companies. If the company does drop back down toward the mid-20s, all things being equal, that will be a solid "BUY" signal. Even at today's valuation, I would say things are cheap enough to where we can see our way clear to buying.

You'd have to accept the fact that the company is not (yet) IG. That's something I can swallow for this company with the circumstances we have here.

Keep in mind, the near term has virtually zero potential positive catalysts. This is a longer-term success story. However, if you're willing to play the patient value investor, I believe the upside here could be well towards 70-80% once the company's long-term growth ambitions start bearing fruit. At a 6.5x forward multiple, which is where the company currently trades, we're at 10% per year, or 33% until 2025E. I believe this to be an entirely realistic prospect.

Recent growth prospects from the quarterly, coupled with history and fundamentals and where the company currently trades, cause me to take the following stance for Organon at this particular time, and in establishing my first thesis for the company.

Thesis

- Organon is a potentially profitable, qualitative investment in Women's health, biosimilars, and an attractive portfolio of legacy assets that are generating decent sales. While the company has seen recent pressures on the EBITDA, debt, and sales side due to FX, pricing issues, and other things, the longer-term trends are far more promising.

- Provided that the upside starts materializing more here, I would say Organon is worth at least 6-7x P/E on a forward basis, which implies a $30-$35 price range. I go at the mid-point of this, coming to $33/share.

- That makes Organon a "BUY" here, even failing the investment-grade test.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills all but one of my criteria, making it a "BUY" here.

For further details see:

Is There Anything Organic Or Interesting About Organon?