POAHY - Is Volkswagen Financial Services An Asset Or A Liability For The Auto Maker?

2023-03-30 12:36:38 ET

Summary

- Volkswagen Group is separated into an Automotive and a Financial Services division.

- Financial Services are highly profitable and responsible for one quarter of the operating profit.

- Profit margins are higher than for the mass market automotive brands of the group, like the Volkswagen brand itself.

- Financial Services have a high penetration of deliveries, with about one quarter of deliveries being financed by the division.

(Note: all amounts in the article are in EUR. At the current exchange rate this is almost equivalent to USD.)

Introduction

It used to be a popular joke that some German companies are just the operating entity attached to a bank. While this was always a hyperbole, a lot of it is also in the past. Siemens ( OTCPK:SMAWF ) clearly is not a bank with an attached electricity department (anymore), it has actually spun off its energy division. In 2008 Porsche had a pre-tax profit of around 13.5bn, although more than 11bn was not from its car manufacturing business, but from financial derivatives . The outcome of this was that Porsche almost bankrupted itself and was rescued by Volkswagen ( OTCPK:VWAGY , OTCPK:VWAPY , OTCPK:VLKAF , OTCPK:VLKPF ). There is still a Siemens Bank, BMW Bank, Mercedes-Benz Bank, etc. – but Volkswagen Financial Services continue to stand out due to the size, but also profitability of the business.

I have read through various Seeking Alpha comments where it was discussed whether Volkswagen is the most indebted car maker in the world, or it has just a lot of customer deposits (Spoiler alert: it is the second one). The important question for investors is whether the Financial Services segment of Volkswagen is an asset or liability? Should you buy Volkswagen because of it, despite of it, or does it even matter?

While I do not think I have a definite answer to those questions, I hope I can shed some light on the context around them. Volkswagen just announced a reorganization of its financial services segment, so this is probably a good time.

Overview

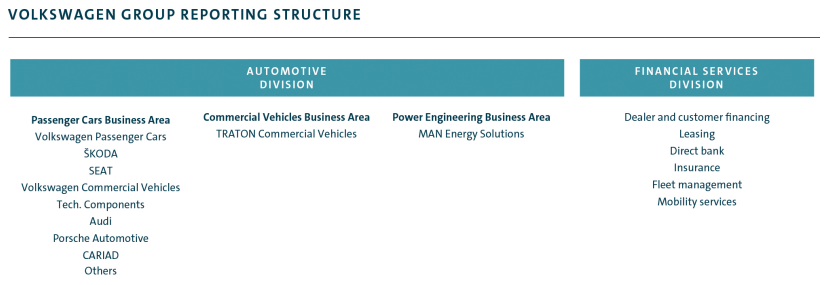

When you look at Volkswagen’s financial reporting , you will immediately notice that there are two segments/divisions, Automotive and Financial Services:

Volkswagen Group Reporting Structure (Source: Volkswagen Group Annual Report 2022)

{kind=link}

Quoting from the 2022 report of Volkswagen Financial Services AG , the key objectives of Financial Services are as follows:

- To promote Group product sales for the benefit of the Volkswagen Group brands and partners appointed to distribute these products

- To strengthen customer loyalty to the Volkswagen Financial Services AG and the Volkswagen Group brands along the automotive value chain (through the targeted use of digital products and mobility solutions, among other things)

- To create synergies for the Group by pooling Group and brand requirements relating to finance and mobility services

- To generate and sustain a high level of return on equity for the Group

I guess all this makes sense. Also, looking at the things listed below Financial Services Division (Dealer and customer financing, Leasing, etc.) in the image above - you would expect that a Financial Services organization within an automotive group does those things. Expect maybe one: mobility services. It is unclear what this is in a financial services context. We will look at this one later.

Financial Services are very profitable and have a high penetration rate

The Financial Services Division works with two key performance indicators, profitability and penetration rate. Again, I think this makes sense for a financial services organization within an auto manufacturing group. Obviously, the more profitable, the better. And the more vehicles are sold with financing or leasing (penetration rate), the more valuable the financing organization is to the overall group.

Profitability

The Financial Services Division is very profitable by itself and in comparison to the group profit margins. Return on equity was 14% in 2022, although RoE was even higher at 17.3% in 2021. While high demand for used cars and low risk costs were profit drivers, the division incurred a 0.5bn charge related to Russia.

As a way of comparison, Ally Financial (ALLY), which is mostly engaged in auto financing (but in the U.S.), had a RoE of 11.47% at the end of 2022 , also down from 19.47% YoY.

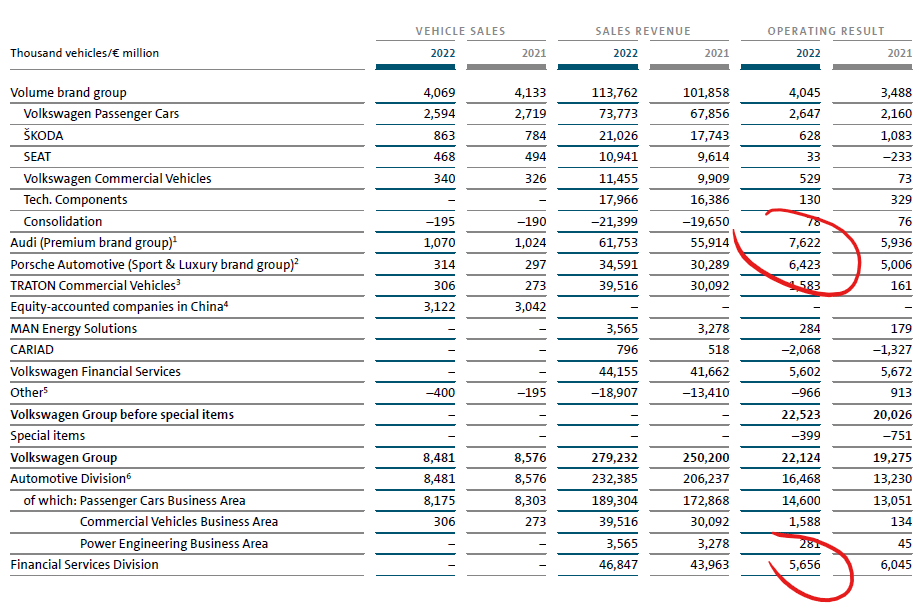

With 5.6bn, Financial Services were responsible for 1/4 of the 2022 operating result (25.6% exactly) of Volkswagen Group. Of the many brands within Volkswagen Group, only Porsche had a (slightly) higher operating result than the Financial Services Division. To put this in context: since the IPO in September last year Porsche AG has become the most valuable car maker in Europe! The Audi brand group shown in the table below also includes other luxury brands, especially Lamborghini and Bentley. By itself, Audi had an operating result lower than the Financial Services Division.

Volkswagen Group Operating Result break down (Source: Volkswagen Group Annual Report 2022)

{kind=link}

Penetration rate

Penetration rate is a key metric for Volkswagen Financial Services. It is expressed as the ratio of financed or leased vehicles compared to the total vehicle deliveries of the whole Volkswagen Group. In 2022 penetration rate was 32.3%. I think this is high, but in 2021 it was even higher at 35.8%.

A more detailed look at the Financial Services division

At the end of 2022 the Financial Services Division had assets of 263.4bn, which would make it not a super-large, but quite sizeable bank. The whole division is well capitalized, with a total equity of 38.2bn. The companies within the division use a diverse set of financing sources. They range from money market and capital market instruments to asset backed securities and retail customer deposits from its direct banking business (through Volkswagen Bank).

If it were not spread out over several companies (Note – a planned reorganization this year should change this), the division would be among the largest financial institutions in Germany. Its profit in 2022 was about the same as Deutsche Bank (DB), still the largest bank by far in Germany by asset size.

Due to this size, some numbers can look very odd when you look at Volkswagen Group as a car manufacturer. Net liquidity for Volkswagen Group was -125.8bn in 2022. This seems like one step away from bankruptcy. But if you look only at the Automotive part, it was actually +43bn. The same with debt. Total third party borrowings were 205bn, but on the Automotive side it is only 10.9bn.

Structure of the Financial Services Division

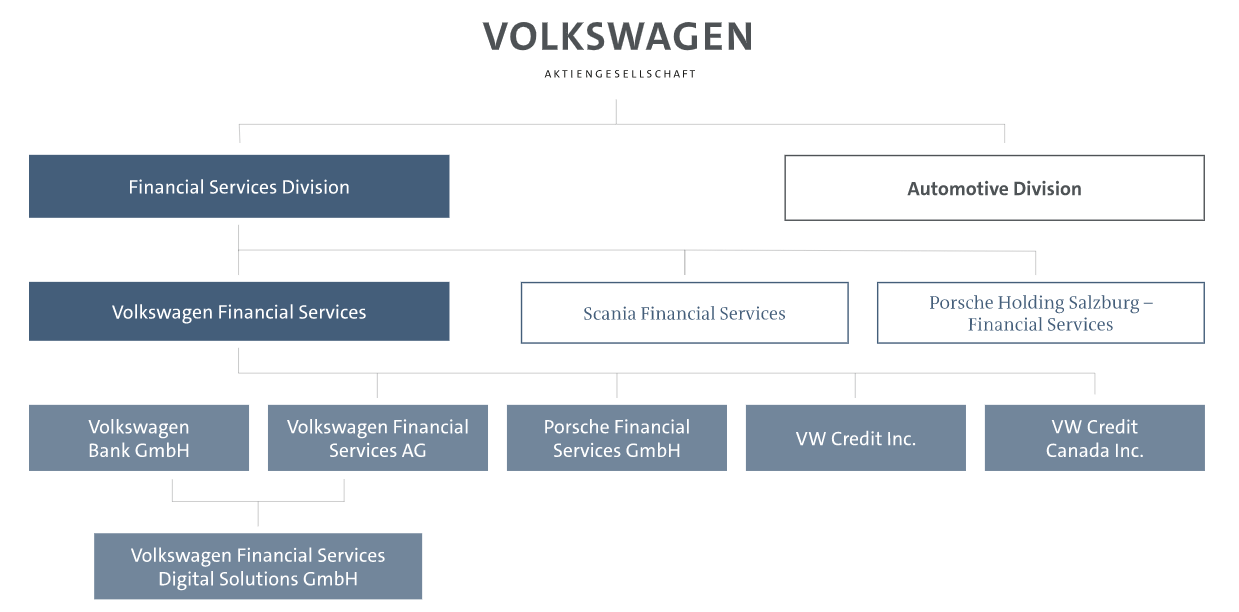

Volkswagen Financial Services operates in 47 countries and consists of a multitude of different companies:

Volkswagen Financial Services structure (Source: Volkswagen Group)

{kind=link}

The most important companies within Volkswagen Financial Services are Volkswagen Bank GmbH, Volkswagen Financial Services AG, VW Credit Inc, VW Credit Canada Inc, and Porsche Financial Services GmbH.

Banking operations within the European Economic Area (EEA, which is the EU plus Iceland, Liechtenstein, and Norway) are carried out by Volkswagen Bank, whereas the banking and lending business outside the EEA is managed by Volkswagen Financial Services AG.

Volkswagen Credit Inc. and Credit Canada Inc. are responsible for the lending and leasing business in the United States and Canada. Porsche Financial Services GmbH conducts all lending and leasing business for the Porsche brand.

Planned reorganization

On March 1 this year, Volkswagen announced a reorganization of its financial services companies. A new financial holding company (Volkswagen Financial Services AG) will be established for all European (including UK) financial services activities. Volkswagen Bank will be integrated and consolidated within this holding. A new overseas holding company (Volkswagen Financial Services Overseas AG) will become the holding company of all non-European financial services activities. The changes will take until 2024 to be fully implemented. In my view this makes sense. The current structure is too complicated.

Volkswagen Bank

Volkswagen Bank GmbH is the only part of the Financial Services Division with a full banking license. It is also the weakest part from a profitability point of view. I hope that the planned reorganization will change this.

The bank makes full use of its banking license and, besides automotive financing, also offers a wide range of retail banking services, including branches and ATMs in Germany. It has less than 1mn direct banking customers, and I doubt that this business makes much sense as it must be subscale. Anyway, in the bigger picture it does not matter much.

The bank has a CET1 capital ratio of 16.9%, compared to an ECB requirement of 12.5%. Total equity is 10.9bn and assets are 61.2bn. If you do the math, risk weighted assets are not much lower than total assets. I guess you can call this well capitalized. Sitting on its capital buffer, the bank achieved a RoE of a meager 6.9% in 2022. The cost income ratio was 51.1%. For a specialty bank this seems quite high to me. I think they should try to do better.

As a way of comparison, my favorite bank in the DACH (Germany, Austria, Switzerland) region is BAWAG Group (I explain this in my article BAWAG Group: An Undervalued, Highly Profitable Retail Bank With A Low-Risk Profile ). BAWAG also has an auto financing business, although much smaller than Volkswagen. BAWAG had a RoE of 18.6% and a C/I ratio of 35.9% in 2022.(To be fair – Volkswagen Bank still beats Commerzbank, the second largest publicly listed bank in Germany, on profitability, and would also beat Deutsche Bank, the largest German bank, if it was not for a one-time 1.4bn tax credit in 2022. Commerzbank’s RoE for 2022 was 4.9% and Deutsche Bank was at 8.4% .

On the bright side – the underwhelming results of Volkswagen Bank make the whole Volkswagen Financial Services division look even better.

The most interesting part of Volkswagen Bank, in my view, are the customer deposits, as they provide access to low-cost financing. At the end of 2022 deposits stood at 26.2bn. Interestingly the bank says in its 2022 annual report that it had excess liquidity. The planned reorganization should make this hopefully available to the group.

NEW AUTO and MOBILITY2030 strategies

The NEW AUTO strategy lays out the overall Volkswagen Group roadmap for the transformation to a software-oriented mobility provider. The creation of mobility solutions is a key element here, and this is where Volkswagen Financial Services come into play beyond their more traditional role as a financial services provider.

Volkswagen Financial Services have laid this out in their MOBILITY2030 strategy:

The core task of Volkswagen Financial Services is to develop and offer an overarching mobility platform in close cooperation with the brands of the Volkswagen Group. This will give customers fast, digital and flexible access to mobility - from car sharing and car subscriptions to leasing. We are thus expanding our existing business model from a pure automotive financial services provider to a mobility provider. The focus is increasingly on vehicle-on-demand offerings. This applies in particular to Europe and North America. However, we will also focus on growth in China, South America and other international markets.

Ambitions are grand, like becoming the largest platform for used cars in Europe. But I think this is still vague and needs more elaboration and especially execution. While interesting first applications are already being tested, one of them in Vienna, the whole thing seems still far away from a comprehensive mobility platform. Volkswagen (together with partners) has acquired Europcar last year and the car rental company certainly will come into play here. But at least I cannot see what an integrated offering will actually look like. I am also not sure whether a Financial Services organization is the right place to execute what is at its core a technology program.

Conclusion

Just looking at two facts, the profitability of the Financial Services Division and the high penetration rate, makes it clear in my view that the Financial Services division is a valuable asset for Volkswagen Group. But should you buy Volkswagen shares because of it? Probably not, I would say. There are other reasons for that.

Like other Seeking Alpha contributors, I think Volkswagen is undervalued and a Buy. I have already written one article beginning of this year about the software strategy of the car manufacturer with a Buy recommendation, which I repeat here.

I have had a long position (which I have gradually built up) in Volkswagen preferred shares for a year now and I am only barely positive because of the dividend. While I am still bullish about the company’s prospects, I also need to point out that the Volkswagen has a complex structure which causes the market to discount the stock. Because of the size of the company, a trigger for a positive share price development cannot be small. Even the Porsche IPO last year did not do it. Ironically, Porsche AG ( OTCPK:DRPRY ) ( OTCPK:DRPRF ) is now the most valuable car manufacturer in Europe, surpassing its own parent company whose share price has gone nowhere.

For further details see:

Is Volkswagen Financial Services An Asset Or A Liability For The Auto Maker?