ISD - ISD: Diversified Junk Bond Fund But Distribution Does Not Appear Sustainable

2023-11-16 18:01:33 ET

Summary

- The PGIM High Yield Bond Fund, Inc. seeks to provide a high current income by investing in junk bonds with a yield of 10.81%.

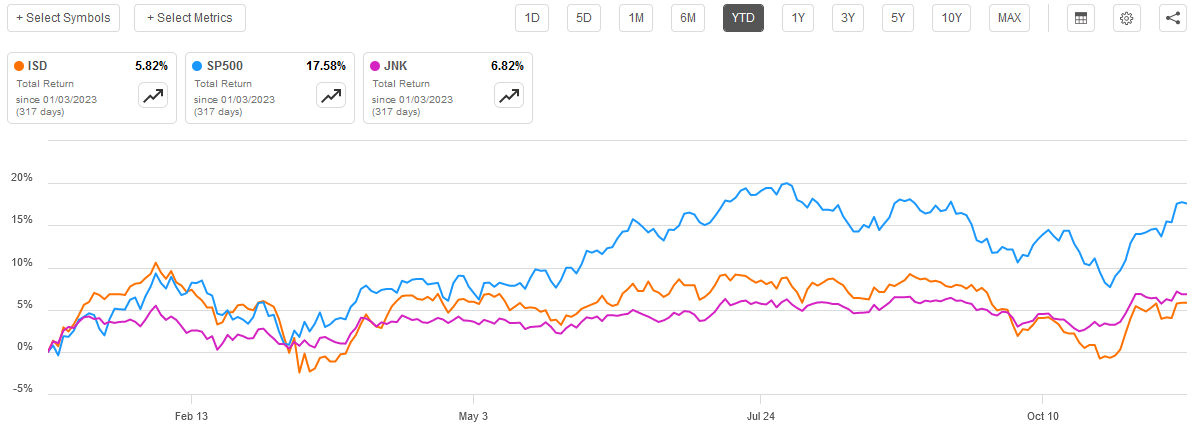

- The ISD closed-end fund's total return of 5.82% this year is lower than the Bloomberg High Yield Very Liquid Index and the S&P 500 Index.

- The fund does not completely ignore investment-grade securities, although it is mostly in high-quality junk debt.

- The fund has failed to have sufficient NII plus realized gains to cover its distributions for the past two years, and its net asset value is declining.

- The fund is trading at a discount, which seems to be pricing in a possible distribution cut.

The PGIM High Yield Bond Fund, Inc. ( ISD ) is a closed-end fund, or CEF, that is designed to provide its investors with an incredibly high level of current income. As the name suggests, the fund seeks to accomplish this by investing primarily in junk bonds and similar assets, which have remarkably high yields in the current market environment. In fact, the Bloomberg High Yield Very Liquid Index ( JNK ) has an average yield-to-maturity of 8.75% right now. This is, admittedly, not nearly as high as the index had earlier this year but it is still likely to be very attractive considering how used to low interest rates most of us have become over the past twenty years. The PGIM High Yield Bond Fund has a similarly high yield, as the fund yields 10.81% at the current price.

The PGIM High Yield Bond Fund has delivered a reasonable return so far this year, but it is certainly not as impressive as some investors would like. On a total return basis, the fund has delivered 5.82% since the start of the year. This is worse than the Bloomberg High Yield Very Liquid Index or the S&P 500 Index ( SP500 ) over the same period:

{kind=link}

With that said though, the fund’s shares have actually declined since the start of the year. The only reason that the fund’s total return has been positive is because the distributions were more than sufficient to offset the share price decline and leave money left over. That is always an important thing to consider with closed-end funds like this, as the fund pays out most to all of its investment profits to the shareholders in the form of distributions.

Junk bonds and junk bond funds have generally proven to be a pretty good place to be for the past year or so, so let us investigate and see if this fund could make sense to purchase today.

About The Fund

According to the fund’s webpage , the PGIM High Yield Bond Fund has the primary objective of providing its investors with a high level of current income. This makes a lot of sense considering that the fund seeks to achieve this objective by investing in junk bonds. After all, all bonds and other debt securities are by their very nature income vehicles. A bond is purchased at face value when it is first issued, and the owner of it receives face value back when the security is redeemed. As such, there are no net capital gains over the bond’s lifetime due to the simple fact that debt securities have no inherent link with the growth and prosperity of the issuing company.

As everyone reading this is no doubt well aware, bond funds have generally struggled over the past two years. This is mostly because bond prices are very sensitive to changes in interest rates. This is a very interesting situation considering that anyone who holds a bond for the security’s entire lifetime is guaranteed to make money as long as the issuer does not default. However, bond prices in the secondary market are determined by interest rates, and the performance of bond funds is set by the secondary market. As a result, when interest rates started rising last year, bond funds got clobbered.

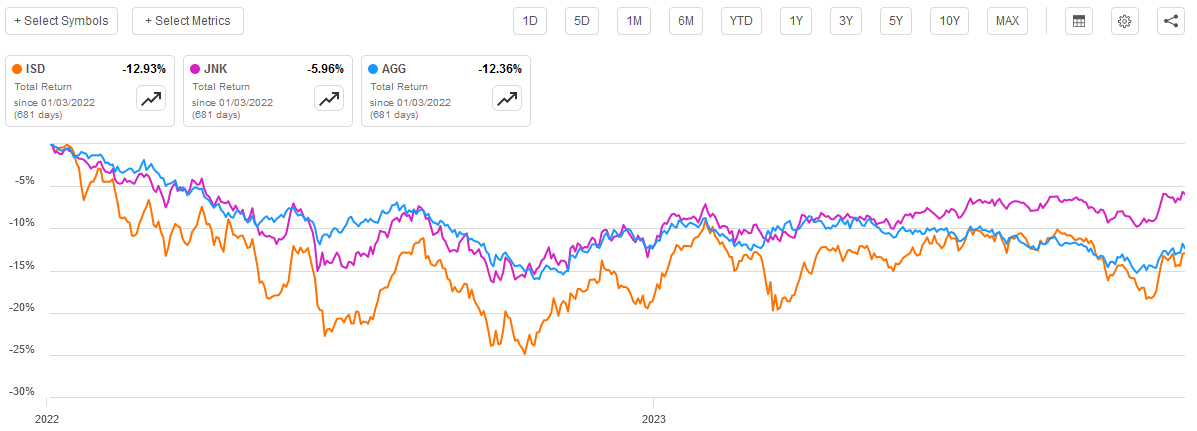

This chart shows the total return of the Bloomberg U.S. Aggregate Bond Index ( AGG ), the Bloomberg High Yield Very Liquid Index, and the PGIM High Yield Bond Fund since the start of 2022:

{kind=link}

As we can see, junk bonds in general held up much better than the aggregate bond index. This makes sense because junk bonds typically have a much shorter duration than most bonds. We can see that here:

| Index |

| Effective Duration |

| Bloomberg U.S. Aggregate Bond Index |

| 6.00 Yrs. |

| Bloomberg High Yield Very Liquid Index |

| 3.49 Yrs. |

As duration is a measure of interest rate sensitivity, we would expect that assets with a lower duration would hold up much better when interest rates start to rise. This is certainly what we see here.

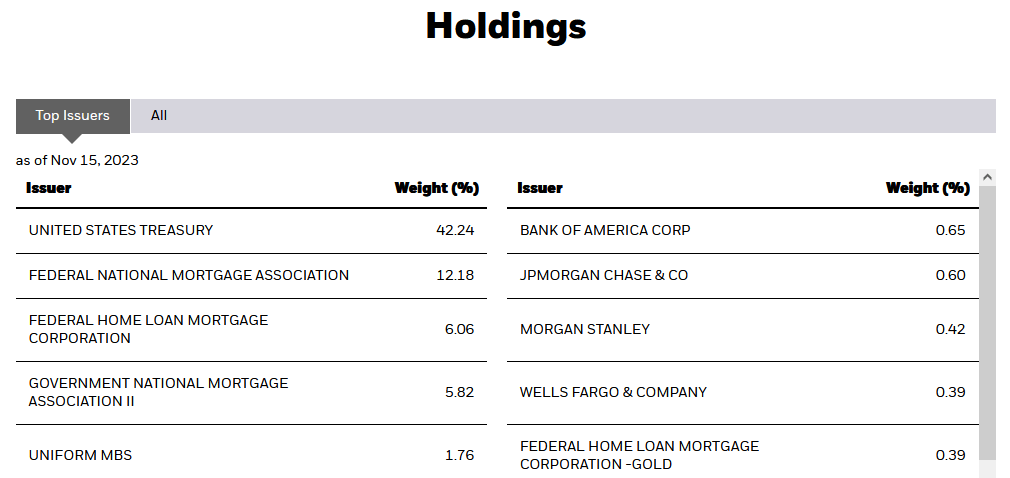

The PGIM High Yield Bond Fund is an interesting outlier though, as its performance is much closer to that of the Bloomberg U.S. Aggregate Bond Index than it is to the junk bond index. This may be partly a matter of duration, as the PGIM fund has an average duration of 4.8 years, which is higher than the junk bond index. However, it is also lower than the aggregate bond index, so we would normally expect that this fund would outperform the aggregate bond index. One possible reason for this discrepancy could be this fund’s use of leverage, which tends to amplify downside movements. It is also possible that a few occasions in which investors bid up the price of U.S. Treasuries in a flight to safety benefited the aggregate bond index, which has a 42.24% weighting to U.S. Treasury securities:

{kind=link}

As might be expected from the previous statement, the PGIM High Yield Bond Fund does not significantly invest in U.S. Treasury securities. After all, while there are certainly some people on the fringes of the markets who think that U.S. Treasuries should be junk-rated instruments, they are for the time being still investment-grade securities that are considered to be the safest instruments in the world.

The fund does still have a higher allocation to investment-grade securities than might be expected from a junk bond fund, though. We can see this here:

PGIM

We can see that 6.9% of the fund’s assets are invested in AAA-rated securities, along with a 3.7% allocation to cash equivalents that are basically risk-free. Thus, we have 10.6% of the fund’s assets invested in things that have negligible default risk. This fund takes things a step further though. An investment-grade security is anything rated BBB or better, which accounts for fully 17.3% of the fund’s total assets. That is, undoubtedly, a bit higher than we expect to find in most junk bond funds.

Nevertheless, the fact that this fund does have a noticeable allocation to investment-grade securities could appeal to those investors who are concerned about the preservation of capital and have become somewhat jittery in the volatile market that we have seen over the past eleven months. It seems as though the market is either up or lot or down a lot in rapid succession, so it would be an understandable reaction to just go to cash. Investment-grade securities are generally considered reasonably safe from default, and so some might see them as a safe place to hide out for a while. Of course, there is still interest rate risk to worry about.

Naturally, though, less than 20% of the portfolio is invested in investment-grade debt, which means that the majority of the fund’s assets are invested in various forms of junk debt. We can see that quite clearly in the table above. This is something that could be very concerning to anyone who wants to ensure the safety of their investment principal. After all, we have all heard about the risks of losing money when a junk bond issuer defaults. Moody's Investor Service warns that this risk may have gotten worse in the current market environment. According to Business Insider :

Non-investment grade US companies face growing refinancing and default risks with interest rates expected to stay high and financial conditions for borrowers tightening, according to Moody's Investor Service.

The ratings agency says about $1.87 trillion of junk-rated debt is maturing between 2024 and 2028. That signifies a 27% jump from the $1.47 trillion recorded in last year’s study for 2023-2027.

Debt maturing in the next two years accounts for about 18% of the five-year total, Moody's said, though the absolute amount for those two years has surged 25% compared to last year’s study, to hit $333 billion.

Moody’s analysts expect the US speculative-grade default rate to peak at 5.6% in January 2024 before easing to 4.6% by August 2024.

Moody’s concern appears to be that many junk-rated companies will not be able to afford the higher interest rates on their debts after they mature. This runs counter to the market right now, which seemingly expects rates to drop substantially over the course of 2024 alone, let alone by 2027 and 2028. As I pointed out in a recent article , the market is expecting about 100 basis points of rate cuts by the end of 2024. That should mean that rates will be much lower than 4% by 2027 or 2028.

U.S. Treasury Security Janet Yellen appears to agree with this statement, as back in October she predicted that interest rates would average 1% or lower for the remainder of this decade. Moody's does not appear to concur, as there would be no reason to worry about the majority of this junk debt if rates are that low on average over the coming years.

Personally, I find it far more likely that rates are going to be considerably higher than the market is predicting over the remainder of the decade. I have explained the reasoning behind this is a few previous articles. As such, we may want to be cautious about the potential risk of default-related losses across the fund’s portfolio. Fortunately, the PGIM High Yield Bond Fund is taking precautions to protect itself and its investors against any significant losses due to this cause. First, please notice above how 68.40% of the fund’s assets are invested in BB or B-rated securities. These are the two highest possible ratings for junk bonds. According to the official bond rating scale , companies whose securities are issued with one of these two ratings have sufficient financial strength to carry their debt even through a short-term economic shock. These companies should be able to avoid defaulting even if the economy enters into a recession next year. As such, we can probably be reasonably comfortable with holding these securities in our portfolios. When we consider the fund’s investment-grade rated securities, we see that 85.7% of the fund’s assets should be reasonably safe from default losses. Granted, that is not as good as a money market fund or something similar, but it should be fine for a bond fund with 635 issuers represented in its portfolio.

With so many issuers, we can almost certainly conclude that the fund will not have particularly large exposure to any single issuer. This is certainly the case, which we can see by looking at the largest positions in the fund. Here they are:

PGIM

As we can see, the PGIM High Yield Bond Fund’s largest position only accounts for 2.0% of its assets. That is not a large enough position to have any real impact on the fund. After all, with where the yields on junk bonds are, even a default of that size will be erased by interest payments from the remaining bonds after a few months.

As such, we should not need to really worry too much about losing money to defaults here. The biggest risk is undoubtedly interest rates, and it is very difficult to predict where those will be going over the next year, let alone the next five years.

Leverage

As is usually the case with closed-end funds, the PGIM High Yield Bond Fund employs leverage as a method of boosting the effective yield of its portfolio. I explained how this works in numerous previous articles on such funds. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase high-yield debt and similar assets. As long as the interest rate that the fund receives on the purchased assets is lower than the yield that the fund receives on the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. As the PGIM High Yield Bond Fund is capable of borrowing money at institutional rates, which are considerably higher than retail rates, this will usually be the case.

It is important to note though that leverage is not as effective at boosting the overall yield of the portfolio as it was two years ago. This is because today’s higher interest rates reduce the difference between the rate that the fund pays on the borrowed money and the yield that it can receive on the purchased securities.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As we saw earlier, this fund is much more volatile than the two major bond indices, which might be explained by the leverage that it employs. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see any fund have leverage of more than a third relative to its total assets for that reason.

As of the time of writing, the PGIM High Yield Bond Fund has leveraged assets comprising 22.85% of its portfolio. This is a pretty low leverage ratio for a bond fund, as many of the ones that we see from other fund houses have leverage ratios of anywhere from 30% to 40%. The fact that this one is lower than that is something that risk-averse investors should appreciate as it indicates that the fund’s net asset value should be less volatile than some of its peers.

Distributions

As mentioned earlier in this article, the primary objective of the PGIM High Yield Bond Fund is to provide its investors with a very high level of current income. In order to accomplish this objective, the fund invests in a portfolio that consists of high-yield bonds and similar assets. These bonds tend to have very high yields in the current market, and the fund boosts this by using leverage to control more bonds than it otherwise could with only its net assets. The fund then distributes all of the money that it receives from the bonds in the fund to its shareholders, net of the fund’s own expenses.

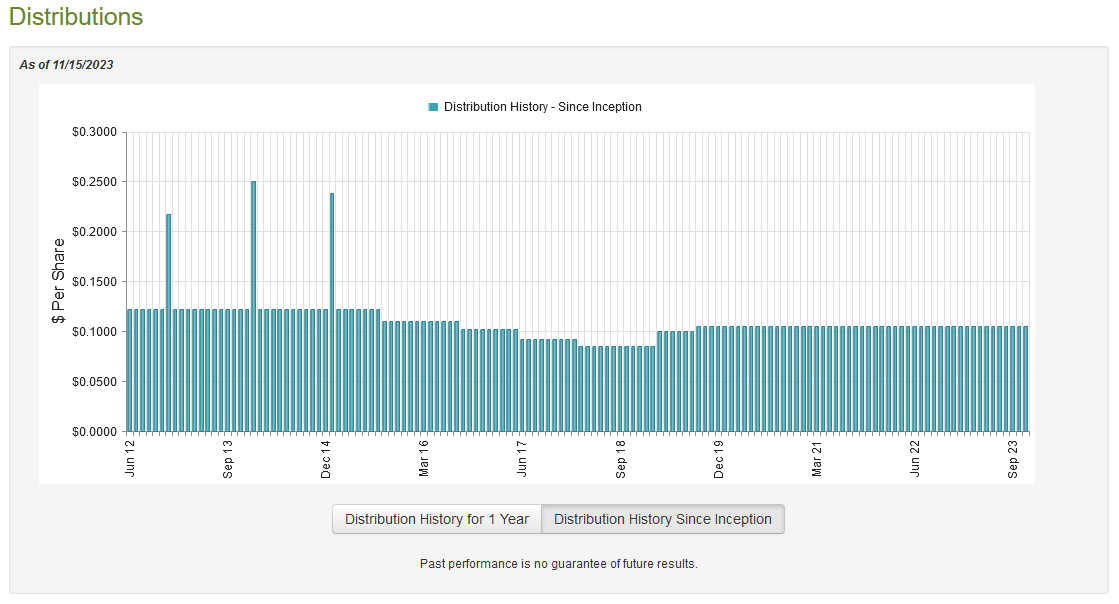

As the assets of the fund have very high yields, we might expect that the fund’s shares will also have a very high yield. That is indeed the case, as the PGIM High Yield Bond Fund pays a monthly distribution of $0.1050 per share ($1.26 per share annually), which gives the fund a 10.81% yield at the current price. While this fund has not been perfectly consistent with respect to its distribution over the years, it has done better than most fixed-income funds recently:

{kind=link}

The majority of fixed-income funds trading in the market today have had to reduce their distributions due to realized and unrealized losses that started piling up in 2022 after the Federal Reserve embarked on its current interest rate hiking program. The fact that this one did not see the need to do this yet is something that we should investigate, as it could be a sign that the fund is paying out more money than is prudent. However, junk bonds have generally held up better than investment-grade bonds in the current environment so that could also be working in the fund’s favor.

Fortunately, we do have a somewhat recent report that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on July 31, 2023. This is a pretty good period to analyze because it basically gives us the best of both worlds. During the latter half of 2022, the bond market in general was still reeling from the Federal Reserve’s shift to a monetary tightening policy and was suffering widespread sell-offs. This naturally hurt bond prices. Things changed during the first half of this year though as investors began to expect that the Federal Reserve would quickly begin cutting rates, so they bid up bond prices in the hopes of locking in high rates of return while they were still available. While the market’s optimism has generally been unfounded, the fund may have still had the opportunity to earn some capital gains by trading bonds as their prices rose.

During the full-year period, the PGIM High Yield Bond Fund received $40,310,837 in interest along with $995,820 in dividends from the assets in its portfolio. This gives the fund a total investment income of $41,306,657 during the period. The fund paid its expenses out of this amount, which left it with $30,104,649 available for shareholders. Unfortunately, this was not nearly enough to cover the $41,903,472 that the fund actually paid out in distributions during the period. At first glance, this is certainly going to be concerning we would normally like a fixed-income fund to be able to fully fund its distributions out of net investment income. This one is failing to do so.

With that said, there are other methods through which a fund can obtain the money that it needs to cover its distributions. For example, it might have been able to take advantage of periods of market strength and sell bonds for capital gains. As has been the case with most other bond funds that actually have a similar fiscal year to that of this fund, the PGIM High Yield Bond Fund failed in this task. The fund reported net realized losses of $2,196,710 along with another $7,902,488 net unrealized losses. Overall, the fund’s net assets declined by $21,898,021 after accounting for all inflows and outflows during the period. As such, it certainly appears that this fund failed to cover its distribution during the full-year period.

This is the second year in a row for which that has been the case. During the previous year, the PGIM High Yield Bond Fund saw its net assets decline by $92,314,722 after accounting for all inflows and outflows. The fund’s net investment income and net realized gains during that year were not sufficient to cover its distribution either. Thus, it appears that this fund has now failed to cover its distribution for two straight years. It is difficult to see how it can maintain it going forward. Investors may want to prepare for a cut, as the distributions right now are depleting the fund’s net asset value.

Valuation

As of November 15, 2023 (the most recent date for which data is currently available), the PGIM High Yield Bond Fund has a net asset value of $13.20 per share but the shares only trade for $11.72 each. This gives the fund’s shares an 11.21% discount on net asset value at the current price. This is not as good as the 13.16% discount that the shares have had on average over the last month, so it might be possible to wait and get a better entry price. However, generally speaking, a double-digit discount is a reasonable price to pay for any fund so buying today is not necessarily a bad decision if you want to own this fund.

Conclusion

In conclusion, the PGIM High Yield Bond Fund is a well-diversified bond fund that appears to be doing a reasonable job of protecting itself from the risk of default-related losses. The fund does still have interest-rate risk, but its assets are lower duration than the bond market as a whole so it should have lower risks than a typical bond fund. Unfortunately, though, it appears that the distribution may not be sustainable, as the fund has now failed to cover it for two years straight.

For further details see:

ISD: Diversified Junk Bond Fund, But Distribution Does Not Appear Sustainable