ILF - iShares Latin America 40 ETF: Slow Growth And Double-Digit Dividend Yield

2023-05-31 06:58:31 ET

Summary

- The growth trigger remains the recovery of the U.S. and Chinese economies as major trading partners.

- Most of the fund's companies are from cyclical or slow-growth sectors (materials, energy, financials).

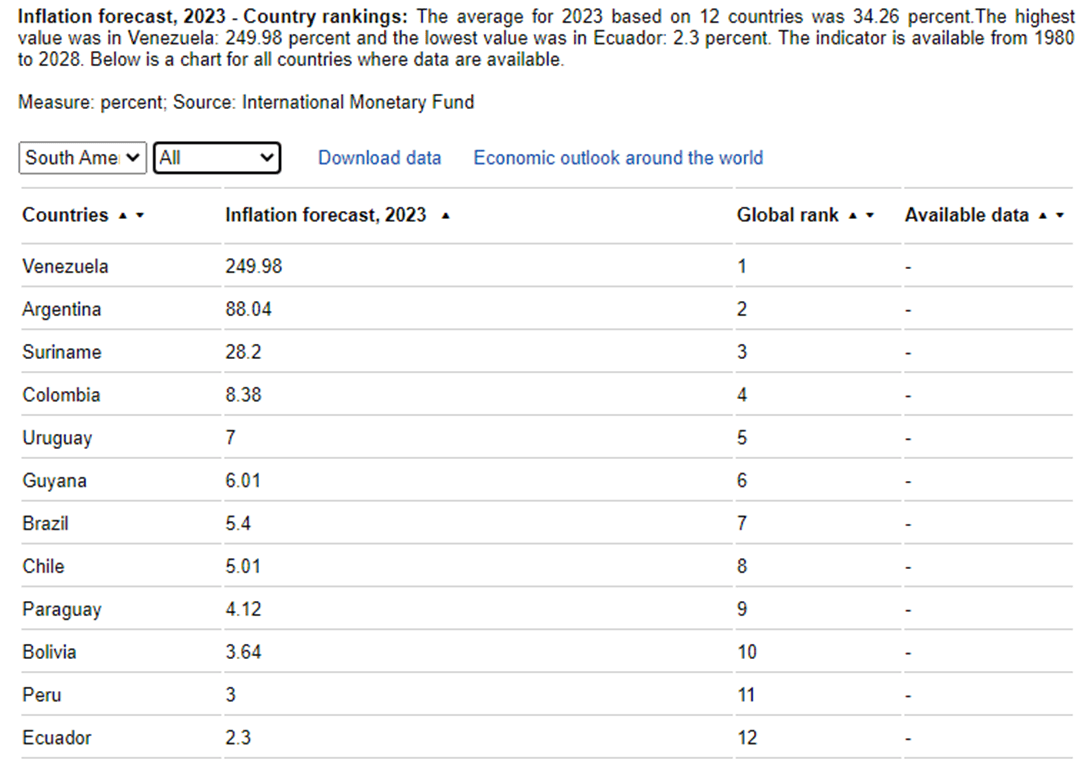

- Regulatory risks are also present. The continent's growth forecast for 2023 is 0.6%.

Introduction

2023-2024 could be a period of recovery for emerging markets. South America is no exception, with the commodity sectors accounting for about 40% of iShares Latin America 40 ETF (ILF) assets. Overall, the continent-wide growth forecast for 2023 is low at 0.6%, as it will remain under the influence of low growth in economic activity and global trade this year. In addition, rising interest rates around the world are exacerbated by the financial turmoil seen in early March. Regional inflation remains high relative to pre-pandemic levels, with the continent's average forecast for the year at 34%. True, most of the inflation is in countries not represented in the ETF. If we look at Brazil and Mexico, which together take up 83% of the index, we get about 5.5-6%, which is not critical for emerging markets. All the fund's profit for investors is formed mainly due to dividend payments. Here we should take into account the fact that they are tied to the net profit of companies. That is, if in U.S. stocks the ETF price falls (usually caused by a decline in corporate profits), and the dive yield rises, then in the case of ILF - the dive yield will not rise, and probably will decline altogether when the prices fall. The ETF itself is virtually flat, with a long sideways trend going on since 2007.

{kind=link}

General information and Market overview

Launched on October 25, 2001, it follows the S&P Latin America 40 Index, which tracks the top 40 companies in South America, accounting for about 70% of the region's total market capitalization; the actual number of companies as of May 8, 2023 is 42; 98.31% of assets are invested in index securities; 1.69% are held in U.S. dollars, Brazilian real, Chilean, Mexican and Colombian pesos, as well as futures on those currencies.

iShares Latin America 40 ETF (fund data)

{kind=link}

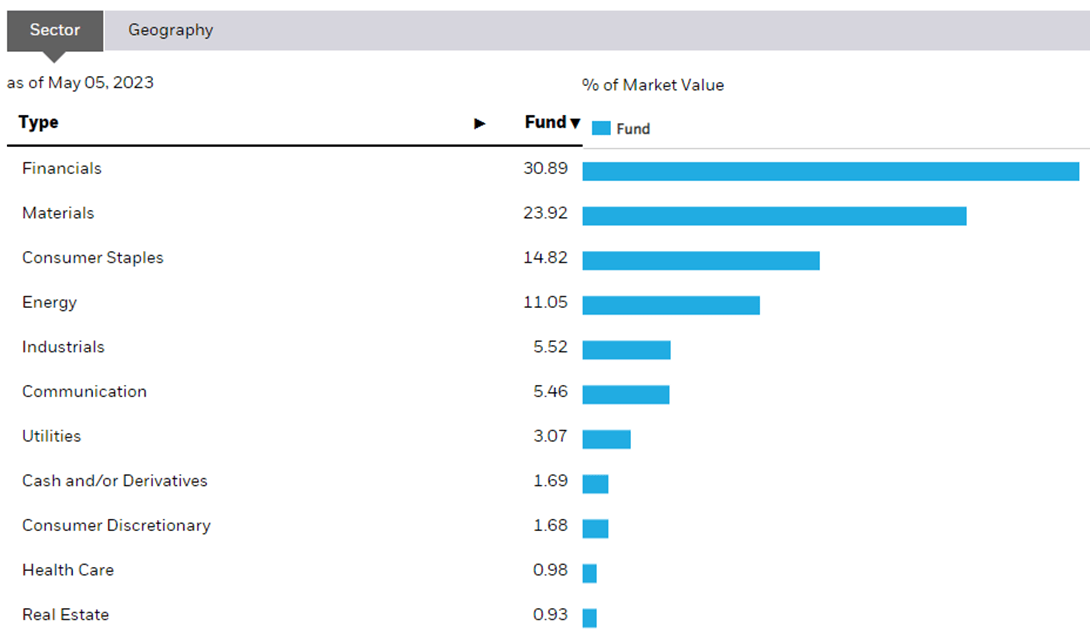

The South American economy is mainly represented by the materials, energy, financial, and consumer sectors. Since there are no statistics with revenue and profit forecasts for the South American market, the graphs below use an analogy with the sectors and industries of the U.S. market. The main focus is on the sectors:

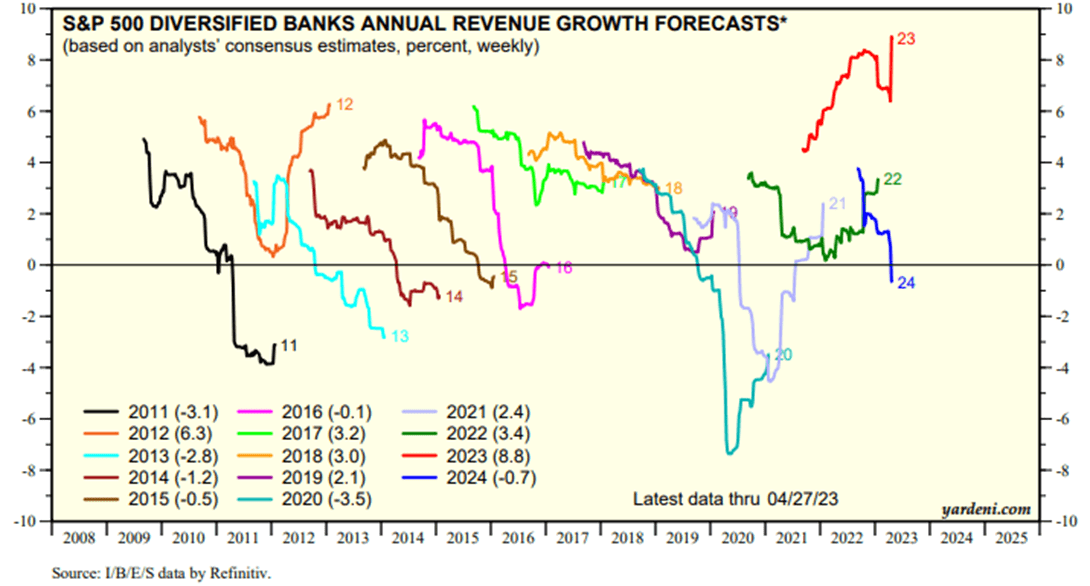

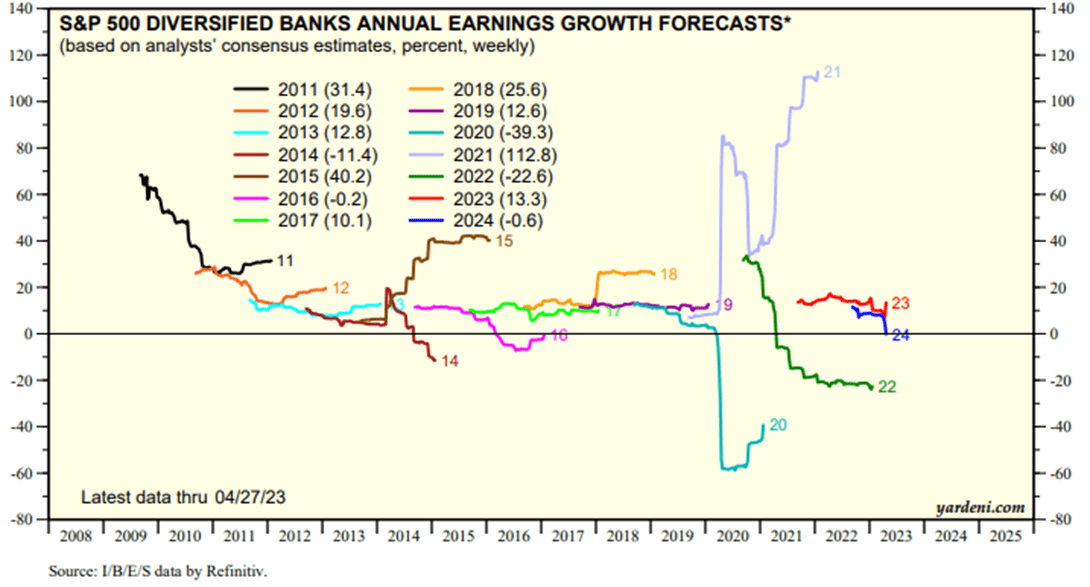

Financial, Banks. The forecast of revenue growth in 2023 is increased sharply against the background of high rates in developing countries, and in 2024, the growth rate of revenue and profits is negative, due to the likelihood of future rate cuts. Analysts suggest that the banking sector in Latin America will be resilient, despite concerns about the state of the global banking system. Capital ratios are high, profitability has recovered from the lows associated with the pandemic; liquidity is ample, and the share of non-performing loans is also under control.

revenue forecast (refinitiv) revenue forecast (refinitiv)

{kind=link}

{kind=link}

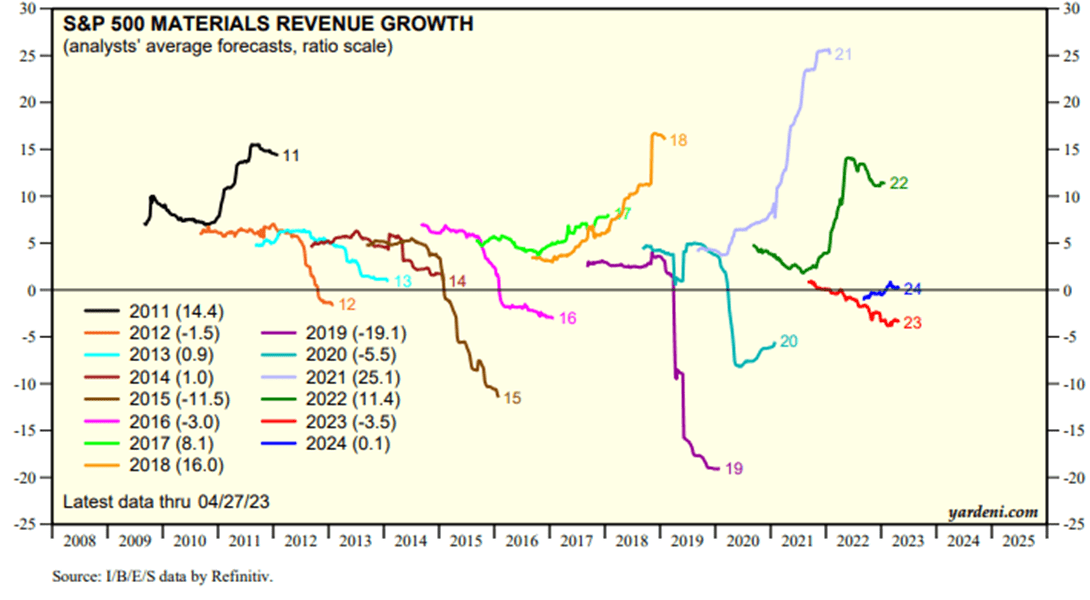

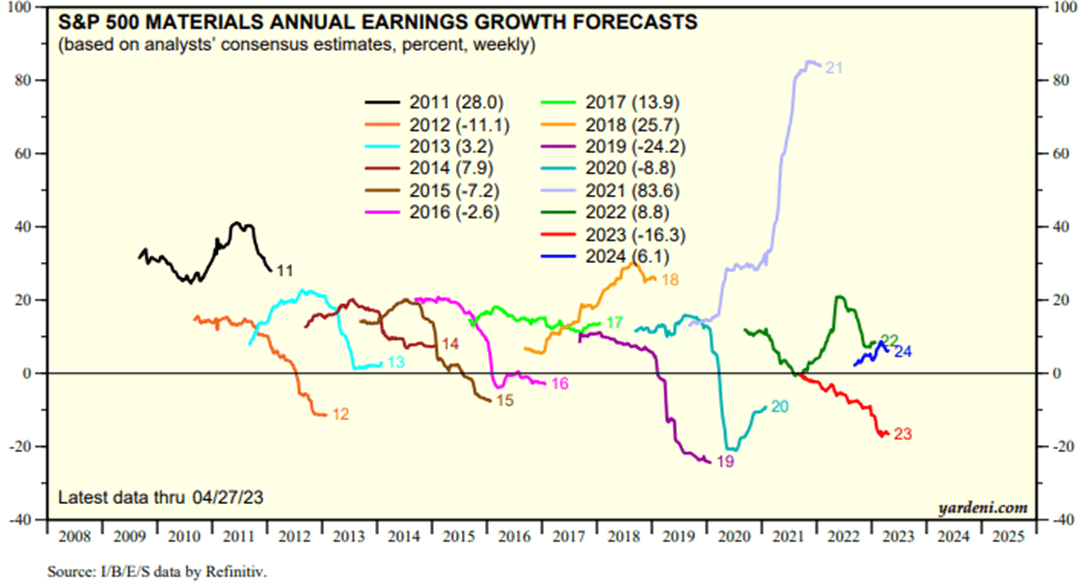

Mining, Industrial Metals and Construction Materials. Revenue and profit growth are expected to decline for 2023, due to a drop in demand in a difficult macroeconomic environment, a high base in 2022, and rising production costs. For 2024, the outlook is better, the exit from the expected recession and continued economic recovery will return the sector to positive revenue growth, and demand for materials will positively affect the profit forecast.

revenue forecast (refinitiv) revenue forecast (refinitiv)

{kind=link}

{kind=link}

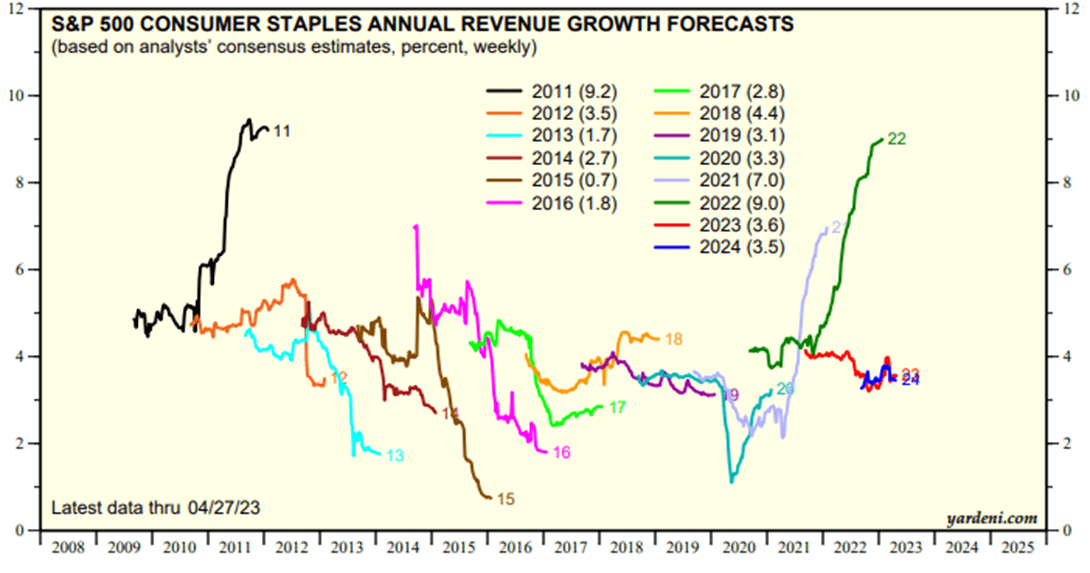

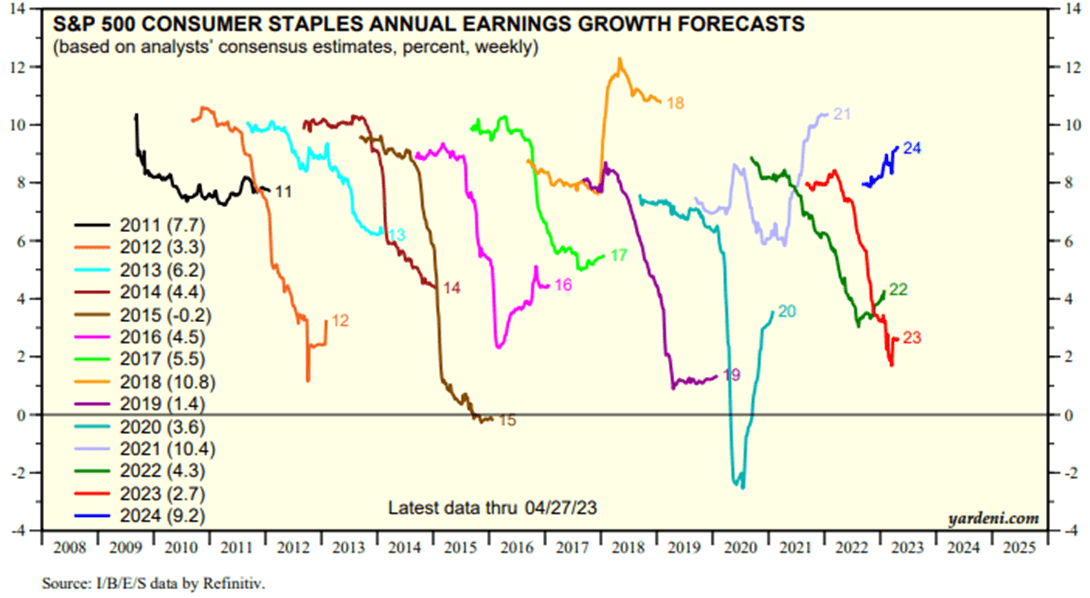

Consumer, manufacturers and retailers of food and everyday goods, clothing. For 2023 and 2024, revenue growth rates will remain at 10-year averages. The earnings growth forecast for 2023 is also weak; for 2024 it is much more optimistic, due to the recovery of logistics chains and lower transportation costs.

revenue forecast (refinitiv) revenue forecast (refinitiv)

{kind=link}

{kind=link}

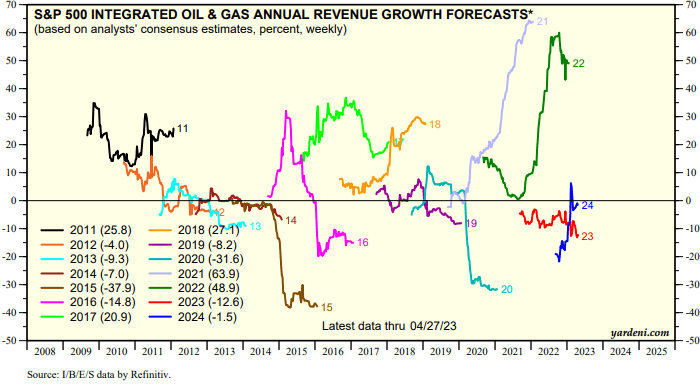

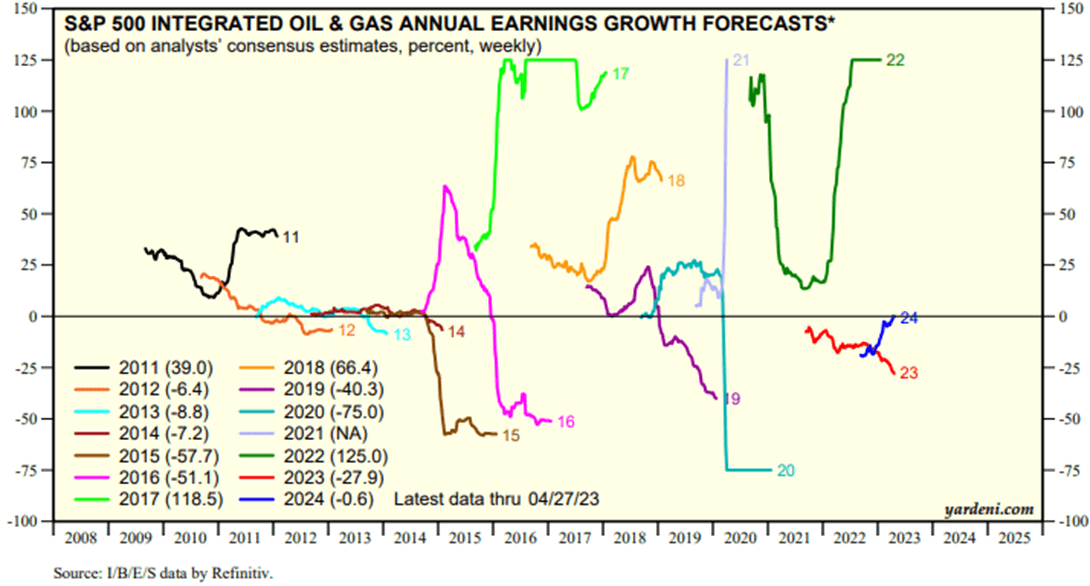

Energy, oil and gas production. The outlook for 2023 and 2024 earnings and revenue growth is negative due to the continued tightening of the ACP, hampering the economy and demand for hydrocarbons. There is also a very high base in 2022.

revenue forecast (refinitiv) revenue forecast (refinitiv)

{kind=link}

{kind=link}

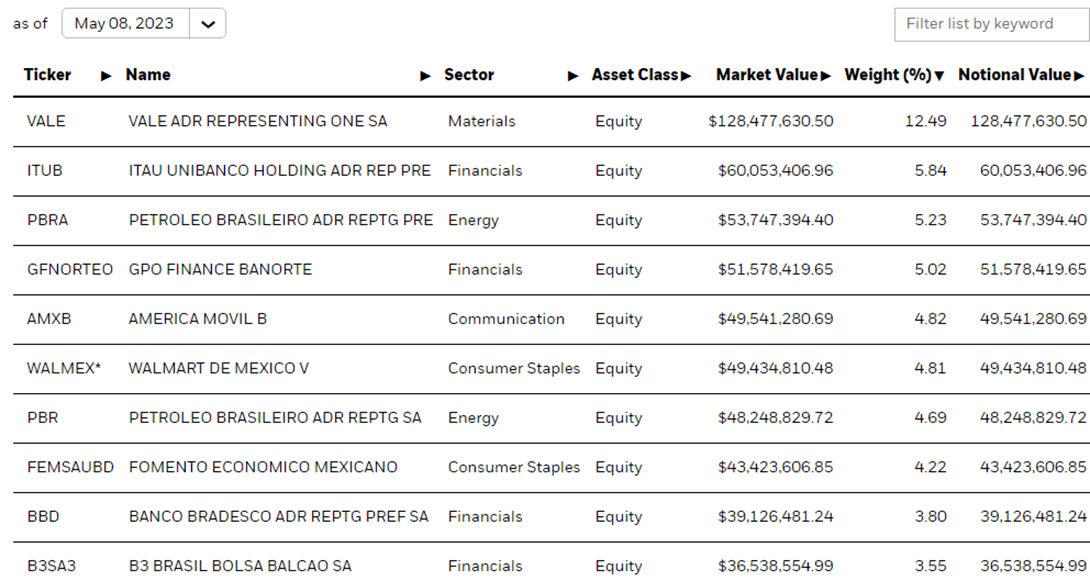

Top 10 holdings

Vale ( VALE ) is a Brazilian miner and producer of nickel, copper, aluminum and iron ore. FWD P/E: 4.7x (-65% to the industry average);

Itau Unibanco ( ITUB ) is Brazil's largest private bank. FWD P/E: 7.3x (-13% to industry average);

Petróleo Brasileiro (PBR.A, [[PBR]]) is a Brazilian oil and gas production, sales and refining company. FWD P/E PBRA: 2.9x (-66% to industry average), FWD P/E PBR: 3.6x (-57% to industry average); Prefs traditionally priced at a discount to common stock.

Grupo Financiero Banorte (GFNORTEO) (GBOOY) (GBOOF) is Mexico's third-largest bank by loans and deposits. FWD P/E: 8.4x (in line with the industry average);

America Movil (AMXB) (AMX) is a Mexican telecom that provides communications, data processing, Internet access, and mobile payment solutions; the 7th largest cellular operator in the world by subscribers. FWD P/E: 13x (-12% vs. industry average);

Walmart De Mexico (WALMEX) - Central American subsidiary of the consumer goods wholesale and retail chain. FWD P/E: 23.5x (+21% over industry average);

Fomento Economico Mexicano (FEMSAUBD) (FMX) is a manufacturer and distributor of Coca-Cola beverages, fuel retailer, automotive accessories, and food processing equipment in Central and South America. The company is loss-making, P/S: 0.9x (-23% to the industry average);

Banco Bradesco ( BBD ) is a Brazilian bank and insurer, 3rd largest in the country. FWD P/E: 8.3x (-1% to industry average);

B3 Brasil Bolsa Balcao (B3SA3) (BOLSY) (BOLSF) is a Brazilian stock exchange. FWD P/E: 16.3x (+94% to industry average).

funn main holdings (fund data)

{kind=link}

Potential Risks

Regulatory risks are also present. For example, in March the Brazilian government announced, without consultation with the industry, that it would collect taxes on crude oil exports for four months to offset the effects of an earlier decision to exempt fuel taxes, and Chile announced a long-term plan to nationalize lithium assets. Also, Brazil, which is home to 55% of ETF assets, is one of the leaders in the depth of regulatory and economic intervention by the authorities in business.

Even though local banks are mostly funded by retail deposits, they continue to suffer from weak capital market activity because deposits are more interesting to private investors when interest rates are high. In addition, a weak economy reduces disposable income of consumers, which will put even more pressure on the quality of bank assets. And the banking sector is a core sector for the Latin American ETF.

Valuation and triggers for growth

P/E ILF IS 4.98x. This is even lower than the Russian market(!). P/E MSCI EM - 12.4x, that is, the fund is undervalued relative to the majority of related indices. Recovery of economies of the USA and China as the largest trading partners remains the growth trigger. In April we talked about the growth of copper and silver prices, as well as the prospects for the lithium industry. The medium-term price outlook for lithium, related to the development of the EV industry in China, is still solid and remains close to historic highs. As you can see from the chart, the ETF is barely growing, a long sideways slide that has been going on since 2007. All profits for investors are generated mainly by dividend payments. Here we should consider the fact that they are tied to companies' net profits. That is, if in U.S. stocks the ETF price falls (usually caused by a decline in companies' profits), and the dividend yield rises, then in the case of ILFs - the dividend yield will not rise, and probably will decline altogether when the quotations fall.

Bottom line

Overall, this is a slow-growth fund focused on dividend investors. Most companies are very conservative. That's why we prefer a more dynamic option - ETFs only for the Brazilian market, there are more small and growth companies. From ILF's point of view, the best entry point is the lower end of the $22 sidewall.

For further details see:

iShares Latin America 40 ETF: Slow Growth And Double-Digit Dividend Yield