PB - It's A Wonderful Life: 3 Regional Banks We're Buying

2023-03-28 07:00:00 ET

Summary

- In this article, we discuss three banks that are a great fit for today's environment.

- Each has declined due to the ongoing banking crisis.

- Yet you likely won't see these banks in the news much. That's the point.

- We want good deals on great banks, not great deals on bad ones.

- Now is not the time to go "dumpster diving" in the banking sector. More dominoes could fall.

This article was coproduced with Williams Equity Research.

Has anyone heard of George Bailey, the good-guy banker in Frank Capra’s classic Christmas film It’s a Wonderful Life ? In this clip (from It’s a Wonderful Life ), George Bailey argues for extending credit to ordinary working people.

Seventy-eight years after its release, It’s a Wonderful Life remains a holiday classic with a plot that happens to touch on some exceptionally relevant topics today, including the banking system, the ethics behind issuing loans, and the way U.S. banking affects the overall economy.

I usually watch the movie every Christmas season, as it reminds me of how important my family is to me, and that humility is the secret to success.

These days, the movie is even more relevant, especially the scene from the movie in which people are rushing to get their money out of their failing financial institution (during the Great Depression.)

Obviously, I was not around during the Great Depression, but I was during the Great Recession, and one of the things that I preach quite a bit on at Seeking Alpha is the fear of too much leverage – just like that one big loss that took down an entire bank.

Now, I’m not here today to bring doom and gloom, I’ll leave that for another day. Instead, in this article, we'll be covering three regional banks that fit a unique profile.

First, these banks are not exposed to the same risks that you've heard of with Silicon Valley Bank of SVB Financial Group (SIVB), Signature Bank ( SBNY ), or First Republic Bank ( FRC ). That's for several reasons.

Their asset base is diversified and not dependent on any one sector of the economy. They didn't receive huge amounts of deposits since 2020. And they aren't involved in crypto anything.

Lastly, their interest risk is manageable.

Second, these banks have all traded lower. That's made them more attractive than they were just a few weeks ago. You'll see, however, that these banks are not trading at distressed levels. That's because they aren't distressed.

In most cases, a company that's declined 60% or more in value in a short period of time has major tail risks. If the whole market has collapsed, that's a different story. But if it's sector-specific and only a few players are really getting hammered, it's wise to be humble. The market may know something you do not. Proceed with caution with those names.

With that, let's get into the first bank I've selected to take advantage of the current crisis without taking on too much risk.

Cullen/Frost Bankers, Inc. ( CFR )

I moved to Austin, Texas, about 20 years ago to attend UT Austin. Believe it or not, there was only one "skyscraper" in the city back then. You are looking at it.

The Frost Bank tower. Now, you can hardly see it in the Austin skyline. That's how things go. While its visual prominence may not be what it used to be, the bank's business is still in the spotlight.

Headquartered in San Antonio, Cullen/Frost is Texas centric. Despite focusing on one state, this regional powerhouse is top 50 in the U.S. by assets with $52.9 billion.

CFR 2022 Annual Report

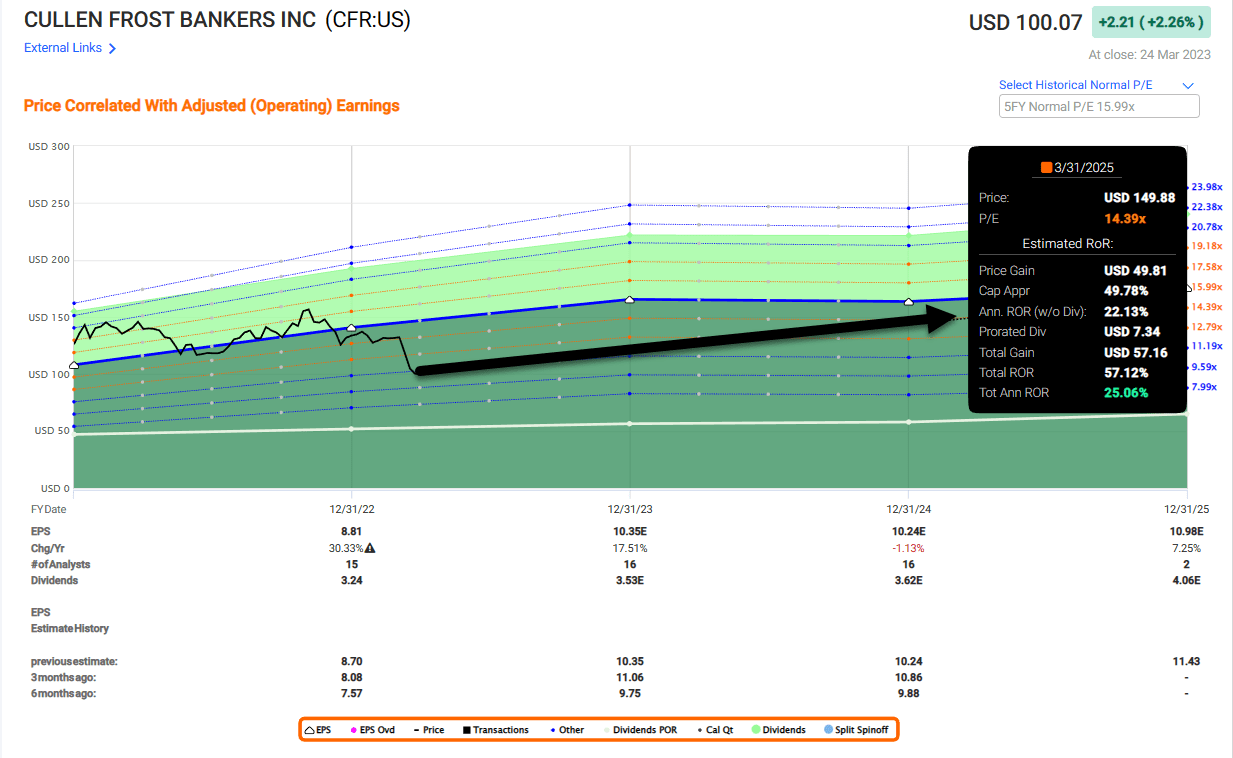

Cullen/Frost grew diluted earnings per share ("EPS") from $6.76 in 2021 to $8.81 in 2022. That's a 30.3% increase in a single year .

Notice what you don't see? Adjusted, Core, or Non-GAAP . Cullen/Frost is putting down serious growth numbers the old fashioned way.

The bank also keeps a historically conservative loan-to-value ratio. 50% or less is considered especially safe. Cullen/Frost's ratio was as low as 38% in 2021. That "extra" level of deposits relative to loans might not seem so "extra" today.

What's perhaps most impressive is Cullen/Frost has been able to increase revenue by 42% year-over-year and translate most of that into profits without taking on excessive risk like some of its peers.

Cullen/Frost has increased its dividend by 16% in the past year. That's among the best of any bank I follow. And despite a double-digit raise, its payout ratio declined (improved) over the same period.

Net interest margins also improved in 2022 versus 2021, another good sign that the business model is working. At the end of 2022, only 0.22% of the bank's loans were non-performing.

What sunk Silicon Valley Bank, among other things, was its large unrealized losses on hold-to-maturity ("HTM") assets. That's a fancy way of saying medium or long-term Treasury bonds. Silicon Valley Bank's unrealized losses were enough to theoretically wipe out its tangible equity. In Cullen/Frost's case, its unrealized losses on HTM securities are only 9% of tangible equity. It's apples-to-watermelons.

For context, First Republic Bank's ( FRC ) is 34.4%.

The issue with Cullen/Frost has never been its fundamentals. It's been price. The bank historically traded with a price-to-book value as high as 2.5x-3x and a price-to-earnings ("P/E") ratio of 14-18x.

Where does that stand today? The price-to-book value is still a little high at ~2x, but that figure moves around a lot due to accounting rules. From a P/E perspective, the bank now trades at just 9.5 times forward earnings estimates. That's a steal considering the bank's track record and balance sheet .

I first discussed this great bank with subscribers back in September 2020. Back then, I recommended shares around $60 per share. While today's $100 might seem steep, the valuation is exactly the same. That's the beauty of earnings growth per share.

I recently added to my CFR position at $100 per share with a ~3.5% dividend yield.

{kind=link}

M&T Bank Corporation ( MTB )

Just like Cullen/Frost, M&T has had a few name changes. Originally Manufacturers and Traders Bank in Buffalo, New York, it became a bank in 1969. Later in 1998 , the name was shortened to M&T Bank.

Just nine days before the collapse of Silicon Valley Bank, M&T came out with an Investor Update presentation. M&T ended Q4 2022 with $201 billion in total assets and $164 billion in deposits.

MTB Q4 Investor Presentation

M&T has consistently outperformed peer averages in "return on" metrics as well as operating EPS. M&T's dividend growth has been strong long-term (7.9% annualized over 20 years versus 1.6% peer median), but it has not kept up with peers in recent years (9.9% for M&T versus 16.2% peer median in the past five years).

One of the reasons I like MTB is its operating efficiency. Since 2013, it's consistently generated significantly greater net interest margins than its peers. That's while also generally taking less risk.

While today's banking crisis is nerve-racking, it's nothing compared to the Great Recession. Unemployment was sky-high, the assets behind bank loans were crashing in value, and half the mega banks were technically insolvent.

Even in all that chaos, MTB's net charge-offs peaked at 1.0%. The peer average was nearly 2.5% and a couple banks exceeded 4.0%. In fact, here's a statistic you probably weren't aware of: M&T Bank is one of only two S&P 500 banks to maintain its dividend during the Great Recession .

Whether commercial real estate, construction loans, HELOC, or consumer loans, M&T Bank has among the best net charge-offs in the industry.

M&T Bank's network is focused in the Northeast but covers approximately 22% of the U.S. population and 25% of U.S. GDP.

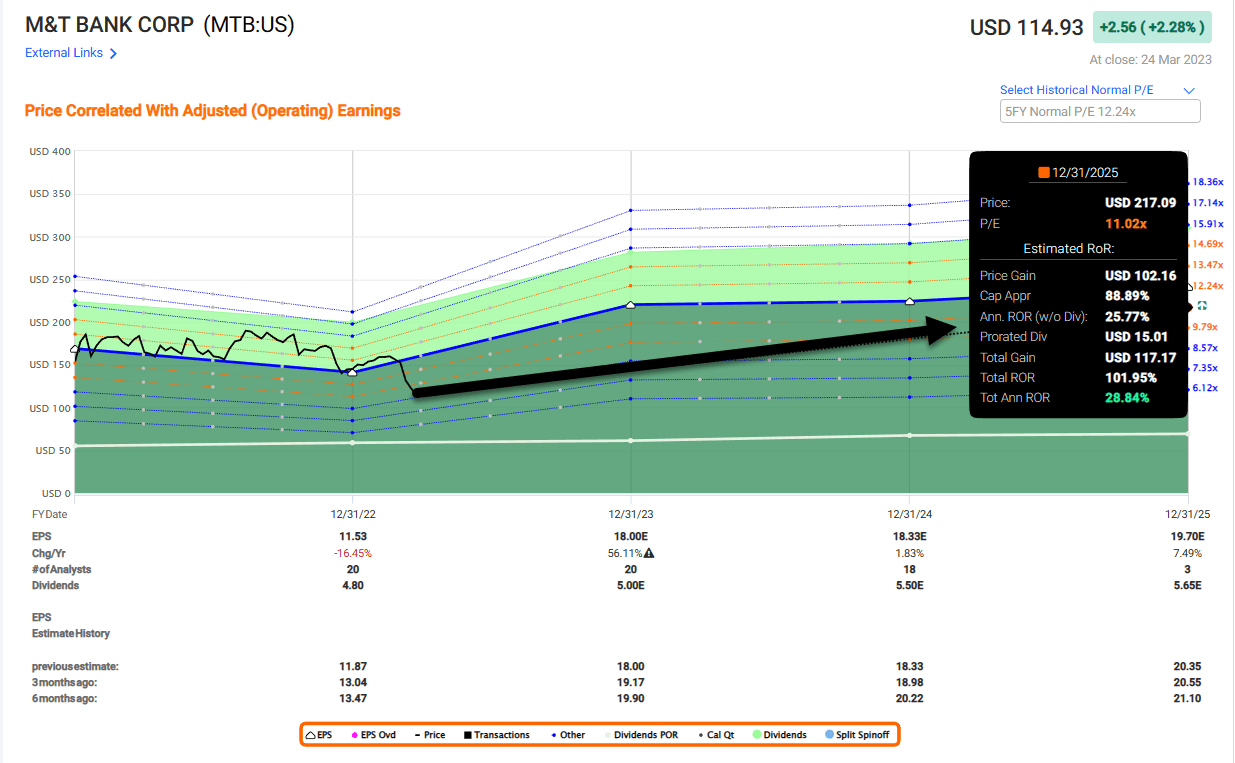

And just like Cullen/Frost, the reduction in tangible equity if we include HTM unrealized losses is 9%. M&T is clearly solid, with one of the best track records in all of banking. Let's talk valuation.

Book value for M&T is also volatile. It was between 1.6x and 2.0x for Q2 2022 and 1.05x and 1.4x in the quarters since then. Due to the recent selloff in regional banks, that ratio now sits at 0.83x. This is a 33% discount to the lower end of M&T's recent range.

From an earnings perspective, M&T typically traded at 9-12x in recent years. That stands at 6.4x today.

I started buying shares of MTB at $127 and will continue to add as the price declines. M&T recently increased its dividend by 8% and now yields over 4.5%.

{kind=link}

Prosperity Bancshares, Inc. ( PB )

We are leaving the East Coast and heading back to Texas. Prosperity is the second largest regional bank in the state and is also active in Oklahoma.

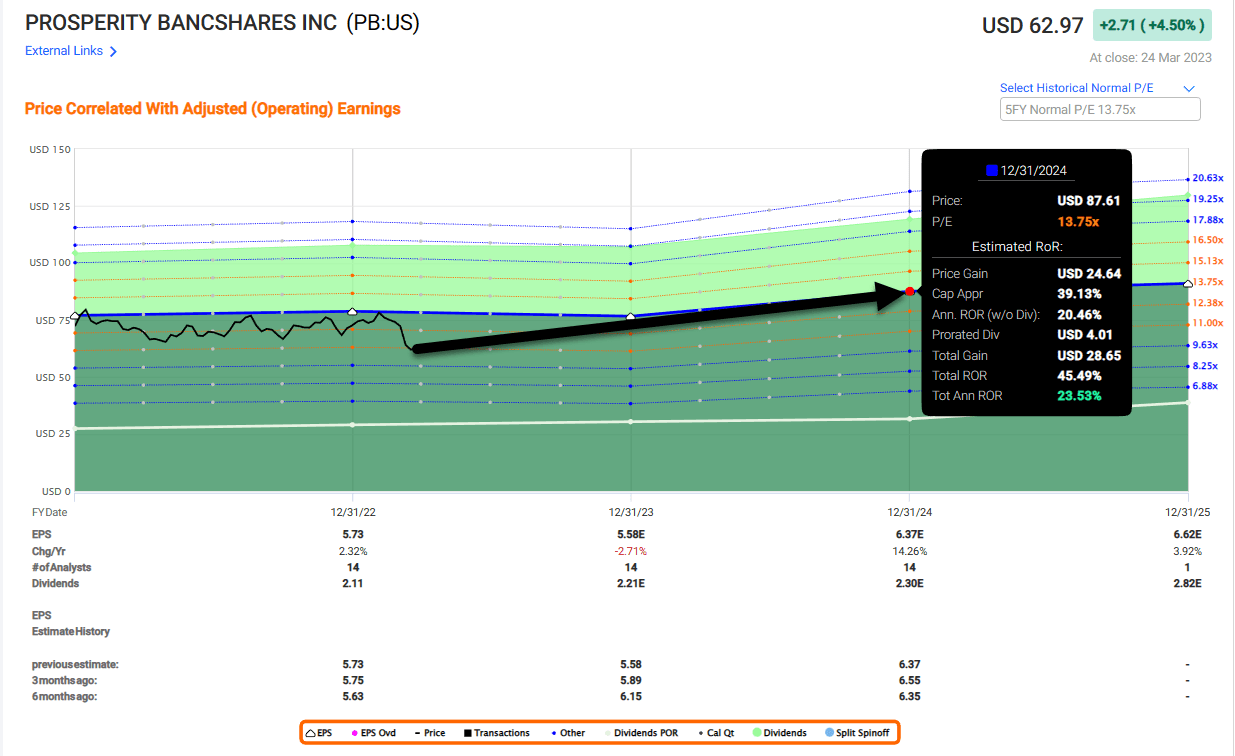

Prosperity's assets are the smallest of today's banks at $37.7 billion, but this medium-sized regional bank sports many "heavyweight" quality statistics.

Nonperforming assets to average earnings assets ended Q4 2022 at only 0.08% or $27.5 million. Annualized net charge-offs/quarterly average loans of only 0.01%. All the banks we've talked about in this article have strong CET1 ratios, and Prosperity's 15.9% CET1 ratio is no exception.

There is another category that Prosperity has punched above its weight class. Its been in included in Forbes America's Best banks since its inception in 2010. And it's been in the top 10 every time. They finished sixth out of the whole country in 2022.

PG Q4-22 Investor Presentation

Prosperity has generated 12.8% and 14.9% Core CAGR in net income in the last 10-years and 5-years, respectively. GAAP net income has increased from $167.9 million in 2012 to $524.5 million in 2022. That's the beauty of "compound" annual growth.

Prosperity has successfully translated 55-65% of net income growth into EPS growth. Net interest margins for Prosperity are back above 3% as of Q4 2022, which is the best metric in many quarters.

PG Q4-22 Investor Presentation

That's at least partly attributable to what we see above. Prosperity's total cost for its deposits is only 0.50%. It's been able to hold off on raising interest rates payable to depositors. This has helped push its margins higher.

Another interesting attribute for Prosperity's business is that 29.7% of its loans are floating rate. These borrowers are charged higher interest as soon as rates move (assuming it's up). Another 27.8% are variable rate. Fixed loans are less than half (42.5%) of the business.

We'll keep a close eye on all these banks' construction loans. In my opinion, these are the most sensitive to both the ongoing banking crisis and the higher interest rate environment in general. Prosperity has $2.8 billion of these loans with single-family the largest at 39%.

As someone currently involved in these types of projects, borrowers of construction loans usually anticipate swapping expensive construction debt for permanent fixed rate debt after completion. In this market, people are worried that the developer, and construction lender , may be left holding the bag.

As of now, tightening lending standards are likely to impact lower quality/higher risk construction loans and refinancing first. Based on Prosperity's metrics, it does not appear they are a higher risk lender. Nonetheless, that's a risk we should all be aware of for any bank investment.

Prosperity is the most expensive of the three banks, but not by much. At 10.7x, it's trading ~14% below its trailing 12-month average. That's still 26% upside to 52-week highs plus the 3.5% dividend yield.

{kind=link}

Conclusion & A Note on Preferreds

All of today's banks are high quality. Their risk metrics are strong, and they don't have exposure to the same problems that sunk Silicon Valley Bank and Signature Bank.

All are set up to deliver double-digit returns over the next few years as the market eventually carries on higher. We'll continue to take the current issues in the banking system extremely seriously. At the same time, provided we do our homework, there is no reason to let a crisis go to waste.

Some may be wondering about these banks’ preferred stocks. Quantumonline is a good resource to learn the details of each issue. For most (95%+) companies, the preferred is not senior to the common when it counts.

By that, I mean bankruptcy. By the time the common is wiped out completely, preferred holders have little to no chance of a recovery. Look what happened at SBNY/SNBYP if you need a reminder.

So what does this mean? Only buy the preferred if it’s a better deal. For example, if you can obtain a preferred with the same or higher projected total return as the bank’s common stock, definitely go with the preferred. Let’s work through a couple examples.

MTB-H (MTB.PH) preferred is trading above $21. That’s less upside than we expect with the common (note: this is a complicated preferred issue and has a fixed-to-floating provision, so keep that in mind). The dividend yield is higher if that’s your primary objective. For me, the MTB provides better risk-adjusted returns. Now, if the preferred were to dip down below $18, that’s a different story.

This seems to be the case for CFR-B (CFR.PB) that last traded for $17.66. That’s a steep discount to par of $25, right? Not exactly .

To Cullen/Frost’s credit, they were able to issue this preferred with only a 4.45% coupon. That means it’s especially sensitive to the higher rate environment. We can verify this by watching how the preferred traded before Silicon Valley Bank collapsed. Going back to late 2022, CFR-B was trading between $18 and $20 per share.

CFR-B is trading well below par because it was issued with an unusually low coupon. You won’t see much capital gains on this unless rates are slashed, so there is no distressed pricing here. Once again, I think the common stock is superior.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

It's A Wonderful Life: 3 Regional Banks We're Buying