V - It's Groundhog Day (All Over Again) With Durbin's CCCA Legislation

2023-06-14 09:36:21 ET

Summary

- Senator Dick Durbin re-introduced the Credit Card Competition Act (CCCA).

- The CCCA will benefit big-box merchants and hurt American households.

- If it passes, expect credit to evaporate and the elimination of reward programs.

- Like his Durbin Amendment, the consequences aren't positive.

- Thankfully, we expect it to garner little support in DC.

Durbin Again

We love Bill Murray’s 1993 movie Groundhog Day. In it, Murray plays Phil Connors who wakes up every day, in the small town of Punxsutawney, Pennsylvania, about to film their annual Groundhog Day decision. It’s a real classic worth watching again.

There’s a pesky insurance agent named Ned Ryerson that asks Bill’s character to purchase insurance each and every day. In one scene, Ned says, “Do you have life insurance ? Cuz if you do, you could always use a little more. Am I right or am I right or am I right, right, right, right?”

We wrote a detailed note on this issue in October of last year, which can be read on the Seeking Alpha website. Unfortunately, Senator Durbin is pushing his anti-card agenda yet again. Senator Durbin reminds us of Ned and his latest card proposal reminds us of that hilarious recurring scene.

Senator Dick Durbin (Democrat, Illinois) re-introduced his CCCA or Credit Card Competition Act last week. After failing to advance his bill last July, Senator Durbin is trying yet again. A year ago, the CCCA reached the Senate Banking Committee, but it lacked enough support to proceed, and it didn’t even get a committee vote.

This time, Senator Durbin has gotten a few new co-sponsors; Senator Peter Welch (Democrat, Vermont), Senator Roger Marshall (Republican, Kansas) and Senator J.D. Vance (R-Ohio). While the bill appears to have attracted bipartisan support, numerous trade groups (representing the payments industry) have condemned the legislation. This version of the CCCA is identical to the prior version and will hopefully get the same response – DOA (dead on arrival). In theory, the CCCA aims to create more competition among US credit card networks and give merchants the opportunity to route payments through the network of their choice. Who wouldn’t want more competition, right?

If the CCCA becomes law, it will benefit big-box merchants, weaken fraud protections, restricting credit access (especially for middle-class and lower-end consumers), and curtail card rewards and loyalty programs. As we continue to discuss, this type of legislation doesn’t seem terribly helpful, especially for an economy struggling for growth and one that is fighting a mountain of worries (continued inflation, higher interest rates, debt burdens, a Ukrainian war, etc.).

Debit Economics

A decade has passed since the Durbin Amendment was written into Dodd-Frank, so we clearly can review its market impact. The quick takeaway is that debit routing rules have been fairly insignificant, except for being a gift to large merchants. Inside of that piece of legislation, it required a third, unaffiliated debit network be made available to all merchants. Today, merchants are free to make specific debit routing decisions off of Visa (V) or Mastercard (MA) and onto Fiserv’s (FI) STAR or Accel network or Fidelity National’s (FIS) NYCE network; they must consider price, risk, and the quality of the transaction. For example, Visa’s tokenization technology provides merchants with safer authentication and real-time fraud scoring capabilities that lower eCommerce chargebacks.

For banks over $10 billion in assets, the Fed mandated that debit pricing get lowered to $0.21 per transaction plus 0.05% of the face value. The market adjusted, eliminated debit loyalty programs, and utilized scale advantages to lower its fixed costs. Back in 2009, the Fed found that the average cost of debit processing was $0.08 per transaction. In 2019, it was down (50%), to just under $0.04. The debit industry is now remarkably lean, and these government mandated prices have taken most of the profit out of this industry.

Did any of those savings’ land in consumers wallets? Did big business pass along the savings to their customers? A recent merchant survey found that since 2011, the vast majority of retailers (76%) have either raised their prices or kept them flat.

Due to these debit interchange caps, banks incurred declines in debit revenue and responded by eliminating debit loyalty programs. In 2019, financial institutions claimed $14 billion in debit losses and have dramatically scaled back customer benefits. The prevalence of free checking accounts essentially no longer exists, and more consumers are getting hit with higher and more frequent bank fees. The Durbin Amendment had an admirable, foundational promise, but it ultimately is another example of political overreach.

Choice

The first aspect of the CCCA states that merchants should be allowed to process their credit payments over two networks, not just the one bug on the card presented for payment. This is the same exact maneuver Senator Durbin did with his debit card legislation, as we discussed above. The thinking behind his logic is that giving the merchant a network choice will increase competition and lower overall costs. That’s a fine theory, but it is entirely devoid of how the market operates.

Just like in debit routing, we don’t believe the vast majority of merchants want to decide – transaction by transaction – how their card payments travel. They simply want the transaction to occur quickly and keep their checkout lines moving. Most retailers rely on their merchant acquirer to make this decision and really don’t concern themselves with how the transaction is processed.

A former CEO of a large payment processor once told us the “inside baseball” of merchant acquiring economics. He said that acquirers always benefit from acceptance cost changes, as the savings from any drop in network fees is rarely passed along to SMB customers. He emphasized that only the largest merchants would realize savings, making it an inherent advantage versus their small business competitors. According to that payment executive, merchant acquirers always have the ability to “round up and round down”, to their advantage.

Credit Economics

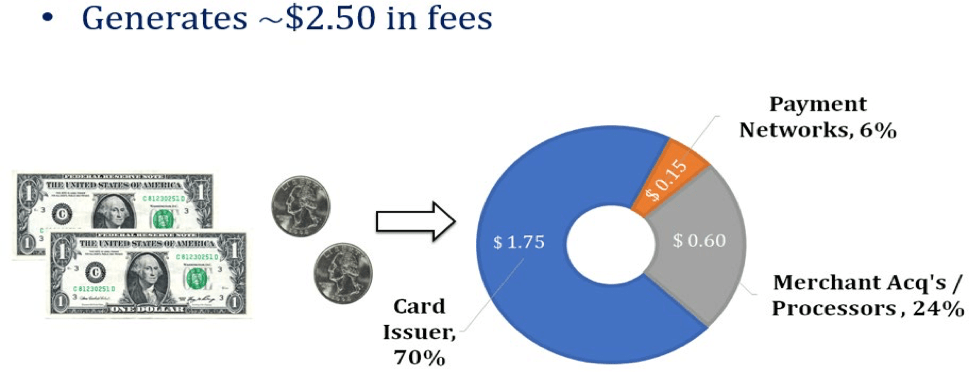

We like to use our 1-page pie chart, which highlights the economics of a typical $100 credit card transaction. As you can see, the vast majority of the economics go to the card issuers and banks, for taking the vast majority of the risk, while the smallest component of these fees goes towards the payment networks. Our simple pie chart shows the fees that are generated on a credit card transaction, but nothing is ever this simple. Transactions differ, based upon merchant type, in-store versus online, and dozens of other factors.

{kind=link}

Manole Capital slide on credit card economics (Manole Capital)

The issue of card acceptance costs is never straightforward. Online or eCommerce transactions have skyrocketed following COVID and now represent roughly 13.6% of all US retail sales. According to the US Census Bureau, US eCommerce sales totaled $215 billion in the first quarter of 2023, up +39% year-over-year.

Why do online transactions impact card acceptance costs? Well, according to the Fed, there was $12.40 in fraud losses per $10,000 in volume in 2019. Back in 2011, that was just $7.80 per $10,000 in volume. Merchants, banks, and card issuers absorb these losses, and the vast majority of fraud has shifted from brick-and-mortar, physical retailers to online shopping.

The Largest Merchants Benefit

We believe that only the largest merchants will benefit, as they try to shave half a penny off of their billions of transactions. Those potential savings will never flow to consumers, but just help the big merchant’s bottom line.

Merchants stand to benefit from the passage of the CCCA, but we do not believe they will pass along these savings to consumers. This has been tried numerous times and merchants always keep the savings for themselves. When debit costs were mandated to decrease under the Durbin Amendment (inside of Dodd-Frank legislation), consumers never received that obligatory discount. We expect the same thing will occur if the CCCA passes.

Senator Durbin’s goal is to reduce credit card processing costs for merchants. Yet, large merchants (like Walgreens, Wal-Mart, Amazon, and Target) already have a built-in advantage versus smaller “mom and pop” stores; they pay a lower interchange rate and MDR than small businesses, because they do significantly more transactions and generate much higher dollar volumes.

Thankfully, we do not think Senator Durbin has enough support to make the CCCA law. We believe there are material flaws in his thinking. While there is really no viable path for the CCCA to make it through the legislative process, there is always the risk that Senator Durbin attaches the CCCA to another critical piece of legislation. Last year, Senator Durbin tried to attach this to the Defense Bill, but it wasn’t allowed.

Competition Between Open & Closed-Loop Networks

According to the Nilson Report, the leading payment publication, Visa has 52% market share of total US credit card volume. After Visa, Mastercard is second at 24%, with American Express (AXP) closely behind at 20%. The fourth player is Discover at 4% of total US credit card spending. Visa and Mastercard are payment networks, not the card issuers (i.e., Bank of America, Capital One, Citi, JPMorgan Chase, Synchrony, Wells Fargo, etc.). Some banks issue both Visa and Mastercard’s, while others choose to utilize just one of the two largest brands.

Visa, Mastercard, American Express and Discover fight “tooth and nail” for business, in an extremely competitive market. Visa and Mastercard compete aggressively with each other to win deals with card issuing banks, while American Express and Discover issue their own cards through their own closed-loop network. As closed-loop networks, American Express and Discover act as both the network, payment processor and card issuer. Looking at our credit card economics pie chart, these closed-loop networks earn the majority of the fees.

If a merchant wants a lower MDR, it can choose to only accept the lowest priced card – Discover. If a merchant wants higher end customers, with higher spending patterns, it can choose to only accept American Express. That is a conversation that every merchant can have with their merchant acquirer, as the entity working with businesses on their card acceptance. Why are our Senators getting involved with instituting price caps and interfering with well-functioning businesses?

In order to process a Visa credit transaction over a closed-loop network like Discover would require a huge (and unnecessary) investment. What is the benefit? Who will pay for this? In 2020, 31 European banks started a new, pan European payments network called EPI (the European Payments Initiative). It failed to obtain the necessary funding to scale, and twenty banks have already opted out of it. Visa can handle 65,000 transactions per second and has proven to be a viable payment network accepted in over 200 countries around the world.

Senator Durbin believes that increased credit card competition will pressure MDR’s or the merchant discount rate that retailers pay for accepting a card payment. We believe this thinking is entirely off base and the CCCA is just another piece of flawed legislation.

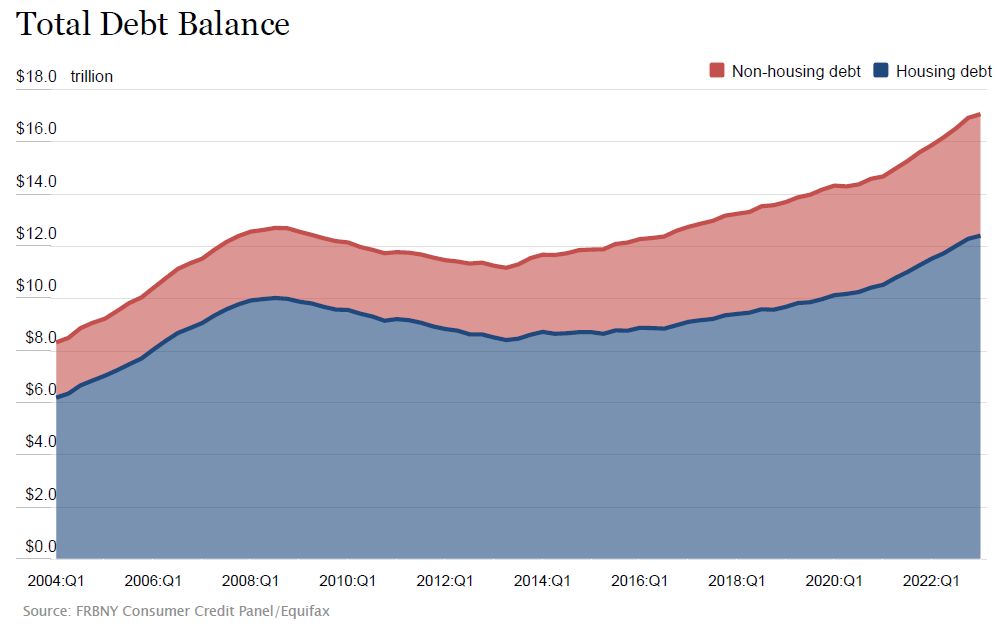

Credit Card Balances

We know that the US consumer is the lifeblood of our economy and consumer spending accounts for roughly two-thirds of our economic activity.

{kind=link}

NY Fed Total Debt Balances (New York Federal Reserve)

Credit card balances are contributing to pressure on US households, with debt levels now topping $17 trillion (as seen in this chart from the New York Fed). Unfortunately, the Federal Reserve recently stated that US households have now amassed nearly a trillion dollars of credit card debt. More than ever, it seems that Americans are relying on their credit cards, as their primary payment mechanism. According to the Federal Reserve Bank of New York, consumers now owe a record $988 billion on their credit cards, up +17% year-over-year. This equates to $5,700 per person.

Higher interest rates are compounding this problem, as APR’s (annual percentage rate) are now over 20%. According to the Fed, which tracks APRs, it is the highest level it has seen since it started tracking these levels in 1994. As balances grow, this problem compounds.

Inflation

Another component of this sharp increase in credit card balances is inflation. It is causing more consumers to put non-discretionary items onto their cards. Merchant advocacy groups, like the Merchant Payments Coalition, claim that small businesses are being taken advantage of by Visa, Mastercard and the big banks in New York City, at a time when average Americans are struggling with crippling inflation and a looming recession. These same consultants and lobbyist groups (National Retail Federation, National Association of Convenience Stores, National Grocers Association and National Restaurant Association) claim that swipe fees are an unfair burden forced onto them by the payment networks. The reality is quite different.

Interchange and MDR’s have remained fairly stable and actually been lowered. Despite inflation trends that remain unfortunately too high, the estimated weighted average credit card interchange rate (for US sellers) has remained unchanged since 2016 at 1.8%. If one looks at MDR’s, the average US merchant is paying 2.2% in fees, less than it did in 2019.

Consumers rely on card payments and all the benefits they provide (reward programs, convenience, safety, and fraud protections). The narrative that big banks are taking advantage of poor ol’ Walmart and Amazon and Target simply are not true. These and other large merchants actually have an advantage over smaller retailers, as they pay significantly less than the average fees listed above. The merchant argument isn’t fair, as they undervalue the benefits of card acceptance like less theft, reduced fraud, transportation costs, and convenience.

Banks & Lending

In March, the banking industry was thrown in chaos, as Silicon Valley Bank and Signature Bank failed. We wrote a detailed note on their collapse, which can be read on Seeking Alpha's website. We also did a podcast on banking volatility, which can be heard by clicking here.

Over the last few weeks, there has been commentary about what the FDIC will do to banks, to refill their insurance coffers. This is a necessary evil but will act as just another headwind to overall lending. Following the banking volatility in March, we know that banks are already hesitant to increase lending because they fear more restrictive capital requirements. If the CCCA passes, it will further pressure banking profitability and tighten overall lending.

Over the last year, we had 13 million US individuals file for bankruptcy. This allows individuals to wipe away their debt, but it is the banks that pay for these losses (in the form of charge-off’s). After a three-year payment hiatus, 43 million American adults (17% of US adults) will be paying their student debt again. These individuals owe $1.6 trillion and it likely will be another $300 to $400 per month in expenses. Clearly, this will act as an incremental spending headwind. For an economy that is struggling to show much growth, this type of illogical legislation is the last thing we need.

If the CCCA were to pass, the card issuers and banks will restrict credit, and this will have a terrible impact on US spending. If banks and card issuers cannot earn a fair return for their risk, they will potentially exit the business. Or maybe they will lower rewards and loyalty programs. Americans love shopping and earning loyalty, points, miles, and rewards for their business. This is entirely funded through interchange fees, earned by the banks and card issuers. When debit got regulated, these loyalty programs (tied to debit usage) disappeared. Does Senator Durbin realize that his legislation poses a risk to the programs that millions of Americans love?

Senator Durbin claims that the CCCA would only apply to financial institutions with $100 billion or more in assets, so it wouldn’t hurt smaller banks and credit unions. If that was actually the case, why would the largest credit union association come out against the CCCA?

The NAFCU (National Association of Federally Insured Credit Unions) represents not-for-profit credit unions and provides banking services to 135 million consumers. It wrote a letter to Congressional leaders that specifically said that the unaffiliated network aspect of the CCCA would be counterproductive. In its view, the NAFCU said the legislation would only benefit retailers, not consumers. Its letter said, “This bill is unwarranted and represents a heavy-handed government intrusion into the credit card payments market that would hurt credit unions and consumers alike, while allowing the largest retailers to pocket significant cost savings.”

The NAFCU warned that the passage of the CCCA would reduce its credit union members’ revenue from swipe fees and thereby limit loyalty programs, fraud protection and other benefits. It said, “Credit unions are committed to serving their members and, as such, must be able to make a reasonable return on payment card programs in order to continue to provide important consumer financial services, such as free checking accounts and member help lines when data breaches occur.” We wonder whether free checking might disappear, if the CCCA passes.

Consequences

In our opinion, the CCCA and its intent to increase credit card routing competition will have unintended consequences. Senator Durbin’s proposed legislation might pressure card fees, but we know that it will greatly reduce rewards programs, access to capital, and add additional fees to credit cards.

The Chairman of the EPC (Electronic Payment Coalition) is Jeff Tassey. He recently said, “This legislation would again boost retailers’ bottom lines at the expense of American consumers — stripping them of their credit card rewards and usurping their choice of network while leading to a less secure, less innovative, and weaker financial system.”

He further argues that the CCCA will make transactions less secure and said, “When [the] government comes in and puts hands on one side of the customer scale, like they did in the Durbin amendment [for debit networks], you have all kinds of unintended consequences.”

Conclusion

The lingering impact of the pandemic is still with us, and it has put a large financial weight on our small businesses and families. Politicians are always looking to get re-elected and are understandably eager to pursue any policies they feel will ease their constituent’s burdens. However, lawmakers must be careful not to write laws when they aren’t sure of the ramifications.

The debit rules inside of the Durbin Amendment did nothing to help struggling Americans and small businesses. Imposing government price controls on debit interchange did nothing to pass along savings to customers but did allow retailers to profit.

We met with Senator Durbin in Washington DC in September 2010. It appears to us that Senator Durbin doesn't seem to understand that Visa and Mastercard (as well as American Express and Discover) have invested billions into security to safeguard the payment system. Their brands resonate the ability to transact anywhere quickly and safely in the world in seconds. Their technology prevents fraud and provides consumers with valuable chargeback protections. Senator Durbin (and his staff) didn’t understand the payment process a decade ago and they certainly don’t understand it in 2023.

We wonder what Senator Durbin has in his leather wallet and what he uses when he shops in Chicago, Illinois or Washington, DC? Maybe he’s the last guy that loves to carry and use paper currency?

The CCCA pits two very powerful lobbying groups against each other – large banks versus retailers. Will this legislation wreak havoc on a well-functioning payment ecosystem? Our payment platforms handle billions of transactions and trillions of dollars, in mere seconds. Back-door price controls have the potential to upset the delicate balance between US cardholders, merchants, acquirors, processors, banks, and card issuers. We will continue to closely monitor the CCCA and its progress. Hopefully it doesn't get attached to another piece of legislation.

Warren Fisher, CFA

Founder and CEO

Manole Capital Management

DISCLAIMER:

Firm : Manole Capital Management LLC is a registered investment adviser. The firm is defined to include all accounts managed by Manole Capital Management LLC. In general: This disclaimer applies to this document and the verbal or written comments of any person representing it. The information presented is available for client or potential client use only. This summary, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any securities or investment advisory services, which may be made only by means of a private placement memorandum or similar materials which contain a description of material terms and risks. This summary is intended exclusively for the use of the person it has been delivered to by Warren Fisher and it is not to be reproduced or redistributed to any other person without the prior consent of Warren Fisher. Past Performance: Past performance generally is not, and should not be construed as, an indication of future results. The information provided should not be relied upon as the basis for making any investment decisions or for selecting The Firm. Past portfolio characteristics are not necessarily indicative of future portfolio characteristics and can be changed. Past strategy allocations are not necessarily indicative of future allocations. Strategy allocations are based on the capital used for the strategy mentioned. This document may contain forward-looking statements and projections that are based on current beliefs and assumptions and on information currently available. Risk of Loss: An investment involves a high degree of risk, including the possibility of a total loss thereof. Any investment or strategy managed by The Firm is speculative in nature and there can be no assurance that the investment objective(s) will be achieved. Investors must be prepared to bear the risk of a total loss of their investment. Distribution: Manole Capital expressly prohibits any reproduction, in hard copy, electronic or any other form, or any re-distribution of this presentation to any third party without the prior written consent of Manole. This presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to local law or regulation. Additional information: Prospective investors are urged to carefully read the applicable memorandums in its entirety. All information is believed to be reasonable, but involve risks, uncertainties and assumptions and prospective investors may not put undue reliance on any of these statements. Information provided herein is presented as of the date in the header (unless otherwise noted) and is derived from sources Warren Fisher considers reliable, but it cannot guarantee its complete accuracy. Any information may be changed or updated without notice to the recipient. Tax, legal or accounting advice: This presentation is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any statements of the US federal tax consequences contained in this presentation were not intended to be used and cannot be used to avoid penalties under the US Internal Revenue Code or to promote, market or recommend to another party any tax related matters addressed herein.

For further details see:

It's Groundhog Day (All Over Again), With Durbin's CCCA Legislation