DBRG - It's Hard To Beat A Cell Tower REIT

2023-03-09 07:00:00 ET

Summary

- That first phone, developed by Martin Cooper weighed 2.5 pounds and measured 11 inches.

- The inspiration for his cell phone idea was not the personal communicators on “Star Trek,” but comic strip detective Dick Tracy’s radio wristwatch.

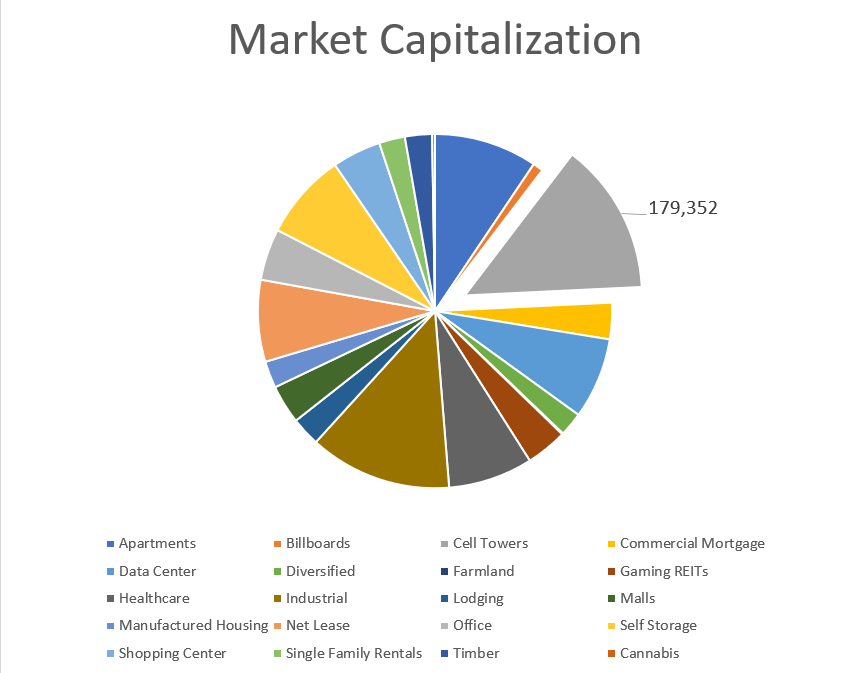

- Of course, little did Cooper know that he would also be responsible for pioneering the largest REIT property sector with a combined market capitalization of over $180 billion.

I never will forget my first cell phone – a clunky bag phone that I used on various jobsites as a real estate developer. It was a brand-new shiny toy for me, and because I was one of the first to own one in my town, it gave me a competitive advantage, for a while.

A few days ago, I ran across an article on a fellow named Martin Cooper, who was credited with inventing the cell phone over 50 years ago.

“Little did he know when he made the first call on a New York City street from a thick gray phone prototype that our world – and our information – would come to be encapsulated on a sleek glass sheath where we search, connect, like, and buy.”

The 94-year-old inventor told The Associated Press,

“My most negative opinion is we don’t have an privacy anymore because everything about us is now recorded someplace and accessible to somebody who has enough intense desire to get it.”

That first phone, developed by Cooper weighed 2.5 pounds and measured 11 inches. The inspiration for his cell phone idea was not the personal communicators on “Star Trek,” but comic strip detective Dick Tracy’s radio wristwatch.

Of course, little did Cooper know that he would also be responsible for pioneering the largest real estate investment trust, or REIT, property sector – cell tower REITs – with a combined market capitalization of over $180 billion.

{kind=link}

The Basic Business Model

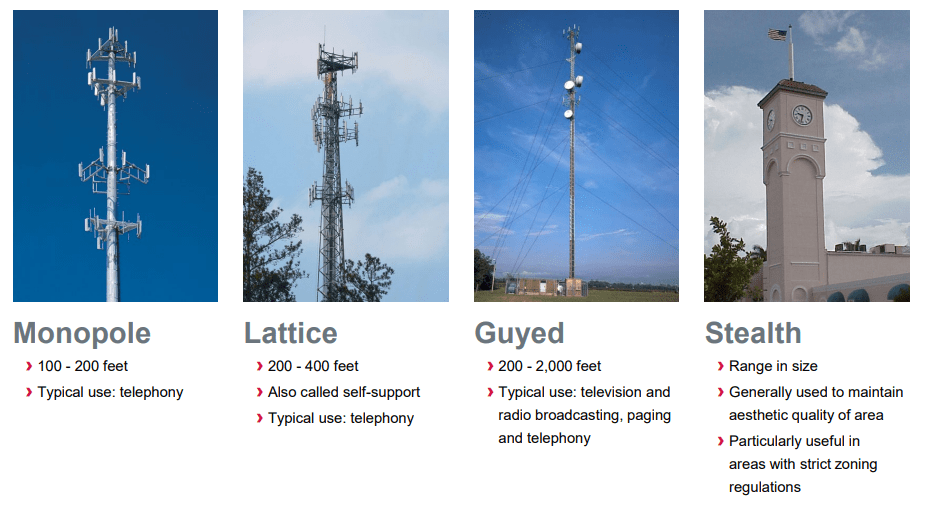

A cell tower is a vertical structure built on a parcel of land, designed to accommodate multiple tenants that utilize many different technologies, including telephony, mobile data, broadcast television, machine to machine and radio.

Cell tower tenants lease vertical space on the tower and portions of the land underneath for their equipment. The cell tower REIT typically owns or leases under a long-term contract. The tenant typically owns and operates the equipment, including antenna arrays, antennas, coaxial cables and base stations. As illustrated below, there are four types of towers:

{kind=link}

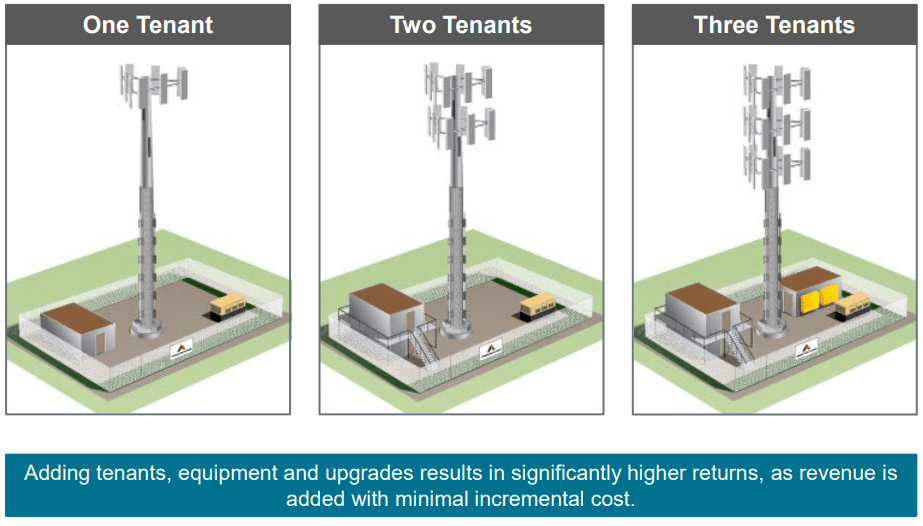

The tower structures are typically owned by the REIT and are constructed with the capacity to support 4 to 5 tenants. The land parcel is owned or operated under a long-term lease by the REIT and oftentimes the REIT also owns the generators to help facilitate back-up power for the site’s tenants.

One primary advantage for owning cell tower REITs is that the towers generate multiple revenue streams because of multiple tenants. The rental charges are typically based on property location, leased square footage, and the weight placed on the tower from the transmission equipment.

{kind=link}

The leases are long-term contracts that are typically non-cancellable and generally include an initial term of 5 to 10 years with multiple renewal terms at the option of the tenant. The leases have annual escalators (in the U.S.) that are typically fixed at an average of approximately 3%. Rent escalations in international markets are typically based on local inflation rates.

One other advantage for owning cell tower REITs is that the require low ongoing cap ex requirements. Examples for cap ex improvements include spending on lighting systems, fence repairs, ground upkeep, etc. Per tower cap ex spend is ~$500 - $800 annually in international markets and ~$1,200 - $1,700 in the U.S.

Cell tower REITs also have revenue generated cap ex that includes redevelopment (spending to increase capacity of towers), ground lease purchases (to purchase land under sites), and discretionary capital projects (primarily for the construction of new communications sites).

{kind=link}

Crown Castle Inc. ( CCI )

Crown Castle is a real estate investment trust that owns, operates, and leases communication infrastructure including cell towers, rooftops, small cells, and fiber optic cables. They are well spread out across the U.S. and have over 40,000 cell towers, approximately 120,000 small cells, and around 85,000 route miles of fiber.

Most of their communication infrastructure is shared and can support multiple tenants. CCI’s core business is supplying access to their shared communications infrastructure by long-term contracts, including lease, sublease, license, and service agreements.

Because their communication infrastructure assets can be shared, CCI aims to increase rental revenues by adding more tenants on their shared infrastructure.

CCI - Investor Presentation

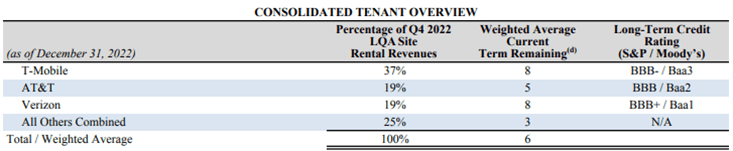

Crown Castle’s largest tenants are T-Mobile, AT&T and Verizon which together make up around 75% of CCI’s site rental revenues. Site rental revenues makes up the majority of CCI’s total revenues at 90% as of December 31, 2022.

Most of CCI’s site revenues are generated from their towers segment, with 69% coming from this segment, and 31% of their site rental revenue comes from their fiber segment. At the end of 2022, CCI’s tenant contracts had a weighted average remaining life of roughly six years, which represents approximately $40 billion of expected future cash flows.

{kind=link}

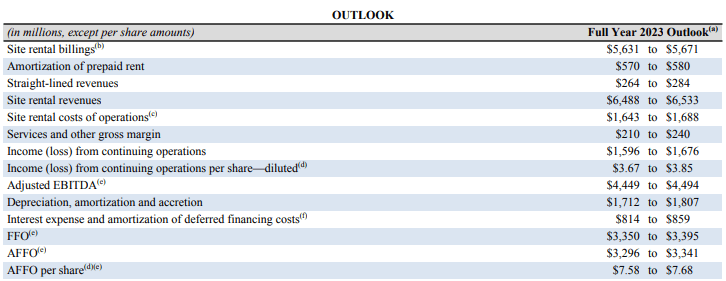

CCI reported its fourth quarter and full year 2022 results on January 25, 2023. Site rental revenues for the full year came in at $6.3 billion for a 10% increase compared to 2021.

Income from continuing operations per share was $3.86, representing a 45% increase over the prior year. Adjusted EBITDA was reported at $4.3 billion for a 14% increase over 2021, and AFFO per share came in at $7.38 for a 6% year-over-year increase.

Their 2023 guidance calls for a midpoint of $6.5 billion in site rental revenues, adjusted EBITDA midpoint of $4.4 billion, and a midpoint AFFO per share of $7.63 for an increase of 4%, 3%, and 4% respectively. During 2022, CCI paid approximately $2.6 billion in dividends, or $5.98 per share for more than a 9% increase when compared to 2021.

{kind=link}

CCI has good debt metrics with a net debt to LQA EBITDA of 4.9x, an interest coverage ratio of 5.5x, and a fixed charge coverage ratio of 4.9x. They have a long-term debt to capital of 75.66% and as of December 31, 2022, CCI had $327.0 million in cash or cash equivalents and $6.6 billion in revolver availability. Their weighted average interest rate is 3.6%, their weighted average term to maturity is 8.2 years, and 87% of their debt is set at a fixed rate.

CCI - Investor Presentation

{kind=link}

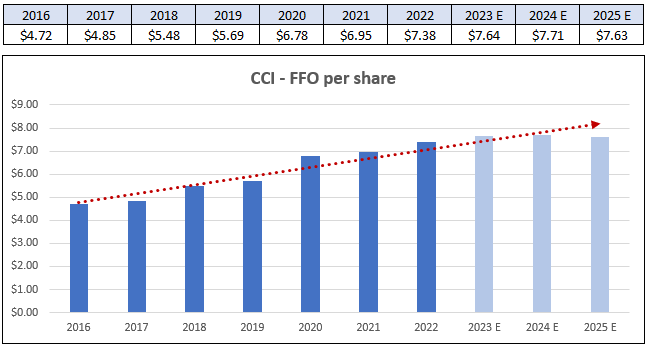

Since 2016 Crown Castle has delivered steady growth in its funds from operations (“FFO”) with an average growth rate of 5.89% per year. They have increased FFO each year from 2016 to 2022 and are expected to see 4% growth in FFO in 2023. Analysts expect for growth to tail off in 2024 and 2025 with FFO growth rates of 1% and -1% respectively.

{kind=link}

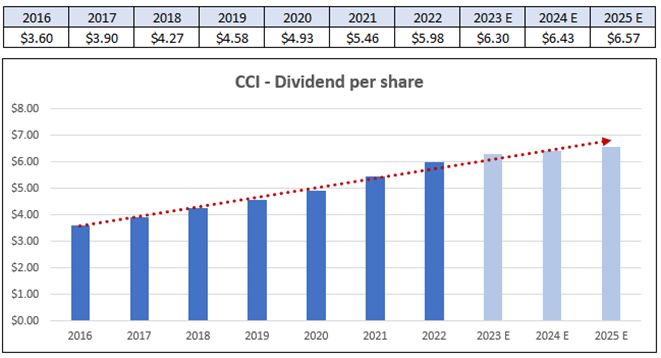

Currently CCI pays a 4.76% dividend yield that is covered by a 2022 AFFO payout ratio of 80.96%. They have delivered strong growth in their dividend payouts with an average dividend growth rate of 8.64% since 2016. Analysts project 2023’s dividend to be $6.30 which would represent a 5.35% year-over-year increase.

{kind=link}

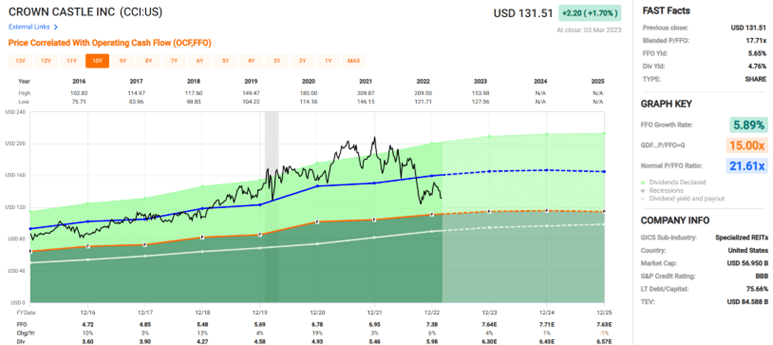

Crown Castle is trading at a P/FFO multiple of 17.71x which is well below their normal P/FFO multiple of 21.61x. They are investment-grade with a credit rating of BBB and have good debt metrics.

CCI has an above average yield that is covered by AFFO and have consistently delivered FFO & dividend growth. Additionally, they are in an industry with a long runway for future growth. At iREIT, we rate Crown Castle a Spec BUY.

{kind=link}

SBA Communications Corporation ( SBAC )

SBA Communications is a real estate investment trust that owns and operates wireless communications infrastructure that includes cell towers, rooftops, distributed antenna systems (“DAS”) and small cells.

They refer to their communication assets as “sites” or “towers.” SBAC operates through two main business segments, site leasing and site development services. SBAC’s main focus is leasing antenna space on its communication sites to wireless service providers under long-term leases.

At year-end 2022, SBAC owned 39,311 towers the majority of which are able to lease space to multiple wireless providers. Their primary operations are in the U.S., but they also have locations in South America, Central America, Canada, South Africa, the Philippines, and Tanzania.

Their primary segment is their Site Leasing business. For the year-end 2022, SBAC generated 96.2% of their operating profit and 88.73% of their revenue from their Site Leasing business. SBAC’s second business segment, Site Development, makes up the minority of their revenue, representing only 11.3% of their revenue. Through their Site Development business line, they assist wireless service providers to maintain and develop their wireless networks.

{kind=link}

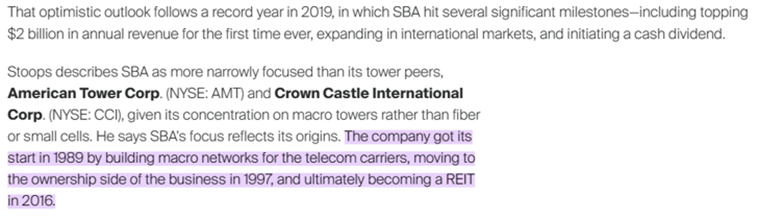

SBA Communications was founded in 1989 and started by building towers for telecom carriers before moving to the ownership side in 1997. The company converted to a REIT in 2016, but did not start paying a dividend until 2019 due to past net operating losses that they were able to carry forward to offset earnings, which essentially allowed them to maintain their REIT status without paying dividends for several years.

{kind=link}

SBAC has high tenant concentration among the largest wireless carriers. In 2022 T-Mobile made up 36.4% of their revenue, AT&T made up almost 20.0%, and Verizon made up 14.5% of their revenue.

In addition to the major carriers, SBAC leases space to smaller companies including Liberty Technologies, Telefonica, U.S. Cellular, and Vodacom.

SBAC - Form 10-K

SBA Communications credit metrics could be better. They are not investment-grade rated, with a credit rating of BB+ by S&P Global. They have net debt totaling $12.8 billion with negative equity / total shareholder deficit of $5.3 billion.

Their long-term debt to capital is 150.43% and they have a net debt to annualized adjusted EBITDA of 6.9x. On a positive note, they have ample interest coverage with a net cash interest coverage ratio of 4.7x.

{kind=link}

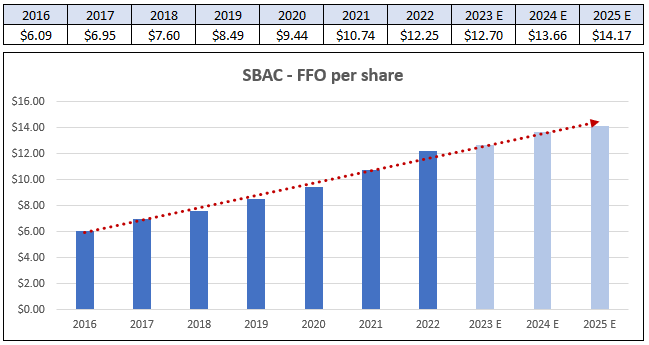

While their credit metrics could be better, there is no issue with the growth in their funds from operations. Since converting to a REIT in 2016, SBAC has averaged FFO growth of 9.55% per year with analysts expecting FFO growth of 4% in 2023 and 8% in 2024.

{kind=link}

The same can be said of their dividend. Since initiating the dividend in 2019, SBAC has a compound growth rate of 56.57%. Much of this growth came from the increase from $0.74 in 2019 to $1.86 in 2020 (151.35% increase), but over the last two years they have increased the dividend by an average amount of 23.57%. They pay a dividend yield of 1.31% that is extremely well covered with an AFFO payout ratio of just 23.18% in 2022.

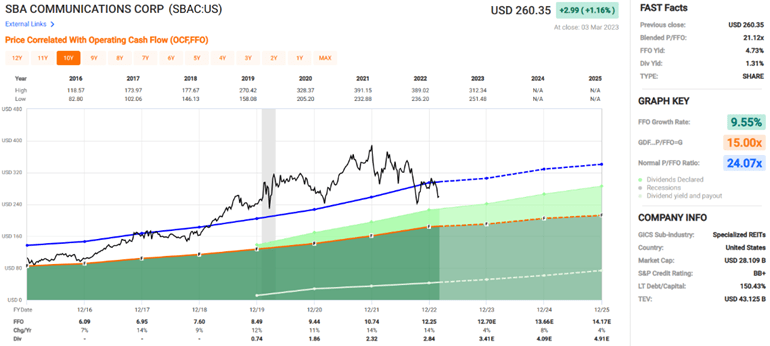

FAST Graphs (compiled by iREIT)

SBAC is currently trading at a P/FFO of 21.12x which is below their normal P/FFO multiple of 24.07x. Their dividend yield isn’t the highest, but their dividend growth rate is excellent and their AFFO coverage is one of the best I’ve seen, and leaves plenty of room for future dividend growth.

Similarly, their FFO growth has been excellent and should have no problem supporting the dividend. My biggest concern is their debt as a percentage of their total capital and their debt when compared to earnings (leverage ratio of 6.9x). At iREIT, we rate SBAC as a Spec BUY.

{kind=link}

American Tower Corporation ( AMT )

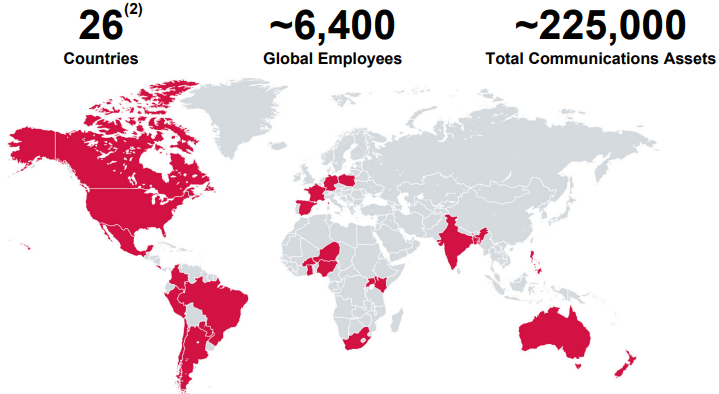

American Tower is the largest Cell Tower REIT with a total market capitalization of $92.53 billion. They specialize in multitenant communications real estate that includes cell towers and distributed antenna systems (“DAS”) networks.

They also hold other telecommunications infrastructure, fiber, and property interests that are leased to third party operators. In all, they have a global portfolio of almost 225,000 communication sites in 26 countries.

{kind=link}

Additionally, since their acquisition of CoreSite Realty, American Tower has a portfolio of interconnected data centers that are primarily leased to enterprises, network operators, and cloud providers.

AMT’s core business, referred to as their property operations, is leasing space on its communication sites to wireless providers, broadcast companies, government agencies, and multiple tenants in other industries.

Property operations accounted for 98% of AMT’s total revenues as of December 31, 2022. In addition to their property operations, they have service operations that offer tower-related services including zoning and permitting, site application, and construction management.

{kind=link}

AMT has made significant improvements to its balance sheet over the last year. They reduced their net leverage from 6.8x in 2021 to 5.4x in 2022. Their liquidity increased by a billion dollars, from $6.1 billion in 2021 to $7.1 billion in 2022.

Additionally, they improved their fixed rate debt as a percentage of total debt, bringing it to 78% vs 69% in the prior year. They are investment-grade with a credit rating of BBB- by S&P Global and have a long-term debt to capital ratio of 79.32%.

AMT - 4Q22 Operational Update

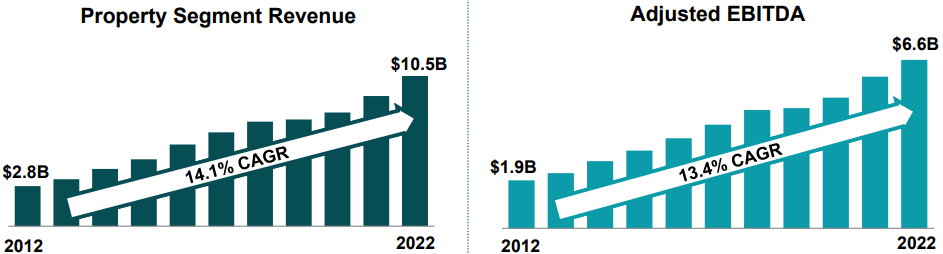

Over the past decade AMT has delivered growth in property segment revenue, adjusted EBITDA, and funds from operations. AMT’s property segment revenue had a compound annual growth rate of 14.1% and their Adjusted EBITDA had a compound annual growth rate of 13.4% since 2012.

{kind=link}

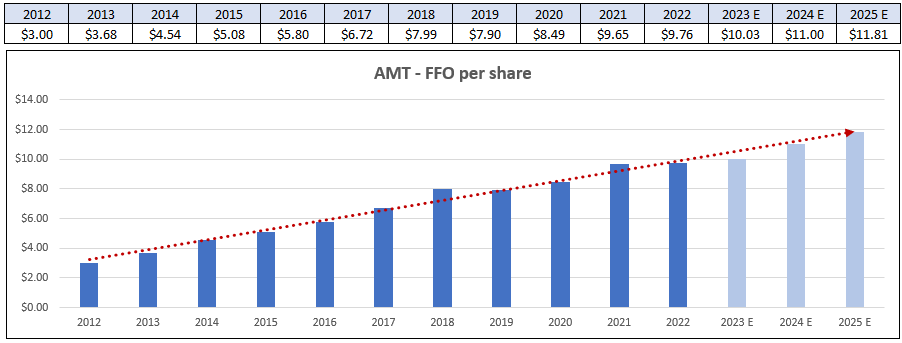

American Tower has an average FFO growth rate of 11.85% since 2012. Within that time period, AMT increased FFO per share in every year except for 2019 when it declined by -1%. Analysts expect FFO to grow by 3%, 10% and 7% in the years 2023, 2024, and 2025 respectively.

{kind=link}

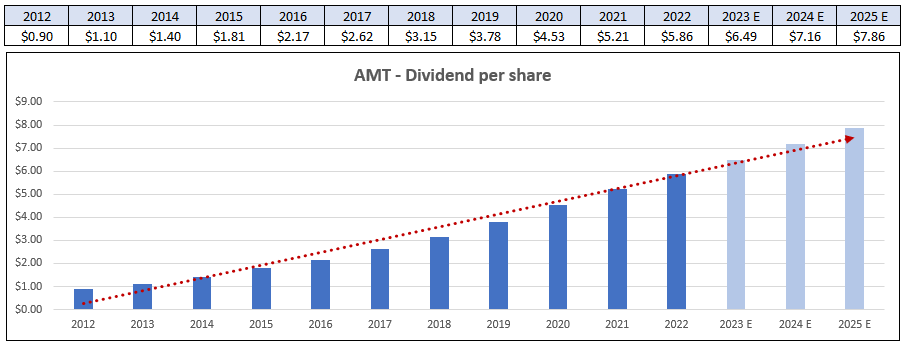

AMT’s dividend growth has been even more impressive. Over the last 10 years AMT has increased its dividend by a compound growth rate of 20.61%. The dividend was increased by 12.48% in 2022 and analysts expect a dividend increase of 10.75% in 2023. Currently AMT offers a dividend yield of 2.89% that is very well covered with a 2022 AFFO payout ratio of just 60.04%.

{kind=link}

{kind=link}

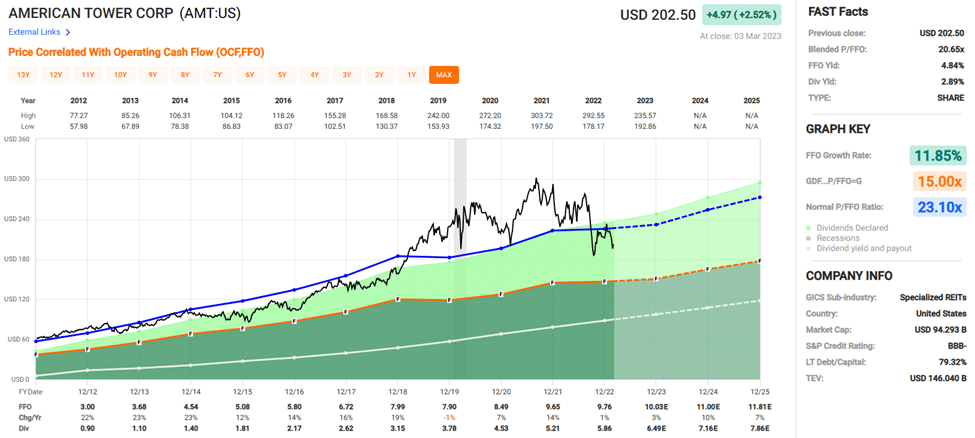

American Tower is a blue-chip, fast growing REIT with an above average yield that is very secure. They are trading at a P/FFO of 20.65x which is a discount to their normal P/FFO multiple of 23.10x. They have strong credit metrics and plenty of liquidity for future investment. At iREIT, we rate American Tower a Strong BUY.

{kind=link}

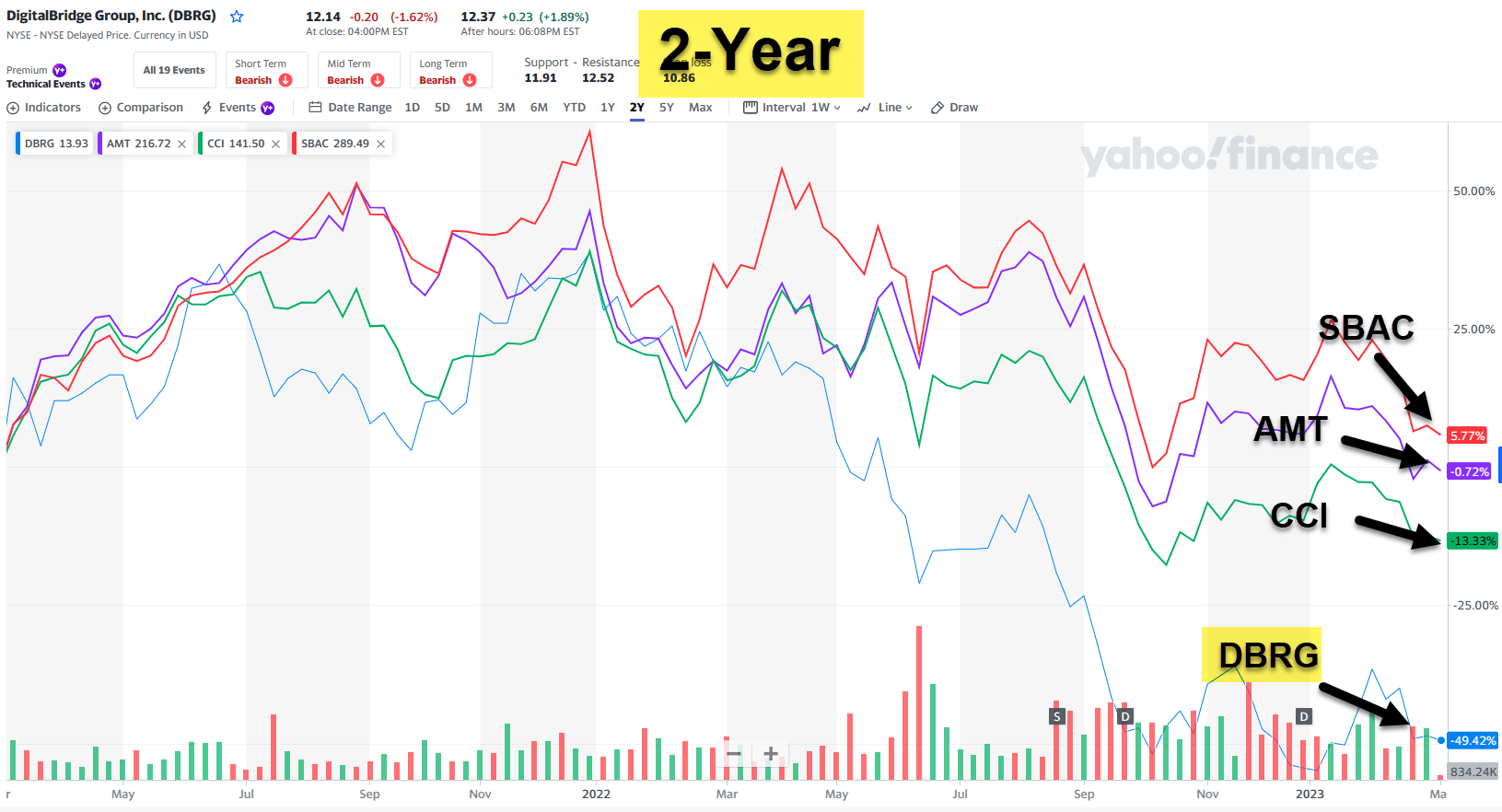

What about DigitalBridge?

DigitalBridge Group, Inc. ( DBRG ) is NOT a REIT.

Formerly called Colony Capital, the company is considered a global-scale digital infrastructure firm that invests across five key verticals: data centers, cell towers, fiber networks, small cells, and edge infrastructure .

The company manages nearly $65 billion on behalf of its limited partners and shareholders and is focused on identifying differentiated investment opportunities within digital infrastructure around the world.

DBRG is currently unrated by the big 3 credit rating agencies and a comparable analysis of DBRG’s credit profile puts them as a non-investment grade issuer. Last week BrightSpire (BRSP) said that they were pricing a secondary offering to unload DBRG’s stake (in BRSP) at $6.00 per share.

Our members have requested a deep dive on DBRG, and we will put together a report in short order.

{kind=link}

For further details see:

It's Hard To Beat A Cell Tower REIT