O - It's Not Always Rainbows And Butterflies

2023-12-17 07:00:00 ET

Summary

- I believe we’re in the early stages of a REIT rally.

- While investing can be difficult and challenging (not all rainbows and butterflies), I’m beginning to see the light at the end of the rainbow.

- It’s important to continue to maintain strict discipline and avoid chasing yield.

I can’t say I’m the biggest Maroon 5 fan ever. Though like most people who listen to contemporary music, I do know who they are.

The band has produced hit after hit, such as:

- “Harder to Breathe

- “Moves Like Jagger”

- “This Love”

- “Cold”

- “Sunday Morning”

- “Sugar”

- “Animals.”

In all, they have at least 20 top 20 hits, including the one I happened to hear the other day that inspired this article, “She Will Be Loved.”

It’s one of Maroon 5’s older songs, released way back in 2002. But you still might recognize these lines:

“It’s not always rainbows and butterflies

It’s compromise that moves us along. Yeah.

My heart is full and my door’s always open.

You come any time you want. Yeah.”

Really, the song is a little sappy, not to mention “soppy” with a chorus that croons:

“I don’t mind spending every day

Out on your corner in the pouring rain

Look for the girl with the broken smile

Ask her if she wants to stay a while”

As an older and wiser man these 21 years later, I can tell you that sounds like a perfect plan to catch pneumonia. But I will give credit where credit’s due about the “It’s not always rainbows and butterflies” part.

Every part of life – investing including – involves its ups and downs, its pros and cons. If you want to make money in the markets, that’s the first lesson you need to learn.

And then never, ever forget it.

My Biggest Losers on Display

Anyone who tells you they can guarantee you’ll make money is either:

- A well-meaning nitwit

- A scam artist.

I can’t think of any other options available. That’s why I publish an article about my worst picks every single year: to keep as many cards on the table as I can.

It keeps me humble and you informed – including about how I’m not perfect.

It’s true that I publish my best picks every single year as well. But that keeps you informed too, this time about how valuable real estate investment trusts (REITs) and other dividend-paying stocks can be.

I’ll be publishing “My Biggest Winners of 2023” sometime soon. But for right now, I want to focus on its counterpart I just published on Wednesday.

In “My Biggest Losers of 2023,” I write at the very end:

“So there you are.

“I just showed the world that I don’t bat 1,000, which means I’m far from perfect.

“The good news is that I have far more winners than losers, and that allows me to sleep well at night.”

I’ll skip the “bragging” part about some of those winners to get to this part:

“… I’ve purposely diversified my investment portfolios to avoid catastrophic losses. These three losers [mentioned in the article] account for less than 5% of my combined portfolios.”

That’s a logical thing to do when you understand that investing isn’t “always rainbows and butterflies.” You spread out your risk to catch as much sunshine as you can and as few rounds of unexpected hail.

Because the unexpected can and does happen more often than we’d like.

Always Be Prepared

One of this year’s biggest losers is Medical Properties Trust ( MPW ).

I’m still holding onto it, but I fully acknowledge that shareholders like me “have suffered greatly since the beginning of 2023. The stock has fallen “by almost 60% year-to-date” and “by more than 80% since the beginning of 2022.”

Ouch!

(Update: Shares are +10% today, so the numbers aren’t that bad)

And, as some of my readers were quick to point out in the comments section, MPW is also now under federal investigation.

I can honestly tell you I didn’t see any of that coming despite all my research.

But, again, that’s also why I only bought up a bit of it – and shared the cons as well as the pros with my readers. I knew it had its problems, even if I had no clue they’d get this bad.

Moreover, even if I couldn’t find a single negative detail about a company, I’d still limit my position (though not as much as with something like MPW). Again, it’s the smart thing to do when you can never quite tell what’s around the next economic corner.

Who knows. We could be in for a recession. Or a boom. Rates could go down (though they’ll probably stay as-is for another quarter or two).

You want to be as prepared as possible.

That’s why I also advised:

“… I have a strategic blueprint with asset allocation targets, and I encourage all readers to do the same. I suggest utilizing a custom-tailored portfolio that’s designed for your unique risk tolerance level.

“Finally, don’t be too cocky. Overconfidence produces greater risks and generates lower returns.”

Don’t be cocky. Don’t be greedy. Don’t be impatient.

Not even with well-researched REITs with solid histories and great prospects looking forward. Because as those sappy, soppy philosophers once sang, “It’s not always rainbows and butterflies.”

Alexandria Real Estate ( ARE )

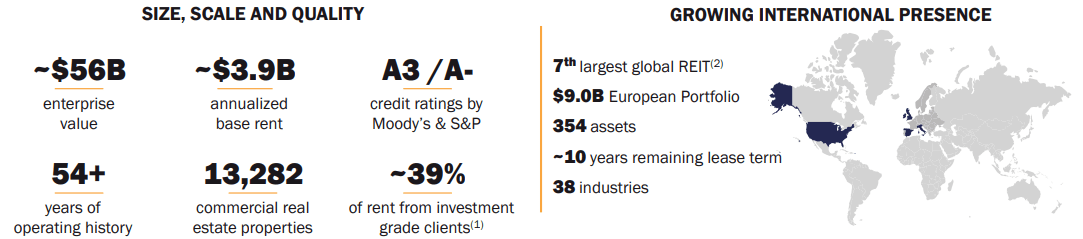

Alexandria pioneered the life science real estate niche since its formation in 1994 and is the most established, longest-running owner, developer, and operator of collaborative life science properties.

ARE is classified as an office real estate investment trust (“REIT”) and has sold off along with the other REITs in the sector but ARE is very different from a traditional office REIT.

Alexandria builds and leases out laboratory space to leading biotech and multinational pharmaceutical companies such as Eli Lilly, Merck, and Moderna as well as top academic institutions such as Harvard and New York University.

Their tenants use ARE’s lab space to conduct experiments, develop medicine, and perform other types of research and development that are regulated and cannot be done from home. With Alexandria, I like to think of it as beakers and flasks instead of desktops and cubicles.

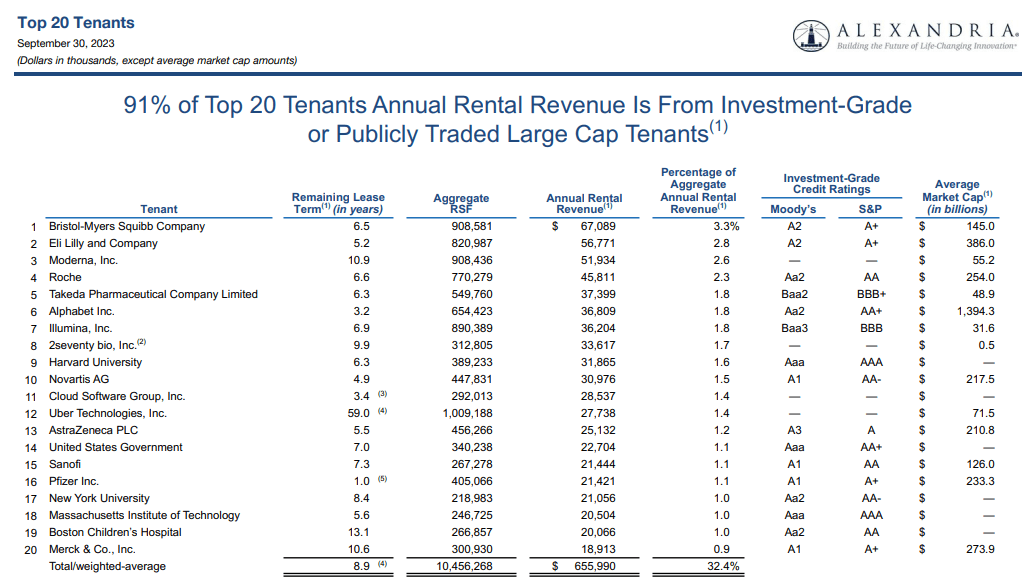

ARE has a high-quality tenant base of approximately 800 and is well diversified with their top tenant (Bristol-Myers) only making up 3.3% of ARE’s rental revenue and their top 20 tenants only making up 32.4% when combined.

Plus, 16 out of ARE’s top 20 tenants are investment-grade rated.

{kind=link}

Alexandria has a 75.1 million SF asset base in North America that consists of the following:

- 41.5 million rentable square feet (“RSF”) of operating properties

- 5.6 million RSF of Class A/A+ properties under construction

- 8.9 million RSF of near-term development projects, and

- 19.1 million square feet allocated for future development

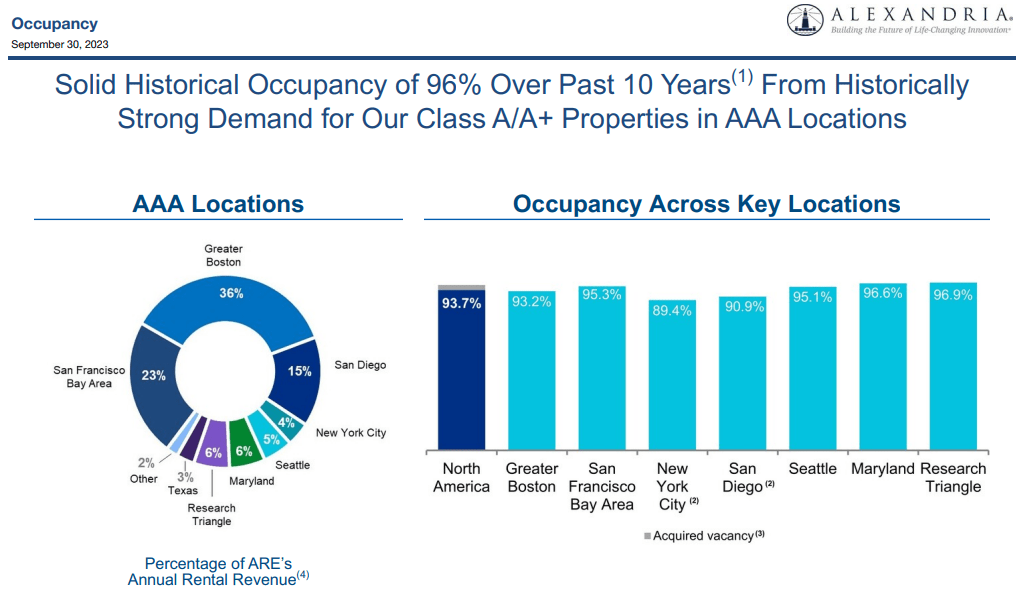

ARE develops life science properties in AAA innovation cluster locations which are primarily located in Boston, New York City, San Francisco, San Diego, Maryland, Seattle, and the Research Triangle.

At the end of the third quarter, ARE’s operating properties had a 93.7% occupancy rate with a weighted average lease term (“WALT”) of approximately 7 years.

{kind=link}

Alexandria is unique as they are the only pure-play life science REIT that is publicly traded.

Some office REITs, including Boston Properties ( BXP ), have recently been adding life science exposure but ARE has a large first mover advantage as they have been developing life science properties since the mid-90’s and have had a long-term relationship with many of the top pharmaceutical and biotech companies in the space.

I believe the recent work-from-home movement has motivated many office REITs to start building or converting existing properties into life science as it is much more insulated from the work-from-home movement.

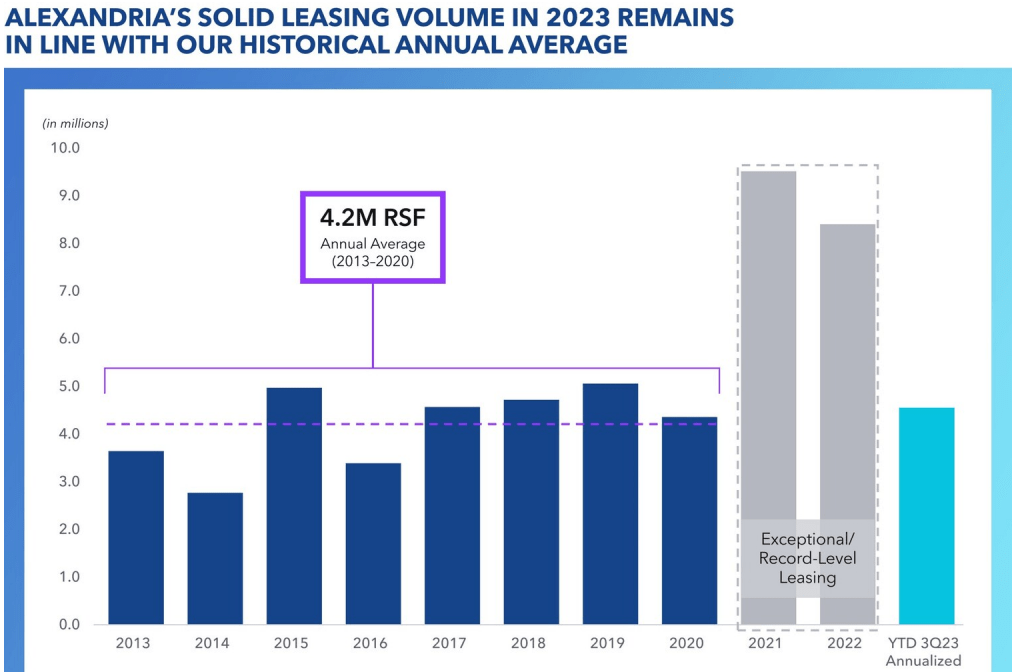

ARE’s resilience to the recent movement shows up in their YTD 3Q23 annualized leasing volume of 4.6 million RSF, which is in-line with their average leasing volume from 2013 to 2020.

Additionally, leases signed during 3Q23 had a WALT of 13.0 years with rental rates increasing 19.7% on a cash basis.

ARE’s third quarter and YTD leasing figures are impressive and not something you would expect to see from a traditional office REIT struggling with occupancy.

{kind=link}

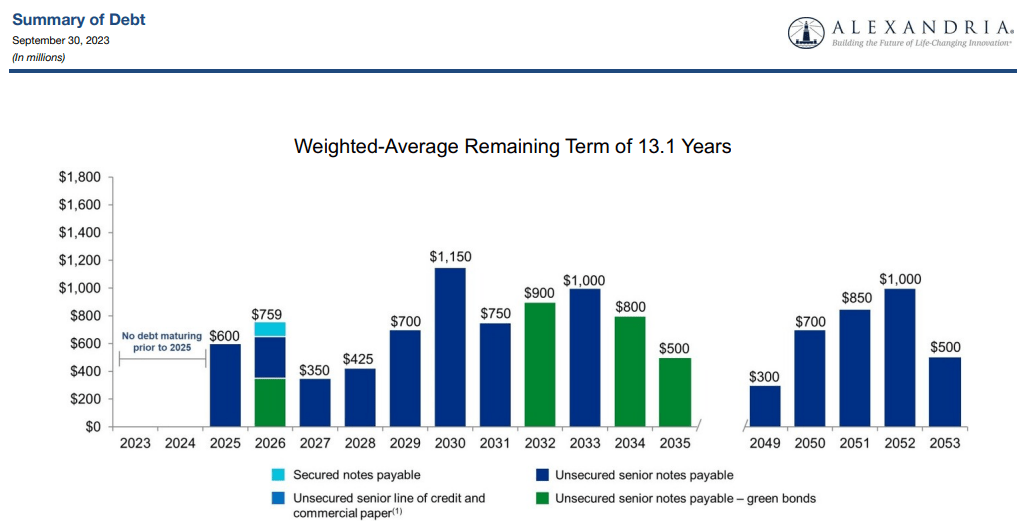

Alexandria has a BBB+ credit rating and one of the strongest balance sheets in the REIT industry with a net debt + preferred stock to adjusted EBITDA of 5.4x, a long-term debt to capital ratio of 39.05%, a total debt and preferred stock to gross assets ratio of 27%, and a fixed charge coverage ratio of 4.8x.

ARE’s debt is 99% fixed rate with a weighted average interest rate of 3.70% and a weighted average term to maturity of 13.1 years.

Plus, at the end of the third quarter, the life science REIT reported significant liquidity of $5.9 billion with no debt maturities prior to 2025.

{kind=link}

I truly believe that life science as an industry will continue to grow far into the future.

People’s desire for life-saving medicine, medical devices, or medicines that alleviate a chronic condition will always be in high demand and there will always be large pharmaceutical companies that need laboratory space to fill that demand.

Alexandria is the only pure-play, publicly traded life science REIT in a fast-growing industry that I believe will continue to grow as medical advances are made.

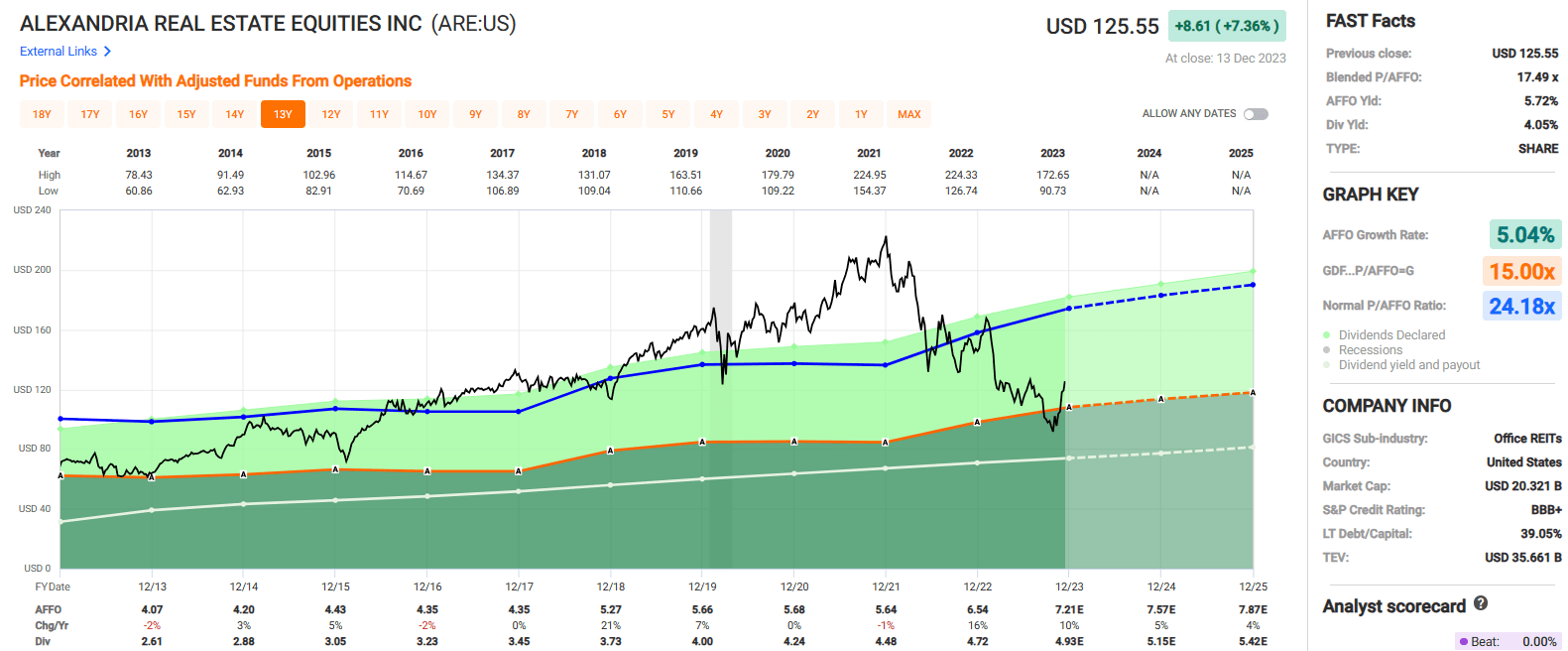

Over the past decade, ARE has had an average adjusted funds from operations (“AFFO”) growth rate of 5.04% and an average dividend growth rate of 8.62%.

The stock pays a 4.05% dividend yield that is well-covered with a 72.17% AFFO payout ratio and trades at a P/AFFO of 17.49x, compared to their 10-year AFFO multiple of 24.18x.

We rate Alexandria Real Estate a Buy.

{kind=link}

Note: ARE is +13% since my last publication (December 10 th ) and also +18% since Land & Building published its short thesis in June 2023.

Seeking Alpha

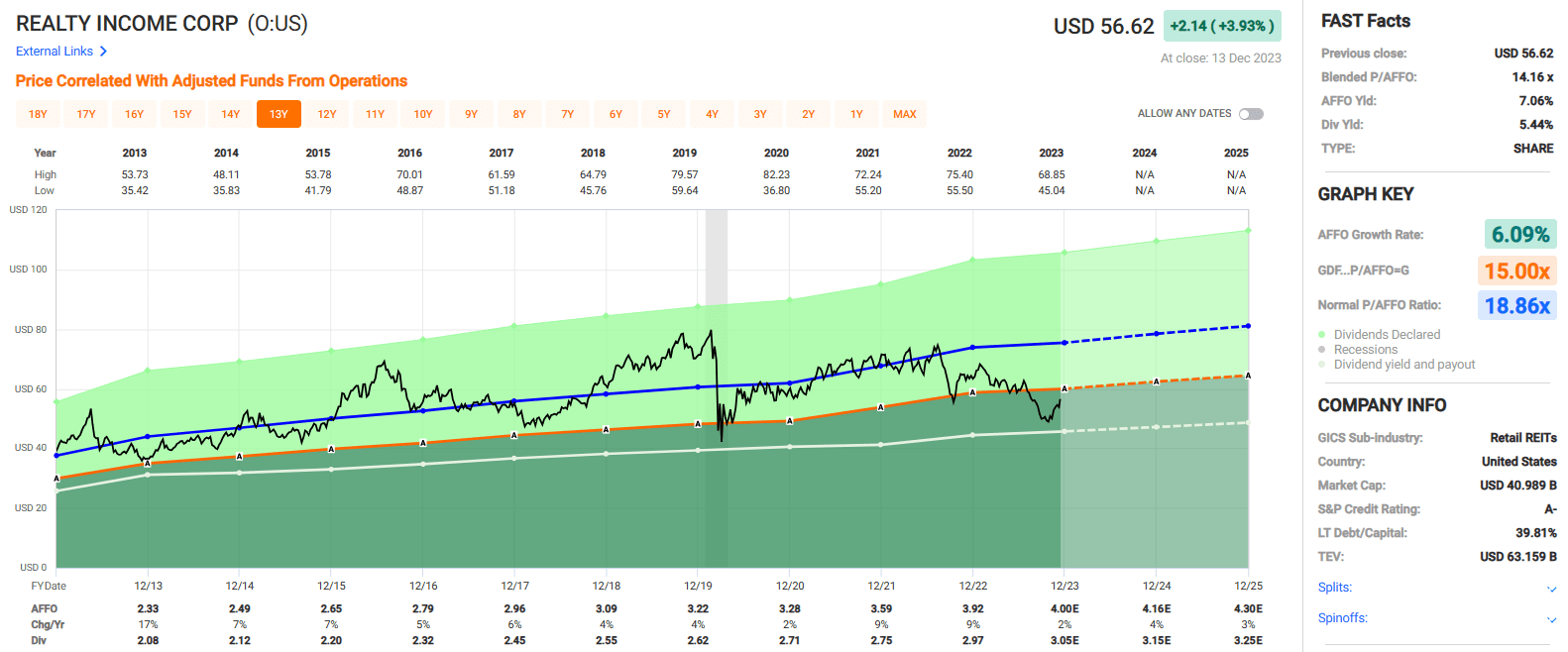

Realty Income ( O )

Realty Income is a net-lease REIT that invests in single-tenant, free-standing commercial properties with a diversified portfolio of retail, industrial, and gaming properties.

Realty Income’s portfolio is primarily made up of retail properties, but industrial makes up approximately 13% (~15% after Spirit merger), and gaming makes up approximately 3% of their total portfolio.

In addition to the properties in its consolidated portfolio, Realty Income recently entered into a joint venture with Digital Realty ( DLR ) for the development of 2 data centers in Northern Virginia which will further expand the diversity of its property types.

Realty Income’s portfolio is comprised of 13,282 commercial properties covering roughly 262.6 million SF of leasable space which are leased to approximately 1,300 tenants on a long-term, triple-net basis.

They have properties located in all 50 U.S. states and have an international presence with properties located in the United Kingdom, Spain, Italy, and Ireland.

At the end of the third quarter, Realty Income reported a portfolio occupancy of 98.8% and a WALT of approximately 9.7 years.

{kind=link}

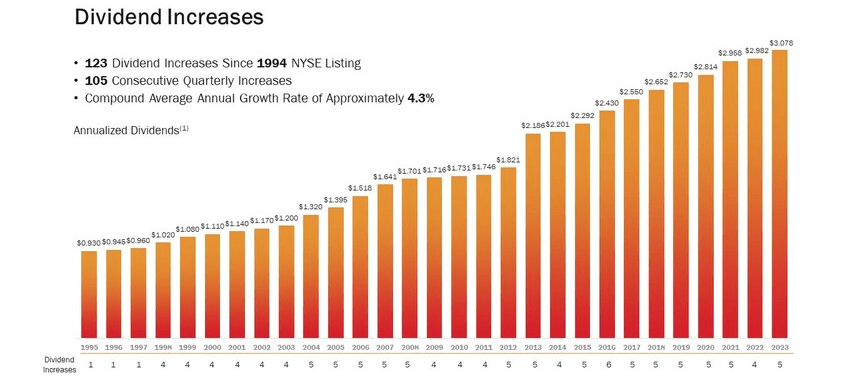

Realty Income is probably best known for its monthly dividend which has been declared for 642 consecutive months throughout the company’s 54-year operating history and increased 123 times since the net-lease REIT went public in 1994.

On December 12, the company announced it increased the monthly dividend from $0.2560 to $0.2565 per share, which when annualized comes to $3.078 per share, representing a 0.2% increase over the annualized dividend paid in the previous year.

While a 0.2% increase might not seem like that much, the company normally increases its dividend each quarter and has done so for 105 consecutive quarters.

Realty Income is a Dividend Aristocrat and has increased its dividend for 29 consecutive years at a compound average annual growth rate of roughly 4.3% since 1994.

{kind=link}

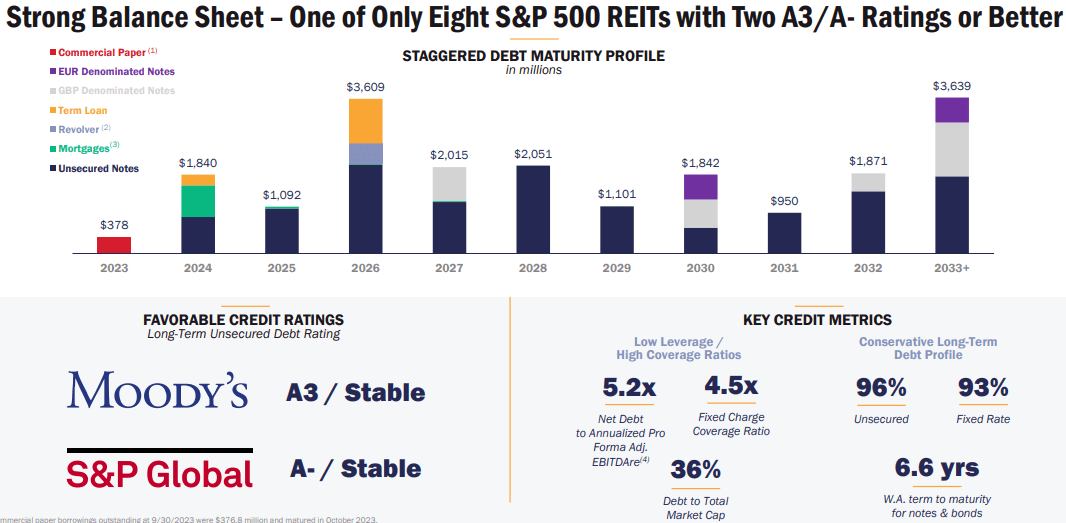

Realty Income has an investment-grade balance sheet with an A- credit rating and solid debt metrics including a net debt to pro forma adjusted EBITDAre of 5.2x, a long-term debt to capital ratio of 39.81%, and a fixed charge coverage ratio of 4.5x.

Their debt is 96% unsecured and 93% fixed rate with a weighted average term to maturity of 6.6 years.

At the end of the third quarter, Realty Income reported approximately $4.5 billion of available liquidity, which includes around $749 million of unsettled forward equity.

{kind=link}

If investors selected stocks solely based on past performance, then I believe Realty Income would be in most people’s portfolio.

The company started operating in 1969 with a single property (Taco Bell) and has since grown to become the largest net-lease REIT with a market cap of approximately $42 billion and more than 13,000 rent checks coming in each month.

Their execution has been stellar, with positive AFFO per share growth in 26 out of the last 27 years and an AFFO median growth rate of 5% since 1996.

Currently, Realty Income pays a 5.44% dividend yield that is well covered with a 75.69% AFFO payout ratio and trades at a P/AFFO of 14.16x, compared to its 10-year average AFFO multiple of 18.86x.

We rate Realty Income a Buy.

{kind=link}

Note: O is +21% since my last article published on November 2023. I’m also working on a compare and contrast article – O vs Agree Realty ( ADC ) this weekend.

Seeking Alpha

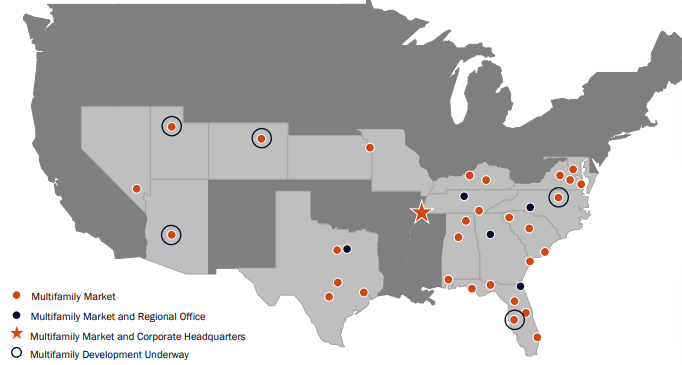

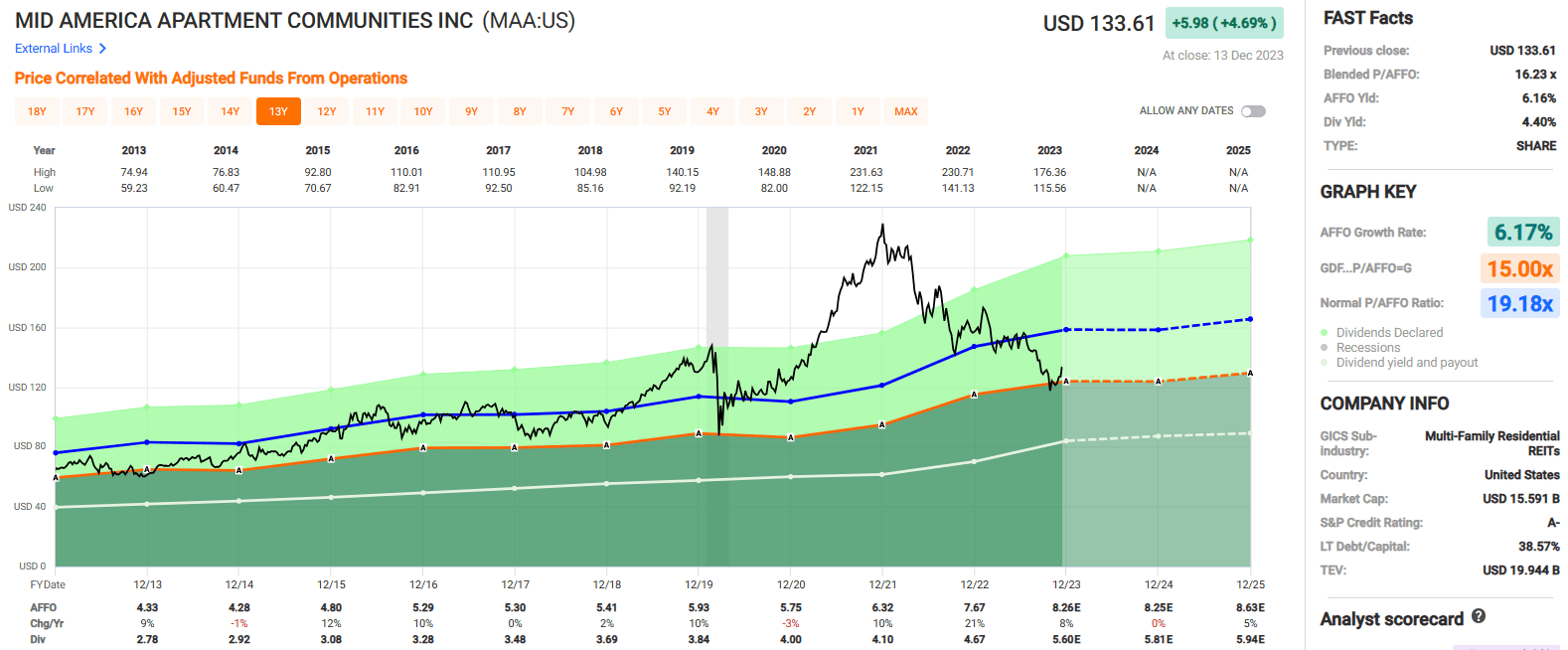

Mid-America Apartment ( MAA )

Mid-America is a Sunbelt-focused multifamily REIT that acquires, selectively develops, and owns or has an ownership interest in multifamily communities spread across the Southeast, Mid-Atlantic, and Southwest regions of the country.

At the end of the third quarter, MAA owned and operated 290 multifamily communities containing approximately 102,000 apartment homes.

In addition to their stabilized properties, MAA also has 5 development communities undergoing construction which are expected to add 1,970 apartment homes once completed.

MAA’s properties are primarily multifamily, but they also have several mixed-use properties with 34 multifamily communities that include a retail component.

MAA has multifamily communities located in 16 states and the District of Columbia and one feature I really like about MAA’s Sunbelt exposure is the heavy concentration in Texas and the Southeast, but no exposure to California residential markets.

{kind=link}

It's hard to overstate MAA’s focus on the Sunbelt as most of their top 10 markets are located in this region.

As a percentage of same-store net operating income (“NOI”), MAA’s largest market is Atlanta, GA which made up 12.7% of their 3Q NOI, followed by Dallas, TX which made up 10.0%, and Tampa, FL which made up 6.9% of their same store NOI during the third quarter.

MAA IR

Mid-America’s apartment communities are diversified by both property class and type.

54% of their portfolio consists of Class A- / B+ properties, 33% consists of Class A+ / A, and 13% of their portfolio consists of Class B / B-.

At 62%, most of MAA’s apartment communities are Garden Style which are 3 stories or less. 34% of their portfolio is made up of mid-rise apartments (4 to 9 stories), and 4% of their portfolio consists of high-rise apartments.

MAA IR

Each company previously discussed in this article has excellent, fortress-like balance sheets, and MAA is no exception.

They are investment-grade with an A- credit rating and have superb debt metrics including a net debt to adjusted EBITDAre of 3.4x, a long-term debt to capital ratio of 38.57%, a total debt to adjusted total assets ratio of 27.3%, and a debt service charge coverage ratio of 7.8x.

Additionally, MAA’s debt is 100% fixed rate with a weighted average interest rate of 3.4% and a weighted average term to maturity of 7.2 years.

{kind=link}

MAA has a time-tested dividend track record and has never suspended or cut its dividend since its IPO in 1994.

MAA has not increased its dividend each year, but it has either maintained or increased its dividend for the last 29 years and has increased its dividend for the last 14 consecutive years.

On December 12, MAA announced its Board approved a quarterly dividend of $1.47 per share, which represents a 5% increase over the rate paid for the comparable period in 2022.

{kind=link}

Over the last decade, MAA has delivered an average AFFO growth rate of 6.17% and an average dividend growth rate of 5.92%.

Analysts expect muted AFFO growth in 2024, but project AFFO per share to increase by 5% in 2025.

When it comes to multifamily residential properties I believe that MAA owns real estate in all the right places. There has been a migration to the Sunbelt region for years and the recent pandemic only served to accelerate that process.

MAA pays a 4.40% dividend yield that is very secure with an AFFO payout ratio of 60.95% and trades at a P/AFFO of 16.23x, compared to its 10-year average AFFO multiple of 19.18x.

We rate Mid-America Apartment a Buy.

{kind=link}

Note: MAA is +12% since my last article published on November 5, 2023.

Seeking Alpha

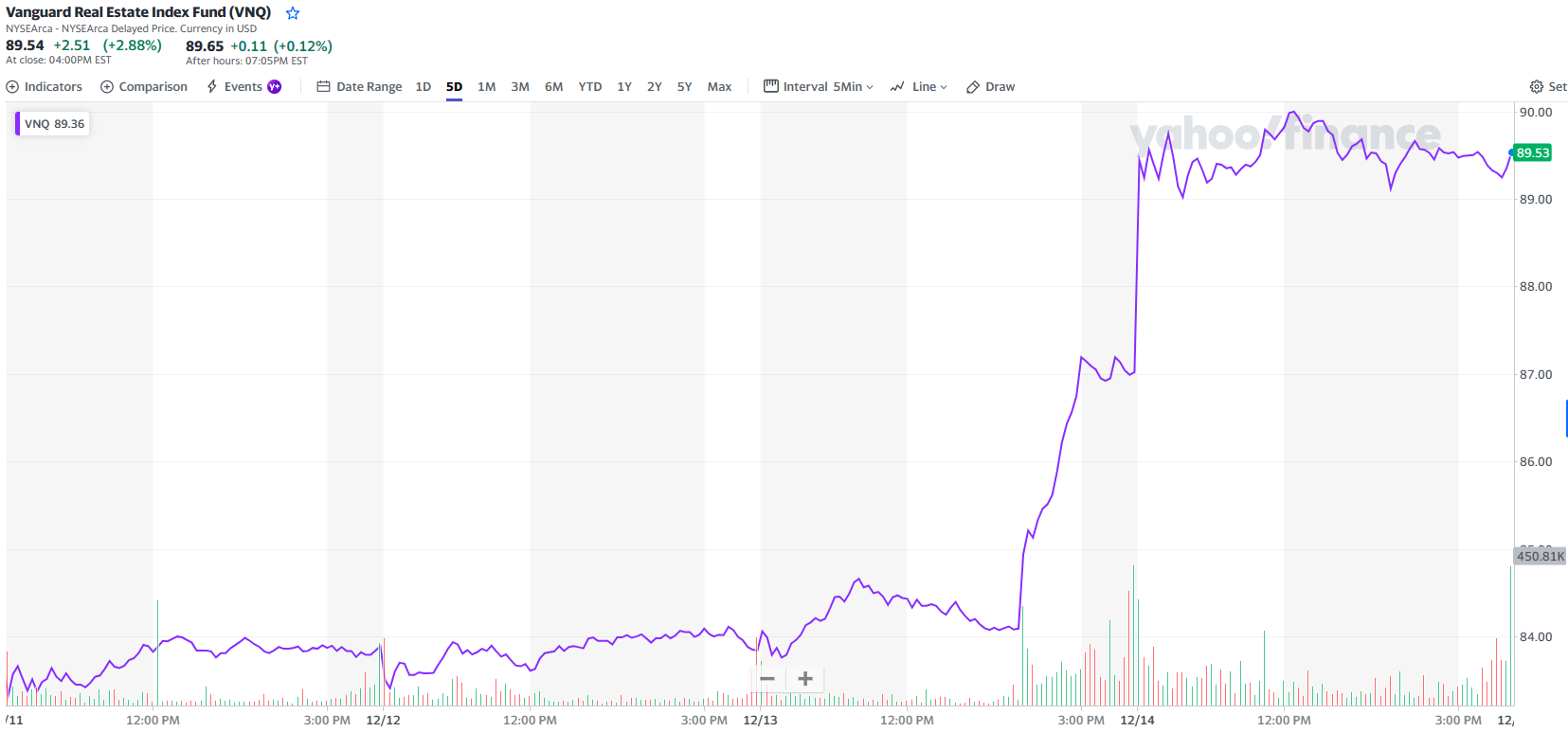

More Rainbows for REITs?

The Federal Reserve’s new "dot plots" imply rates will be cut 75 bps in 2024, then roughly by around 25 bps per quarter through 2025 and 2026 until the long-run neutral level of 2.5% is achieved.

Needless to say, Mr. Market liked the news:

{kind=link}

In case you missed it, I’ve been advocating a REIT rally and most recently wrote :

{kind=link}

I went on to explain:

Seeking Alpha

I believe we’re in the early stages of a REIT rally, and while investing can be difficult and challenging (not all rainbows and butterflies), I’m beginning to see the light at the end of the rainbow.

It’s important to continue to maintain strict discipline and avoid chasing yield .

Remember, I have the benefit of 30 years of investing experience (living through multiple recessions) that includes over $1 billion of deals under my belt.

While the last two years have been challenging, prudent REIT investors should be singing these words with me a year from now:

And wake up where the clouds are far behind me,

Where troubles melt like lemon drops

Away above the chimney tops

That’s where you’ll find me.

Judy Garland, Somewhere Over the Rainbow

Happy SWAN investing!

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

It's Not Always Rainbows And Butterflies