WSR - It's The Perfect Time In The Interest Rate Cycle To Buy REITs

2023-06-08 08:05:00 ET

Summary

- It appears that we are at or near the peak in interest rates for this cycle.

- The main reason most REITs have been pummeled so much is the sharp increase in interest rates.

- We highlight a handful of REITs that should soar if and when interest rates decline.

Co-produced by Austin Rogers

It sounds crazy.

Invest in real estate investment trusts ("REITs") ( VNQ ) right at the peak of interest rates?

We may not even be at the peak yet, in terms of the Federal Reserve's key policy rate on the short end of yield curve. There could be one or a few more rate hikes yet to come.

(We tend to think this would be a mistake that would incrementally raise the risk of something breaking, not just in real estate but in the economy more broadly. But no one from the Fed has reached out to us for our opinion.)

So, why would one choose to invest in REITs now , at or near the peak in the interest rate cycle when the headwinds of rising interest expenses are strongest?

Answer: Because REITs, like all stocks, are forward-looking. The market is always trying to price in the future , not the present or past.

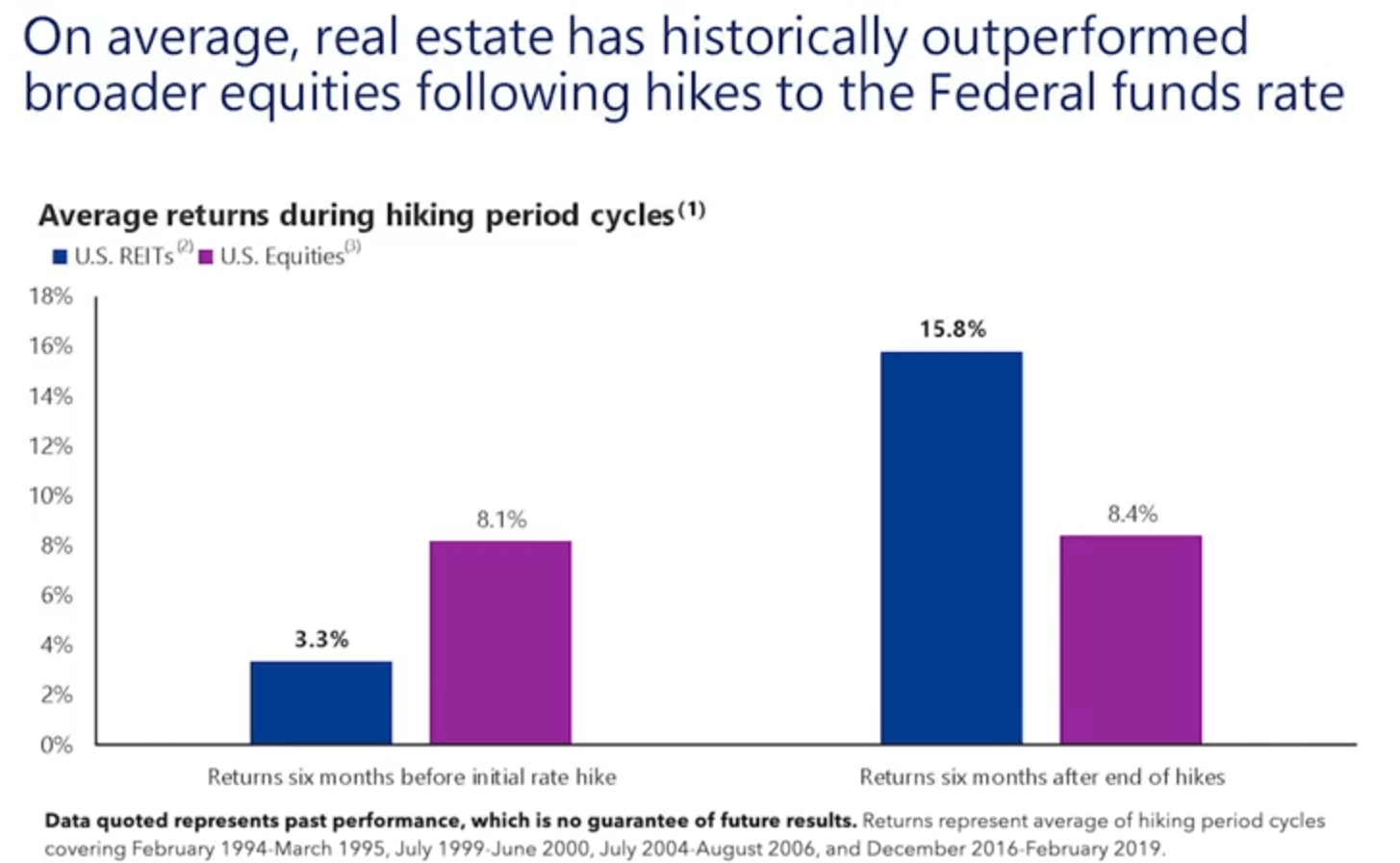

That is why, historically, REITs have underperformed stocks ( SPY ) during the six months leading up to Fed rate hikes, when interest rates are near their lowest point in the cycle, and outperformed during the six months after the end of Fed rate hikes, when interest rates are at or near their highest point in the cycle.

{kind=link}

Today, REITs are ~32% off their all-time high. They have shed around 1/3rd of their value, and many are now valued at, near, or below their COVID-19 lows in terms of price-to-FFO:

REITs have already priced in higher interest expenses and a recession.

Consider this: REITs lost 40% of their value from peak to trough during COVID-19 (although if you blinked, you would've missed the bottom, as REITs quickly rebounded). So, the 32% peak-to-trough decline we've seen in REITs since the beginning of 2022 has mostly priced in a COVID-like black swan event.

But what if we have a recession without a black swan event that is uniquely bad for REITs? What if the widely anticipated upcoming recession doesn't feature a housing market crash (like 2008) or a pandemic (like 2020)?

If that is the case, then the performance of the broad real estate index ( VNQ ) and interest rates will probably look like this example from 2018-2019:

Notice that REITs broke above their ceiling in early 2019 and soared to a new all time-high during the year. The catalyst? Falling interest rates.

The economy was weakening, but there was no black swan event or crash. Meanwhile, the elevated interest rates made REITs a coiled spring, waiting to be released by falling interest rates. And when interest rates did fall, REITs soared.

We think the current market is set up for just such a REIT resurgence in the second half of 2023 and into 2024. It wouldn't require interest rates to fall all the way back to their COVID-era lows. It would just require some relief from the upward trajectory in rates.

Let's take a look at a few REITs that we think have huge upside in a falling interest rate scenario.

BSR REIT ( OTCPK:BSRTF , HOM.U)

BSR is a multifamily REIT that owns Class B apartment complexes located almost entirely in the suburbs of Texas. The landlord is over 40% off its high from early 2022.

BSR REIT

So what is fundamentally wrong with BSR?

Answer: Absolutely nothing.

Consider this. In Q1 2023, BSR reported:

- AFFO per share growth of 10%

- Weighted average rent growth of 10%

- Lease renewal rent growth of 7.7%

- Same-property NOI growth of 17.8%

- Occupancy of ~96%

- Debt to gross book value of 36%

And yet, BSR's stock is priced at around 60% of net asset value.

To be clear, BSR does face some challenges. The population influx over the past few years has attracted a lot of attention from developers, so completions of new multifamily communities should be elevated for the next few years. This should cause rent growth to slow. And BSR is primarily listed on the Toronto Stock Exchange, also available over-the-counter as BSRTF, which limits the shareholder base to some degree.

Other than that, BSR mainly looks weighed down by elevated interest rates. If interest rates come down, BSR will almost certainly go up and just to recover to its NAV per share, it would need to rise by over 70% . While you wait, for the upside, you earn a 4% dividend yield .

Global Medical REIT ( GMRE )

GMRE owns net leased medical office buildings and hospitals across the country. The "net lease" part refers to terms in the lease contract that obligate the tenant to pay for all or most property taxes, insurance, and maintenance, which gives GMRE strong margins and consistent cash flow.

Moreover, these healthcare properties, leased overwhelmingly to health systems or their affiliates, are highly defensive and recession-resistant in nature.

So why has GMRE shed over 50% of its value from its all-time high?

Global Medical REIT

{kind=link}

In a word? Debt. GMRE's debt to EBITDA ratio is somewhat high at 6.6x, and around 20% of its debt is floating rate (most of which is hedged). In Q1, interest expenses surged 72% YoY.

The good news is that GMRE has no debt maturities until June 2024, and the hedges in place put fixed rates on most of the floating debt for years into the future.

If and when interest rates decline, GMRE's cost of capital should come down considerably, allowing the REIT to continue its acquisitive growth spree. CEO Jeffrey Busch commented in the Q1 2023 earnings release :

With ample liquidity and continued dialogue with the seller community, we believe we are well-positioned to ramp up our acquisition activity when cap rate spreads return to an attractive level and markets normalize.

Such a drop in interest rates would likely trigger a rapid recovery in its share price, resulting in up to 100% upside potential just to return to where it was prior to the crash, and you earn a 9.5% dividend yield while you wait.

Whitestone REIT ( WSR )

WSR is a retail REIT that owns high-quality shopping centers in five Sunbelt markets: Phoenix, Houston, Dallas/Fort Worth, San Antonio, and Austin. Last year, WSR's occupancy increased to a record high as FFO per share surged by double-digits. In Q1 2023, the momentum continued with straight-line rent growth of ~21% on a blended basis (new and renewal leases), while same-store NOI growth came in at a solid 2.8%.

And yet WSR is down over 35% from its 2022 high.

Whitestone REIT

What's the problem? Again, debt. WSR's net debt to EBITDA ratio is 7.8x, and there are a few more debt maturities coming this year and in 2024.

The good news is that the vast majority of WSR's debt does not mature until after 2026, and management is confident in their ability to get the crucial net leverage ratio to the low 7x range by the end of the year. Moreover, though interest costs are going up this year, so are revenue and NOI as high tenant demand translates into rent growth.

What happens if and when rates come down from here? Investor sentiment about WSR flips, and the stock soars. We estimate that the stock is today priced at a 40% discount to its NAV so the upside potential could be up to 70% and you earn a near 6% dividend yield while you wait.

Bottom Line

We don't have a crystal ball. We are not saying we know where interest rates will be at any given date. What we are saying is:

- A recession later this year looks highly likely

- Recessions have an unblemished track record of causing interest rates to drop

- Lower interest rates should reverse REITs' underperformance and cause some in particular to soar

Investing isn't about certainty. It's about understanding probabilities and allocating capital in a way that puts them in your favor.

Today, with interest rates seemingly near their peak (at least for this cycle), certain REITs look like fantastic buying opportunities.

For further details see:

It's The Perfect Time In The Interest Rate Cycle To Buy REITs