ITUB - Itaú Unibanco: Ahead Of Brazilian Private Banks With Resilient Q2 Performance

2023-08-11 01:43:28 ET

Summary

- Itaú's Q2 results showcase resilience and consistency amid challenging economic conditions and credit market shifts.

- Despite service revenue and credit costs challenges, Itaú maintains an optimistic outlook with efficient credit quality management.

- Itaú's attractive valuation multiples and consistent performance make it a standout in the Brazilian private banking sector.

Brazil's private bank, Itaú Unibanco ( ITUB ), recently unveiled its second-quarter results, which, despite revealing specific challenges and setbacks, highlighted a consistent pattern and positioned the bank ahead of its primary private competitors, Santander Brasil ( BSBR ) and Bradesco ( BBD ).

While the bank's net profit figures remained robust, it did adjust its service revenue outlook due to a sluggish start in the investment banking sector this year – a move that was not unexpected.

During Q2, the Brazilian economy witnessed a year-over-year deceleration in credit growth. Brazil's National Financial System has encountered elevated delinquency rates, although these have displayed signs of stabilizing in recent months. Furthermore, delinquencies in revolving credit have been on the rise.

Banco Central do Brasil

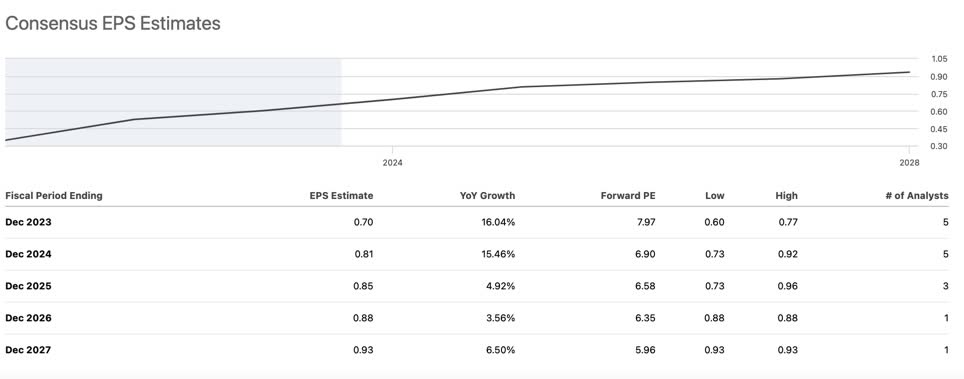

However, these downward revisions are not anticipated to significantly impact the implied Itaú's profit projections, expected to drive a 16% increase in earnings per share [EPS] this year.

{kind=link}

Despite facing challenges like the bank's credit portfolio contraction due to forex issues, the bank would have exhibited a slightly positive growth trajectory, particularly considering Brazil's adverse credit conditions.

On a positive note, Itaú's credit quality management has progressively improved, positioning the bank near its annual credit cost projections and distinguishing it from its primary private domestic competitors.

Furthermore, Itaú has undergone an institutional transformation in its approach, shifting towards a long-term focus on client-centric rather than product-centric transactions. This shift aims to enhance offerings for strategic clients and selected customers who contribute higher value.

Considering Itaú's numerous strengths, particularly in comparison to private peers such as Itaú and Santander, I foresee the bank effectively navigating the complex macroeconomic environment. Its steady performance shows its capability to deliver results consistently. Also, its attractively low valuation multiples compared to its private peers in Brazil further bolsters the optimistic outlook.

Q2 Results

Amid a complex economic landscape, Itaú's recent Q2 earnings results have offered a glimpse of remarkable consistency, although not entirely devoid of minor challenges.

These outcomes highlight the bank's ability to stand resilient in the face of a juxtaposition of high default rates and a decline in credit within the Brazilian market. This scenario, characterized by two significant challenges, makes Itaú's demonstrated consistency even more noteworthy, as it manages to weather the storm and maintain its stability.

Strengths: treasury, capital, and funding.

Itaú reported a net interest income [NII] of R$26 billion, indicating a quarter-over-quarter (QoQ) growth of 5.3% and a year-on-year (YoY) increase of 14.8%. Both components, NII from Clients and NII from the Market, exhibited favorable results. Notably, NII from the Market stood out, reaching R$1.1 billion, marking a remarkable 65.9% QoQ surge and a substantial 64.6% YoY growth. This enhancement is attributed to gains achieved in asset and liability management, alongside the returns from foreign investments.

The Margin with Clients [NII] reached R$25 billion, displaying a QoQ rise of 3.7% and a YoY growth of 3.4%, surpassing the portfolio's growth rate. Factors contributing to this performance encompassed a slight 0.1 percentage point (p.p.) QoQ improvement in the spread, elevating it to 8.8%. Additional contributors included a higher average credit volume and increased business days during the quarter.

Itaú's management expressed contentment with the current NII level, albeit acknowledging a slight shift in the mix.

Two critical impacts on this year's NII performance have been identified. Firstly, the average portfolio balance prevents a comprehensive overview due to the ongoing influence of higher average ratios even as the portfolio contracts. Secondly, the latter half of the year is expected to see increased volume within the context of declining interest rates.

Furthermore, Itaú holds a promising pipeline in the wholesale segment, which has the potential to bolster operational economics and subsequently benefit the NII.

Another highlight was that Itaú had maintained a solid Common Equity Tier 1 (CET1) capital – the bank's strongest capital category – and an impressive Basel ratio, registering 13.6% and 15.1%, respectively, with a YoY increase of over 1 percentage point. Anticipating regulatory adjustments from 3Q23 onward, Itaú's management projects the CET1 to reach 14.7%, enhancing the prospects of an increased payout for 2023. However, due to heightened operational risk requirements, the industry foresees regulatory tightening on the capital adequacy ratio in 2025. Itaú's current payout is 16%, with a 46% average over the past decade.

In addition, client funding exhibited a robust YoY growth of 17.4% and a 2% increase compared to the previous quarter. This growth was propelled by funds from promissory notes and structured operations certificates, which saw a substantial expansion of 57.9% YoY.

Notably, funds under management reached R$2.4 trillion, representing an 11% YoY increase. This growth primarily stems from proprietary products and the open platform.

Struggles: services revenue, cost of credit, and delinquencies

On the downside, though not excessively so, Itaú's service and insurance figures prompted a revision of its annual growth guidance from 7.5% to 10.5%, down to a range of 5% to 7%. The combined revenue from services and insurance amounted to R$12.4 billion, marking a 4% YoY increase.

Service revenues exhibited a subdued performance, with a modest YoY growth of only 1.3% and a marginal QoQ increase of 0.2%. Credit and debit card revenues remained flat compared to the previous quarter due to a 3% QoQ drop in issuance numbers. This shift can be attributed to pricing strategies or efforts to address higher acquiring expenses resulting from a commission rate hike.

Revenues from current account services experienced a decline of 3% in both QoQ and YoY, reflecting fee reductions and reduced performance-based fee earnings. In contrast, insurance revenues performed well, reaching R$2.08 billion and achieving a solid 2.9% QoQ growth and a significant 17.5% YoY increase. This success can be attributed to earned premiums and equity income.

Turning to credit costs and bad debt, despite maintaining the guided range of R$36.5 billion to R$40.5 billion, the results demonstrated a 3.9% QoQ increase and a notable 25% YoY rise. This was primarily driven by higher expenses related to bad debt provisions [ALL] which expanded by 6.7% QoQ and 23.0% YoY.

Itaú's wholesale business segment primarily influenced the quarter's ALL expenses in Brazil due to the normalization of provisioning flows in this sector. Over the year, the most substantial impact continued to emanate from the retail business segment in Brazil.

Delinquencies surpassing 90 days (NPL 90) exhibited a slight QoQ increase of 0.1 percentage points and a YoY uptick of 0.3 percentage points, reaching 3.0%. This quarterly expansion is particularly notable in Brazil's portfolio of micro, small, and medium-sized enterprises, particularly those with lower turnovers. The coverage ratio remained stable QoQ at 212% but deteriorated by 6 percentage points YoY. Notably, this performance outperforms Bradesco and Santander, whose coverage ratios were eroded this quarter.

Setback: loan portfolio

Considering that a contraction in credit for banks had been anticipated for the second quarter, as indicated by the Brazilian Central Bank, the performance of Itaú's loan portfolio could be somewhat less favorable.

The bank reported that its portfolio amounted to R$897.2 billion, representing a 1.7% decline compared to the previous quarter. The expanded portfolio reached R$1.15 trillion, marking a marginal 0.1% YoY decrease, with the reduction influenced by currency exchange rate fluctuations. Within this context, the Individual portfolio's growth rate continued decelerating, showing a mere 0.7% QoQ increase. The 1.5% QoQ drop in credit card-related activities was a noteworthy negative.

The Company's portfolio experienced a negative pull, significantly impacted by currency exchange rate fluctuations, resulting in a 1.7% QoQ contraction and a 0.6% YoY decrease. Additionally, while contributing to a lesser extent, the Latin America portfolio contributed to the portfolio's contraction, declining by 6.2% QoQ.

Still ahead of its peers

Despite encountering negative aspects in its results, Itaú outperformed its fellow private peers in Brazil. A closer examination of leading indicators reveals Itaú's superior position, even in a scenario characterized by tighter credit availability and higher default rates. Notably, Itaú's exceptional efficiency is highlighted, evident in its Return on Equity [ROE], which is nearly twice as high as its peers, Bradesco and Santander Brasil.

| Loan Portfolio (R$ bi) |

| Loan Portfolio Growth (YoY) |

| Gross Margins (R$ bi) |

| Delinquency Rate |

| Expanded ALL (R$ bi) |

| Coverage Ratio |

| ROE |

| CET1 |

| Basel |

| Itaú Unibanco |

| 1152 |

| 6.2% |

| 25.9 |

| 3% |

| -9.6 |

| 212% |

| 20.93% |

| 13.7% |

| 15.1% |

| Bradesco |

| 868.7 |

| 1.6% |

| 16.5 |

| 6.5% |

| -10.3 |

| 164% |

| 11.4% |

| 12.4% |

| 12.9% |

| Santander Brasil |

| 499.5 |

| 6.6% |

| 13.5 |

| 3.3% |

| -5.98 |

| 214% |

| 11.2% |

| 11.7% |

| 13.5% |

Notably, given valuation multiples, Itaú trades at a discount compared to its two primary peers. Its forward Price-to-Earnings (P/E) ratio stands at 7.7x, contrasting with Santander Brasil's 9.6x and Bradesco's 8.9x. The consensus projection further suggests that Itaú's multiple is anticipated to remain below 6x from 2024 onwards.

Regarding the Price-to-Book (P/B) ratio, Itaú positions itself between Santander Brasil and Bradesco. One plausible explanation for Itaú having a higher P/B ratio than Bradesco is the greater confidence investors have in the quality of Itaú's assets, particularly its substantial customer base, which is expected to lead to higher value generation.

The bottom line

Itaú's latest results weren't sensational but demonstrated consistency despite specific blemishes within a challenging landscape characterized by high delinquency rates and reduced credit in Brazil.

While the banking sector faces a challenging scenario, Itaú has consistently outperformed its domestic private peers, trading at attractive valuation multiples in direct comparison.

Itaú's high efficiency further reinforces its position as the top Brazilian private bank among its peers. As a result, I maintain a bullish stance on its future profit growth prospects and the resumption of credit portfolio expansion.

For further details see:

Itaú Unibanco: Ahead Of Brazilian Private Banks With Resilient Q2 Performance