ITUB - Itaú Unibanco: Bullish With Multiple Growth Tailwinds Into 2024

2023-11-07 21:42:47 ET

Summary

- Itaú Unibanco's Q3 earnings were highlighted by solid growth.

- An ongoing digital transformation of the bank as a broader theme across Latin America is driving cost efficiencies and supporting margins.

- We see shares climbing higher through 2024 alongside a new credit growth cycle as regional Central Banks begin to cut interest rates.

Itaú Unibanco Holding SA ( ITUB ) reported its latest quarterly results highlighted by solid growth despite a challenging macro backdrop. Brazil's largest private sector bank with a major presence across Latin America has benefited from an ongoing digital transformation with more customers banking online, driving cost efficiencies and supporting margins.

Indeed, ITUB is up 30% this year, outperforming Brazil stocks and global Financials sector benchmarks. We've covered it previously and like the stock now with an expectation that the bank's operational momentum can continue amid several favorable economic developments in the region. An outlook for easing inflation in Brazil and lower interest rates should be positive for ITUB into 2024.

ITUB Earnings Recap

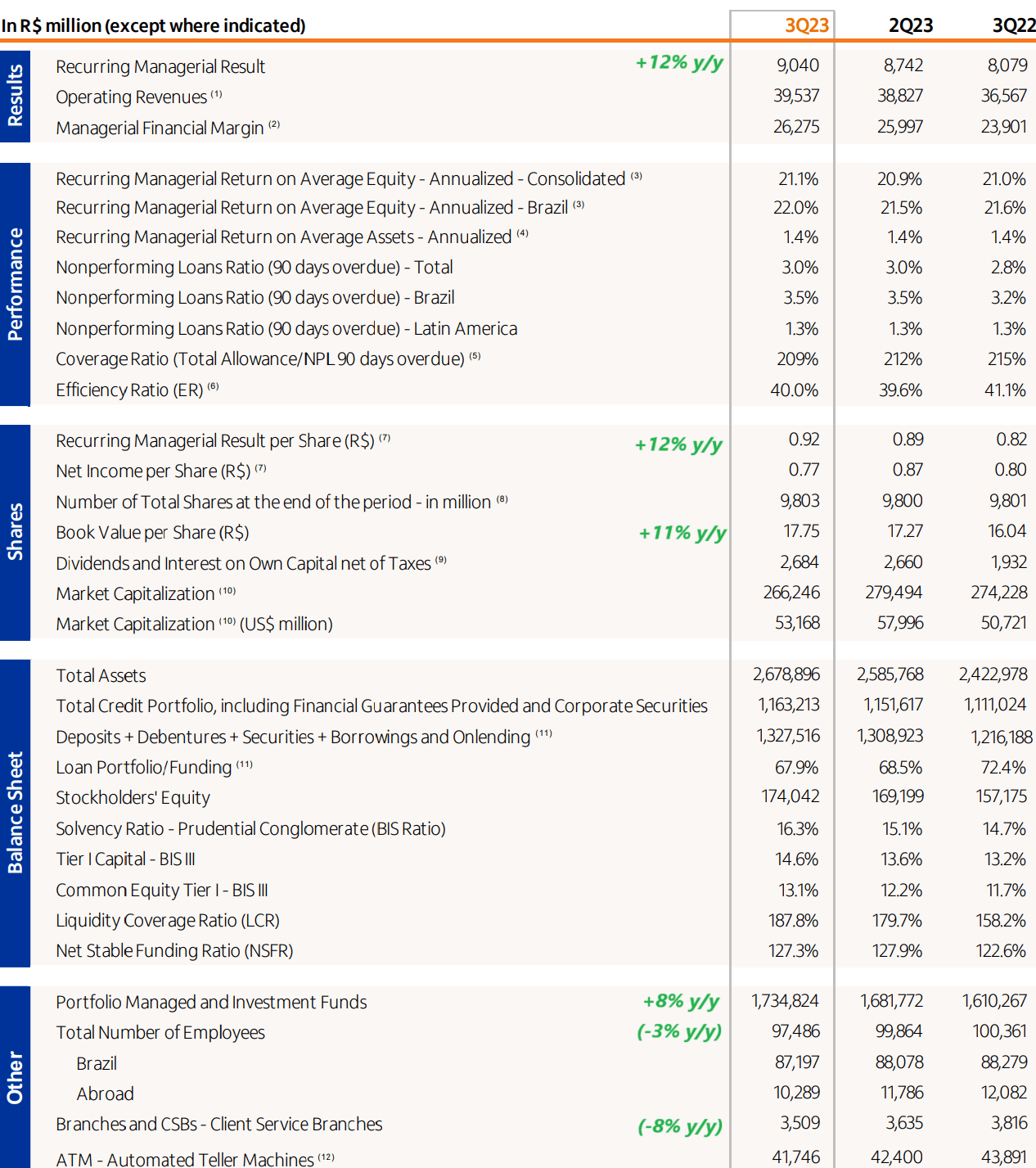

Itau reported adjusted "managerial" Q3 EPS of BRL 0.92 per share, up 12% year-over-year. This was driven by an 8% increase in operating revenues capturing higher interest margins alongside a modest 1% increase in the consolidated loan portfolio between stronger trends on the corporate side against softer trends in individual credit.

The setup here considers what has been higher interest rates, not only in Brazil where operations represent more than 90% of the loan portfolio, but also as a broader theme in Latin America. Chile, for example, has been one area of weakness with Itau citing more volatile financial conditions in the country. Still, credit quality has been stable with 90 days overdue non-performing loans at around 3%.

Even as the firm-wide cost of credit climbed driven by a higher provision for loan losses, the bigger takeaway here is the success of controlling operational expenses. The annualized adjusted return on average equity at 21.1% ticked higher from 20.9% in Q2 and is even stronger looking at the Brazil business specifically reaching 22%.

{kind=link}

That effort in terms of cost discipline is evident by a -3% reduction in the total number of employees while the number of physical client service branches is down by -8% y/y.

A large part of that, as mentioned, is the more structural trend of individuals banking online, reducing the need for historically capital-intensive retail logistics. At the same time, the number of total portfolios managed and investment funds has reached 1.7 million, highlighting the relative strength on the side of private banking and asset management.

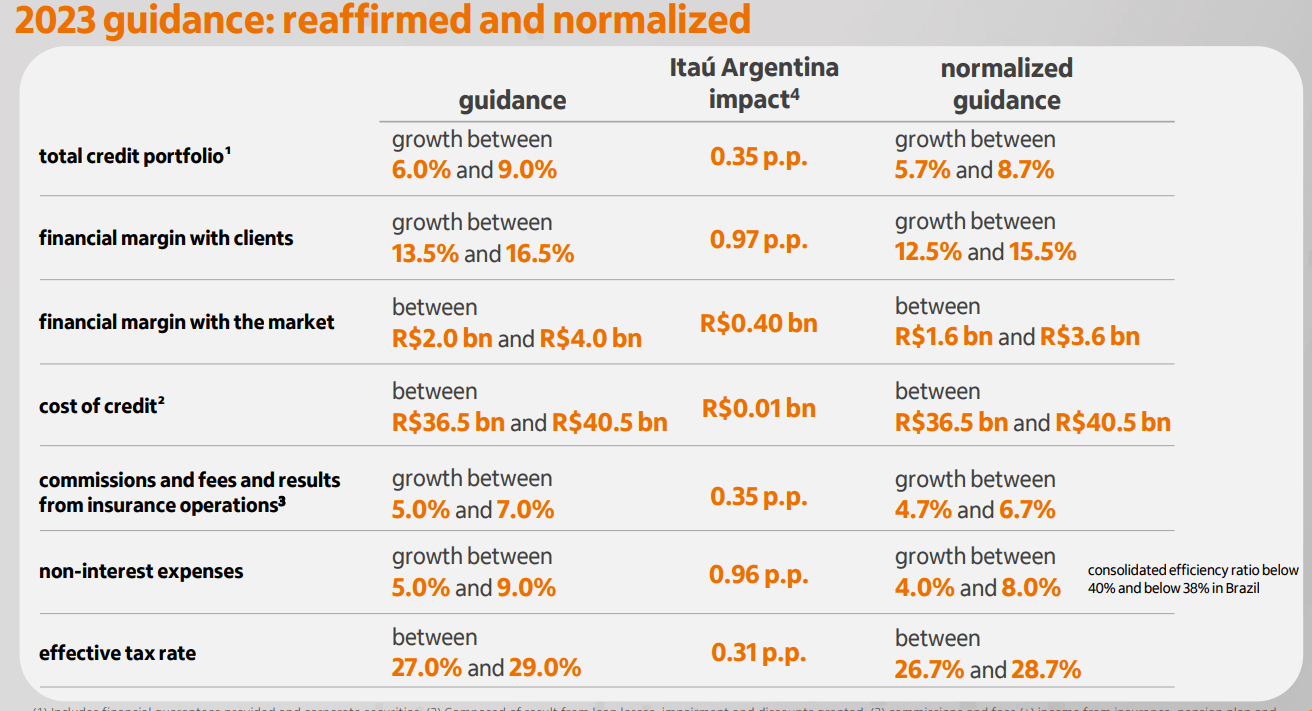

For guidance, the company is expecting total credit portfolio growth between 5.7% and 8.7% for the full year 2023, excluding the divestment of operations in Argentina with the bank selling its local subsidiary this year. The forecast of a 12.5% to 15.5% increase in financial margin with clients this year reflects the combination of higher loan rates.

{kind=link}

What's Next For ITUB?

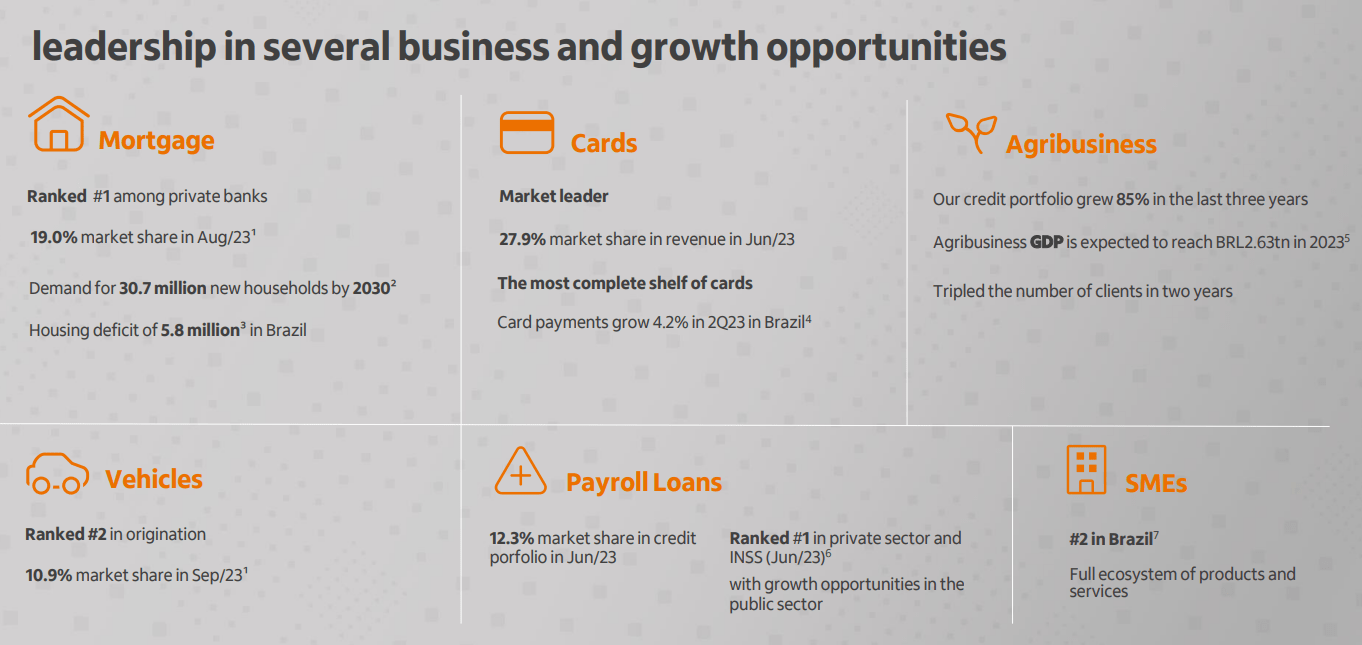

The attraction of ITUB for us comes down to its leadership position in several key market segments between mortgages, credit cards, and even payroll loans with a number one share in Brazil. Even with the emergence of "FinTech" players like Nu Holdings ( NU ) or PagSeguro Digital Ltd. ( PAGS ), which have made waves by offering free checking accounts and mobile wallets, the strength in Itau comes down to its presence in these core traditional segments.

Itau management notes that there is a significant housing deficit in Brazil with upwards of 31 million new demand by households through 2030 as a tailwind for its mortgage lending market share. Similarly, agribusiness has been booming in Brazil where Itau is seeing gains to its loan portfolio where the number of clients has tripled in the past two years.

{kind=link}

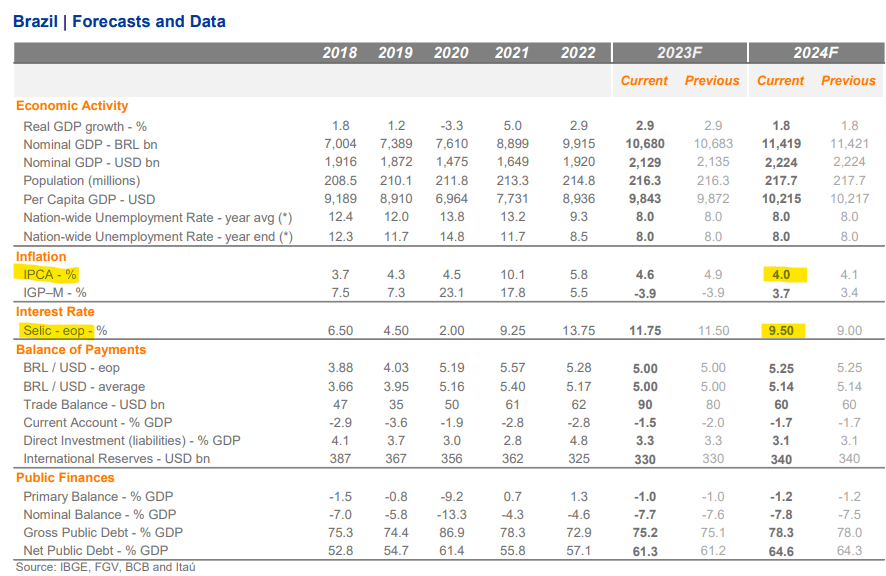

We bring all this up because the expectation is for a new credit growth cycle in Brazil. Compared to a cycle peak inflation rate in Brazil above 12% in late 2021, the local consumer price index ((IPCA)) is down to 5.2% which has provided the Central Bank some flexibility to cut rates.

Itau's economics research group is forecasting the benchmark SELIC interest rate to fall towards 9.5% by next year compared to the current level of 12.5% . We believe this effort at loosening financial conditions in the country should translate into a boost for growth and earnings to Itau overall.

source: Itau Economics Research

{kind=link}

The other side to the discussion would be the overall more favorable global macro backdrop. Easing inflation in developed markets, including stabilizing interest rates in the U.S. could be supportive to emerging markets and even Brazil's currency. Ultimately, we believe ITUB is well-positioned to outperform market expectations and lead higher with upside to earnings.

In terms of valuation, we note that ITUB at an 8x forward P/E is trading at a discount to its historical average earnings multiple above 10x. Similarly, there is also a modest spread to its current price to book value at 1.6x compared to 1.9x. The bullish case is that there is some room for multiple expansions as sentiment and macro conditions improve.

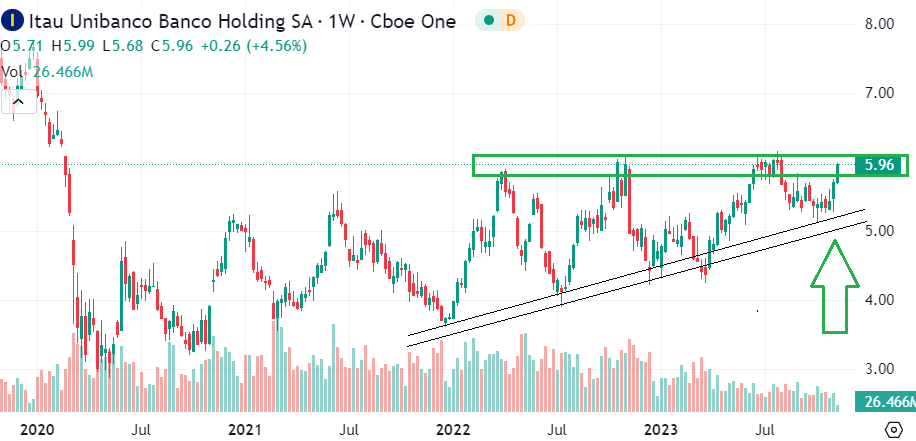

From the stock price chart, we're eyeing an emerging breakout in ITUB towards the highest levels since 2019. Beyond what we view as solid fundamentals, bullish momentum has some room to carry the stock higher over the next several months.

{kind=link}

Final Thoughts

Itau Unibanco is a high-quality foreign bank that maintains a positive long-term outlook. The latest Q3 earnings demonstrated an impressive sense of operational and financial resiliency. We like the setup in the stock and expect shares to generate positive returns over the long run.

The risks here to consider go back to the company's emerging markets profile including FX risk and historically wider swings of volatility. A scenario where economic conditions deteriorate, or higher levels of financial markets stress globally would open the door for a deeper selloff. The possibility of weaker-than-expected macro trends in Brazil or disappointing financial results into 2024 would force a reassessment of our positive outlook.

For further details see:

Itaú Unibanco: Bullish With Multiple Growth Tailwinds Into 2024