RACE - Ithaka Group Q1 2023 IES Commentary

2023-10-27 01:16:00 ET

Summary

- The Ithaka Group is an independent investment boutique that specializes in managing high-quality, concentrated growth equity portfolios.

- The first quarter of 2023 saw the MSCI EAFE get off to its best start in four years, and second-best start in the last ten years.

- The top contributors to the strategy's performance were LVMH, BayCurrent Consulting, and Straumann Group, while the top detractors were Crayon Group, Eurofins, and EQT.

- We sold one company, Sofina, and added three new companies to the EAFE Strategy: Accenture, Hermès, and Ferrari.

{kind=link}

Summary

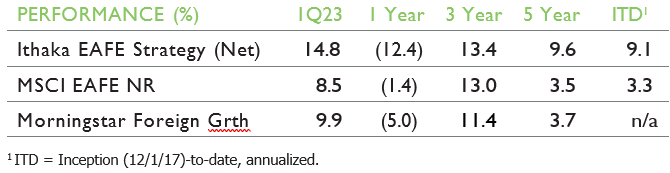

The Ithaka EAFE Strategy (“IES”) gained 14.8% in 1Q23, beating the MSCI EAFE NR (the net return MSCI EAFE index, or “EAFE”) by 6.3 ppts. Turnover for the trailing twelve months was 6%.

{kind=link}

Comment

No less than Warren Buffett and Jack Bogle have insisted that volatility does not equal risk. As managers of a fund that is relatively volatile month-to-month, but comprises high quality companies with low chances of business failure within our investment horizon, we are sympathetic to this view.

Yet, we understand that volatility is a risk. Not Risk, but A risk. It’s a risk because investors are human (for now at least). No matter how much one knows about a company…. or a fund…. there is always much that one doesn’t and can’t know. Thus an investor can be forgiven for less-than-steely conviction as a holding experiences a handful of months in a year with drawdowns of greater than 10%, even if it also experiences a handful of months with surges of greater than 10%.

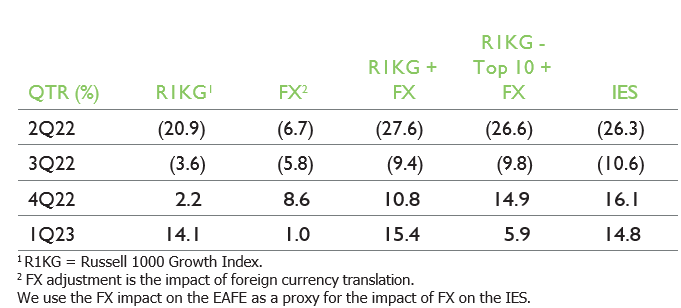

We’ve discussed in the past how the Ithaka EAFE Strategy was created to deliver performance that is closer to that of the high- performing Russell 1000 Growth (“R1KG”) index than it is to the relatively anemic MSCI EAFE index. In fact the correlation of the quarterly performance of the IES and the Russell 1000 Growth, with and without the top 10 holdings, is quite high (R2 = ~90%) over the last five years when adjusted for the foreign exchange effect of investing US dollars overseas.

{kind=link}

One might expect that a fund with performance characteristics similar to those of the Russell 1000 Growth would experience similar volatility. And that is the case. But just as the performance of a foreign portfolio is impacted by currency fluctuations, so

is the volatility. As with performance, sometimes the impact is dampening, and sometimes it’s amplifying. In our experience, the net effect over time is always amplifying. The annualized standard deviation of the monthly returns of the R1KG over the last five years was 20.8%. Adding the impact of currency volatility (as if the R1KG were denominated in the same basket of currencies as the EAFE), the standard deviation of an FX-

adjusted R1KG over the last five years would have been 24.3%. The standard deviation for the IES over the last five years has been…. 24.0%.

While this helps us understand the volatility—and hopefully understanding can boost conviction for our investors—it doesn’t mean it’s something that we will just accept as a necessary tradeoff for our otherwise strong performance. For a given return, less volatility is better. Just as for a given volatility, greater return is better. So as we think about improving as investors over the next five years, we do so with this framework in mind, with the goal of maintaining outstanding relative performance over time, but mitigating some of the additional volatility that comes with investing overseas.

Developed International Markets

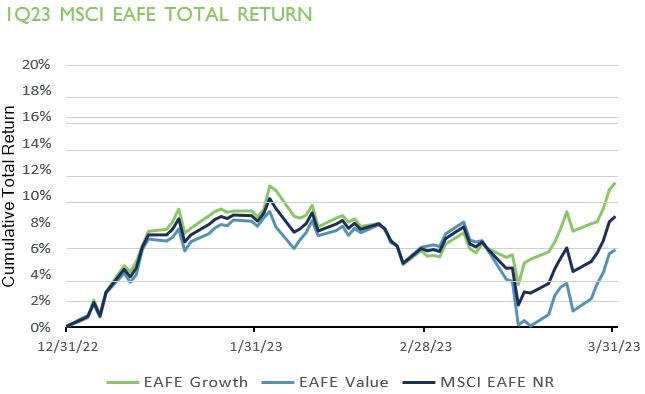

The first quarter of 2023 saw the MSCI EAFE get off to its best start in four years, and second best start in the last ten years. Better-than-expected economic data and hopes that interest rates could be close to peaking sent global equities up sharply in January. Turmoil in the banking sector, including the failure of two regional lenders in the US and the forced sale of an unhealthy Credit Suisse in Europe, sent markets down again

in mid-March. Growth pulled away from value during this banking crisis, as financials comprise more than a quarter of the value weighting vs only ~8% of the growth weighting of the EAFE index. Global markets rallied to end the quarter, as the immediate banking crisis resolved and reassuring inflation signals fed expectations the hiking cycle could shortly come to an end.

{kind=link}

IES 1Q23 Performance

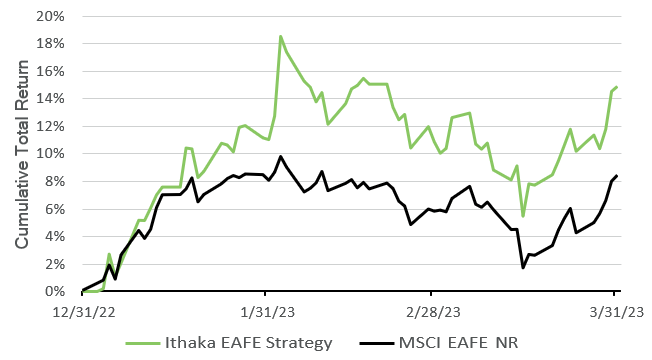

The Ithaka EAFE Strategy gained 14.8% for the quarter, outperforming the MSCI EAFE by 6.3 ppts. The IES was ahead of the benchmark for all but the first few days of the quarter.

{kind=link}

With few exceptions, which we consider temporary, our companies continue to perform well fundamentally. All but three holdings—two private equity firms and a freight forwarder— continue to experience year-over-year revenue growth, the median of which was 18% for the most recent period reported. All of the companies held in the IES have strong balance sheets.

Top Contributors

LVMH (LVMHF). LVMH is a French luxury goods conglomerate that manages many well-known and prestigious brands across the retail spectrum, including Louis Vuitton, Fendi, Moët & Chandon, and Sephora. The strength of the various brands in LVMH’s portfolio provides a high barrier to entry and allows for pricing power and related high margins. High-end luxury continues to perform well in this challenging market. Anticipation of China’s post-COVID reopening propelled luxury shares in the first quarter.

BayCurrent Consulting (BYCRF). BayCurrent Consulting is a Tokyo-based consulting firm that focuses on digital transformation. Japan has a large pool of cash-rich corporations that lag their global peers in digital modernization. Continued strong recruiting of recent graduates and more experienced consultants, along with an increase in revenue per consultant, led to revenue and operating profit growth of greater than 30% year-over-year. BayCurrent is well-positioned to help facilitate Japan’s digital transformation over the coming years.

Straumann Group ( SAUHF ). Straumann is a global leader in aesthetic dentistry, with leading positions in dental implant systems and other preventive and corrective dentistry applications, such as clear aligners. Align Technology’s strong results released in early February indicated that the cyclical headwind impacting largely unreimbursed cosmetic dental procedures might be ending.

Subsequent strong earnings and guidance from Straumann supported this view.

Top Detractors

Crayon Group ( CRAYF ). Crayon Group is a global IT consultant based in Oslo. Its flagship software asset management offering helps customers reduce software expenditure, delivering a return of up to 30x for every dollar spent. Crayon’s other area of growth has been in digital transformation, from helping clients migrate their IT infrastructure to the cloud to helping clients with strategies in artificial intelligence, big data, and cybersecurity. While revenue growth has shown continued strength, the relatively new management team has struggled with expense and capital management. We are being patient with this otherwise high quality company, for the moment.

Eurofins (ERFSF). Luxembourg-based Eurofins Scientific is a global leader in lab testing for food, drug, clinical diagnostics, and other markets. After 18 months of benefiting from a surge in COVID-related testing, Eurofins is facing difficult comparables.

Additionally, margins have been impacted by inflation-related cost increases. We continue to like Eurofins' long-term prospects. Eurofins is well-positioned to continue benefiting from growing demand for lab testing services. The company has a strong presence in key markets around the world and a diverse range of testing capabilities that allow it to serve a wide range of industries. Eurofins’ ongoing investments in technology and infrastructure should also help to drive long-term growth and profitability.

EQT ( EQT ). EQT is a Stockholm-based private equity firm with two main business segments, roughly equal in size: private capital and real assets. Funds in both private capital and real assets have been posting industry-leading returns, generally in the range of 19% to 23%. Industry-leading performance has led to industry-leading AUM growth. As with other publicly-traded private equity firms, EQT shares were caught in the backdraft of the March banking crisis. EQT’s exposure to the crisis is limited to portfolio holdings in its Ventures and Life Sciences segments that banked with Silicon Valley Bank. These represent less than 5% of AUM.

Transactions

We sold one company, Sofina ( SFNXF ), and added three new companies to the EAFE Strategy: Accenture ( ACN ), Hermès ( HESAY ), and Ferrari ( RACE ).

Portfolio Sales

Sofina has struggled since we added it as a holding a year ago, which was a mistake in retrospect, certainly in timing but also in fit for this portfolio. The company initially struggled due to the long duration of its portfolio in a rising rate environment.

Though we purchased it after a significant decline, the decline was not over. More recently, shares struggled due to the collapse of Silicon Valley Bank and the potential exposure of direct and indirect (through VC fund investments) portfolio companies. We sold due to a combination of the holding’s low market capitalization, high volatility, and prospect of significant downward valuations of its holdings.

Portfolio Additions

Accenture is the largest IT consulting firm globally. As the IT services consulting branch of accounting firm Arthur Andersen, the predecessor group helped install the first commercially- available mainframe computer at General Electric’s Appliance Park in Louisville in 1952. A few years later Andersen designed and installed a system for Bank of America that became the backbone for BankAmericard, which was later renamed Visa.

Over the course of the next 30 years, Andersen professionalized the idea of technology consulting. In 2001 Andersen Consulting officially split from sibling Arthur Andersen and rebranded as Accenture, created from the phrase “accent on the future.” Riding the secular trends of digital transformation and outsourcing, Accenture has grown into one of the largest private employers in the world. We expect these drivers to continue, and for Accenture to continue to be a beneficiary.

Established in 1837 by Thierry Hermès, Hermès initially manufactured horse bridles and harnesses for French nobility. The advent of the automobile forced Hermès to diversify beyond equine accessories. After seeing a “close-all” opening and closing system on the hood of a military car in America, 3rd generation Hermès leader Emile Hermès secured the rights to use this technology on leather goods and clothing. Thus the zipper came to be used on many of the Hermès’s bags and jackets, including a leather jacket made for the Duke of Windsor. In subsequent decades Hermès expanded into silk scarves and ties. It is perhaps best known today for its two iconic handbags, the Kelly and the Birkin, which start at ~$10,000 but can be quite a bit more expensive than that. Now under the 6th generation of family leadership, Hermès is among the most prestigious luxury brands globally. We believe that the highest levels of luxury goods will continue to benefit from high demand with the continuing increase of wealthy households globally.

Ferrari is one of the most iconic luxury sports car manufacturers in the world. The company was founded in 1939 by Enzo Ferrari, who had previously worked as a racecar driver and team manager for Alfa Romeo. Enzo’s passion for racing and his drive to create the perfect car led to the formation of Ferrari, whose history is intertwined with that of Formula 1 racing, where Ferrari is the winningest team of all time. Over the last six decades, Ferrari has parlayed its success in racing to become one of the most elite luxury brands globally. As with Hermès, Ferrari will continue to grow with the growth of the number ultra-high-net worth individuals. Also like Hermès, Ferrari has mastered the multiple paradoxes of managing ultra high-end luxury brands, such as innovating while protecting brand heritage, and growing while protecting exclusivity.

Risk Disclosure

Past performance is not indicative of future results. The performance shown is for the Ithaka EAFE Strategy Composite. All fully discretionary taxable and non- taxable accounts are added to the composite following the first quarter in which their ending market values equal or exceed $0.1 million. Results of individual accounts may vary from the composite depending on account size, timing of transactions and market conditions prevailing at the time of the transaction. The gross-of-fee performance does not reflect the payment of management fees and other expenses that are incurred in the management of an account. The net- of-fee performance includes the payment of such fees and expenses and may include fee estimates for clients who pay in arrears. Gross-of-fee performance and net-of-fee performance both include the reinvestment of all distributions, dividends and other income.

The performance shown is compared to the MSCI EAFE NR Index and the median of Morningstar’s Foreign Large Growth fund category. The MSCI EAFE NR Index measures the performance of the large- and mid-cap equities from 21 developed market countries not including the United States. This broad-based securities index is unmanaged and is not subject to fees and expenses typically associated with managed accounts. Foreign Large Growth is a formal category of mutual funds that Morningstar defines as portfolios that focus on high-priced growth stocks, mainly outside of the United States. Individuals cannot invest directly in an index or fund category.

The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed do not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment

recommendations or decisions Ithaka makes in the future will be profitable or will equal the investment performance of the securities discussed herein. Investing in securities entails risk and may result in loss of principal.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Ithaka Group Q1 2023 IES Commentary