CPKPF - Itochu: Macro Headwinds To Hit Consumer Sectors Low Dividend Yield

2023-10-20 18:13:13 ET

Summary

- Itochu has underperformed its peers over the last 12 months. High exposure to consumer sectors will dampen growth prospects for the medium-term.

- We believe a new medium-term plan will focus on continued group reorganization, and increasing dividend payouts.

- With decelerating growth and limited firepower to raise the dividend yield, we downgrade from a buy to a neutral rating.

Investment thesis

We downgrade Itochu ( ITOCY ) from a buy to a neutral rating. We believe a new medium-term plan will target increasing shareholder returns but with a slowing earnings trajectory from macro headwinds and limited firepower to boost dividends, there is no incentive to buy the shares today.

Quick primer

Itochu is one of the top five Japanese trading companies with its roots dating back to 1858. Initially operating in the textile industry, Itochu has focused more on non-resource businesses such as food and technology compared to peers Mitsubishi Corp. ( OTCPK:MSBHF ) and Mitsui & Co. ( OTCPK:MITSY ). It has an effective 10% stake in Chinese financial services firm CITIC Limited ( OTCPK:CTPCF ) and a 25% stake in C.P. Pokphand Co. Ltd ( OTCPK:CPKPY ) ( OTCPK:CPKPF ), a material group company of Thailand's Charoen Pokphand Group.

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

{kind=link}

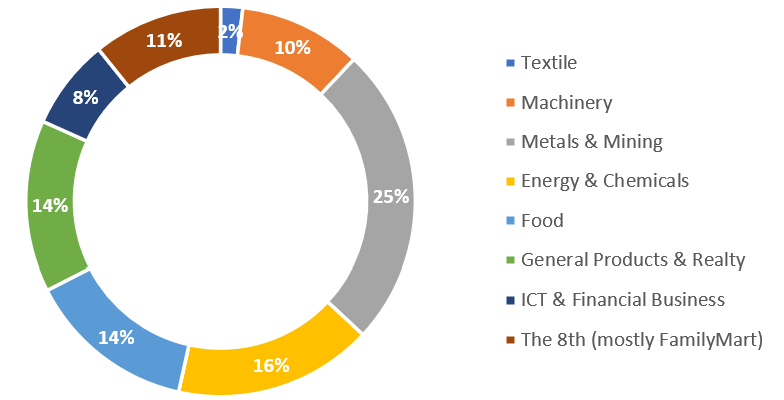

Sales split by segment - Q1 FY3/2024 results

Sales split by segment - Q1 FY3/2024 results (Company)

{kind=link}

Updating our view

We are updating our buy rating from November 2022 , based on strong business execution despite limited exposure to natural resources, and increasing its dividend payout. Whilst the shares have risen, Itochu has continued to underperform its peers with its more diversified business model. On a YTD basis, we see that Mitsubishi ((MSBHF)) and Mitsui ((MITSY)) have outperformed, with major exposure to oil and gas.

Recently, Itochu has been focused on group reorganization focused on its ICT business segment. It sold its mobile phone retail chain CONEXIO to Nojima ( NJMLF ) in December 2022, it is making its IT services subsidiary Itochu Techno-Solutions ( ITTOY ) a 100% subsidiary and is acquiring 100% of associate company Daiken ( DAICF ). Itochu's strategic rationale appears to be strengthening its existing business portfolio, as opposed to making major changes or expansions.

With the global economy impacted by increasing geopolitical risk, the short-term impact has been increasing commodity prices, with business and consumer confidence both remaining sluggish in the face of increasing costs. With Itochu's high focus on consumer sectors such as textiles, food, and retail, we have some concerns over the outlook for the next 12-18 months.

We want to assess whether 1) Itochu's business model allows for risk mitigation in a slowing global economy, and 2) the outlook for improving shareholder returns.

Consumer sector exposure will be hard to manage

Whilst natural resources can see major swings in pricing, activities in the consumer sector tend to be more stable and predictable. However, with the combination of the rise in the cost of living and increasing financing costs from mortgages to credit card borrowing, we believe consumer spending will weaken into FY3/2025. We expect to see a negative impact on Itochu's textile, food, general products, realty (building and construction materials), and pressure on the convenience store business. Itochu's exposure is higher for staples as opposed to discretionary goods, but we believe there will still be some negative impact.

Its limited exposure to natural resources is focused on iron ore and coal, where prices have normalized post-pandemic. In Energy & Chemicals, we have concerns over slowing industrial activity, as well as the slowdown in EV demand in China impacting lithium-ion battery exposure.

The company commented that in Q1 FY3/2024 the 'global economy generally remained stagnant' ( page 4 ). As we do not anticipate a recovery trend, we believe upside earnings risk is significantly limited.

New medium-term plan to be announced

With the current medium-term plan ending in FY3/2024, the company is expected to unveil new targets which should include a progressive policy towards increasing shareholder returns. The FY3/2024 dividend forecast of JPY160 per share is at a historic high, based on an approximate 30% payout ratio. FY3/2024 company guidance is viewed as being conservative.

With the global business outlook set to face headwinds, we believe that the company will focus on addressing the following in its new plan: 1) continued portfolio management and 2) increasing the dividend payout ratio. We believe more capital will be deployed towards making key group companies 100% owned subsidiaries, thereby gaining more strategic control. It may also dispose of further unwanted assets which will streamline operations. With an already diversified business and management's conservative stance over allocating capital to 'high-risk and high-return' ventures such as natural resources, we believe the company will focus on increasing the dividend payout ratio to reach 50% over the next three years; anything above is unrealistic given the company's tendency to avoid dividend cuts. Itochu's ROE is above 15%, the highest in its peer group and management will want to maintain this position as a way of demonstrating management's effectiveness and shareholder friendliness by allocating more of its reserves. All its peers currently have a steady 30% payout ratio.

Focusing capital allocation on group reorganization and dividends can also indicate that there may be limitations over where capital can be put to work. Increased costs will mean that previously viable projects will either have economically lower returns or will need a longer payback timeframe - Itochu management is viewed as conservative and is unlikely to invest where potential benefits do not make the grade.

Valuations

On consensus forecasts, the shares are trading on PER FY3/2025 9.3x on flat growth YoY, with a dividend yield of 3.3%. Whilst we believe the dividend payout will increase, an implied 50% payout would yield 5.4%. However, we do not believe Itochu has the ability to provide a dividend yield above 5% in the short term. On a slowing earnings trajectory, we believe there is no need to buy the shares.

Thesis catalysts

The company will outline its policy of increasing the dividend payout ratio towards 50% by FY3/2027; although a positive step, investors today will have limited incentive to buy, particularly in a high-interest rate environment.

Risks to the thesis

The medium-term plan targets major earnings growth, as well as increasing shareholder returns. Aggressive growth plans will be viewed as a positive surprise.

Conclusion

In hindsight, we believe our buy rating was a miss since it would have been more prudent to be overweight in Mitsubishi or Mitsui as opposed to Itochu over the last 12 months. With increasing geopolitical risk, oil and gas prices are on the rise which provides no benefit for Itochu, whilst business risk increases overall. With slowing growth and limited firepower to increase shareholder returns, we downgrade to a neutral rating.

For further details see:

Itochu: Macro Headwinds To Hit Consumer Sectors, Low Dividend Yield