ITOT - ITOT: Still Uncertain

2023-12-07 10:55:17 ET

Summary

- The iShares Core S&P Total U.S. Stock Market ETF is a more diversified version of the iShares Core S&P 500 ETF.

- Performance has been strong due to the belief that the economy is slowing and inflation will decrease.

- The labour market is an important indicator for inflation, but not all the labour market data is in yet. We want to see unemployment rates.

- Loosening labour markets doesn't mean that employees won't index their wage increases at a minimum to inflation expectations, which likely remain above target.

- We think there's a good chance that inflation is going to be stickier, and it will dawn on markets that some hurt is going to be needed to fight inflation.

The iShares Core S&P Total U.S. Stock Market ETF ( ITOT ) is a more diversified version of the iShares Core S&P 500 ETF ( IVV ) with more than five times the number of holdings. The sectoral allocations are almost identical, so its fortunes will be that of the broad indices.

Performance has been strong after October on the impression that the economy is slowing, indicated for the moment by the jobs data, and that inflation should be on the way down right in time so that the economy doesn't have to go through a recession. We think that there is still the possibility that the economy slows with underlying inflation not coming down. We think the next CPI figures will only include commodity deflation, but the high levels of employment mean that the inflation wheel, that's built on expectations and habit, will not stop turning without a recession.

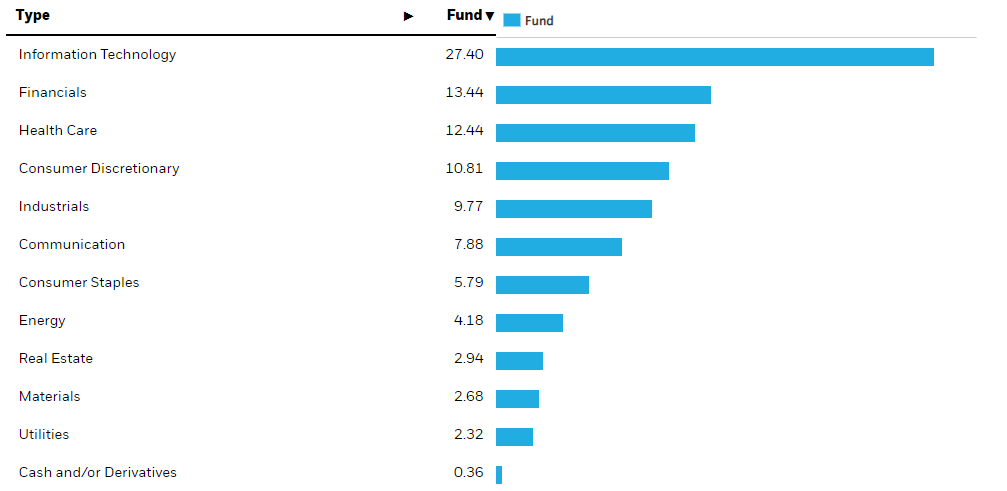

ITOT Breakdown

ITOT is value weighted , but compared to the IVV has more diverse exposure. So the tilt is slightly skewed out towards smaller cap issues and the industries those issues typically belong to.

{kind=link}

Sectors (iShares.com)

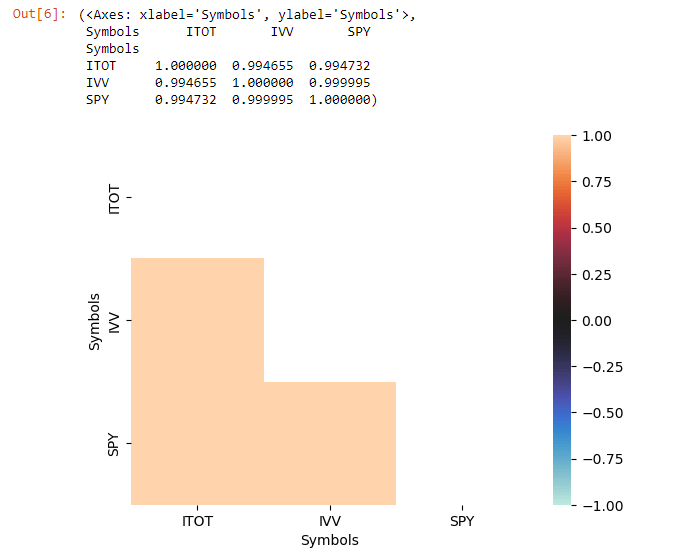

The weightings of the megacaps are slightly lower than in the S&P 500 ( SPY ) trackers like IVV, but ultimately the exposures are super similar, and they are almost perfectly correlated.

{kind=link}

Correlation (VTS)

ITOT's expense ratios are 0.03% same as the 0.03% for the IVV.

Macro Considerations

We already have some jobs data from this month. Next week will be the CPI data which is going to be more important now since we need to see that a cooling jobs market actually translates into an inflation decrease.

The JOLTS data showed us that demand for workers is in the process of being exhausted, with job openings falling, while total separations from jobs remained constant.

It's worth noting that total separations includes retirement, which means people who are leaving the workforce permanently. Since retirement rates are in general on the up due to demographics, this means that a steady total separations rate might be signaling more reticence to quit and more employee concerns about the future availability of jobs. Of course, more retirement also means a smaller workforce, as is inevitable with the demographic situation which is a little inflationary - but the short term feeling seems to be that workers are possibly more concerned about their jobs than before which is positive to reduce upward pressure in wage negotiations.

Labour tightness is on the way down which is quite good, and the markets have acknowledged this information, but possibly ignoring other dimensions and bidding the market up prematurely.

While the labour market is an important leading indicator to underlying inflation because of the wage-price spiral, ultimately the relationship between inflation and the labour market should be through employment rates. The baseline for wage negotiation dynamics are going to be expectations about inflation. Increases in wages in excess of that will be linked to labour tightness, but on an underlying basis, unless people are getting a bit desperate with unemployment increasing, wages are going to have to go up in line with what people believe prices are going to go up. Unemployment rate data comes out Friday, and we think the employment levels should stay the same because there is still a lot of demand for labour. As a consequence, we also think that outside of the effects of lower oil prices, inflation should start demonstrating stickiness.

Bottom Line

We don't think markets are prepared for the eventuality that inflation ends up being stickier than expected, even in the face of falling labour tightness, which doesn't necessarily translate into unemployment. We think there needs to be unemployment to bring down inflation, which includes more recessionary signals.

In Europe inflation has come down more readily as labour markets had been much looser throughout, with no great resignation event, outside of the UK at least. Also, the EU tends to be more savings oriented and money velocity is probably not as high as in the US. Money velocity in the US remains very high .

There is another issue, which is that the belief in a soft landing actually makes a soft landing less likely, since that belief loosens credit conditions and therefore undermines the Fed's efforts in fighting inflation. Eagerness in the US markets are a concerning signal.

In all, with prices approaching former highs, we think broad market bets are unwise at the moment.

For further details see:

ITOT: Still Uncertain