TDY - Itron: Too Much Uncertainty For Me

Summary

- Itron continues to struggle from a sales and cash flow perspective.

- On top of this, shares of the company look anything but cheap and could even be described as expensive.

- The market seems to be paying more attention to growing backlog, but even with that good news, there is too much uncertainty to make me comfortable.

In the eyes of the market, what matters most about a company can vary from firm to firm. Oftentimes, the most recent data provided that shows what the picture was like in the prior quarter or prior year can have a huge impact on how the market values a firm. But in other cases, that recent data can be discarded entirely if the market believes that leading indicators are indicative of a brighter future. One interesting case where this applies can be seen by looking at Itron ( ITRI ).

For those not familiar with the firm, it describes itself as an industrial IoT (Internet of Things) play that focuses on deploying smart networks, software, services, devices, sensors, and data analytics for its customers. It focuses on smart grid and distribution automation for smart street lighting, traffic management, air quality monitoring, electrical vehicle charging, and more. In recent years, the firm has struggled from a revenue and profit perspective. That pain extends through the most recent quarter for which the data is provided. Even so, market participants are willing to reward the company because of some rather positive leading indicators. But until we actually see what fruit that bears, I believe investors should take a more cautious approach to the enterprise.

Recent performance has been ignored

The last article that I wrote about Itron was published in February 2022. In that article, I described how the company had struggled from a fundamental perspective over the prior few years. Some of that pain came from the COVID-19 pandemic. But some of it even preceded the pandemic. At that time, from a cash flow perspective, shares of the company looked cheap compared to similar firms. And at the end of the day, I felt as though the long-term outlook for the company would probably be fine. But because of the pain the company was experiencing, I ultimately concluded that it made for a better 'hold' prospect than anything else. Since then, the company has exceeded my expectations. While the S&P 500 has dropped 9.5%, shares of Itron have seen an upside of 2.4%.

{kind=link}

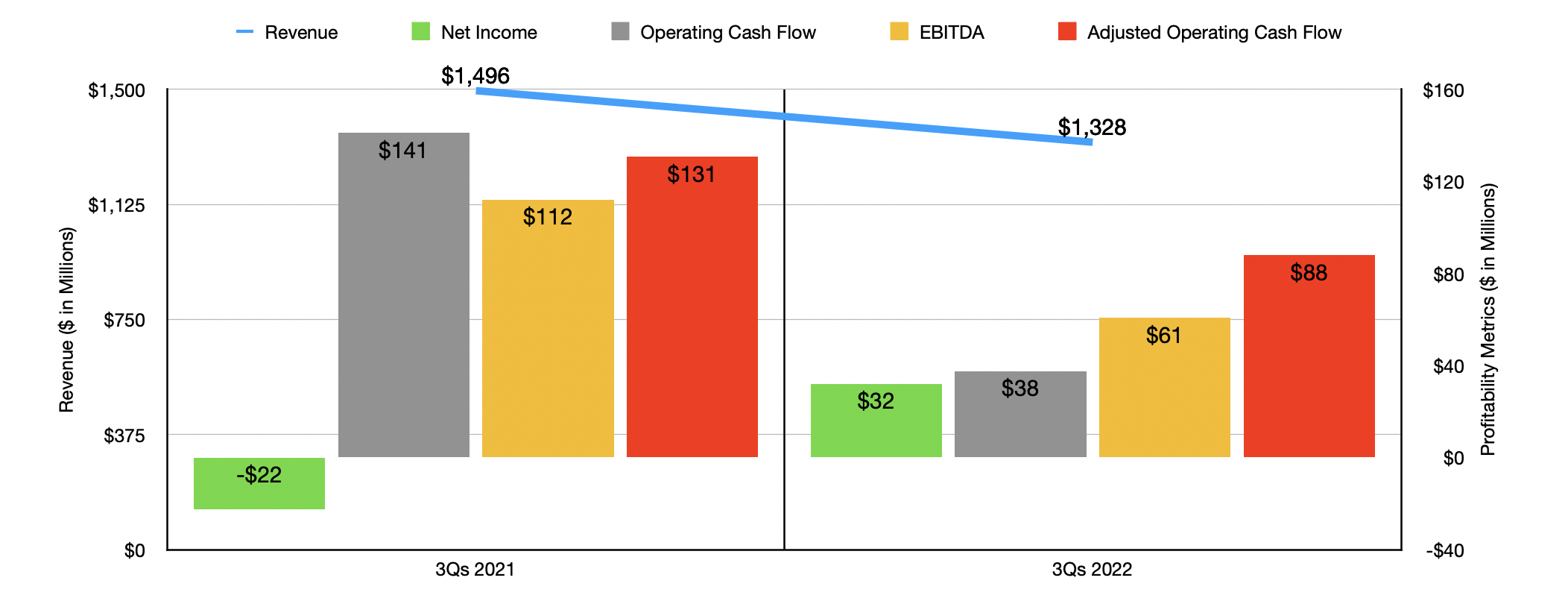

Based on this return disparity alone, you might think that the fundamental performance of the company had been robust. But this has not been the case. Consider, for instance, how the company performed for the first nine months of its 2022 fiscal year. Sales during that time came in at $1.33 billion. That's 11.2% lower than the $1.50 billion generated the same time one year earlier. According to management, the firm suffered largely as a result of global component constraints that ultimately limited how much product it could deliver to its customers. Product revenue, for instance, plunged $158 million. This narrative makes sense to me when you consider that service revenue, something that is far less subjected to supply chain issues, dropped only $9.9 million year over year. After adjusting for size differences, product revenue dropped by 12% while service revenue declined a more modest 4%.

The drop in revenue brought with it mixed bottom line results. Although the company did go from generating a net loss of $22.4 million to generating a profit of $31.9 million, operating cash flow plunged from $141.1 million to $37.5 million. If we adjust for changes in working capital, cash flow would have declined from $130.7 million to $87.9 million. Meanwhile, EBITDA was cut nearly in half, dropping from $112 million to $60.7 million.

{kind=link}

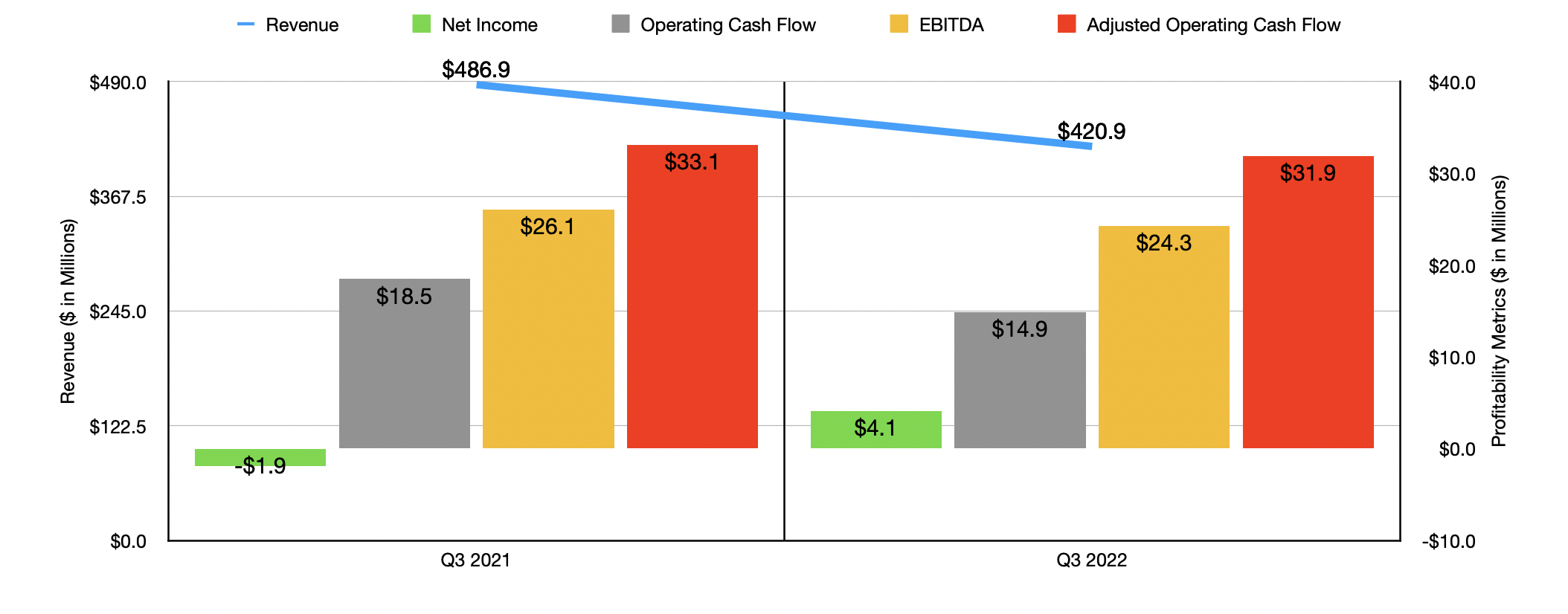

When it comes to the third quarter of 2022 on its own, the company continued to experience pain. Revenue fell from $486.9 million to $420.9 million. Yes, net income did come in higher year over year, turning from a negative $1.9 million to a positive $4.1 million. But operating cash flow fell from $18.5 million to $14.9 million, while the adjusted figure for this went from $33.1 million to $31.9 million. And finally, even EBITDA pulled back, falling from $26.1 million to $24.3 million. When it comes to the final quarter of 2022, management has been forecasting sales of between $420 million and $460 million. Earnings per share, meanwhile, should be between $0 and $0.15 per share, with a midpoint reading translating to full-year earnings guidance of $35.3 million. No guidance was given when it came to other profitability metrics. But if we annualize results experienced so far, we should anticipate adjusted operating cash flow of $43.8 million and EBITDA of $62.4 million.

{kind=link}

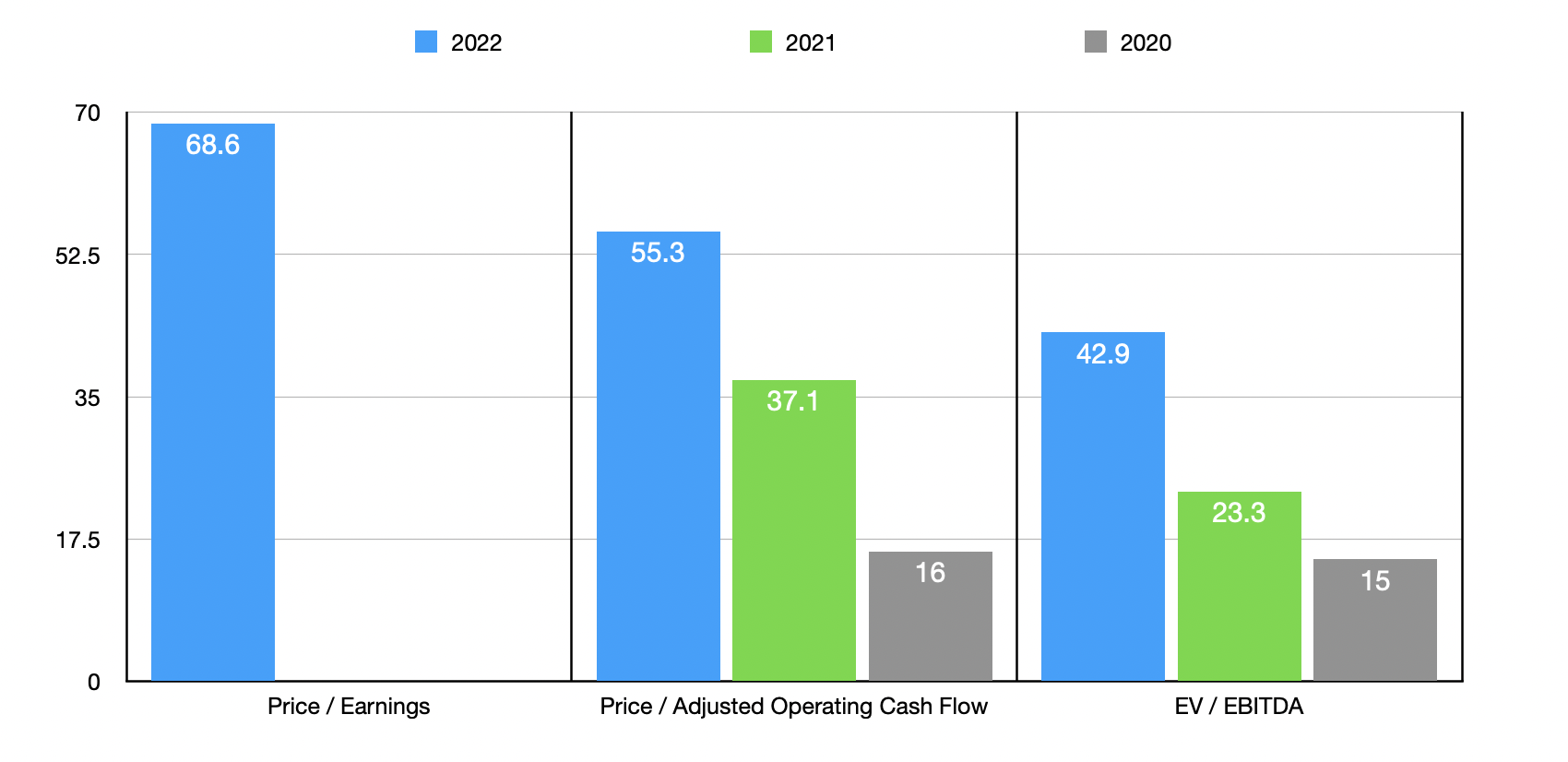

Using these numbers, we can easily value the business. On a price-to-earnings basis, shares are trading at a multiple of 68.6. The price to adjusted operating cash flow multiple is 55.3, while the EV to EBITDA multiple should come in at 42.9. No matter how you stack it, these numbers are incredibly high. Though, if we assume that the company will eventually revert back to the kind of profitability seen in 2020, shares start to become reasonably priced on an operating cash flow and EBITDA basis. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 27 to a high of 36.9. Using the EV to EBITDA approach, the range was from 15.3 to 17.1. In both of these cases, Itron was the most expensive of the group. Meanwhile, using the price to operating cash flow approach, the range was from 28.4 to 106. In this case, four of the five companies were cheaper than our prospect.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Itron |

| 68.6 |

| 55.3 |

| 42.9 |

| Zebra Technologies ( ZBRA ) |

| 32.7 |

| 33.3 |

| 15.3 |

| National Instruments ( NATI ) |

| 36.9 |

| 106.0 |

| 19.7 |

| Teledyne Technologies ( TDY ) |

| 27.0 |

| 35.9 |

| 17.2 |

| Keysight Technologies ( KEYS ) |

| 28.8 |

| 28.4 |

| 19.7 |

| Trimble ( TRMB ) |

| 27.6 |

| 30.0 |

| 17.1 |

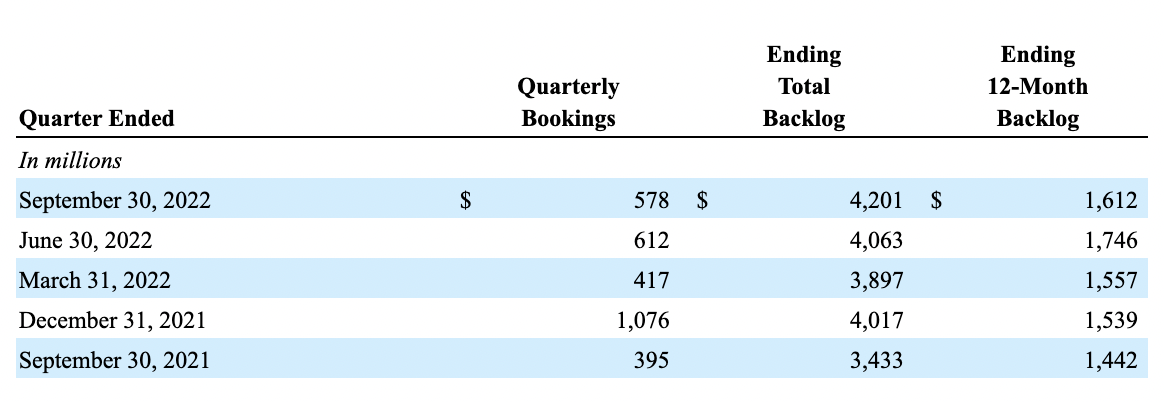

If we were to base the company's health solely on these financial figures, you would expect shares to have fallen. But there is one big thing that the company has going for it. And that is an increase in backlog that has developed over the past year. As of the end of the third quarter, backlog totaled $4.20 billion. Of that backlog, $1.61 billion is coming due over the ensuing 12-month window. To put this in perspective, this backlog figure compares favorably to the $3.43 billion reported for the same quarter one year earlier and the $1.44 billion that was supposed to be for the ensuing 12-month window. In fact, backlog is higher now than it has been in at least five quarters, with ending 12-month backlog coming in second only to the first quarter of 2022 when it totaled $1.75 billion. This signals potential strength ahead for the company. But of course, whether or not this robust backlog will mean much is something that only time will tell. If the company is not pricing its contracts accurately and is not fully passing on increased costs onto its customers, additional margin and cash flow data could look unfavorable.

{kind=link}

Takeaway

At this time, I definitely believe that Itron is an interesting company in an interesting position. The fact of the matter is that the company very well could go on to post improved bottom line results and justify an attractive upside for shareholders. But when it comes to investing, one of the biggest things that you need to keep in mind is that risk matters. What we have here is a company that looks incredibly pricey on both an absolute basis and relative to similar firms. We have revenue continuing to decline and cash flows under pressure. Yes, earnings do look to be on the rise. On top of that, the company does have a growing backlog. But for me personally, those two positives do not outweigh the negatives at this moment. Because of the uncertainty regarding the picture, I believe that a 'hold' rating still makes sense at this time.

For further details see:

Itron: Too Much Uncertainty For Me