IWL - IWL: Expensive Valuation Means Downside Risk Is High

2023-11-14 22:28:07 ET

Summary

- iShares Russell Top 200 ETF has a high expense ratio compared to its peers.

- IWL has slightly outperformed the S&P 500 index in the past and is expected to continue outperforming due to its higher exposure to the technology sector.

- The valuation of IWL is considered elevated, and there is significant downside risk due to the potential economic recession in H1 2024.

Fund Overview

iShares Russell Top 200 ETF ( IWL ) owns a portfolio of 200 largest U.S. stocks in terms of market capitalization. IWL has a high expense ratio of 0.15%, which is high among its peers. Other large-cap funds such as Vanguard Large-Cap Index Fund ETF Shares ( VV ) and Schwab U.S. Large-Cap ETF ( SCHX ) have expense ratios of only 0.04% and 0.03%, respectively. IWL has slightly outperformed the S&P 500 index in the past and is expected to continue to outperform the S&P 500 index thanks to its higher exposure to the technology sector. However, its valuation is quite elevated. Given that an economic recession is likely to occur in H1 2024, significant risk is not out of the question. Therefore, we think investors may want to wait for a pullback before buying.

YCharts

Fund Analysis

IWL has recovered most of its losses since October 2022

Let us begin our analysis by reviewing IWL's performance in the past two years. The fund has reached its price peak in early 2022. However, as sky-rocketing inflation forced the Federal Reserve to aggressively hike its rate in 2022, IWL has declined substantially. In fact, the fund has declined by about 25.6% from the peak in early 2022 to the trough in mid-October 2022. Fortunately, IWL has struck back with strong momentum in 2023 and is now only 6.5% below the price peak in early 2022.

YCharts

IWL has slightly outperformed the S&P 500 index in the past

IWL may have been in a rollercoaster ride lately, the fund has actually performed quite well in the long run. As can be seen from the chart below, IWL delivered a total return of 462.3% since its inception in September 2009. In fact, it has slightly outperformed the S&P 500 index's 436% in the same period. IWL's average annual return in the past 10 years was 12.46%, slightly outperforming the 11.87% average annual return of the S&P 500 index.

YCharts

IWL's slightly higher exposure to the tech sector should continue to provide slightly better long-term growth performance

Looking forward, we expect IWL to continue to outperform the S&P 500 index slightly due to its higher exposure to the information technology sector. As can be seen from the table below, the fast-growing information technology sector represents nearly one-third of IWL's portfolio. In contrast, information technology sector represents 29.2% of the S&P 500 index, about 3.3 percentage points less. We believe most stocks in the information technology sector is poised to deliver strong outperformance from several important megatrends such as the emergence of an electric vehicle, autonomous driving, artificial intelligence, Internet of Things (IoTs), industrial automation, cloud computing, etc. Therefore, IWL's slightly higher exposure to this sector should help it to continue to deliver slightly better performance than the S&P 500 index.

| IWL |

| S&P 500 Index |

| Information Technology |

| 32.50% |

| 29.23% |

| Health Care |

| 13.30% |

| 12.61% |

| Financials |

| 12.44% |

| 12.65% |

| Consumer Discretionary |

| 10.73% |

| 10.60% |

| Communication |

| 9.95% |

| 8.79% |

Source: iShares Website

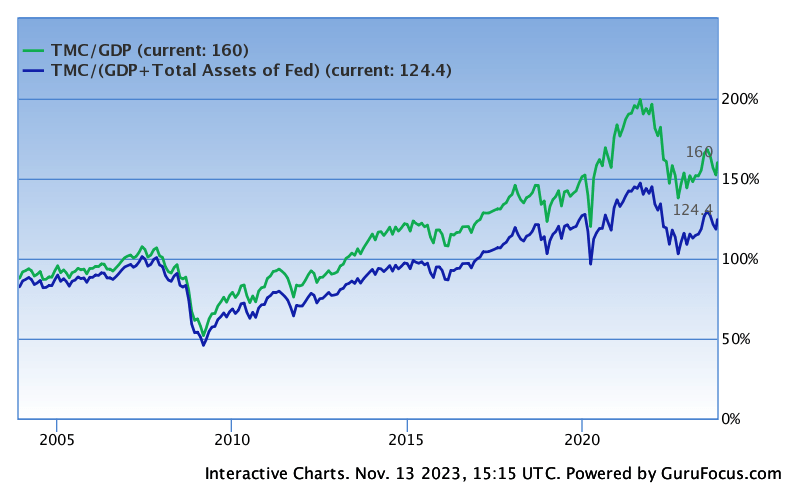

Buffett Indicator suggests that its valuation remains rich

We will now evaluate IWL's valuation based on the Warren Buffett Indicator. In a Forbes interview in December 2001, Warren Buffett suggested using the ratio of market capitalization to GDP to evaluate whether the broader stock market is overvalued or not. If the total market capitalization to GDP rate is in the range of 75% to 90%, the market's valuation is fair. If this ratio is above 90%, the stock market is overpriced. If this ratio is above 120%, the stock market is considered very expensive.

Since the Buffett Indicator is used to gauge whether the entire U.S. stock market is expensive or not, one may argue that the result is not suitable to analyze whether IWL's portfolio of only 200 stocks is expensive or not. However, we noted that these 200 stocks represent nearly 70% of the total U.S. stock market capitalization. Hence, the result can still help us quickly gauge the valuation of IWL.

Since Buffett introduced this indicator in 2001, the Federal Reserve has injected trillions of dollars into the economy, therefore the pure market capitalization to GDP ratio may not accurately reflect the situation. A better gauge of the market is to also include the balance sheet of the Federal Reserve. Therefore, the ratio should be revised to total market capitalization / (GDP + Total Fed Assets). Using this equation, we derive the current ratio to be 124.4%. This ratio is still way above the fair valuation range of 75% ~ 90% and is considered quite expensive. Hence, IWL appears to be expensive right now.

{kind=link}

Recession will drive another round of selloffs and earnings revisions

Since IWL appears to be expensive, downside risk need not be neglected. We believe the biggest downside risk is the eventual arrival of an economic recession. We believe the aggressive rate hike that the Federal Reserve has engineered in 2022 will eventually tip the economy over to a recession. This recession will likely happen in the first half of 2024. The reason this has not yet happened is that it usually takes a year or longer for the monetary policy to fully transmit through the economy. We believe two scenarios will happen if an economic recession arrives. First, there may be another round of market selloff, and this will cause valuation compression. Second, forward earnings of stocks may need to be revised downward. This will also cause downward pressure to IWL's fund price. Therefore, downside risk is quite high.

Investor Takeaway

IWL appears to be overvalued and downside risk is high. Given that we expect an economic recession to arrive in the first half of 2024, we think investors should exercise caution and wait on the sidelines.

For further details see:

IWL: Expensive Valuation Means Downside Risk Is High