IWM - IWM: The Reasons For Small-Cap Carnage

2023-03-16 16:34:57 ET

Summary

- The iShares Russell 2000 ETF told us something was wrong with the small-cap companies before the Silicon Valley Bank failure.

- IWM has underperformed the S&P 500 in 2022 and 2023 - small-caps need funding and a significant source has dried up in March 2023.

- The regulators were asleep at the wheel - the risks of large, long-bond portfolios with a hawkish Fed were as plain as the noses on the regulators’ faces.

- Government policymakers, regulators, and central banks are reactive - it is time for a proactive approach.

- It will take a long time for IWM to get back on its feet because of less financing, cash burn, and investors heading for fixed income - an opportunity for the cash-rich large caps.

It has been a nervous week in markets, as bank failures have added insult to injury for the stock and bond markets that have had a rough time over the past year. The Fed has increased short-term rates by 4.5% since March 2022, and the most recent consumer price data that revealed nagging inflation suggests at least another 25-basis point hike at the upcoming March FOMC meeting. Quantitative tightening pushes rates higher for further maturities and continues at $95 billion monthly. Stocks and bonds had been falling. The rapid decline in bonds created challenges for banking institutions that need to invest deposits but balance those investments with the potential for on-demand withdrawals.

Last week, three banks went under, including Silicon Valley Bank of SVB Financial Group (SIVB), with assets over $200 billion. When the value of bonds fell below the deposits, a run on the bank caused SVB to fail. SVB was a leading lender to new and emerging technology companies, posing funding risks for the small-cap sector. Bank failures always create challenges for the overall economy. Concerns over Europe's Credit Suisse only exacerbated the volatility. The small-cap iShares Russell 2000 ETF ( IWM ) made another in a series of lower highs on February 2, 2023. IWM signaled problems in the small-cap sector, which is most vulnerable to the latest round of bankruptcies.

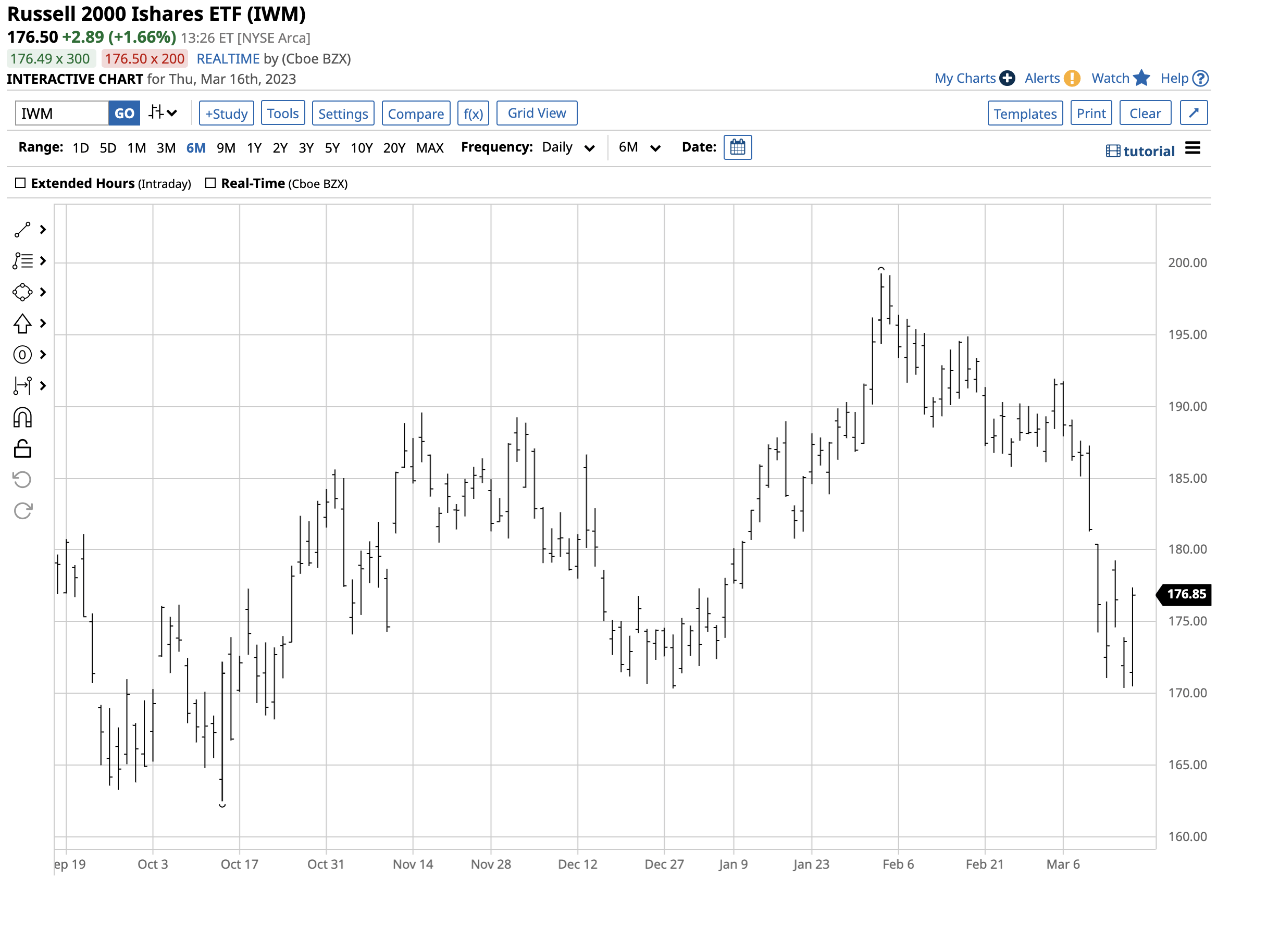

A bearish trend in IWM

On February 2, 2023, the Russell 2000 index's IWM exchange-traded fund ETF reached $199.26 per share, where it ran out of upside steam. One month before Silicon Valley Bank's failure, the small caps smelled problems.

{kind=link}

The chart shows a 14.5% decline from $199.26 on February 2 to $170.38 per share on March 15. Over the same period, the SPY dropped from $418.31 to $380.65 per share or 9%. The tech-heavy QQQ fell from $313.68 to $285.19 per share, a 9.1% decline that took SPY and QQQ to lows on March 13. Meanwhile, the DIA ETF dropped from $340.43 on February 2 to $314.97 on March 15, a 7.5% drop. The IWM was the weakest of the four, and the bearish trend in the small caps has been intact since the November 2021 high.

{kind=link}

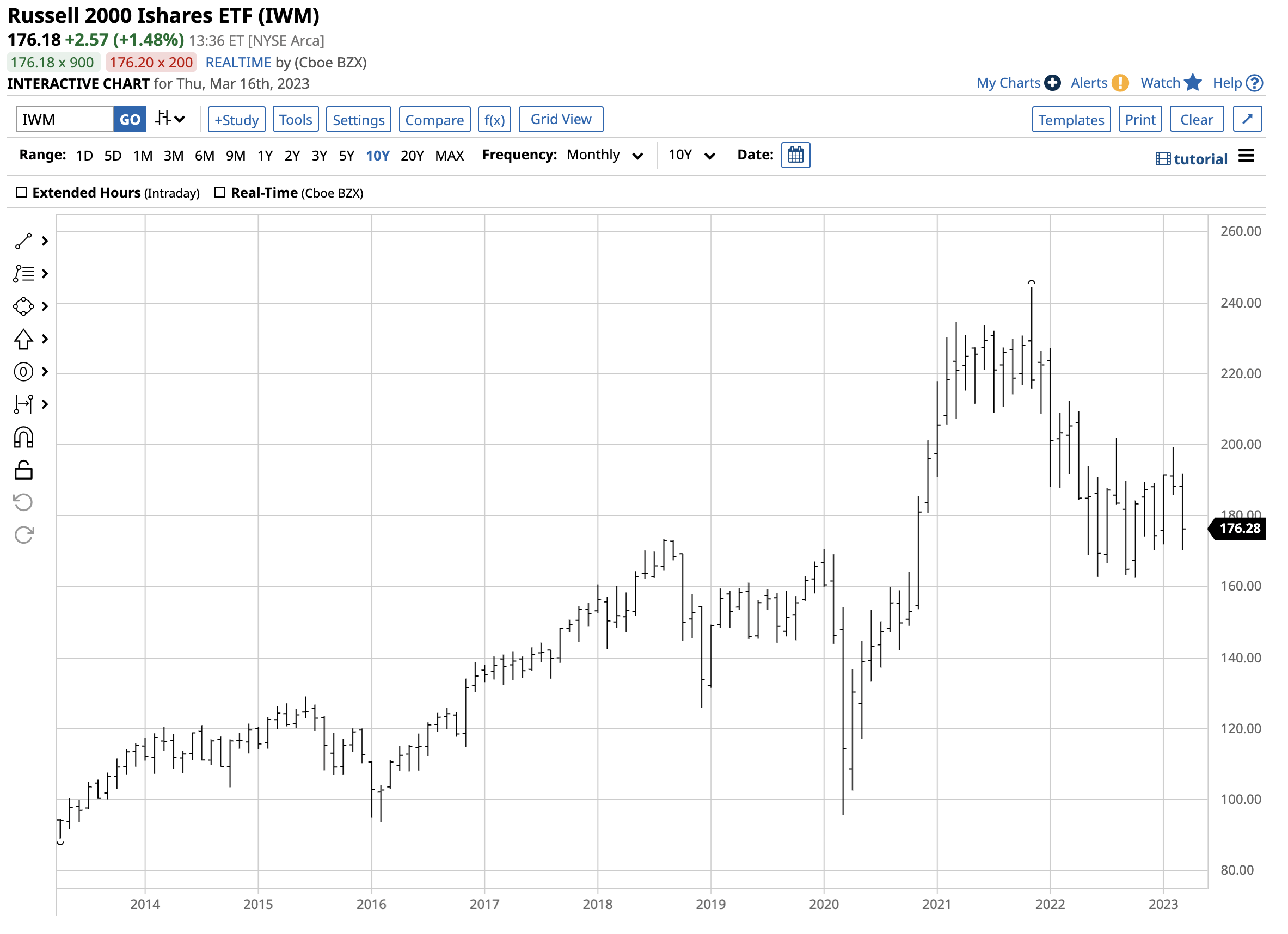

The longer-term chart shows the pattern of lower highs and lower lows in the small-cap ETF.

IWM reflects the companies that need capital the most

The Russell 2000 index makes up the smallest 2,000 stocks in the Russell 3000 index. The index weights each stock component by its market cap, typically between $300 million and $2 billion. The stocks that comprise the Russell 2000 have demonstrated strength in annual revenues, cash flow, and public demand for their products.

Small-cap companies have the greatest need for financing and are often emerging innovative businesses, many of which are technology companies. With over $200 billion in assets, Silicon Valley Bank was a leading funding agent for these companies and became the sixteenth-largest U.S. bank. SVB became the second largest bankruptcy, behind Washington Mutual.

Silicon Valley Bank invested deposits in government bonds. As the Fed increased short-term interest rates and tightened credit further along the yield curve via quantitative tightening, those bonds lost mark-to-market value. If held to maturity, the government bonds were safe investments, but if liquidated early, they resulted in losses. As deposits were on demand, a flood of withdrawals forced SVB into receivership. The FDIC and government stepped in to guarantee the deposits, not the equity, and SVB went bankrupt.

Meanwhile, Signature Bank (SBNY) also went under, and European Credit Suisse experienced a liquidity crisis over the past few days.

Small-cap emerging companies depend on credit, higher interest rates, and more selective financing limit their options and opportunities for success. The IWM began declining before the SVB bankruptcy, and the bankruptcy of a leading funding source sours the potential for future small-cap success.

Where were the regulators?

Following the 2008 financial crisis, the Dodd-Frank legislation created a regulatory framework for banks' capital adequacy. Moreover, the Federal Reserve conducts periodic stress tests that can identify undercapitalized institutions at risk of bankruptcy when market volatility creates either mark-to-market or realized losses that prevent them from meeting on-demand deposit obligations. The previous administration exempted banks with assets below $250 billion from some Dodd-Frank regulations.

Ironically, former U.S. Congressman Barney Frank, co-author of the legislation, was on Signature Bank's board and lobbied for the exemption for banks with assets between $50 and $250 billion, arguing the smaller banks do not threaten systemic risks for the banking sector. Meanwhile, the recent government actions have contradicted the importance of midsize banks extending deposit guarantees for uninsured depositors at SVB. The government also set up an emergency Federal Reserve Bank Term Funding Program to extend liquidity to troubled banks and insulate the financial system from contagion. The byline in a March 15 Wall Street Journal article was " The Federal Reserve fails to account for interest-rate risk. "

The bottom line, despite the easing of banking rules, is the regulators should have realized that the trajectory of interest rate hikes and the quantitative easing program battling inflation significantly impact financial institutions of all sizes. Bank failures can have a domino effect, the definition of systemic risk. The Fed, FDIC, policymakers, and all financial regulators fell asleep at the wheel.

Reactive versus proactive regulation and policy

While regulators can hide behind the relaxation of regulations for mid-sized banks with assets between $50 and $250 billion, the root of the problem is far more profound. The government regulators continue to have a reactive approach, addressing issues after they occur, instead of a proactive course to prevent them from happening.

There are many examples, starting with the Dodd-Frank Act itself, which was a reactive response to the 2008 housing, mortgage-back bond, and global debt crisis. Another example of reactive thinking is the Fed's slow approach to rising inflation in late 2020 and throughout 2021, blaming rising prices on " transitory " pandemic-related factors. While the Fed became hawkish in March 2022, it waited too long. In 2023, interest rates continue to rise as inflation remains a nagging issue. Over the past weeks, the data-driven Fed has continued its hawkish squawking despite the rising odds of a recession. Data is a snapshot of the past, but the economy is a real-time, living, and breathing financial organism. The trajectory of rate hikes fighting inflation has unintended consequences like the recent bankruptcies at financial institutions. The Fed has its hands full as it convenes for the March FOMC meeting to decide if it will increase the Fed Funds rate again. The most recent February CPI snapshot data supports another rate hike. On March 16, the ECB raised its short-term rate by 50 basis points, despite Credit Suisse's travails.

Any trained Ph.D. economist has experience in forecasting, which is a proactive exercise. While historical data are critical inputs, the output forecast yields a proactive answer. However, it is much easier and politically acceptable to blame mistakes on reacting to past data than on actions based on projections. So long as the Fed, regulators and policymakers follow a reactive approach, they will remain behind the curve, battling economic fires when blazing instead of snuffing them out before they ignite. We may look back at the current hawkish monetary policy in the U.S. and Europe as another reactive case. Monetary policy actions have a lagged economic impact, and the trajectory of rate hikes will likely overshoot the problem, as did the dovish policy and government spending moves during the pandemic.

IWM could face continued selling- an opportunity for the large-caps

Small-cap stocks face a new reality after SVB's failure and the continuation of tight monetary policy. As the funding for new and innovative companies dries up, so will progress. However, there is a silver lining in every cloud. Well-capitalized companies with tons of cash are now positioned to acquire small-cap emerging companies at bargain basement prices, creating accretive opportunities.

Regulators and policymakers are concerned about the concentration of power among the leading technology companies, leading to monopolies that increase consumer prices. A wave of acquisitions will create another headache, and I view SVB's failure as another success for the technology leaders.

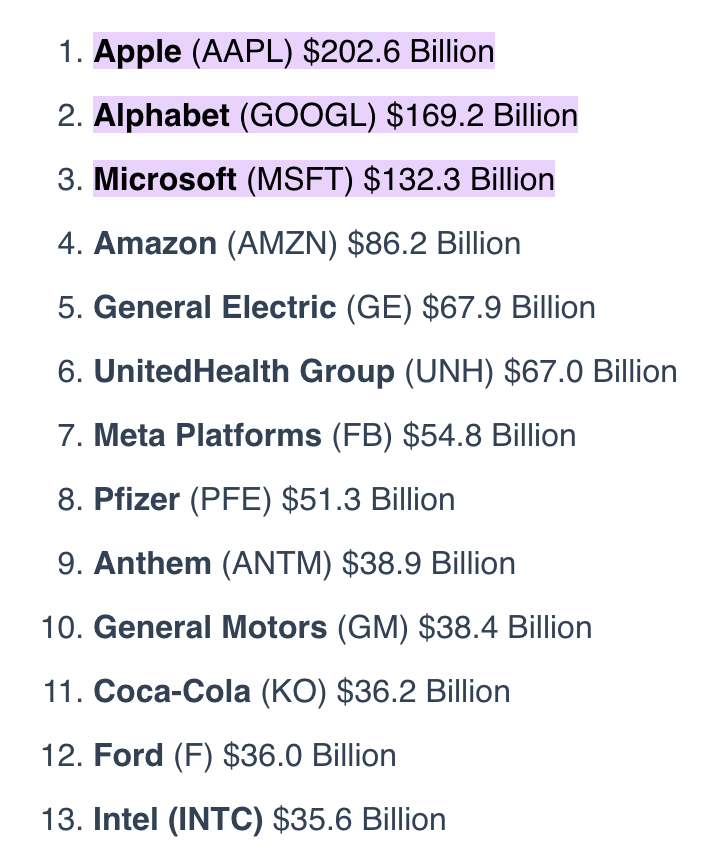

{kind=link}

The chart shows the 2023 cash top companies have on their balance sheets. When the dust settles, less bank financing for emerging small caps will lead to acquisitions that strengthen companies facing regulatory scrutiny because of their size.

Poor management and a regulatory misstep led to SVB's failure. A reactive approach was to guarantee deposits and reinstitute previous regulations on banks with $50 to $250 billion in assets. However, a proactive method would address the failure's impact, strengthening the growing technology monopolies as cash-rich companies stand to be the victors.

While iShares Russell 2000 ETF's trend remains bearish, the next bullish move could come from a series of aggressive acquisitions that are the alternative to the past funding.

For further details see:

IWM: The Reasons For Small-Cap Carnage