IUSV - IWN: Low Growth Is Not Necessarily Value

Summary

- Systematic value investing is the idea that fundamentally cheap stocks tend to outperform expensive stocks over the long term on average.

- The iShares Russell 2000 Value ETF tracks the Russell 2000 Value Index and offers a simple, transparent, and cheap implementation of the value premium for US small caps.

- Unfortunately, the index equates "value" with "low sales growth" and therefore contradicts with well-known results of the academic and practitioner literature on the value factor.

- Despite decent performance since inception in 2000 and over the last years, IWN is therefore not my preferred value instrument.

After writing a rather long article about QVAL and (systematic) value investing in general, this one examines the next ETF of my peer-group: the iShares Russell 2000 Value ETF ( IWN ).

For a more comprehensive overview on systematic value investing, I refer interested readers to the "Value Investing - Idea and Evidence" section of my previous article. To get everyone on the same page, however, here is a brief working definition of what I understand as systematic value investing.

Since the introduction by Benjamin Graham and David Dodd in the 1930s, the underlying idea of value investing has not changed: cheap stocks (with respect to fundamentals) tend to beat expensive stocks over the long-term, on average. Translated into a systematic investment process, value investing usually means buying a diversified portfolio of stocks with low fundamental valuation multiples (Price/Book, Price/Earnings, EV/EBITDA, etc.). You can incorporate a lot of further details (controlling for industry exposures, interactions with other factors like quality, proprietary value signals, ...), but the underlying idea always remains the same. As a value investor, you want to be long/overweight cheap stocks and short/underweight expensive stocks.

Systematic value investing (or the "value factor") has been extensively studied in the academic and practitioner literature and there is pervasive empirical evidence that cheap securities tend to beat expensive ones in virtually all of the world's equity markets and even within other asset classes. In addition to that, there are plausible theories (both behavioral and risk-based) why value investing worked, should work, and probably continues to do so.

Overall, this makes systematic value a very appealing investment strategy that investors should definitely consider in their portfolios. So let's see how IWN implements it.

IWN's Implementation of Value

According to its website and quite obvious from its name, IWN tracks the Russell 2000 Value Index. To understand how the underlying value process works, we therefore need to look at the index. Before we do that, however, one important comment. As we all know, the Russell 2000 is a small/mid cap index. Given that the Russell 2000 Value Index is a subset of this "parent index", IWN is a dedicated small-cap value strategy. By itself, this is neither good nor bad. It just depends what kind of exposure you want to have. Having said that, the empirical evidence strongly suggests that systematic value investing worked much better among small caps (see first chart below). So if you plan to add value to your portfolio and can live with higher volatility of small caps, you may want to think about implementing value with small caps.

Back to the methodology of the Russell 2000 Value Index. The latest factsheet provides a brief summary of the index:

The Russell 2000® Value Index measures the performance of the small-cap value segment of the US equity universe . It includes those Russell 2000 companies with relatively lower price-to-book ratios , lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years) . [...] The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics

Source: Russell 2000 Value Index Factsheet , accessed February 27, 2023. Annotations by the author.

From this short paragraph we already know something about the underlying value process:

- As mentioned before, the universe are US small caps.

- The value signals are Price/Book, 2Y forecasted sales growth, and 5Y historical sales per share growth.

- The index rebalances annually.

Although a good starting point, these information are not sufficient for a nerdy finance guy like me. So let's go to the latest index methodology from January 2023. Starting at page 26, we learn that "FTSE Russell uses a "non-linear probability" method to assign stocks to the growth and value style valuation indices [...]."

To illustrate the portfolio construction of the Russell 2000 Value Index, suppose a stock has a 2% weight in the parent Russell 2000 Index. To decide if the stock is a "value" or "growth" stock, FTSE Russell first looks at the stock's ranking of the three signals and convert them into a composite score. The cheaper and the less growing, the more likely that the "non-linear probability method" classifies a stock as "value".

There are more details in the document, however, the result of the method is actually quite straight forward. The "non-linear probability method" assigns a "value" and "growth" probability to each stock. These form the basis for the portfolio weights. If our example stock receives an 80% value probability, it will get a 2% x 80% = 1.6% weight. Similarly, the weight in the growth index will be 2% x (1 - 80%) = 0.4%. The sum of the value and growth weights therefore always equals the weight in the parent Russell 2000 Index.

To get the final Russell 2000 Value and Growth Indices, FTSE Russell re-scales those weights back to 100%. That way, the Russell 2000 Value Index overweights value stocks with respect to the parent index. Given that the parent Russell 2000 is market-cap weighted, we have something like a value-weighted small cap value strategy. Note, however, that these are just the basic principles. FTSE Russell further employs a bunch of filters and exceptions to ensure compliance with regulations and manage turnover.

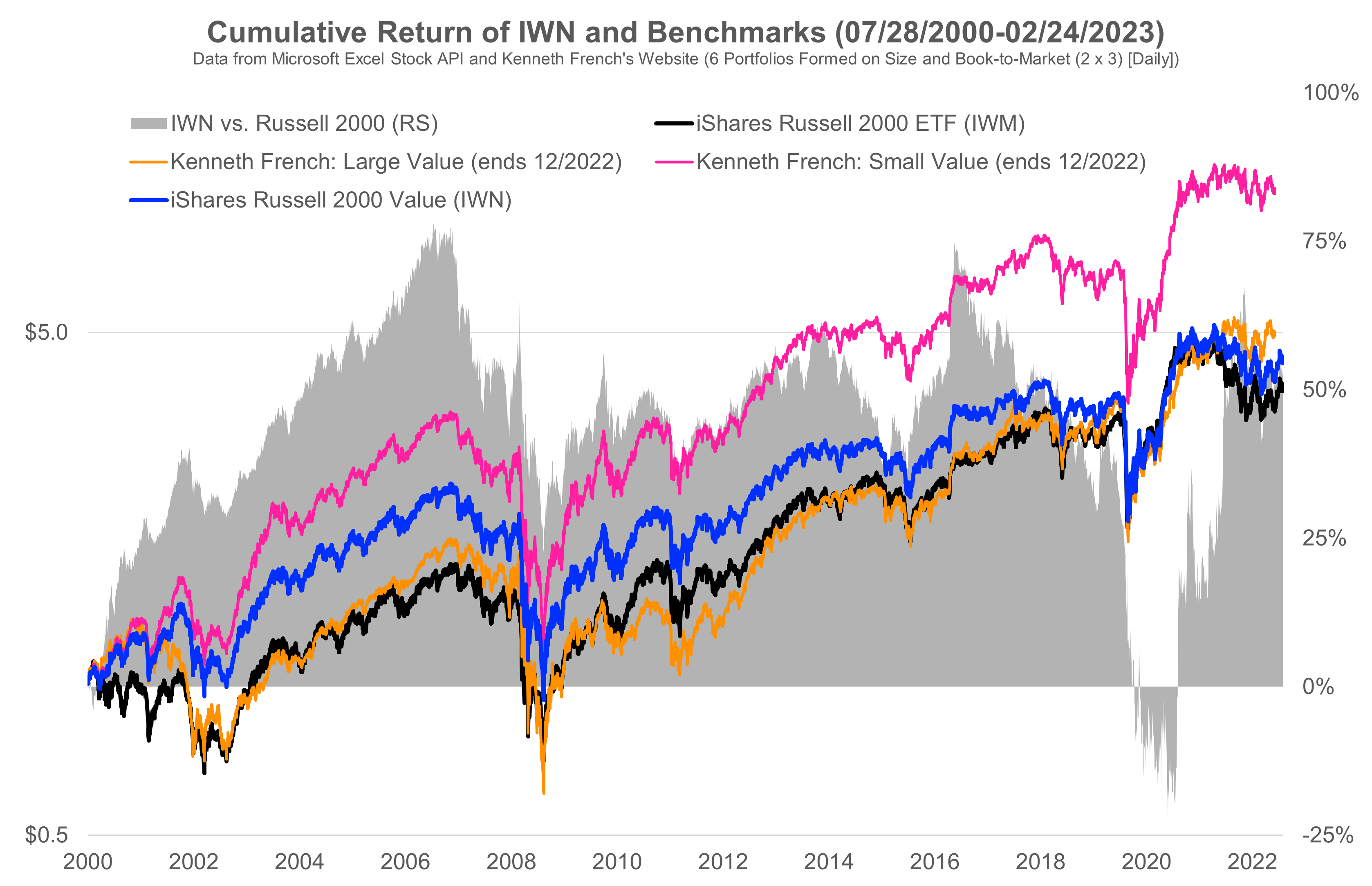

The following chart shows the results of this process since inception of IWN in July 2000 compared to the Russell 2000 Index, and the two simple academic value portfolios from Kenneth French's website.

Own illustration of data from Kenneth French's website and market data. (Tuck School of Business and Microsoft Excel Stock API)

{kind=link}

The good news first: IWN outperformed the parent index since inception by about 50%-points (note the log scale). However, the ride has been anything but smooth. In the last two market crashes (2008/09 and 2020), the ETF lost much of its accumulated outperformance in a very short period of time just to recover sharply thereafter. So overall, the results were satisfying but hard to stick with.

Compared to the academic value benchmarks, however, the ETF doesn't look too good. While outperforming Large Cap Value most of the time since inception, the IWN trailed it recently and is now even behind it. For the Small Cap Value portfolio, which is the more appropriate benchmark for a Russell 2000 universe, things look even worse. Much of it is probably due to some additional constraints that are required in practice (investability, active risk to the parent index, etc.). Nonetheless, such a drastic performance gap raises questions. So let me give you a few points that I personally don't like about the value process of IWN.

Value Signals: IWN uses just one fundamental valuation ratio (Price/Book) and two growth measures as value signals. While Kenneth French's portfolio are also just built on Price/Book, I am not aware of any rigor research that finds sales growth to be a reliable value signal. In fact, I really don't like the fact that FTSE Russell equates "low growth" with "value".

For some reasons, the majority of the investment industry and financial media at some point decided that the opposite of a cheap "value" stock is an expensive "growth" stock. If you go back to the original research on value from Fama and French ( 1992 ), however, you will not find the term "growth stock" and systematic value has never been about growth. It is of course possible that value stocks are cheap because the underlying companies do not grow. You may also use sales growth as an additional screen to filter out the fastest growing cheap stocks or vice versa ("Growth at a reasonable price"). But using growth rates as primary value signal is very strange and not in line with the methodology you typically see in the literature. Low growth is not automatically value.

Rebalancing: As mentioned before, IWN rebalances annually (but has some exceptions to deal with corporate actions). In general, this is not a big problem for value as the factor is much "slower" than for example momentum (i.e. it requires less turnover to be profitable). However, given that most companies release quarterly fundamentals, I think it would make more sense to use this information and update the portfolio quarterly or at least semi-annually.

IWN and Value-Peers

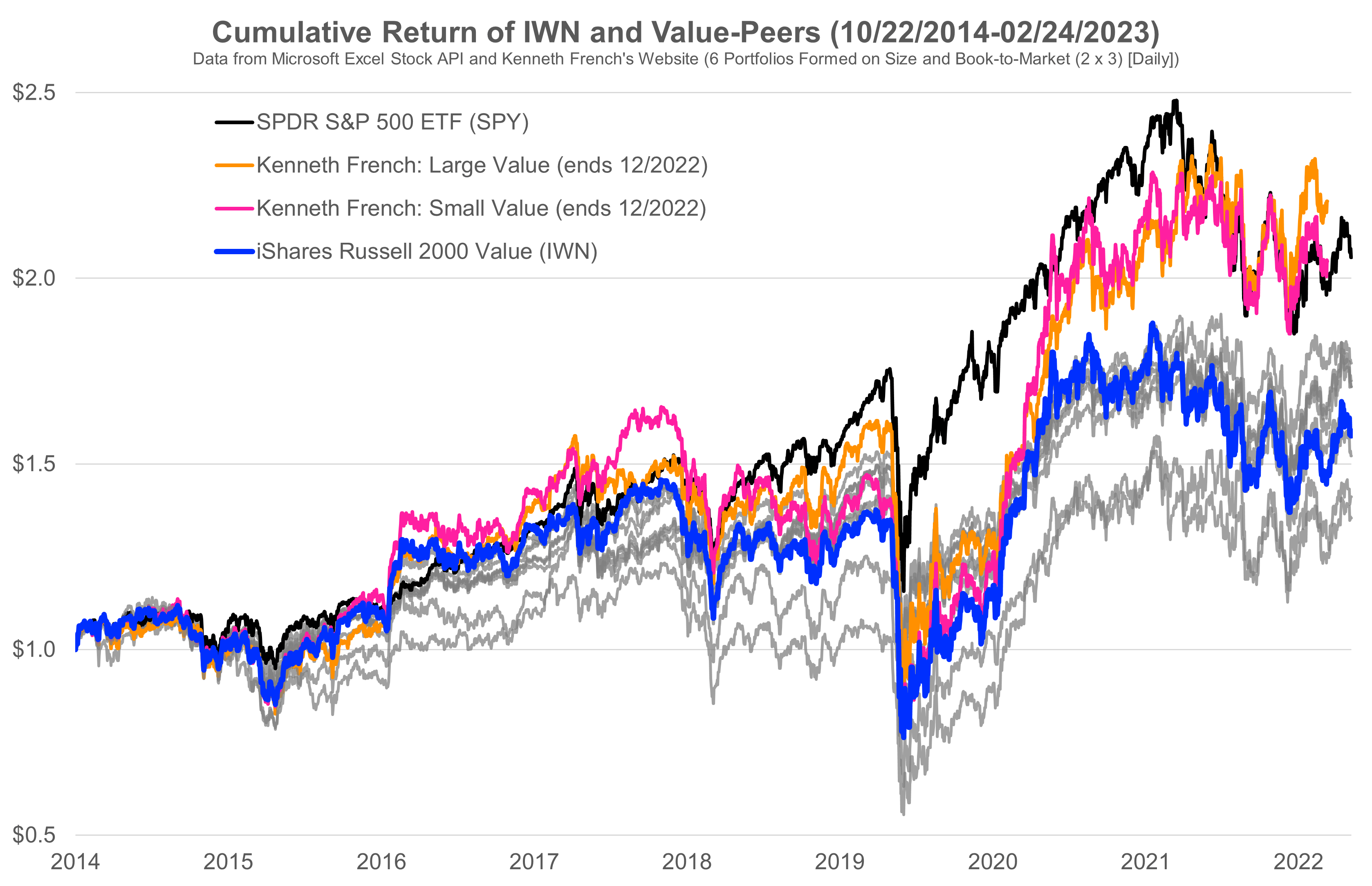

In addition to the long history of IWN versus its benchmarks, the following chart shows the ETF versus my (admittedly somewhat arbitrary) peer-group of other value ETFs for the longest common period since October 2014. The peer-group consists of VLUE , VTV , VBR , IVE , IWD , QVAL , DFFVX , and IUSV . I haven't included them in the legend of the chart as the goal is to give you a broad overview how IWN compares to some of its peers.

Own illustration of data from Kenneth French's website and market data. Value-peers are QVAL, VLUE, VTV, VBR, IVE, IWD, DFFVX, and IUSV. (Tuck School of Business and Microsoft Excel Stock API)

{kind=link}

For a discussion of the relative performance of the value-peers with respect to the S&P 500 and the academic benchmarks of Kenneth French, I again refer more interested readers to my first article .

With respect to IWN, I would say the peer-performance is somewhere between "improvable" and "okay". There are worse funds like QVAL and DFFVX, and there are some better ones which, however, didn't beat IWN by a wide margin. Once again, we also see that the value portfolios from Kenneth French massively outperformed all of the value ETFs. Given the simple construction, this is (in my opinion) quite striking. However, I suspect that much of it is due to the unconstrained, and rather theoretical nature of the academic portfolios.

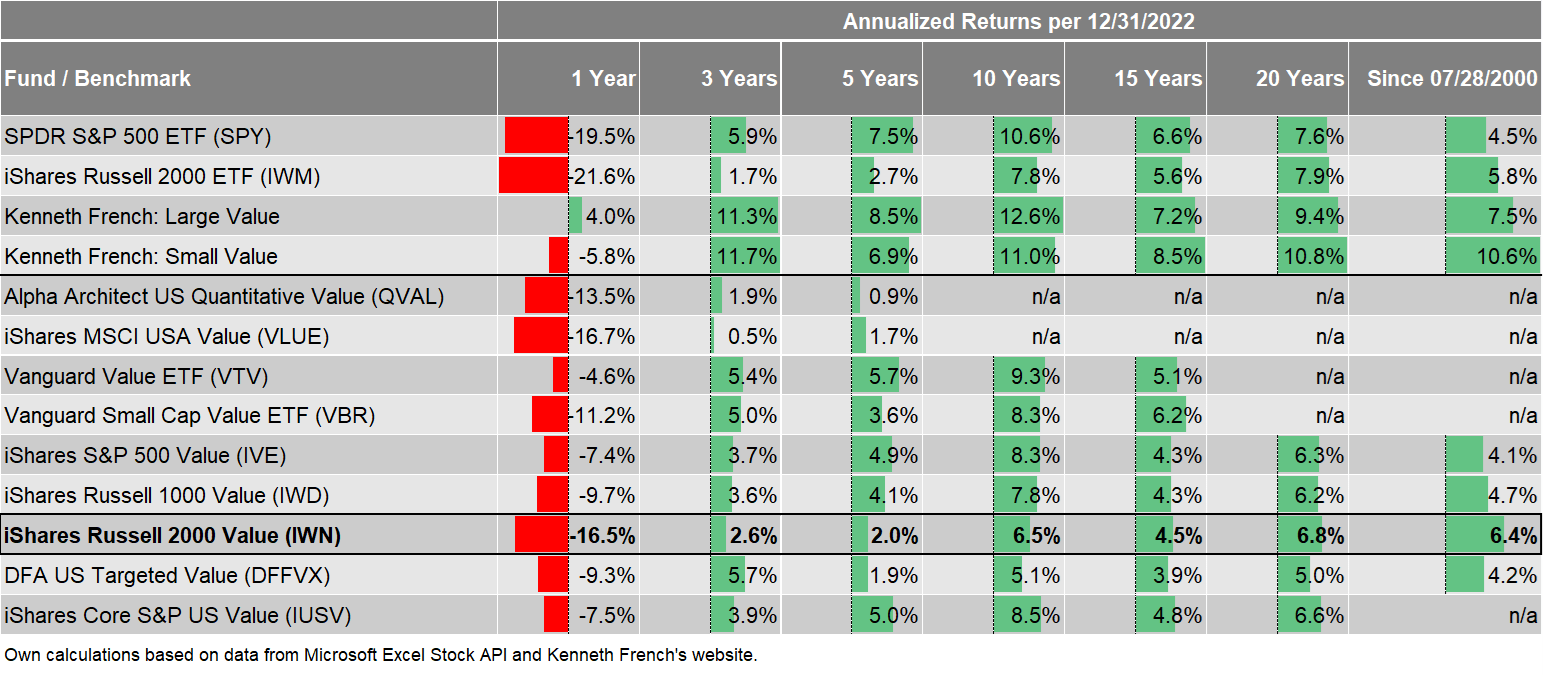

The following table again summarizes the data numerically and also shows returns over some sub-sample periods. The results remain mostly unchanged. With respect to performance, IWN finds its place somewhere in the middle or lower half of the peer-group. Over the very long-term, the results are very decent and the ETF beat both the S&P 500 and the Russell 2000 Index. This deserves credit! At the same time, however, it also lags the simple and well-known academic value benchmark by more than 4%-points per year.

Tuck School of Business and Microsoft Excel Stock API

{kind=link}

Conclusion

The fact that IWN exists for almost 23 years and outperformed common market benchmarks since inception deserves credit. But despite decent performance, I personally don't like the underlying value process. The index addresses the popular "Values vs. Growth" distinction and defines value stocks as "low Price/Book", "low forecasted growth", and "low historical growth". The first is fine, the remaining two are in my opinion problematic.

I am not aware that the academic or practitioner literature on systematic value finds sales growth to be a robust value signal. Of course, it is certainly possible that value stocks are cheap because of low growth. But this is a different story.

Taking another perspective, what do I as an investor expect from a systematic value ETF? Well, I want to use it to implement the results of rigor empirical research on the value premium in my portfolio. Therefore, the ETF should incorporate the findings in its methodology. To the best of my knowledge , value is best implemented with a composite of fundamental valuation ratios, measured within industry, and maybe even in combination with quality. This has nothing to do with the "low growth" filter of IWN. Despite its decent performance and simple process, IWN is therefore not my preferred value instrument. As it could still somewhat profit from the value-premium, I assign a "Hold" rating.

For further details see:

IWN: Low Growth Is Not Necessarily Value