IXN - IXN: Global Tech Stocks Should Bounce Back Even As The Economy Heads Into Recession

Summary

- IXN invests in global tech stocks, with a United States bias.

- The fund could be argued as pricey if we assume a large drop in the underlying return on equity (and hence earnings growth).

- However, if earnings growth numbers come even close to consensus analyst estimates, the implied IRR should exceed 10% over the longer term.

- I would remain bullish on IXN with a long-term view.

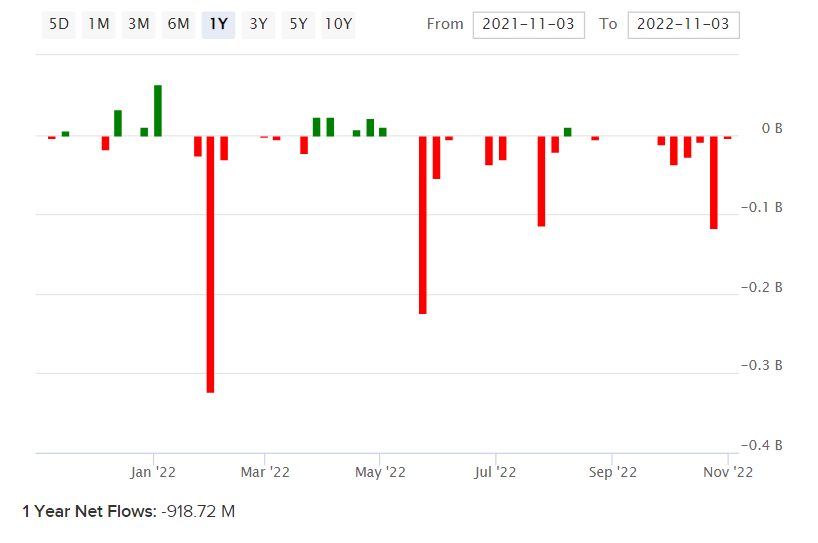

iShares Global Tech ETF ( IXN ) is an exchange-traded fund that invests in electronics, computer software and hardware, and informational technology companies. IXN invests in accord with its chosen benchmark, the S&P Global 1200 Information Technology Sector Index. Net assets under management summed to $2.66 billion as of November 4, 2022, and the fund carries an expense ratio of 0.40%. This follows negative net fund flows over the past year of -$919 million.

{kind=link}

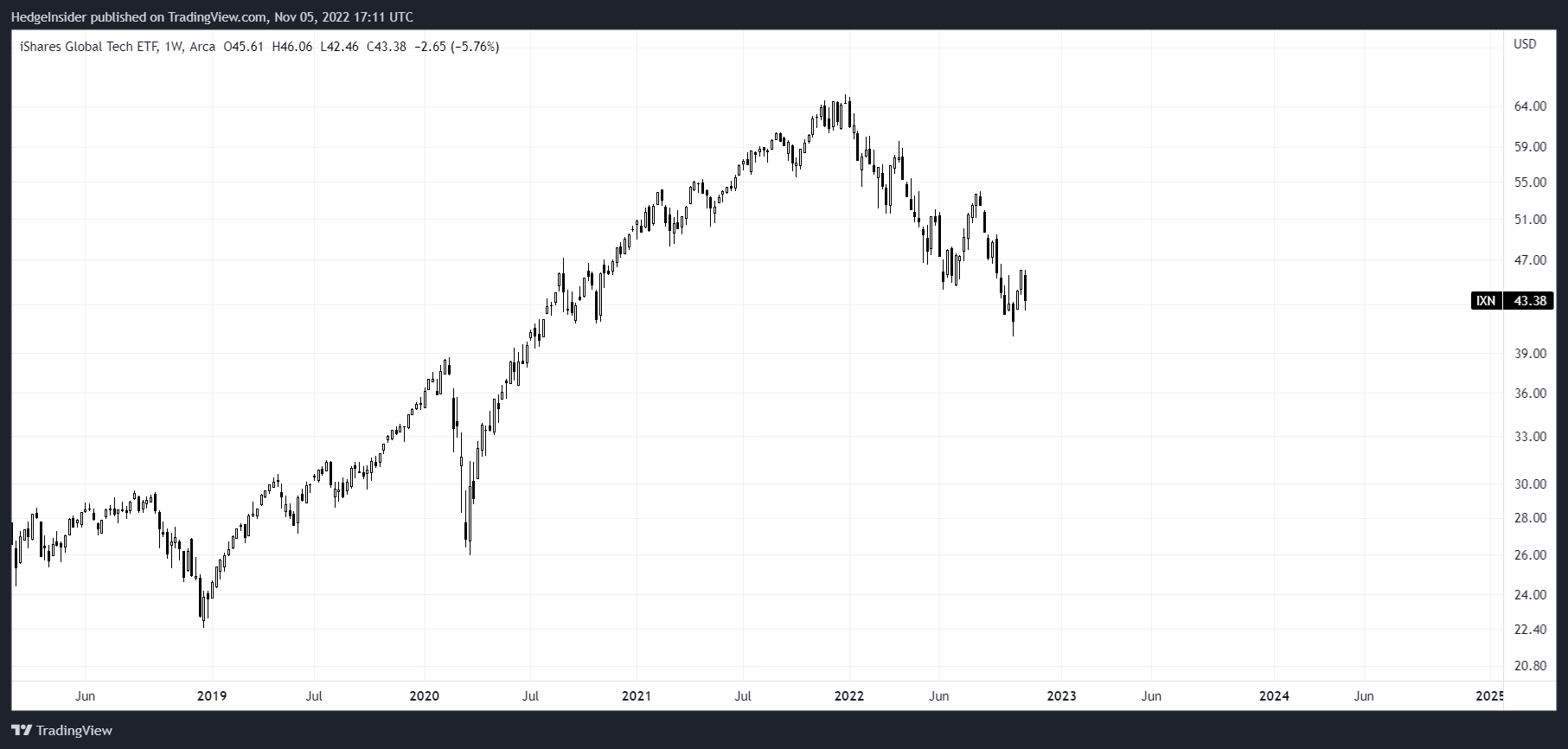

I last reviewed IXN in June 2022 , which marked a short-term bottom, however those lows have been revisited by the market more recently in September 2022. I have maintained a long-term bullish stance on IXN given that the valuation has consistently implied a healthy underlying equity risk premium, however long-term bond yields have continued to rise. Fiscal and monetary policy have been contractionary (as scaled by GDP), and the U.S. Federal Reserve's current rate-hiking cycle is not yet over. The upper bound on the Fed's short-term rate was increased to 4% in November 2022.

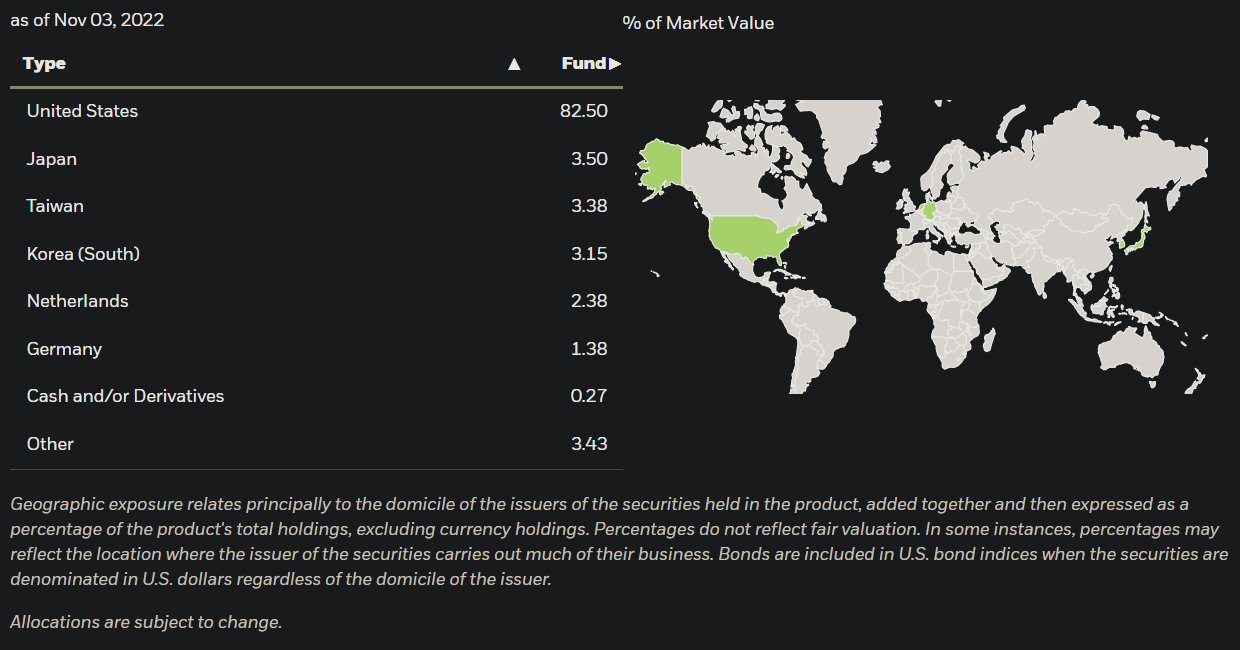

While IXN is a global fund, its main exposure is the United States (82.5% of the portfolio as of November 3, 2022). Other top exposures include Japan, Taiwan, and South Korea, however these countries only represented 3-4% each as of recent (see below).

{kind=link}

Therefore, when valuing and thinking about IXN, one should generally view the fund as a U.S.-centric fund, and that is likely to remain the case given the large market capitalizations of the United States' major tech companies vis-à-vis the rest of the world.

IXN's benchmark index can be used as a proxy for IXN's actual portfolio, given IXN's close tracking of its benchmark. The benchmark's most recent factsheet (for the S&P Global 1200 Information Technology index) is dated as of October 31, 2022, and offers trailing and forward price/earnings ratios of 22.13x and 20.20x, respectively, with a price/book ratio of 6.11x. Those figures imply a forward earnings yield of 4.95% and a forward return on equity of 30.25%. The return on equity is unsurprisingly high given the sector focus, however the price/book ratio is also high; investors pay up for highly productive businesses, which makes sense. The forward earnings yield is quite tight, given that the U.S. 10-year yield is presently 4.16%. IXN is still priced with an expectation that the portfolio will continue to produce strong earnings in the long run.

Morningstar data suggests that three- to five-year earnings growth will come to 12.68% for IXN's portfolio, which is still quite high, although not especially high in relation to other funds' earnings growth expectations. I can use the above information to create a basic valuation model, however large tech companies remain heavily involved in buybacks (see Yardeni Research which indicates that well over 50% of operating earnings are being used to buy back stock, now at discounted prices). I will assume 50% to keep things simple across a six-year cycle in which I assume that the return on equity of the portfolio will drop back to about 25%. Given near-term recessionary risks, I am taking a more pessimistic approach to last time. This takes my average earnings growth assumption to just 3.5-4.5% per year over the period, safely under the circa 13% consensus figure from Morningstar.

{kind=link}

This investment case takes our implied equity risk premium to about 4%. This is on the low end, and given IXN's five-year beta of 1.16x, makes the beta-adjusted ERP even worse at 3.48%. In both cases, this also assumes a 4% risk-free rate. However, this is of course based on a lower earnings growth model. In order to take the return on equity gradually down to 25%, the model had to assume 2% earnings growth from year two onward.

The market seems to be implying a combination of closer-to-consensus earnings growth/consistently strong returns on equity, probably a sharp improvement in macroeconomic conditions (including inflationary pressures), and possibly also lower long-term bond yields.

If I were to instead assume that returns on equity hold at just over 30% (as in the trailing year), then average earnings growth would jump to 7-8%, but still underneath the analyst consensus figure of about 13%. In terms of valuation, that would take our implied equity risk premium to 8.77%, a sharp improvement, or 7.56% on a beta-adjusted basis. That assumes a risk-free rate still of 4%, for a total IRR of just under 13%.

We are also assuming a constant forward earnings multiple. If long-term yields were to fall over the period, this would support the multiple. However, equity risk premiums and bond yields tend to move inversely to some degree. Meanwhile, we should probably check to see the viability of the multiple.

We can do this by assuming an equity risk premium of at least 4%, a risk-free rate of 4%, and earnings growth of 2-3% in the long run. The implied forward multiple would be the inverse of the sum percentage (subtracting the growth element), being 18.2x. Should our terminal multiple drop to 18.2x by year six in my last iteration, the implied IRR would drop from just under 13% to just under 11%; it wouldn't break the investment case, but it is worth noting.

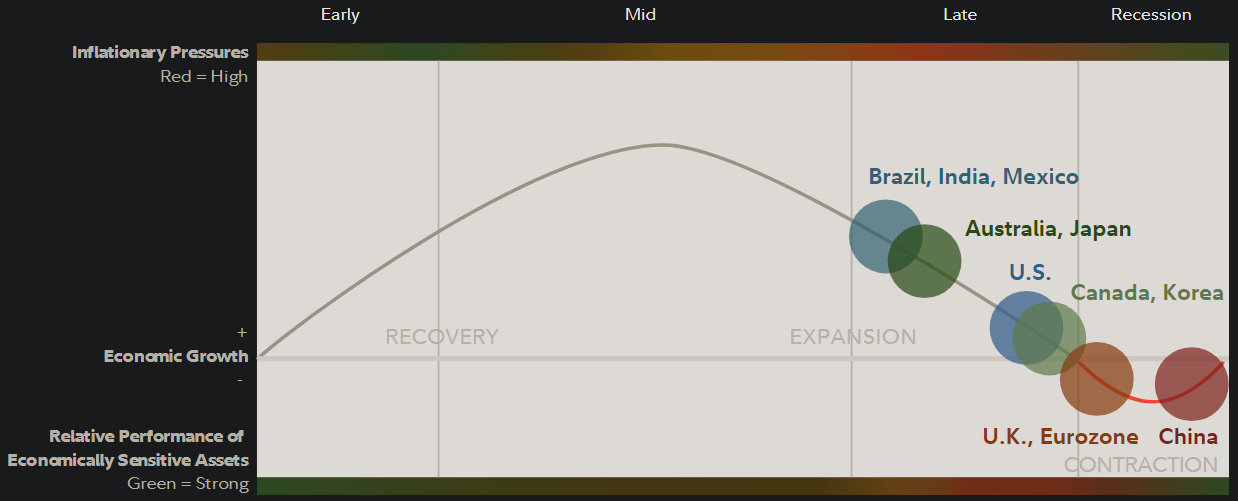

As of Q4 2022, Fidelity research suggests that much of the world is in a slowing-growth and/or contracting phase. The United States is expected to head into a recession next, based on moderating growth, tighter credit, earnings and inflationary pressures, tighter monetary policy (and fiscal policy also tighter as scaled by GDP), and weaker (i.e., higher) inventory/sales ratios.

{kind=link}

However, with IXN being tech-exposed (economically sensitive), and markets being forward-looking by about 6-12 months, it makes sense that IXN would bottom-out before an outright recession, provided that the recession is not likely to be protracted. Given the large scale of stimulus during the COVID-19 pandemic, I would argue that a recession is more likely now more than ever (now being between now and the end of 2023). If a recession does not occur given that inverse scale of the stimulus impulse "post-COVID", it would be surprising to say the least. If we assume a recession in 2023, and if we assume a soft recession given the still-low unemployment rate (3.7% in October 2022), we might have a serious bounce-back between the second half of 2023 or first half of 2024.

Therefore, it is more than possible that IXN has already bottomed in the current business cycle.

{kind=link}

As before, while a conservative estimate would take our ERP to a low figure, any forecasts that are even close to consensus earnings growth expectations take our implied IRR safely above 10% per year. That implies a surprisingly high ERP for a tech-oriented portfolio. While earnings growth estimates could disappoint, provided that IXN's portfolio remains robustly productive over the longer fund it is likely that portfolio will be able to continue to provide investors with returns via share buybacks, with near-term price discounts affording good long-term opportunities. I would continue to remain bullish on IXN with a long-term view.

For further details see:

IXN: Global Tech Stocks Should Bounce Back Even As The Economy Heads Into Recession