JBHT - J.B. Hunt: A Better Road Ahead But Shares Appear Fairly Priced

Summary

- J.B. Hunt is an industry leading transportation company that is fresh off their Q4FY22 earnings release.

- Though quarterly results were worse than expected, a positive outlook contributed to a reversal of the share price declines logged immediately following the release.

- While a mean reversion in inventory trends could prove to be a tailwind for the company, shares appear to be fairly valued at current pricing.

J.B. Hunt Transport Services ( JBHT ) is a transportation bellwether and an industry leader that is fresh off their Q4FY22 earnings release.

While topline results disappointed at first, with broad-based reported declines in volumes that resulted in weak operating income, shares reversed early losses to end the day higher by about 5%.

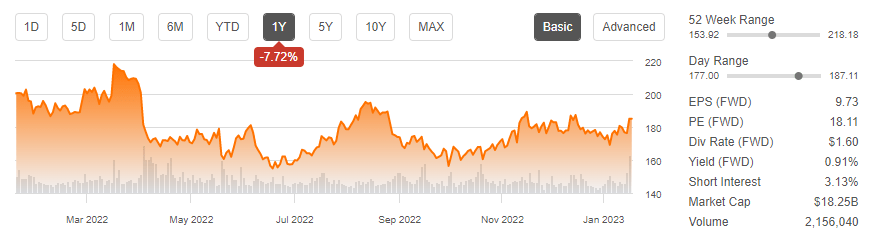

Since a prior analysis conducted shortly after their Q3 release, shares have gained just over 10% compared to the S&P 500’s ( SPY ) 6% gain over the same period. Over the past year, however, shares are still down over 7.5%, and they are currently trading at the midpoint of their 52-week range.

{kind=link}

Seeking Alpha - Basic Trading Data Of JBHT

An optimistic outlook for the 2023 demand environment could produce better than expected results in the coming periods. However, shares already appear to be fairly priced. Current trading multiples, for example, are at a premium to broader market indexes, and though down from historical averages, there may not be much further upside remaining.

And despite the optimistic tone, the overall macroeconomic environment still remains too unsettled and could prove more challenging than expected. While the stock makes for a good hold in existing portfolios for long-term investors, others may be better off using the company’s earnings release as an early barometer of the broader health of the macroeconomic environment.

Q4FY22 Earnings Recap

In the quarter and year ended December 31, 2022, JBHT reported total revenues of +$3.65B. This was up 4.3% YOY but short of estimates by +$140M. And when excluding fuel surcharge revenue, total revenues were actually down 3% from last year, due primarily to volume declines in their Integrated Capacity Solutions (“ICS”) and Intermodal (“JBI”) segments of 27% and 1%, respectively.

Q4FY22 Earnings Presentation - Comparative Summary Of Total Revenues By Year And Quarter

More specifically within individual segments, seasonally weaker than normal demand was cited as one factor weighing on Intermodal demand. This was due to generally lower activity levels leading up to the holidays. In October, for example, volumes were up 4%. But in November and December, volumes dipped 3% and 5%, respectively.

This was offset in part by improvements in rail velocity and customer detention of equipment. And overall segment revenue did increase 11% YOY, driven by a 12% increase in revenue per load. The revenue growth, however, was not enough to fully offset the impacts of lower volume and higher costs, as segment operating income still came in 8% lower.

In their ICS and Truckload (“JBT”) Segments, which is collectively lumped together as “Highway Services”, ICS weighed heavily on results, with a 33% decrease in revenue on volume declines of 27% and a 9% decline in revenue per load.

This weakness was offset in part by strength in JBT, which produced revenue growth of 6% or a decline of 2% when excluding fuel surcharge revenue on a 6% increase in load volume. In addition, their total average trailer count increased by about 3,900 units, which represents a 37% increase from the prior year; though it should also be noted that turns were down 21% from last year due to the softer freight market.

In their Dedicated Contract Services (“DCS”) unit, demand for their solutions remained strong during the quarter. Revenue was up 24% on greater revenue producing trucks and productivity gains. In addition, they sold about 330 trucks during the quarter, which is up sequentially.

And for the year, they’ve now sold over 2K trucks. That is well above their targeted range of 1K to 1.2K/year. The current backlog in the segment also held up, though moderation was noted.

With regards to their current liquidity and capitalization, JBHT maintained low leverage of just around 1x EBITDA and had cash on hand of +$52M. In addition, the company did not repurchase any shares during the quarter and had approximately +$551M remaining under their authorization.

Post-Earnings Insights

Slowing shipping demand due to weaker than expected activity leading up to the holidays, in addition to higher labor, maintenance, and insurance costs drove operating income down 13% during the quarter. A +$64M hit resulting from casualty claims also was a one-off that unexpectedly impacted results during the quarter.

These casualty claims could create a further headwind in future periods, as management noted that more severe claims are settling at significantly higher levels than historical averages, sometimes 5x to 10x more than five years ago. And though another one-time charge isn’t expected in 2023, premiums are expected to be up 15%, and their expected incurred losses are expected to increase as much as 30-35% as a result.

While rising insurance costs pose one threat, the overall outlook appears more promising. Though JBHT incurred broad-based volume declines during the quarter, the company expects demand to rebound in 2023 as companies gradually return to more normal ordering schedules. The normalcy in the purchasing environment is also likely to be accompanied by the continued fading of pandemic-driven disruption in supply chains.

Though guidance for 2023 was not provided, management does foresee the mean reversion in the inventory cycle occurring through the second half of the year, particularly in the summer and fall months. The optimistic tone resulting in a better than feared earnings release helped send shares about 5% higher after an initial post-release decline.

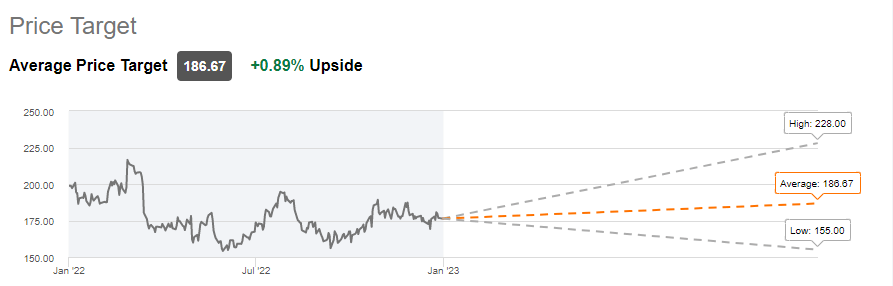

At 18x forward earnings, the stock trades slightly above the 17x forward estimate of the broader market index . In addition, the current trading price is in-line with average Wall Street price targets .

{kind=link}

Seeking Alpha - Average Wall Street Price Target Of JBHT

While shares can rebound higher on further optimism in the market environment, the stock doesn’t scream of a highly attractive buying opportunity. Sure, it’s current trading multiple is several points lower than the 5-year average, as is their EV/EBITDA multiple, which currently hangs around 10x compared to a historical average of 13.5x. But there is still not enough disconnect in the share price. While it may fit as an adequate holding for long-time shareholders, others may be better off elsewhere.

For further details see:

J.B. Hunt: A Better Road Ahead But Shares Appear Fairly Priced