JBHT - J.B. Hunt: A Good Buy In The Early Phases Of Recovery

2024-01-05 17:35:03 ET

Summary

- J.B. Hunt Transport Services, Inc. is expected to see a recovery in its revenue growth due to improving macroeconomic conditions and potential interest rate cuts.

- The company's Intermodal segment is experiencing improved volumes and pricing, while its Dedicated Contract Services segment is expected to see improved trends.

- The outlook for the company's Truckload, Final Mile Services, and Integrated Capacity Solutions segments also looks positive.

I last covered J.B. Hunt Transport Services, Inc. ( JBHT ) a year ago and, while I acknowledged that 2023 would be a tough year for the company, I expected J.B. Hunt to weather the slowdown well. The company’s intermodal business has a good track record of gaining market share from highway-only trucks given its cost-effectiveness. During the slowdown, when customers look to reduce costs, J.B. Hunt’s value proposition becomes apparent, helping it win new business and emerge stronger on the other side of the cycle.

2023 indeed turned out to be a tough year for the company. However, green shoots are emerging, with inventory destocking at customers nearing the end and the macroeconomic backdrop improving with potential interest rate cuts by the Federal Reserve this year expected to drive recovery. The freight volume recovery in the transportation business is usually followed by pricing recovery as well, which bodes well for the company’s revenue growth outlook. Further, operating leverage from higher volumes and higher prices should drive margins higher. The company is expected to post a double-digit EPS growth in FY24 and beyond, and I believe the stock is a good buy in the early phases of the recovery.

Revenue Analysis and Outlook

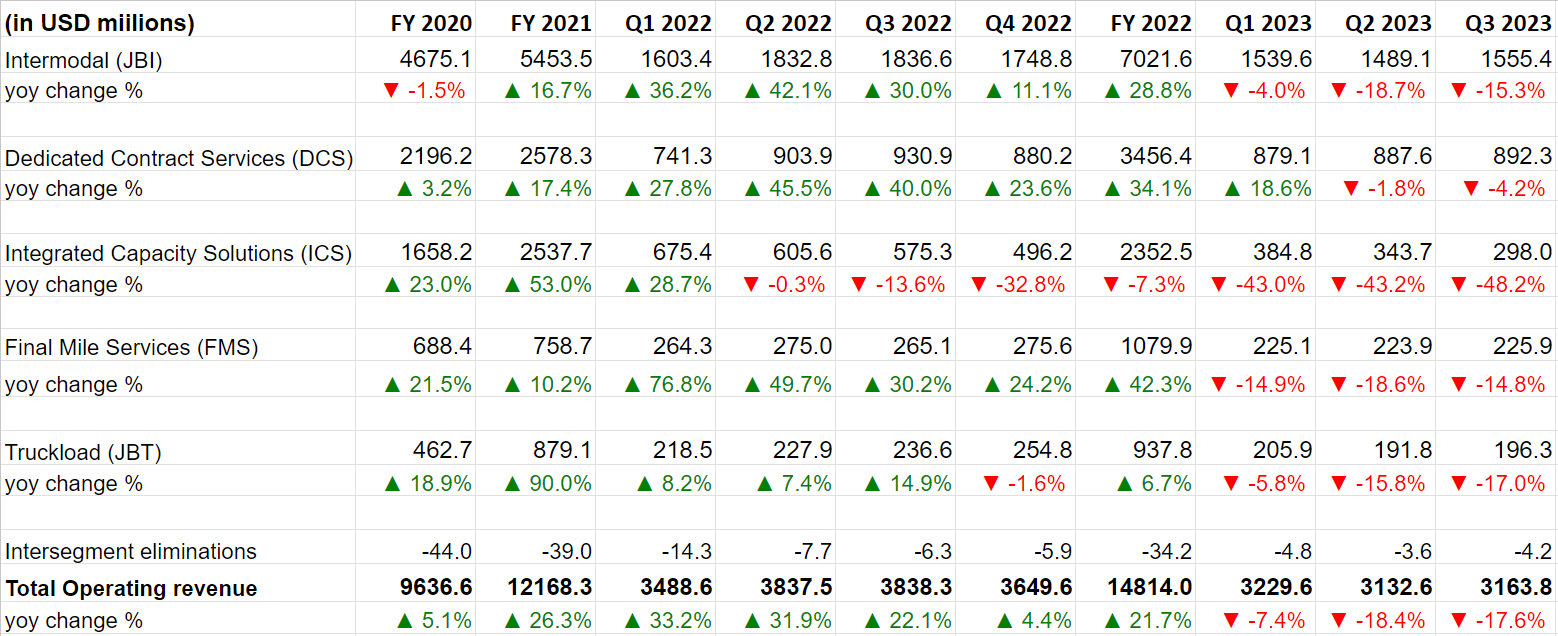

J.B. Hunt Transport Services, Inc. has seen a challenging freight environment, with declining freight prices and inventory destocking at its customers impacting its revenue growth in recent quarters. While the company’s Intermodal ((JBI)) segment saw Y/Y improvement in its volumes as the inventory destocking trend moderated in Q3 2023, declining freight prices continued to impact its revenues negatively and resulted in a 16.3% Y/Y decline in revenue per load (excluding fuel surcharge revenue). The Truckload ((JBT)) segment also saw a 17% Y/Y decline in revenue with lower pricing (~22% Y/Y decline in revenue per load ex. fuel surcharge) more than offsetting a mid-single-digit increase in volume.

Further, the company's revenue growth was also negatively impacted by a 37.7% Y/Y decline in volume and a 16.9% Y/Y decline in revenue per load in the Integrated Capacity Solutions ((ICS)), a 20.1% Y/Y decline in stop count in Final Miles Services ((FMS)), and a decline in average revenue producing trucks for its Dedicated Contract Services ((DCS)). These negative factors resulted in a 17.6% Y/Y decline in total operating revenue to $3.16 billion. Total operating revenue, excluding fuel surcharge revenue, declined 15% Y/Y in the third quarter.

JBHT’s Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company’s revenue outlook looks positive.

The company’s biggest segment, JB Intermodal, was impacted by inventory destocking last year, but these destocking headwinds started moderating from mid-2023. As a result, the volumes in this segment improved from -1% Y/Y in July to +1% Y/Y in August and +4% Y/Y in September. The October trends were going strong as per management commentary during the last earnings call and, given the sentiment improved meaningfully in November onwards with all the commentary around potential interest rate cuts in 2024 and a good holiday sales season, I am expecting a strong Q4 earning report and positive commentary around the volume recovery on the upcoming earnings call (Q4 earnings scheduled for post-market January 18th).

The pricing was also a big concern in this segment (and for the company overall), as the contracts were getting rebid at lower prices but with the freight recession likely over, I believe pricing should also follow volumes and improve as 2024 progresses.

In the long term, the prospects of this segment look solid given the strong value proposition Intermodal transport offers in terms of cost efficiencies and lower carbon emissions versus highway-only trucks.

The company’s second-largest business, Dedicated Contract Services, usually has long-term contracts from 3 to 10 years and follows a cost-plus pricing model, making it relatively immune during the slowdown. The contracts in this segment have index base price escalators and the company was able to see improved productivity (revenue per truck per week) excluding fuel surcharge in this business in Q3 2023. I expect productivity (ex-fuel surcharge) to remain resilient. The segment’s churn rate which has been worrying many investors is also likely near the bottom. The company did a good job in terms of signing new deals for the deployment of trucks, however, due to higher-than-expected customer churns, there were 370 fewer revenue-producing trucks in the fleet in Q3 2023 compared to same quarter prior year. However, the good news is the number of revenue-producing trucks in the fleet improved sequentially in Q3 2023 versus Q2 2023. With the company doing a good job in terms of signing new deals and the freight recession likely nearing end, I expect this segment to see improved trends moving forward.

JBHT’s Q3 2023 Revenue Mix by Segment (Company’s Q3 2023 Earnings Presentation)

The outlook for three smaller segments, Truckload ((JBT)), Final Mile Services ((FMS)), and Integrated Capacity Solutions ((ICS)) also look good.

JBT is benefiting from J.B. Hunt 360 box service, which is gaining good traction and has helped the segment post good volume growth outperforming the broader trucking market. The continued outperformance coupled with a potential end market recovery in 2024 from favorable macros (inventory destocking ending, interest rate cuts driving demand) bodes well for the growth in this segment.

While the company’s Final Mile Services ((FMS)) segment, which transports big and bulky items to customer homes, saw some headwinds last year due to a slowdown in furniture deliveries, the longer-term outlook remains healthy and management noted a strong sales pipeline for this business on the last quarter’s earnings call.

The company’s ICS segment has been in a relatively tough spot of late due to normalization in the demand for truck booking services as the supply chain constraints have eased compared to the last couple of years. Management is also focusing on improving revenue quality which resulted in reducing low-margin revenues. However, I am not too worried about this as management noted the gross profit dollars have started seeing sequential improvement in this segment. Further, the company recently acquired BNSF’s logistics business (B N Logistics Ltd) ,which according to management should add ~$100 mn to the segment’s revenues per quarter. So, I expect improvement in this segment’s growth in 2024.

The company also has a strong balance sheet with a net leverage of less than 1x and is well positioned to invest in both organic and inorganic growth opportunities as the broader macroeconomic environment improves in 2024.

Margin Analysis and Outlook

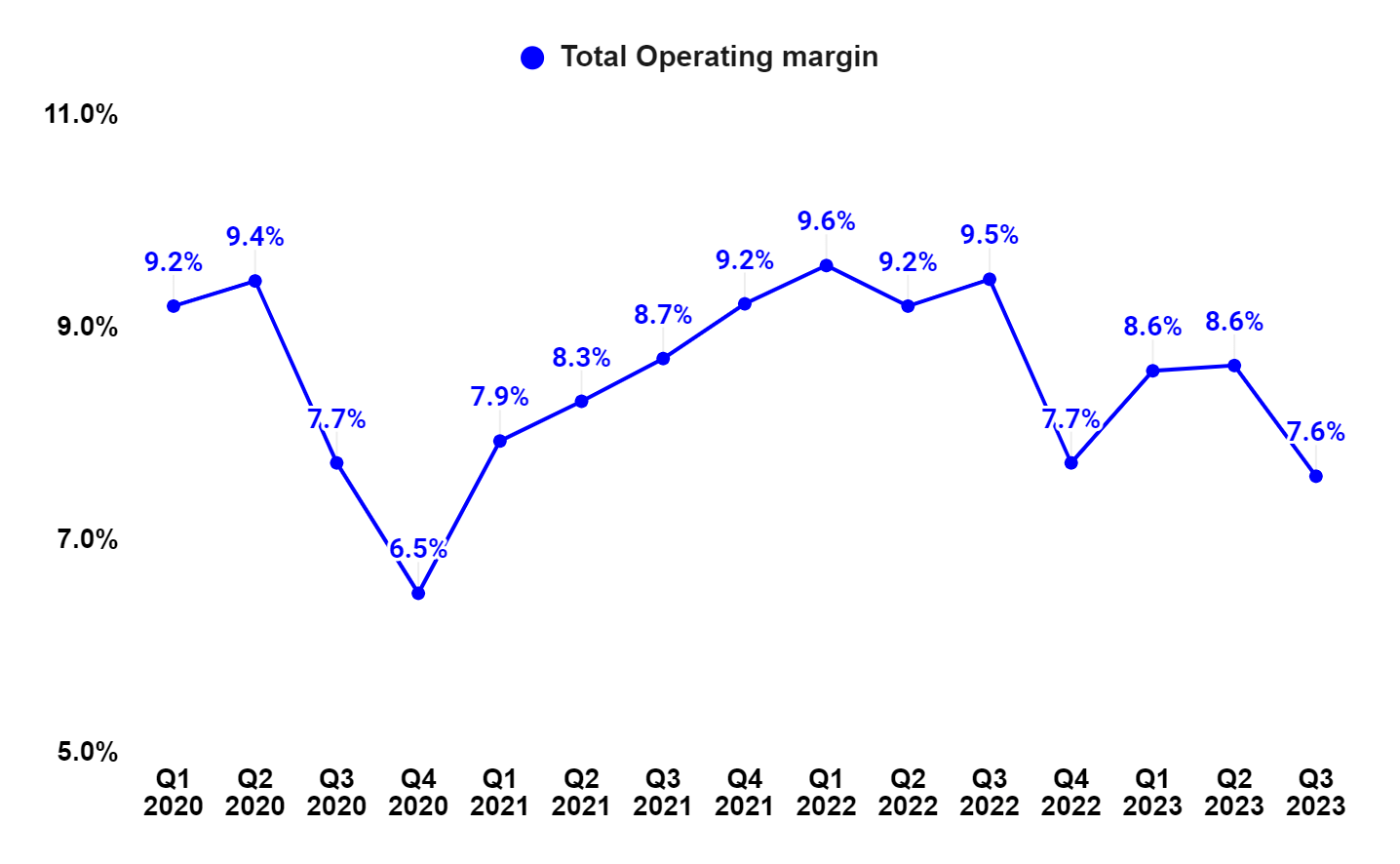

In Q3 2023, the company’s operating margin contracted by 190 bps Y/Y to 7.6% due to lower revenues across all business segments, higher equipment-related costs, and increased insurance and claims expenses.

JBHT’s Total Operating Margin (Company Data, GS Analytics Research)

{kind=link}

Moving forward, the company’s margins should benefit from volume leverage. As discussed in the revenue analysis, with headwinds from inventory destocking ending and improving macroeconomic outlook given the probable rate cuts by the Federal Reserve in 2024, I believe the Freight recession is over and we should see improved volumes in 2024. Increasing volumes should result in better utilization of equipment and higher leverage on fixed costs benefitting margins.

Further, the pricing should also improve as the volume recovery takes hold helping margins. The inflation has been running quite high for the last couple of years, and I expect it to return to normalized levels as 2024 progresses. Overall, the benefit from operating leverage and pricing should be able to offset cost inflation, resulting in improved margins in 2024 and beyond.

Valuation and Conclusion

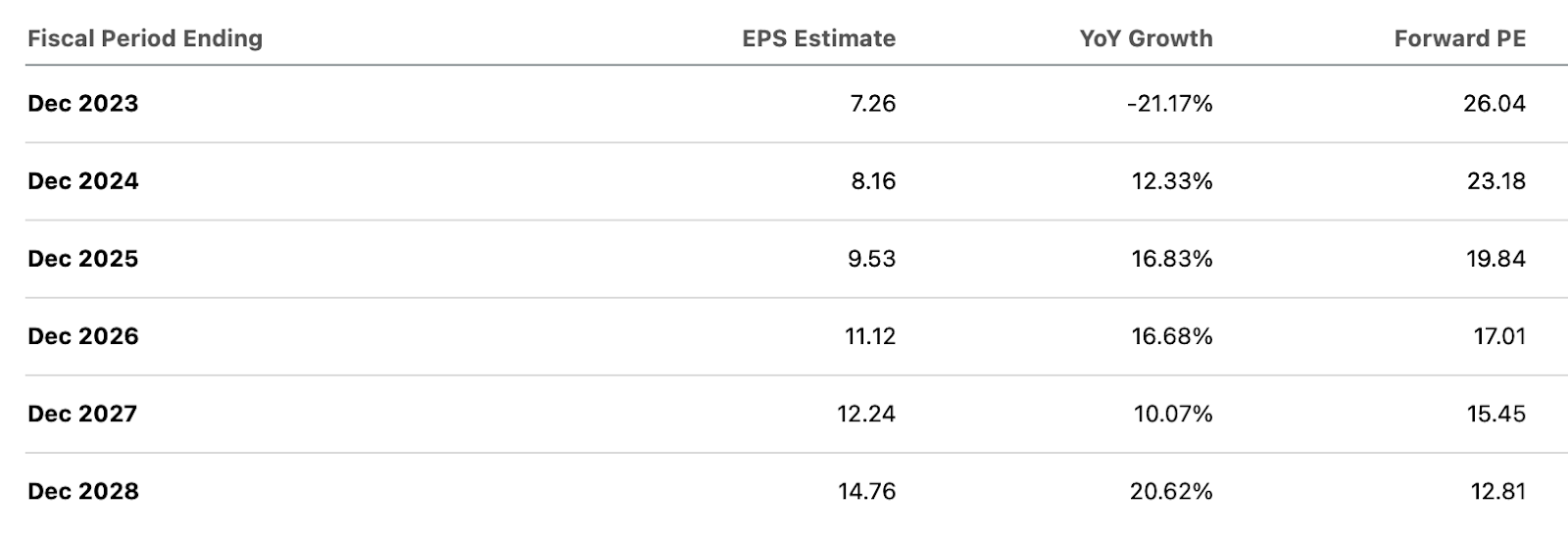

JBHT is currently trading at a 23.18x FY24 consensus EPS estimate of $8.16 and a 19.84x FY 25 consensus EPS estimate of $9.53. Over the last 5 years, the company has traded at an average forward P/E of 22.38x.

While the company’s P/E multiple on FY24 earnings is slightly higher than its historical averages, its P/E multiple on FY25 EPS is lower. Cyclical companies typically trade at a higher valuation multiple compared to their long-term averages near the bottom of the cycle and during the early phases of recovery when their earnings are at depressed levels. This is called the Molodovsky effect .

JBHT has strong growth prospects, and if we look at the sell-side estimates, it is expected to post double-digit EPS growth in FY24 and beyond.

JBHT Consensus Estimates (Seeking Alpha)

{kind=link}

I find the current valuation reasonable considering we are in the early phases of recovery . J.B. Hunt Transport Services, Inc. has good long-term secular growth prospects driven by market share gains in its Intermodal business. Hence, I have a buy rating on the stock.

For further details see:

J.B. Hunt: A Good Buy In The Early Phases Of Recovery