JBHT - J.B. Hunt Has Some Bad News

2023-04-18 12:08:28 ET

Summary

- J.B. Hunt just reported its 1Q23 earnings, which showed a mix of demand and pricing headwinds, resulting in poor revenue and EPS numbers.

- The company sees a trucking recession and focuses on margin protection while trying to remain flexible for the next upswing in demand, as it aims to capture more market share.

- While shares are trading at an attractive price, I expect more downside if economic sentiment remains poor.

Introduction

Earnings season is heating up. One of the first industrial companies to report its earnings is transportation giant J.B. Hunt ( JBHT ). This Arkansas-based company isn't just an interesting dividend growth stock, but it is also a great economic indicator, thanks to its massive footprint in the North American surface transportation industry, including intermodal, truckload, and brokerage. The company's numbers and insights are valuable, even for people who don't own JBHT shares.

In my case, I own three railroads, and I have various transportation stocks on my watchlist and model portfolios, which makes every JBHT earnings call a must-follow event.

That said, the company's 1Q23 earnings were poor. Both sales and EPS came in below estimates, while the company expects prolonged weakness on the horizon. It even used the R-word.

In this article, we'll discuss all of this and more.

So, let's get to it!

Why JBHT Matters

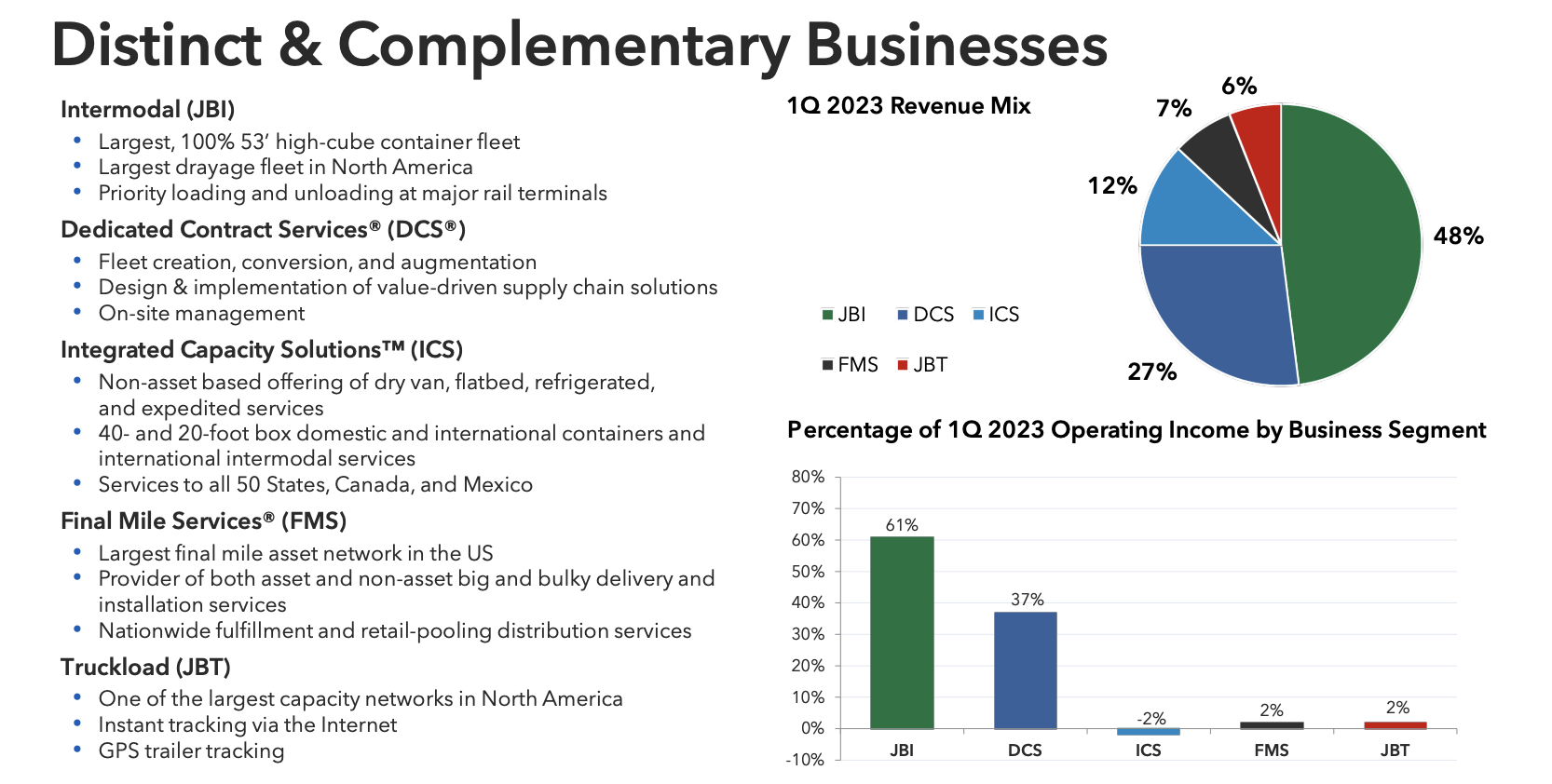

JBHT has an $18.3 billion market cap. That isn't extremely large. However, the company's footprint in surface transportation is huge. Founded in 1961, JBHT has grown into a key player in logistics. In its JBI (Intermodal) segment, which accounted for 48% of 1Q23 revenues, the company has long-term contracts with Class I railroads and related carriers. This segment includes close to 100,000 containers and a fleet of more than 6,000 trucks. This makes it the largest drayage fleet in North America.

In its Dedicated Contract Services segment, the company specializes in converting and creating private fleets for replenishment and specialized equipment in supply chain solutions for transportation networks.

{kind=link}

The remaining quarter of its revenue comes from asset-light integrated capacity solutions, final mile services, and truckload operations.

In other words, the company's numbers matter, as it doesn't just tell us how JBHT is doing, but also what is going on in other areas of the economy. Especially in this scenario, these comments are important.

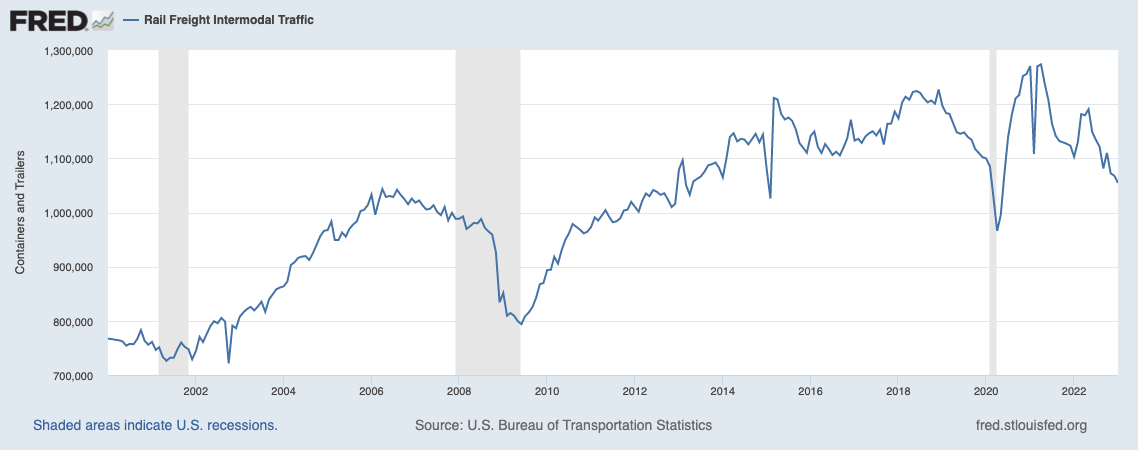

For example, going into this year, intermodal freight traffic was down to fewer than 1.1 million containers.

{kind=link}

Meanwhile, Southern California truckload tender volumes were down 23%. That's below April 2019 levels and a bad sign of weak volumes at the nation's largest ports.

{kind=link}

On top of that, the ISM Manufacturing Index points to more downside, including lower manufacturing production.

Wells Fargo

Now, let's see how JBHT did and what it had to say!

Some Bad News From J.B. Hunt

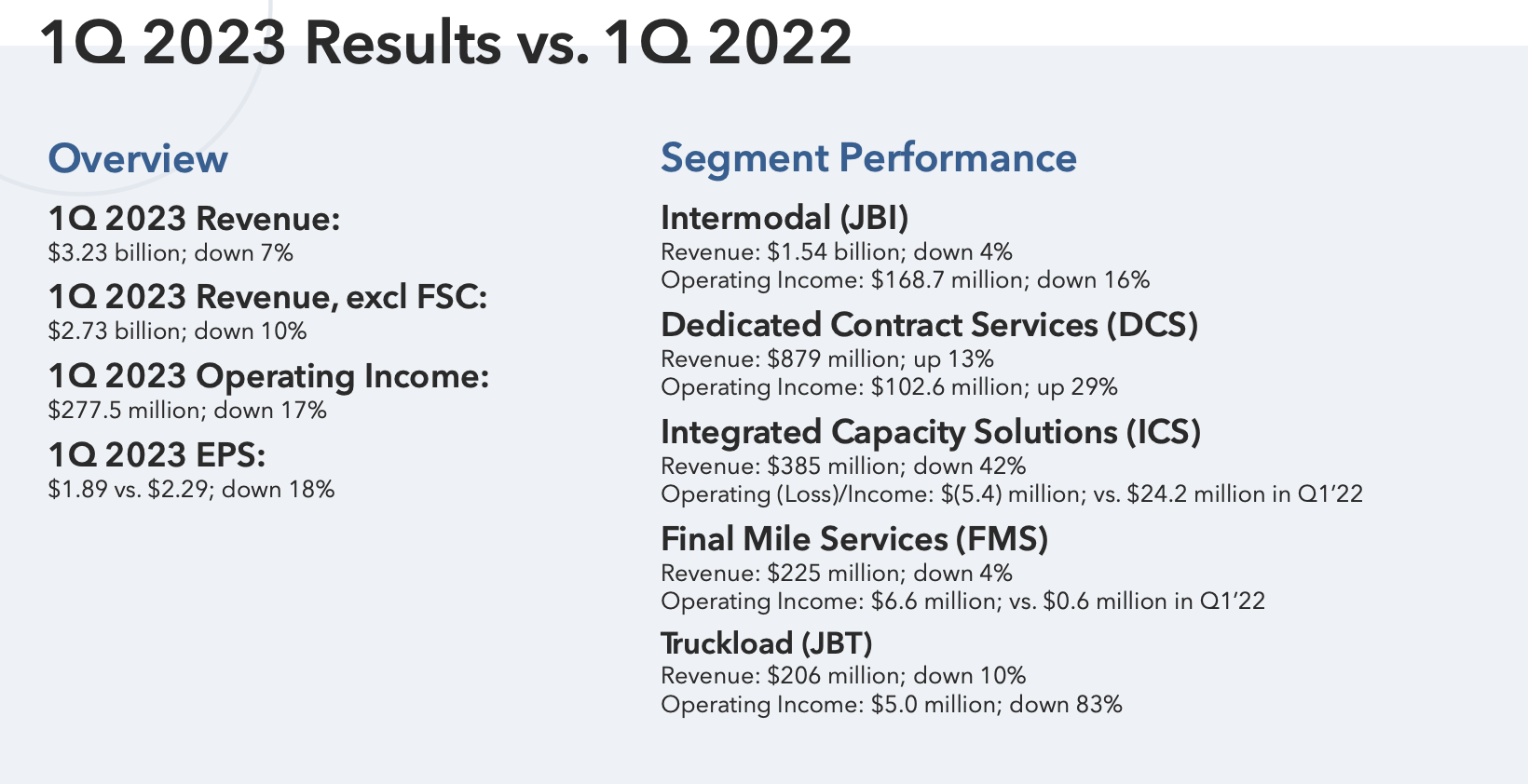

In 1Q23, JBHT generated $3.23 billion in revenue. That number was $180 million below estimates and 7.4% below its prior-year quarter result.

GAAP EPS came in at $1.89, which was $0.11 lower than expected and 17.5% below its 1Q22 result.

{kind=link}

In the earnings call that followed, JBHT President Shelley Simpson didn't sugarcoat anything. She came out explaining what we're dealing with here when it comes to the bigger picture.

To start, we're in a challenging freight environment where there is deflationary price pressure for an industry that continues to face inflationary cost pressures . Simply stated, we're in a freight recession .

CFO John Kuhlow followed with an explanation of the poor revenue result. He explained that declining financials was caused by lower freight volumes, moderating pricing trends, and inflationary cost pressures in areas such as salaries and wages, insurance and claims, and parts and maintenance expenses.

Using FreightWaves data, we see that the National Truckload Index, which is based on an average of booked spot dry van loads from 250,000 lanes, is displaying 31% lower spot rates. This is a great indicator of pricing in the industry, which is confirmed by JBHT's comments and numbers.

FreightWaves

Based on this context, let's dive deeper into the Intermodal segment. Not only is this segment responsible for 61% of 1Q23 operating income, but it is also a great indicator of railway transportation and related industries.

Intermodal President Darren Field noted that demand for Intermodal capacity was tempered due to lower imports and elevated inventory levels across the supply chain, resulting in a decline of 5% in volumes year over year. Monthly volumes were down 2% in January, 4% in February, and 8% in March. However, Field pointed out that Eastern volumes were up 1%, showcasing growth in the most truck-competitive market, despite a depressed truckload environment.

The operating ratio increased to 89% as a result of lower margins.

FreightWaves

All of these observations are in line with my own findings. Retailers continue to reduce inventory, resulting in lower intermodal demand. Moreover, Eastern volumes are outperforming Western volumes, as Eastern ports are increasingly taking away business from Western ports.

However, the trend remains down. The chart below shows intermodal volumes until week ten from CSX ( CSX ), the largest Eastern railroad in the United States.

CSX Corp.

Furthermore, Field emphasized that JB Hunt's Intermodal franchise offers significant value to customers by converting freight from highway to intermodal, reducing costs and supporting fuel cost and carbon emission savings. Hence, he concluded his remarks by expressing optimism about the potential for significant growth in the Intermodal business and unlocking value in the network for the benefit of stakeholders as the bid season progresses.

Here, I agree with that as well. Railroads are in a terrific spot to benefit from secular growth. Both challenges in the trucking industry and efforts to decarbonize the industry are beneficial for intermodal. Unfortunately, this is a long-term trend. It won't be a major factor in offsetting current weakness, especially because railroads are very slow to adapt.

The good news is that the company's J.B. Hunt 360 platform (its digital support platform) continued to impress.

In the truckload segment, demand for drop trailing capacity was strong. 360 Box volumes were up by double digits.

With regard to the outlook, the company used the word "cautious" a number of times, which makes sense, as companies are not likely to comment on anything specific in a macroeconomic environment as volatile as the current one.

This is how CEO John Roberts put it:

Our customers want more of what we do when they need it. Import volumes are clearly not strong. And so there is question marks out there about what will happen in the second half of the year. And so, as the quarter went on, I would say, we're slightly less optimistic . We've said that multiple times. Outside of that, I don't know what else to say other than I know our customers do want our capacity as soon as the import volumes return to normal .

Basically, JBHT is doing a great job handling the decrease in volumes while staying flexible to bounce back when volumes pick up again. This smart approach puts them in a good position to grab a bigger share of the market once customer volumes start to recover.

The company estimates that its system is built to handle a 15% to 20% increase in volumes without having to make major adjustments. That's good news for margins when demand rebounds.

Look, in terms of the margin profile as we move forward, we continue to be confident in our ability to take cost out as we pour volume over the top. We have long term margin targets that are not being changed, and we're confident in our ability to win and grow with our customers at acceptable returns.

What Does This Mean For Shareholders

The most straightforward answer is: shareholder returns will remain poor until demand rebounds. After all, the stock remains highly dependent on economic expectations.

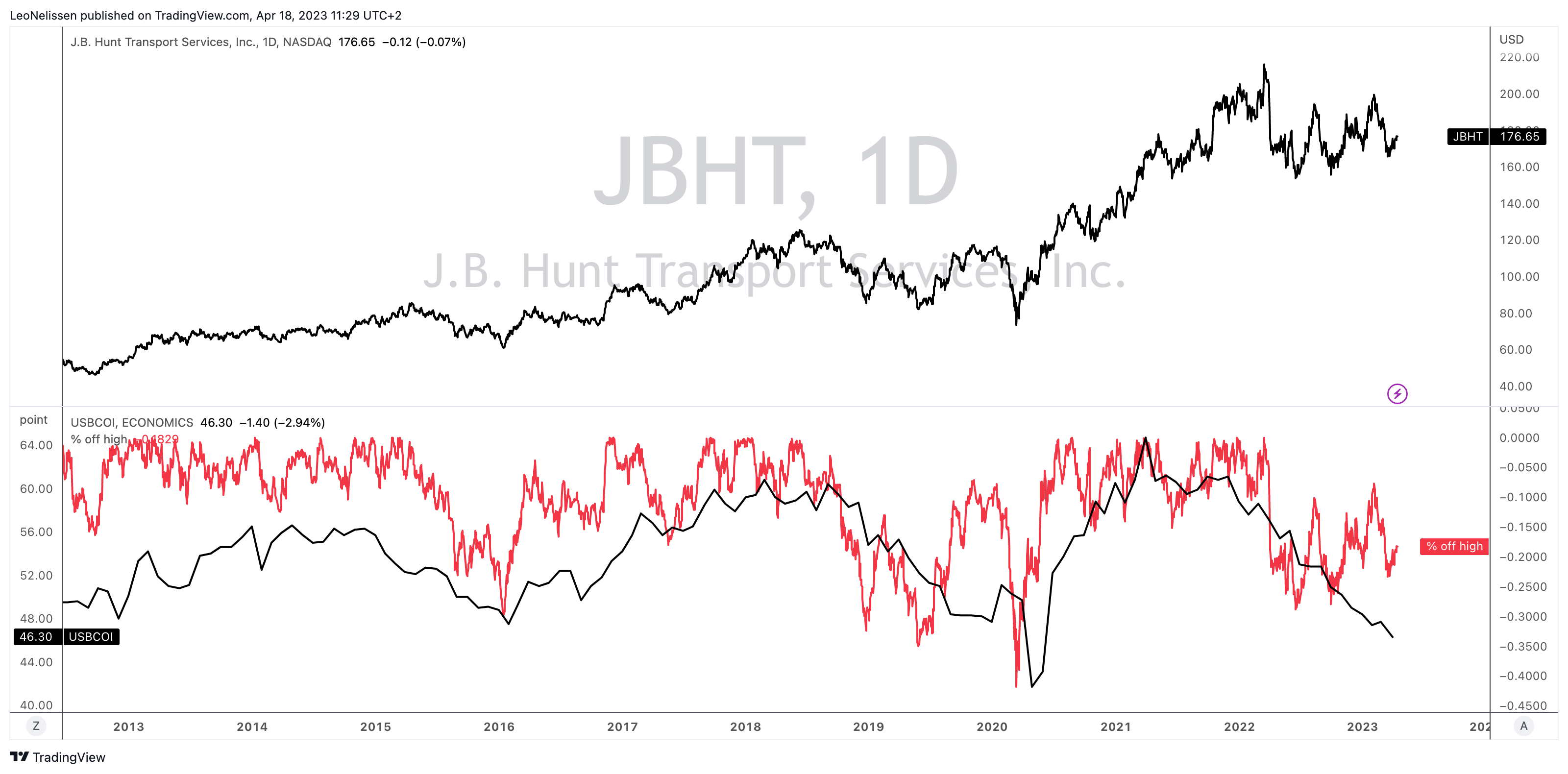

To visualize this, I made the chart below.

- Upper part : the upper part of the chart below displays the JBHT stock price.

- Lower part : the lower part displays the ISM index I briefly mentioned in this article (black line) and the total sell-off from JBHT's all-time high.

{kind=link}

JBHT shares are currently less than 20% below their all-time high. That is a decent correction, yet not what we should expect if economic growth remains weak. In that case, the risk is to the downside.

Historically speaking, the risk/reward gets really good when shares are between 25% and 30% below their all-time high.

That said, this year, the company is expected to do $1.9 billion in EBITDA, down slightly from $2.0 billion in 2022. That number is expected to rebound to $2.1 billion in 2024 and $2.3 billion in 2025. Essentially, it's a soft-landing scenario where demand will bottom close to current levels.

The company is trading at 9.9x EBITDA, which is far from overvalued. Especially with the longer-term impact of J.B. Hunt 360 and additional capacity, the company should be trading at 11x EBITDA.

Unfortunately, without a rebound in global economic growth expectations, that's not happening.

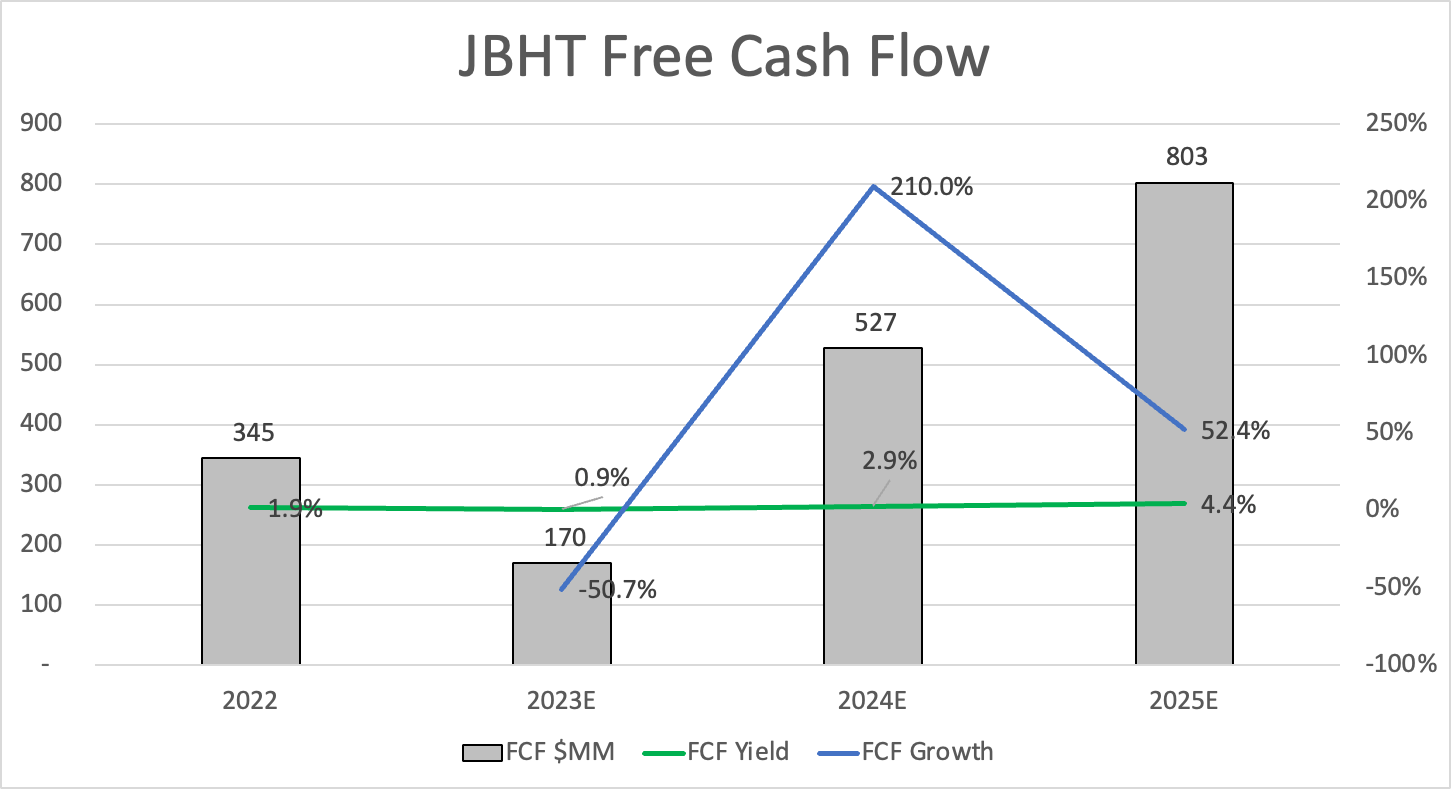

Free cash flow expectations are also subdued. The company is unlikely to reach a >4% free cash flow yield before 2025.

{kind=link}

Over the past ten years, the median free cash flow yield was close to 2%. That is not a lot.

It's one of the reasons why the company was limited in returning cash to shareholders. Its dividend yield is 1%.

Nonetheless, a total return of 180% over the past ten years is far from bad.

I expect JBHT to outperform the market if it gets a boost from demand. At that point, the company will be able to boost its margins as it uses its excess capacity to remain ready to capture market share. For now, this is keeping margins subdued. On a long-term basis, it will likely pay off.

Takeaway

JBHT had a very tough quarter. Demand was down, pricing suffered, and input costs remained high.

The company struggled with very slow intermodal volumes and headwinds related to the ongoing downturn in the United States and abroad, which impacted exports.

Furthermore, these developments are likely an indication of what we can expect from other transportation companies as well.

If this downturn continues, the stock could see another 10% to 15% downside.

That said, on weakness, the stock becomes a buy. JBHT is in a good position to benefit from a future demand rebound. It has excess capacities, an increasingly successful digital platform, and secular intermodal benefits.

For now, however, I remain neutral on the stock.

For further details see:

J.B. Hunt Has Some Bad News