JBHT - J.B. Hunt: The Freight Environment Is Clearly Challenged

2023-04-19 03:14:32 ET

Summary

- J.B. Hunt is a freight and transportation bellwether that provides services to customers across North America.

- The company is an early reporter in the standard quarterly earnings season. And their results could provide a peak into what's ahead in the macroeconomic environment.

- Recent results didn't provide much confidence, as management acknowledged that they are in fact in a "freight recession."

- Given current market dynamics, it's hard to foresee significant upside potential in the periods ahead. As such, I am maintaining a neutral outlook on the stock.

J.B. Hunt ( JBHT ) is a freight and transportation bellwether that is a component of the Dow Jones Transportation Average ( DJT ).

The company operates five primary segments : Intermodal ("JBI"); Dedicated Contract Services ("DCS"); Integrated Capacity Solutions ("ICS"); Final Mile Services ("FMS"); and Truckload ("JBT"). Of the five, JBI and DCS, together, represent the lion's share of total revenues, at over 70%.

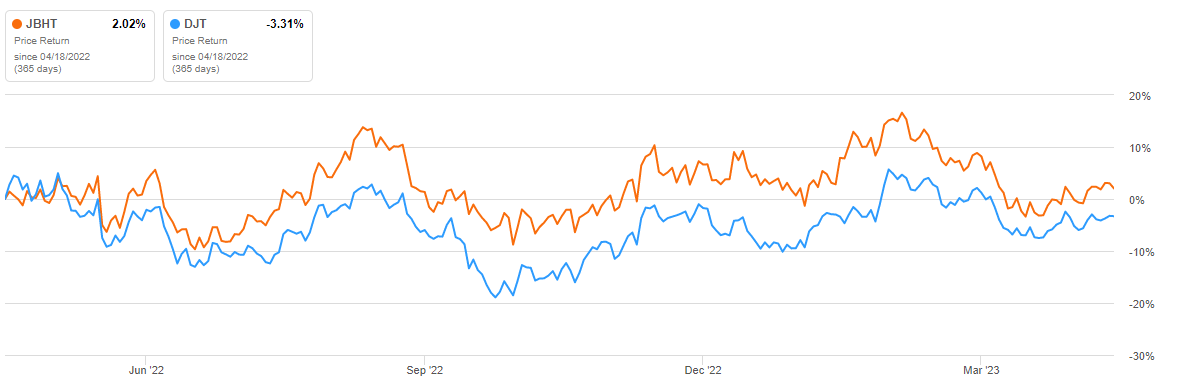

Over the past year, JBHT has outpaced the DJT, gaining 2% over this timeframe versus a decline of 3% logged by the broader index.

Seeking Alpha - 1-YR Performance Of JBHT Compared To The DJT Index

{kind=link}

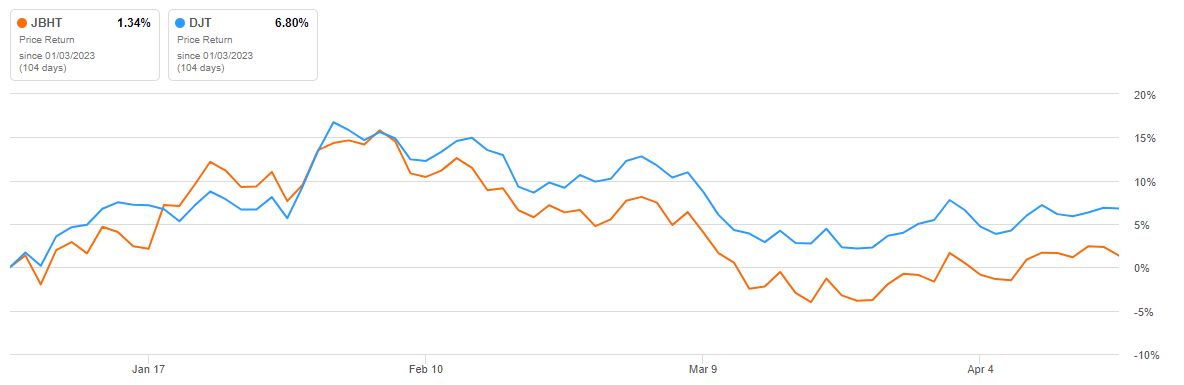

YTD, however, they are trailing at a larger margin than they have over the past three years, where they've returned about 73% compared to the broader averages' 80% returns.

Seeking Alpha - YTD Performance Of JBHT Compared To The DJT Index

{kind=link}

The stock's performance provides some view of the broader macroeconomic landscape in the freight environment. And since they are early reporters, investors can glean some sense of what's to come based on their results. Following results, the road ahead appears bumpy. Import volumes are down and the company is operating on deflationary pricing while still incurring inflationary pressures in salaries and other charges. Given the current outlook, it's hard to foresee much upside ahead. As such, consistent with my prior view , I remain neutral on the stock.

An Overall Decrease In Quarterly Revenues

JBHT reported total revenues in the first fiscal quarter of 2023 of +$3.2B. This was down 7% on a YOY basis due primarily to weakness in all reportable segments, except for DCS, which exhibited growth of 13% on a 7% increase in average revenue producing trucks.

Q1FY23 Investor Presentation - Summary Of Total Revenues By Fiscal Year And By Comparative Quarters

Lower Intermodal Volumes

Weaker overall freight activity, especially on import-related freight, held back overall intermodal volume during the quarter. Compared to last year, total volume was down 5%, though strength in their Eastern network did provide some reprieve, up 1%, which offset, albeit slightly, the 9% decline in transcontinental loads.

The Intermodal volume declines more than offset the 1% increase in gross revenue per load. In addition to lower volumes, JBHT also incurred higher professional driver and non-driver wages and benefits, as well as insurance-related costs. Significantly lower net gains from the sale of equipment further subtracted from their bottom-line performance, which was down 16% in the segment.

Rate Headwinds In Highway Services

Highway Services, which is comprised of their ICS and JBT segments, also reported broad-based declines during the quarter. Reported revenues in ICS were down a more notable 42% than JBT's 10% decrease. In addition, JBT benefitted some by strong, double-digit volume growth in 360box.

Nevertheless, contractual and transactional rates were down in their JBT business, which in turn resulted in a 22% decline in ICS' revenue per load. And the impact was even greater since contractual volumes represented 63% of the unit's total load and 64% of total revenue compared to 44% and 42% in the same period last year.

Operating income declined in both units, yet JBT remained in the positive at +$5M. This compares to an operating loss the other way in ICS. Despite the decline in ICS, gross profit margins improved to 13.4% compared to 12.8% last year. This was due in part to lower personnel-related expenses and reduced technology costs.

Milder Losses In FMS

Revenue declines in FMS added to quarterly losses. But the extent of the declines in the segment were less pronounced, at 4%. This was due to the accretive benefits of their recent acquisition activity, as well as improved revenue quality at underperforming accounts.

In addition to milder revenue losses, FMS reported a +$6M increase in operating income due to better cost management and revenue quality.

Positive Contributions From DCS

Strong performance in their DCS segment partially offset the negatives reported elsewhere. Segment revenues and operating income were both up 13% and 29%, respectively. This was due to greater productivity and utilization of assets. The segment also logged a 7% increase in average revenue producing trucks during the period.

Positive customer retention rates, which held above 98%, and a boost from the movement of JBT operations to DCS also contributed favorably to the segment's quarterly results. These benefits were partially offset by higher wages and other expenses, such as maintenance and insurance-related costs.

Looking ahead, the environment is expected to be challenged due to moderated demand for freight capacity, as well as fading trends in pricing strength. The company's balance sheet and liquidity position, however, provide a strong protective buffer against these threats.

And despite the moderation, management still expects to spend between +$1.5B and +$2B in capital investment in 2023. In addition, they foresee allocating +$400M to +$500M to real estate. And as a result of the prior lack of availability of new equipment due to the supply chain dynamics at the time, a large portion of their 2023 tractor capital is expected for replacement needs.

Post-Earnings Insights

On their conference call, management acknowledged the challenging freight conditions and noted that they were in fact in a freight recession. And JBHT's Q1 results reflected this sentiment, as they clearly didn't impress .

Revenues and earnings both missed expectations and segment results were largely negative, save their DCS unit, which reported strength in both their top and bottom-line results. But despite the strength, moderation was still noted.

The segment did report 200 trucks of new business during the quarter, which creates an optimistic outlook of hitting targets for the year. But of the 426 truck adds during the quarter, a large portion were from transfers from their JBT segment. Excluding these transfers, total adds were just 28 units.

Additionally, though a net additional 541 revenue producing trucks were in the DCS fleet at the end of the quarter compared to last year, there was 49 less on a sequential basis.

And in other segments, performance moved in opposite directions than in prior periods. In their JBT segment, for example, greater haul lengths have previously been matched with greater revenues per load. But in the current quarter, there was a reversal in that dynamic, as the company realized lower revenues per load on rising haul lengths.

Rising expenses, particularly labor- and insurance-related costs have also hit segment margins. Looking ahead, I expect the trend to continue as the deflationary price pressures continue to co-exist with an environment where operating costs linger higher for longer.

At nearly 20x forward earnings and at the mid-point of their 52-week range, it's hard for me to justify new or further positioning in the stock at these prices. Current Wall Street estimates peg shares fairly valued at about the $190/share range, which seems appropriate. At those prices, shares would have upside potential of less than 10%, which I don't view as acceptable in the current rate environment. As such, I am staying neutral on this freight bellwether.

For further details see:

J.B. Hunt: The Freight Environment Is Clearly Challenged