JBHT - J.B. Hunt: The Good The Bad And The Ugly

Summary

- The good: J.B. Hunt is doing a tremendous job improving its business, offering new services, and attracting a lot of new clients. Moreover, trucking demand might be bottoming.

- The bad: the company missed 4Q22 earnings estimates as it suffers from economic weakness, high inflation, and investment-related costs.

- The ugly: leading economic indicators are not bottoming but indicating more pain ahead.

- JBHT remains attractively valued with a great long-term growth outlook. However, I remain cautious and would love to see a drop to $160 per share for a better risk/reward.

Introduction

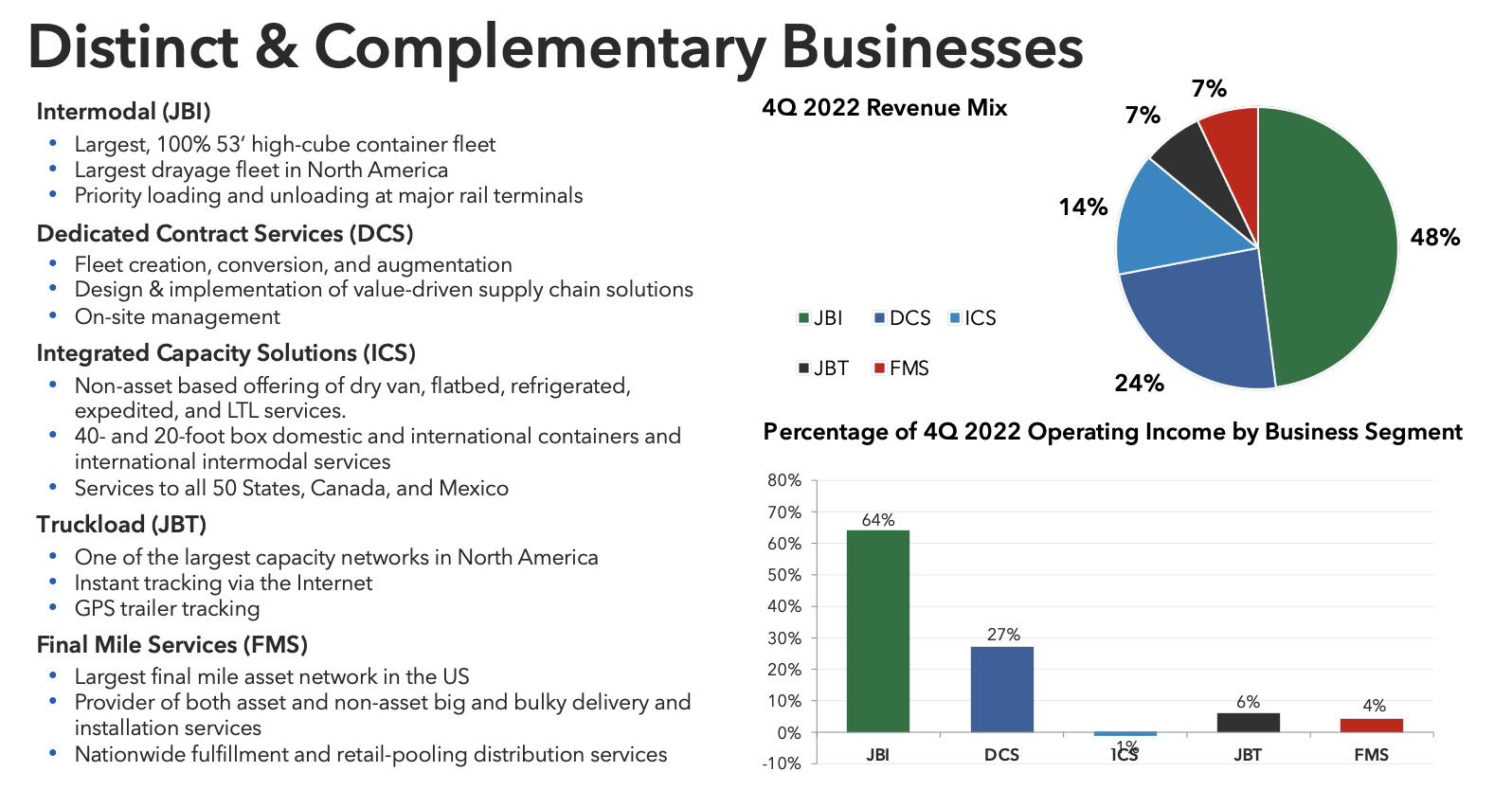

There are at least two reasons why I like covering J.B. Hunt Transport Services (JBHT) . Reason one is the company's impressive turnaround from a boring trucking and intermodal company to a streamlined tech-focused transportation powerhouse.

J.B. Hunt is doing a tremendous job accelerating growth. The company is not only streamlining its existing business but actively using technology to deeper penetrate the market for brokerage services and related.

Margins are rising, along with an accelerating uptrend in sales, EBITDA, and free cash flow after 2022. - Article June 2022

Reason two is the company's dominant position in the North American transportation industry, which means its financials and comments tell us a lot about the state and outlook of the economy.

While the company missed both revenue and EPS estimates in its fourth quarter, analysts were bullish thanks to higher profitability. Moreover, prominent voices are calling for a bottom in the industry, which is fueling investors' demand for shares.

In this article, I'll give you the details and my thoughts on where JBHT might be headed.

So, let's get to it!

Some Economic Background Info

The earnings season has just started, and I have to say that my expectations are low. Leading economic indicators like the ISM index show that both production and new orders are now in contraction territory.

Wells Fargo

Meanwhile, the Fed is still hiking rates to fight inflation, which is making the markets nervous.

The same goes for analysts, which are busy downgrading earnings estimates.

Goldman Sachs

According to Bloomberg :

"Profit expectations now stand as arguably the single biggest contrary indicator to the burgeoning optimism. Estimates are moving down at a rate that in recent history has always presaged a recession."

Here's What Happened To JBHT

The headline numbers were nothing to write home about. The company generated $3.65 billion in revenue, which is an improvement of 4.3% year-on-year but $140 million less than expected.

GAAP EPS came in at $1.92 in the fourth quarter, $0.52 short of estimates.

{kind=link}

J.B. Hunt, which generates roughly half of its sales in its massive intermodal business, is seeing a trend toward sourcing reliability and cost efficiency. During the pandemic, the focus was almost solely on capacity, according to JBHT President Shelley Simpson :

We see the shift occurring now where customers are putting more value on cost or how to save the money and on service quality as capacity is less difficult to source. We believe our suite of services can and will present our customers opportunities to save money with our industry leading intermodal franchise, highly engineered dedicated capacity, a scaled asset light highway services offering, and one of the largest Final Mile Services in North America.

The company entered 2023 with a cautious view on demand, yet the ability to serve changing customer needs.

When it comes to demand, the company struggled in its intermodal business. Volumes were down 1% in the fourth quarter as transcontinental loads were down 7%. According to the company :

Demand for intermodal capacity was seasonally weak in the fourth quarter, while rail velocity and performance made further progress.

Note that the company mentioned further improving rail velocity. That's good news for everyone investing in and watching railroad stocks.

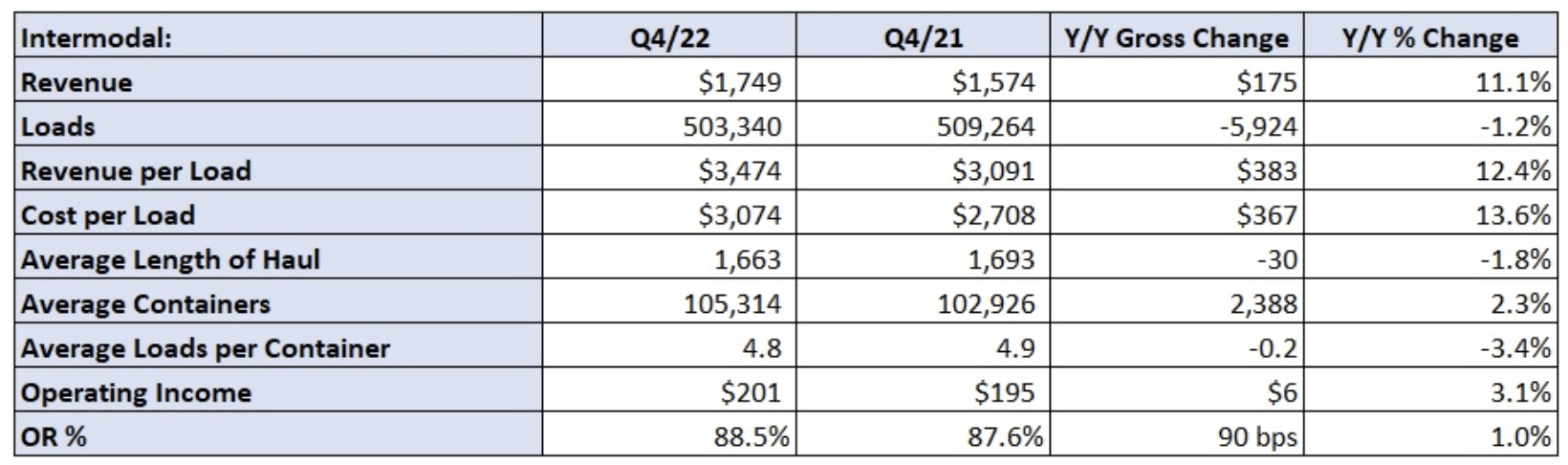

Anyway, as we can see below, intermodal revenue was still up 11.1%. This was driven by a 12% increase in revenue per load, resulting from changes in the mix of freight, customer rates, and fuel surcharges. Total loads declined by 1.2%. The same goes for the average loads per container.

{kind=link}

Unadjusted operating income fell by 8% as a result of higher investment requirements and higher wages to retain professional drivers, office personnel, and technicians. Insurance costs also increased.

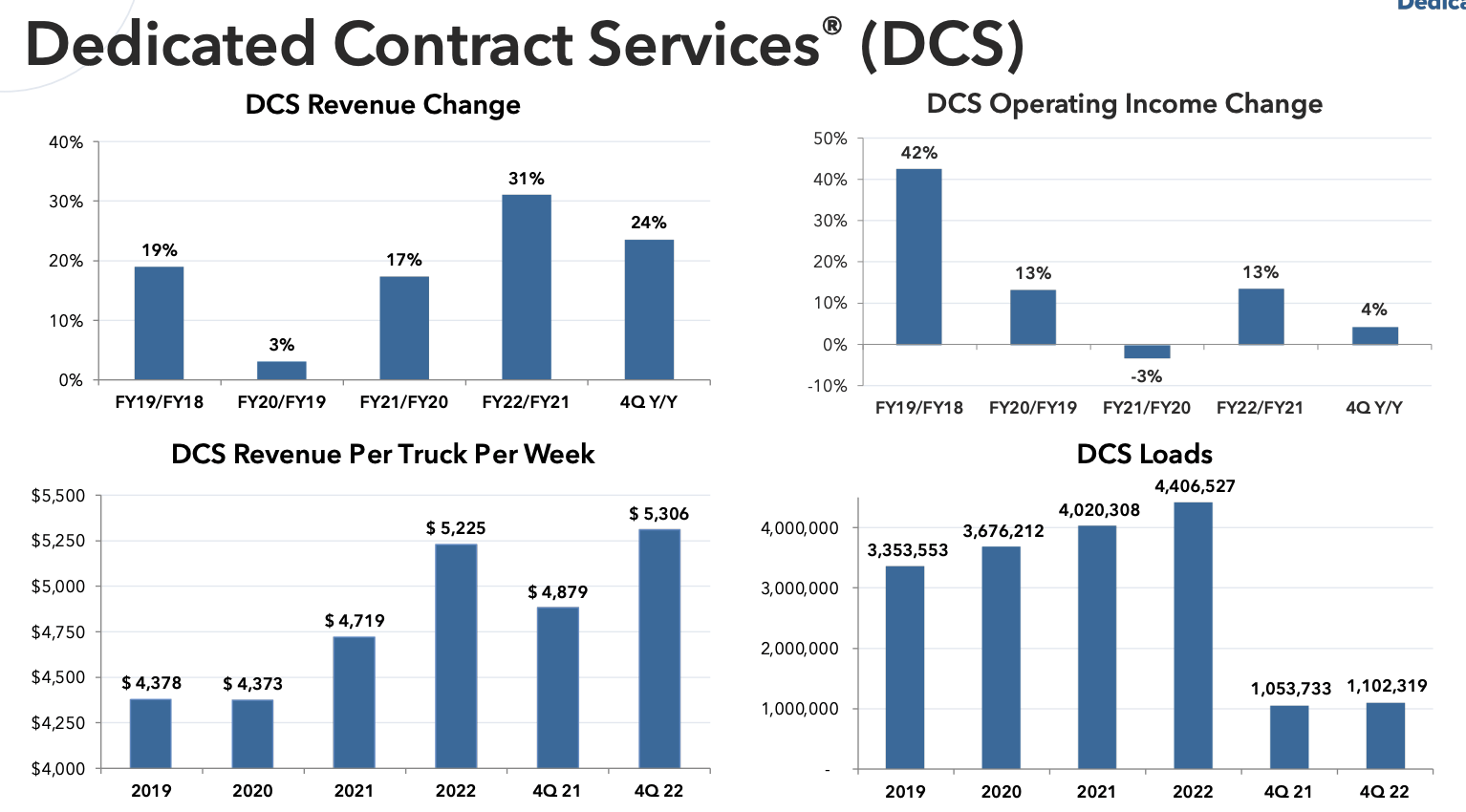

Dedicated contract services confirm the company's earlier comments. It is indeed delivering what customers are asking for. The highly engineered private-fleet outsourcing segment reported 24% revenue growth. This comes from a 14% increase in average revenue-producing trucks and a 9% increase in productivity.

Operating income improved by 4% due to new business onboarding and higher productivity. These benefits were partially offset by higher material costs and related inflationary factors.

{kind=link}

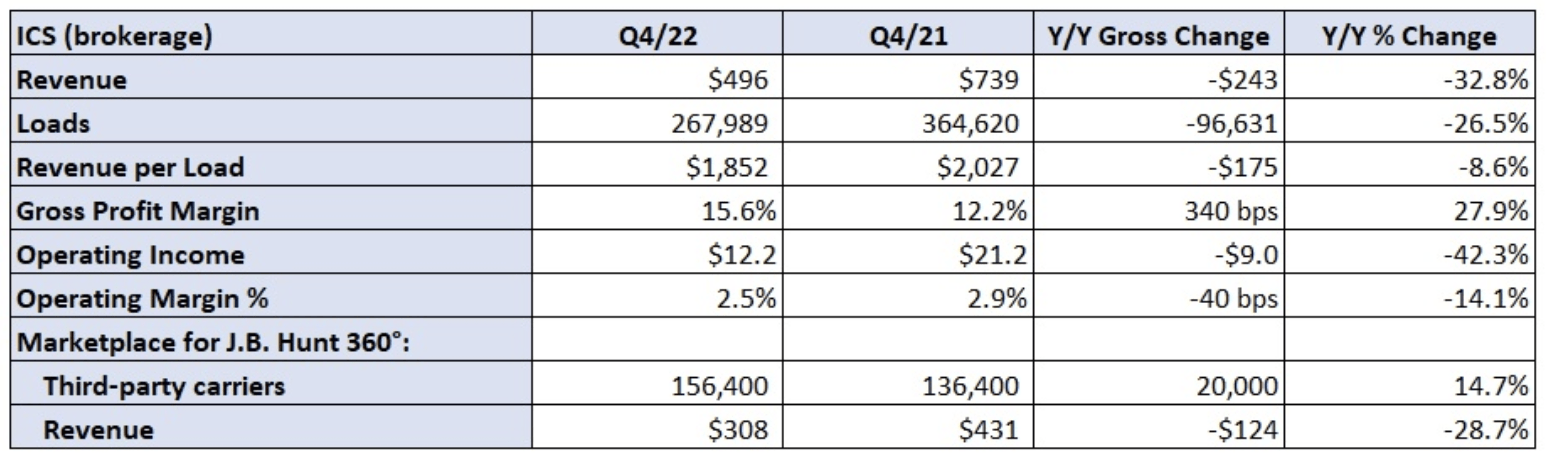

The integrated capacity solutions segment was hit by weakness in the trucking industry. Revenue declined by 33% as a result of a 27% decline in volumes. Truckload volumes were down 21%. Revenue per load was down 9%.

Due to higher expenses, the operating income result was even worse.

{kind=link}

As the table above shows, the good news is that its J.B. Hunt 360 marketplace did well, adding 14.7% more customers.

This is expected to continue:

As we move into 2023, we will remain focused on leveraging our investments and our people, technology, and capacity to further scale the business. We see a long runway of opportunity for future growth in 360box supported by disciplined investments, solid execution, and earning appropriate return on our capital. Wrapping up on J.B. Hunt 360, I wanted to take the last minute here to make sure the investment community understands that our digital freight marketplace is a tool that drives value across our entire enterprise.

The smallest segment, truckload, reported 6% higher revenues. Excluding fuel surcharges, revenue growth would have been down 2%, as revenue per load excluding fuel declined by 8%. The company's investments in hardware also showed results. The average trailer count increased by 3,900 units or 37%.

Unfortunately, this is also the reason why the company's operating expenses caused operating income to decline by 35% - on top of higher inflation-related costs. According to the company :

JBT continues to leverage the J.B. Hunt 360 platform to grow power capacity and capability for the J.B. Hunt 360box® service offering. Benefits from higher volume and revenue were more than offset by higher truck purchased transportation expense, trailer parts and maintenance costs, personnel costs, insurance and claims expense and continued technology investments to build out 360box.

So, What's Next?

The JBHT ticker rallied more than 4% after earnings, despite significant market weakness. The stock is now more than 20% above its 52-week low and less than 16% below its 52-week high. That's pretty good, given the bigger picture.

FINVIZ

Especially because of the bigger picture, it might be a bit surprising that investors bought the stock after earnings. After all, the company did suffer from weakening demand and high costs. If I had a bearish bias, I could have written a very bearish article. However, I would have to exclude important bullish info like the company's success in growing its J.B. Hunt 360 platform and service-based operations.

Moreover, despite ongoing economic headwinds, insiders see bottoming freight demand. As I discussed in a recent article on Seeking Alpha, FreightWaves CEO Graig Fuller came out mentioning rebounding demand after expectations seemed to have hit rock bottom.

Over the past week, we've spoken with numerous freight executives who have mentioned that the first two weeks of the first quarter are shaping up better than expected, granted, expectations were incredibly low after such a weak peak.

Going into the quarter, executives we spoke with predicted a significant collapse in freight for the first quarter, with a seasoned veteran executive of a large trucking technology firm predicting that the first quarter would be the worst in his four-decade career. It was a fair bet considering how challenging the second half of the 2022 was for most in the freight market.

The truckload spot rate has bounced back to $1.98 per mile, after falling to $1.67 in November of 2022.

FreightWaves

Tender volumes also suggest that the market is not seeing gloom and doom. The Outbound tender Volume Index has improved after briefly dipping below 2019 and 2020 levels.

FreightWaves

Moreover, according to Mr. Fuller:

If the first few weeks of the new year are an early omen, then the freight market may have bottomed in the fourth quarter and carriers can look forward to a far less volatile market in 2023.

Seeking Alpha reported something similar in a post-earnings news article. Major banks said that JBHT's earnings could have been much worse, as dynamics are still favorable.

Analysts at Deutsche Bank, UBS, Citi and JP Morgan also suggested results were better than feared. In particular, Citi analyst Christian Wetherbee shrugged off volume declines in intermodal, noting that profitability dynamics remain sturdy. Meanwhile, Deutsche Bank highlighted the one time nature of charges that hampered results. JP Morgan's analysis also highlighted negative sentiment heading into the quarter.

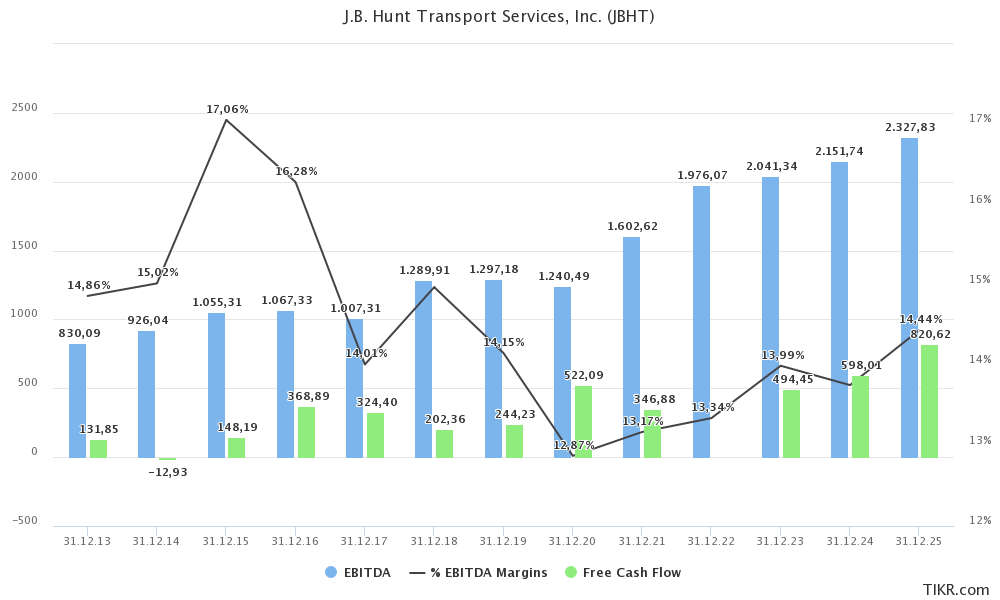

With that in mind, it's interesting that JBHT is not expected to see lower EBITDA in 2023 as analysts expect more than 3% growth. This growth rate is expected to gradually rise to 8% in 2025, opening up a way to more than $2.3 billion in annual EBITDA. Moreover, analysts expect margins to recover to more than 14.4% by then.

{kind=link}

In other words, it's what the company has been working on for years. It can accelerate growth thanks to new services and more equipment/major customers. Moreover, thanks to a focus on costs, it can grow margins. Not by a lot, but steadily and gradually. This could end up pushing free cash flow to almost $600 million next year. That would imply a free cash flow yield of more than 3.0% again.

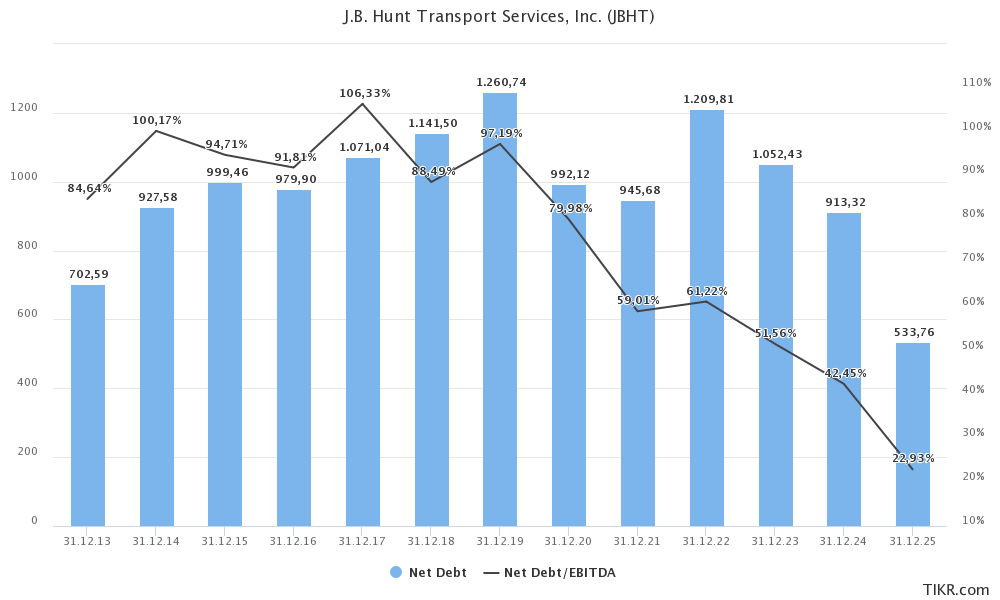

The company is also gradually lowering net debt to $1.1 billion this year (expected). This would imply a leverage ratio of just 0.5x. The company has a BBB+ credit rating, which is the closest one can get to the A-range.

{kind=link}

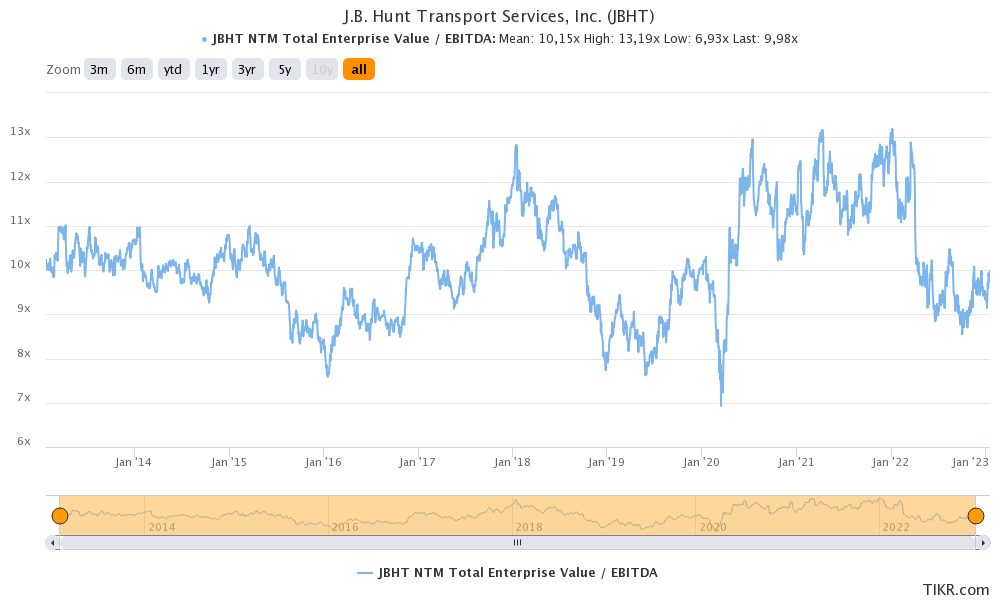

When adding this expected net debt number to its $19.5 billion market cap, we get a $20.6 billion enterprise value. That is roughly 10.3x 2023E EBITDA.

Looking at the historic EV/EBITDA (next twelve months) chart, I have to say that 11x EBITDA is a fair valuation. 11.5x would also be appropriate as JBHT is in a good spot to deliver outperforming EBITDA growth on a longer-term basis.

{kind=link}

From current prices, I think JBHT has between 7% and 14% upside potential this year.

This also means that I'm not a huge fan of the risk/reward, given underlying economic challenges. While I agree with sell-side research that dynamics are good and the company is improving its business (we discussed this for a long time on Seeking Alpha), I simply dislike the risk/reward.

If you like JBHT, I would try to get in as close to $160 as possible. Given the bigger picture, that's where I would start to really like the risk/reward.

Takeaway

In this article, we discussed the risk/reward of transportation giant J.B. Hunt. The company's earnings show a mixed picture. On the one hand, the company continues its impressive business transformation, growing J.B. Hunt 360 customers, adding new equipment and employees, and benefiting from its ability to deliver reliable services at competitive costs.

On the other hand, macroeconomic challenges are rising, resulting in pressure on volume growth.

While JBHT remains far from overvalued, I believe the risk/reward warrants caution. I would argue that the stock becomes a buy close to $160.

(Dis)agree? Let me know in the comments!

For further details see:

J.B. Hunt: The Good, The Bad, And The Ugly