JBHT - J.B. Hunt Transport: Capacity Gains Consumer Demand Recovery And Share Gains Drive Growth

2023-10-19 03:54:46 ET

Summary

- J.B. Hunt Transport Services stock is recommended as a buy due to expected above-average growth from intermodal and potential for volume growth.

- JBHT reported 3Q23 revenue growth of 0.3%, with intermodal revenue growing by 3.5%.

- Despite challenges in intermodal profitability, positive signs in volume and box turnover support the potential for sustained volume growth.

Summary

Following my coverage of J.B. Hunt Transport Services ( JBHT ), I recommended a buy rating due to my expectation that the business can generate above-average secular growth from intermodal. I believed that there was room to exceed the industry average for domestic intermodal growth over the past few years. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for JBHT as I believe the downcycle is coming to an end, and JBHT should see incremental volume growth driven by capacity expansion, consumer demand recovering, and share gains from truckload delivery.

Investment thesis

JBHT reported 3Q23 total revenue of $3.16 billion (0.3% growth), of which $1.55 billion was from intermodal, which grew by 3.5% vs. 3Q22. However, due to faster growth in operating expenses, operating income saw a decline of 10.1% to $241 million. However, on the EBITDA level, EBITDA saw growth of 9.6% to $429.4 million (D&A was the fastest-growing expense in the JBHT 3Q23 report). A decline in EBIT led to a decline in net income and EPS of $187.4 million and $1.80 million, respectively.

Expanding further on the subject of intermodal performance, which constitutes a crucial aspect of my optimistic stance, it is worth noting that although revenue experienced growth, the decrease in EBIT by 11.7% was somewhat underwhelming. The primary factors contributing to the decline were elevated equipment expenses, diminished utilization rates, and weakened pricing conditions. However, I derived positive outcomes from the results, despite the fact that intermodal profits were lower. This was due to the encouraging progress observed in terms of volume and box turnover, which are fundamental aspects. An essential piece of data for understanding volume growth is box turn performance (by JBHT and its rail partners). A strong box turn performance directly impacts utilization and volume growth. In my opinion, stronger box turns, a possible return in consumer demand, and capacity expansion will all contribute to sustained volume growth. Regarding the latter point, namely the expansion of capacity, it is noteworthy that the management exhibited a positive trend by increasing the number of containers added during the third quarter of 2023. Specifically, they added 1,000 containers during this period. albeit this figure still fell short of the average number of containers added in 2022, which stood at 4,600. That said, I maintain a positive outlook regarding the continuity of capacity expansion, as management has reaffirmed their objective of reaching a container count of 150,000 within the next 3-5 years, as initially stated in their 1Q22 announcement. Furthermore, management remained confident that the necessary capacity will be available once freight activity resumes within the network. With respect to the aspect of demand, it is my belief that we are currently approaching the trough of the cycle, as indicated by segment margins declining below 10%, a range that has historically spanned from 10% to 14%. Management observations regarding the destocking trend also indicate that it is probable that the conclusion of this trend is imminent. Once the destocking situation concludes, it is highly advantageous for JBHT as retailers are compelled to replenish their inventory (sell-in), thereby providing JBHT with a significant, temporary surge in volume. Retailers are compelled to replenish their inventory in due course, as there is an increase in consumer demand.

Our customers have been working through excess inventory and as we stated last quarter, we felt like that destocking trend started to moderate in June.

The freight recession has been a real thing as we've talked about inventory destocking and the role that that played in demand in our industry for several quarters now. And we're confident that, that pressure relief during the third quarter. 3Q23 earnings results call

Looking ahead, I feel optimistic about the upcoming growth prospects. First and foremost, I think that the increased intermodal service capability will act as a catalyst to allow trucks to gain a larger share of the market even though truck contract rates declined in 2023 . The fact is Intermodal still offers a significant cost advantage over long-distance transportation. Moreover, I anticipate that JBHT will experience a resurgence in volume, as the company intends to enhance its service and expand its capacity. This will be achieved through their strategic objective of incorporating an additional 40,000 containers within the next 3-5 years, resulting in a total container count of 150,000 (currently 117,387). Although there are concerns regarding excessive capacity, it is worth mentioning that JBHT has the ability to adjust container allocation within its network in order to sustain capacity and fulfill market demands. This was acknowledged by management when they mentioned the retrieval of equipment from storage in the third quarter of 2023. The numerical data also supports this claim, as management has effectively maintained an 82% utilization rate in a sequential manner, even with an approximate increase of 1,000 containers.

Valuation

{kind=link}

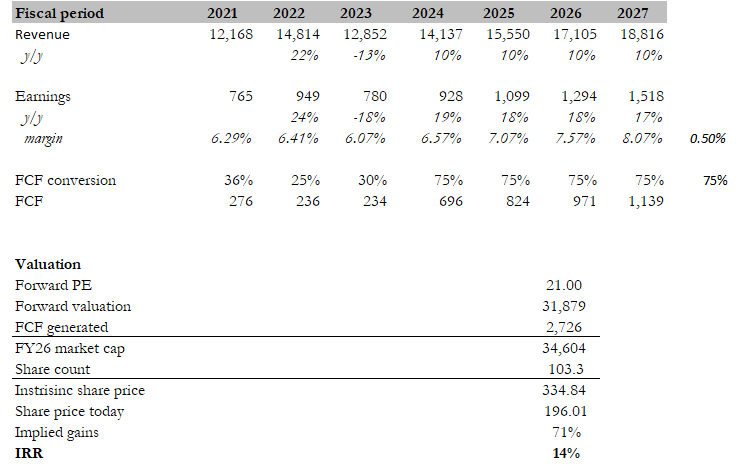

I believe the fair value for JBHT based on my DCF model is $334. My model assumptions are that JBHT can achieve 10% growth for the next few years, in line with historical growth rates. The growth will be driven by capacity expansion, a recovery in consumer demand (resulting in strong growth from restocking), and capturing share from truck delivery. Margin should expand as volume growth drives margin expansion due to the fixed-cost nature of the business. Since my last write-up, the JBHT share price has appreciated as expected, driven mainly by the valuation expanding from 2x to 23x forward PE. While I like the returns, I hold a conservative view that valuation will re-rate back to 21x forward PE (JBHT long-term average) as the cycle normalizes.

Risk

There are various factors that may hinder the anticipated global economic recovery in the latter half of 2023. The factors to consider are the potential occurrence of a substantial economic decline, the ongoing sluggishness in rail service despite the overall improvement, and the emergence of new digital competitors competing for dominance in the brokerage industry. Moreover, the persistence of challenges, such as an excess of industry capacity that exceeds the level of demand, may lead to a deflationary impact on pricing.

Conclusion

In conclusion, my continued recommendation for a buy rating on J.B. Hunt Transport Services remains rooted in the anticipated end of the downcycle and the potential for incremental volume growth. Several key factors support this stance. Despite challenges in intermodal profitability, positive signs in volume and box turnover are promising indicators. Capacity expansion is on the horizon, with a strategic goal to add 40,000 containers within 3-5 years. The expected resurgence in volume will be driven by improved service and capacity expansion, reinforcing JBHT's position in the market. While concerns exist about industry capacity, JBHT's ability to adapt and maintain utilization rates is evident.

For further details see:

J.B. Hunt Transport: Capacity Gains, Consumer Demand Recovery, And Share Gains Drive Growth