JBHT - J.B. Hunt Transport: I Remain Confident That Sales And Margin Will Recover In 2024

2024-01-03 23:13:24 ET

Summary

- J.B. Hunt Transport stock price has increased by 9.15% since the last article, making it an appealing stock to buy or hold onto.

- JBHT derives revenue from diverse business operations, with the Intermodal segment being the largest contributor.

- Despite declines in operating revenues, the Company has access to a significant portion of the growing US transportation market and has the potential for record sales results in the future.

Investment Rundown

Almost half a year ago I covered J.B. Hunt Transport Services, Inc. ( JBHT ) and concluded that the company appeared to offer a good entry point to make a buy. Since the article, the stock price is up around 9.15% now and I think as we have now entered 2024 it remains an appealing stock to buy or hold onto to benefit from the likely rate decreases in the second half of 2024. My thesis now revolves around increased economic spending which would provide higher demand for the products that JBHT makes and the services they provide.

The last results from the company showcased significant declines in the top and bottom line compared to last year as there has been a halt in demand in recent quarters, not just for JBHT but for a lot of delivery companies. When FedEx Corporation ( FDX ) posted earnings and indicated lower expected sales and earnings in the short term the market punished the stock price and it slid nearly 14% in a day. For JBHT the stock price has been on a very steady uptrend since late October and I think it can keep chugging along this year too. The p/e sits at 27 but I think 2024 will be a recovery year for the sales and earnings and 2025 and 2026 will be the big years when JBHT achieves record results once again. I had the company as a buy around 6 months ago and I will stand by that rating still.

Company Segments

JBHT derives its revenue from five primary streams, showcasing the company's diversified business operations. The largest contributor to its revenue is the Intermodal ((JBI)) segment, accounting for a substantial 53% of the total revenues. Following closely is the Dedicated Contract Services segment, responsible for generating 42% of the company's overall revenues.

Segment Overview (Investor Presentation)

The Dedicated Contract Services segment adds a layer of diversity to JBHT's revenue streams by offering on-site management and services to its customers. This segment demonstrated noteworthy growth in the last quarter, with strong performance results. In Q1 2023, the segment witnessed a notable increase in operational capacity, marked by 541 more trucks in operation compared to the previous year. This seems to have continued in the last report as well and the revenues have not fallen drastically from Q1 results of $3.23 billion.

{kind=link}

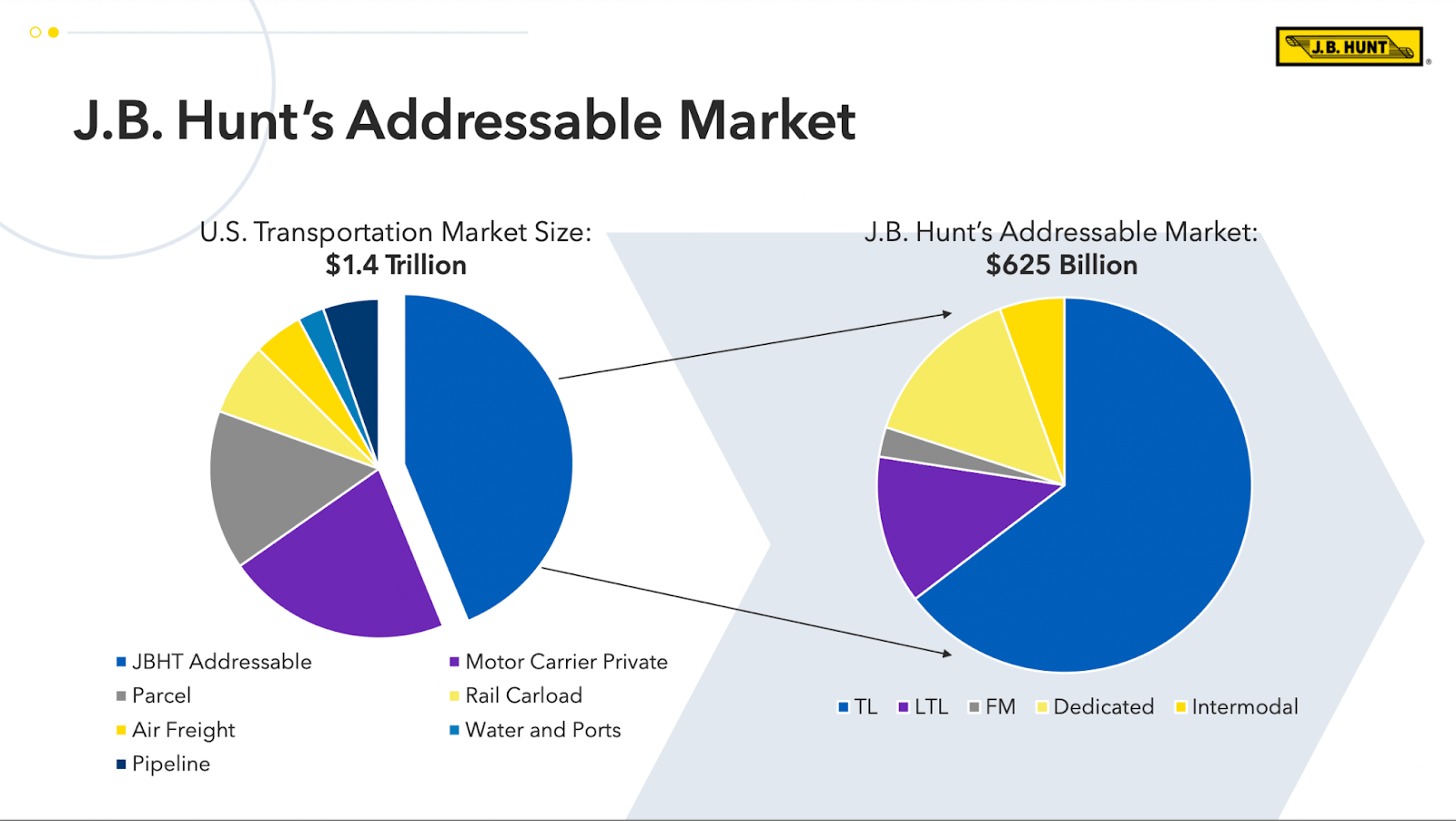

One of the appealing factors I find with JBHT right now is the large TAM they have access to. The US transportation market size is at $1.4 trillion now and JBHT has direct access to around $625 billion of that. It's a significant amount and the fact the market has been growing steadily over the past decade has aided JBHT in its growth as well. The US economy continuing to grow despite the higher interest rates showcases some of the robust resilience it has and why it's a market that companies flock to when times are tough otherwise.

Earnings Highlights

{kind=link}

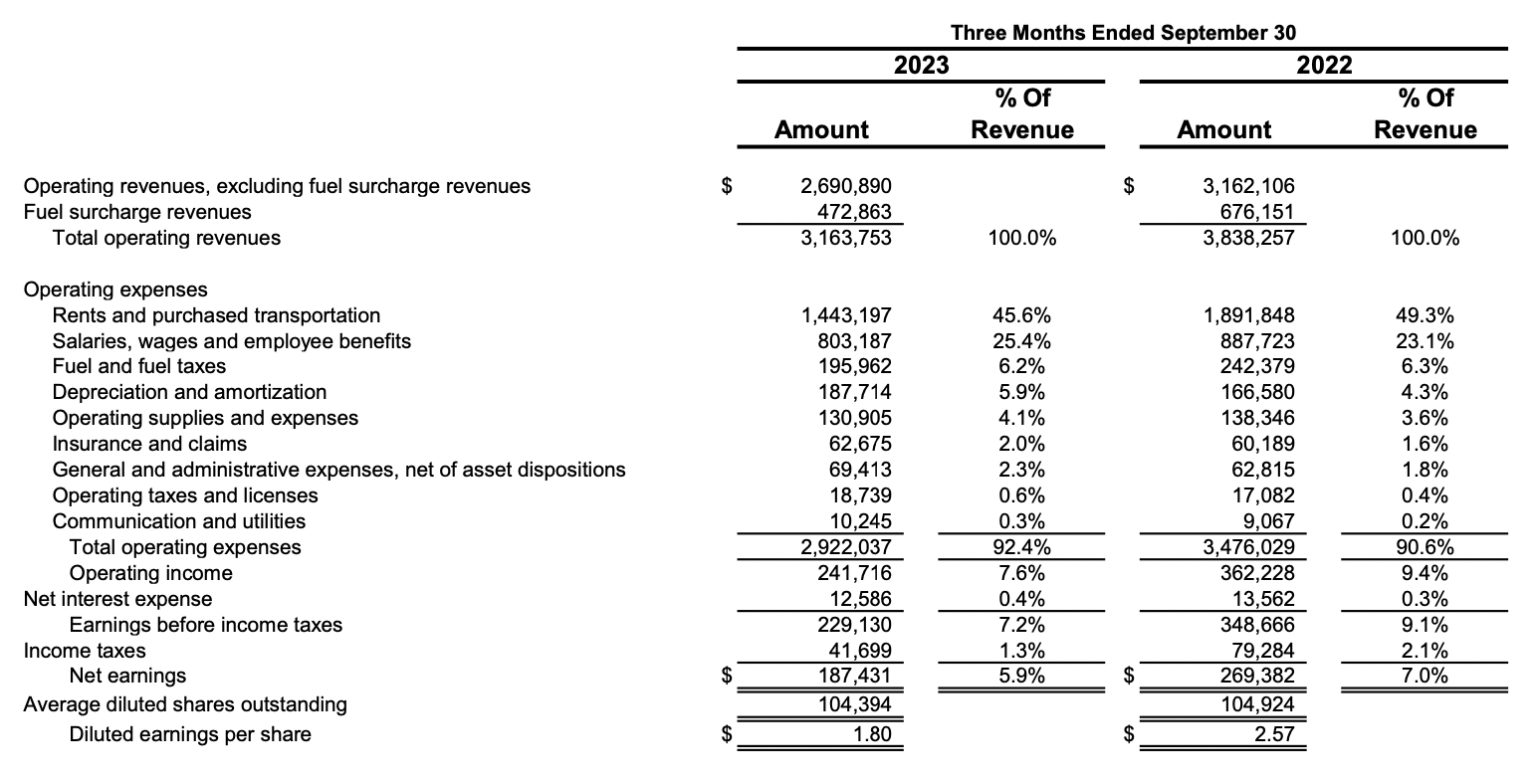

Taking a closer look at the results from Q3 of 2023 we can see a pretty significant decline in the operating revenues, falling to $3.1 billion, down from $3.8 billion. The decline seems to be the result of softer demand and a general decline in US economic activity, at least in terms of shipments and deliveries.

{kind=link}

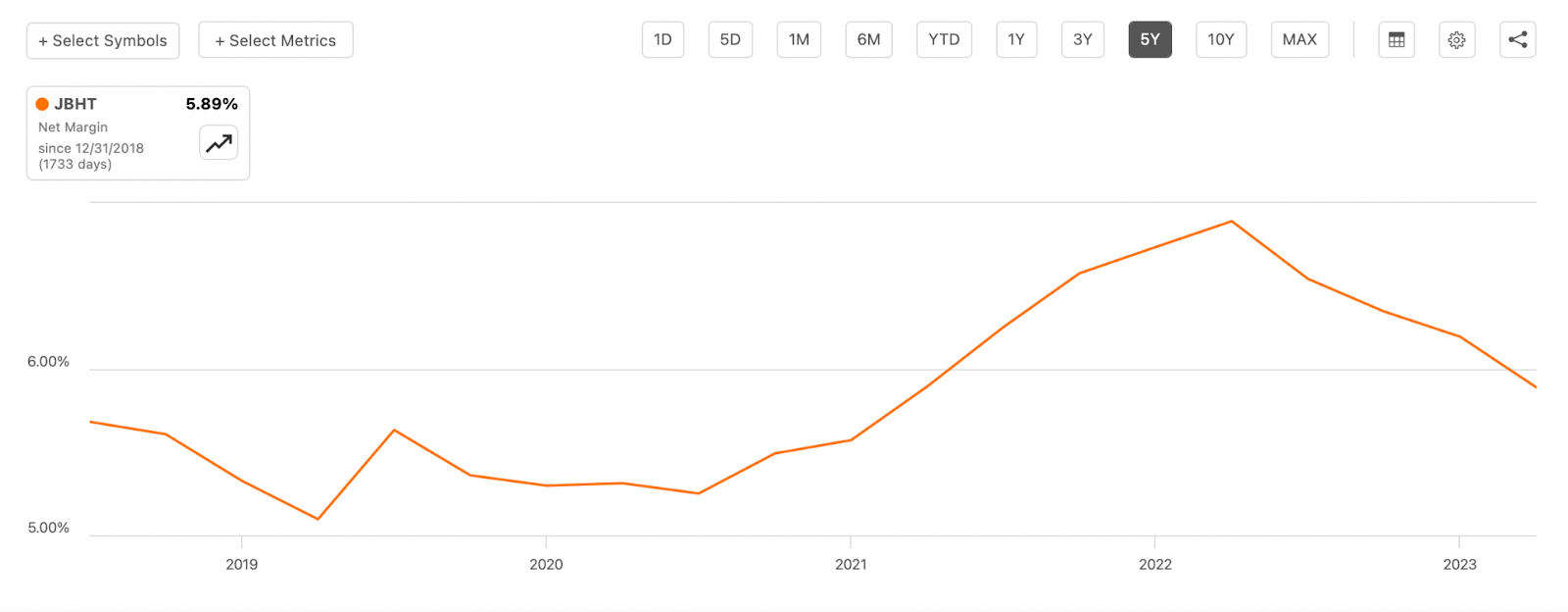

Going into the next quarters I think my key point to watch will be the margins of the business. The last few quarters have been difficult in terms of margin growth. It peaked in 2022 as the US economy was booming and demand remained high. 2023 saw a decline as interest rates increased and with JBHT having roughly $1.2 billion in long-term debts it has put a toll on the bottom line. Interest expenses were $54 million last 12 months. I think this might be a sort of peak though for the interest expenses for the company as there is a high likelihood of rate cuts this year. Expectations seem to be that it will fall to 4.6% which would incentivize more economic activity and is a key supporting factor as to why I think JBHT might in 2025 and beyond post record sales results, which would be anything over $14.8 billion. If they achieve that in 2025 it would put them at an FWD p/s of roughly 1.35. This is a decent discount to the sector average of 1.61. I think the quality of the business will shine through and we might see that p/s of 1.6 be applied to JBHT meaning there is decent value here to be had. In terms of precise targets, I would land at around $236 bringing or 19% higher than today's price level. This is adequate to be to make a buy case here still for JBHT, and with the dividend yield at roughly 1%, it adds further to the value investors can collect here.

In Q4 FY2023 I will be watching the margins mostly and I do anticipate an uptick in the sales as the quarter tends to showcase quite high demand in general. If results impress then we will likely see the stock price tick even higher, potentially closer to $205. Nonetheless, I think JBHT is in the long-term a solid business and my buy rating continues for them.

Risks

The trucking industry grapples with an enduring shortage of qualified drivers, posing persistent challenges for companies like JBHT. This scarcity of skilled drivers not only raises concerns about increased labor costs for the company but also introduces the potential for service disruptions and capacity constraints. The shortage of drivers remains a critical factor influencing the operational landscape and profitability within the trucking sector. If there aren't enough people to hire and JBHT can't efficiently scale their operations without having to offer extremely high wages which will impact margins then the market may reduce the premium the company currently trades at, which would bring short-term pain for investors.

{kind=link}

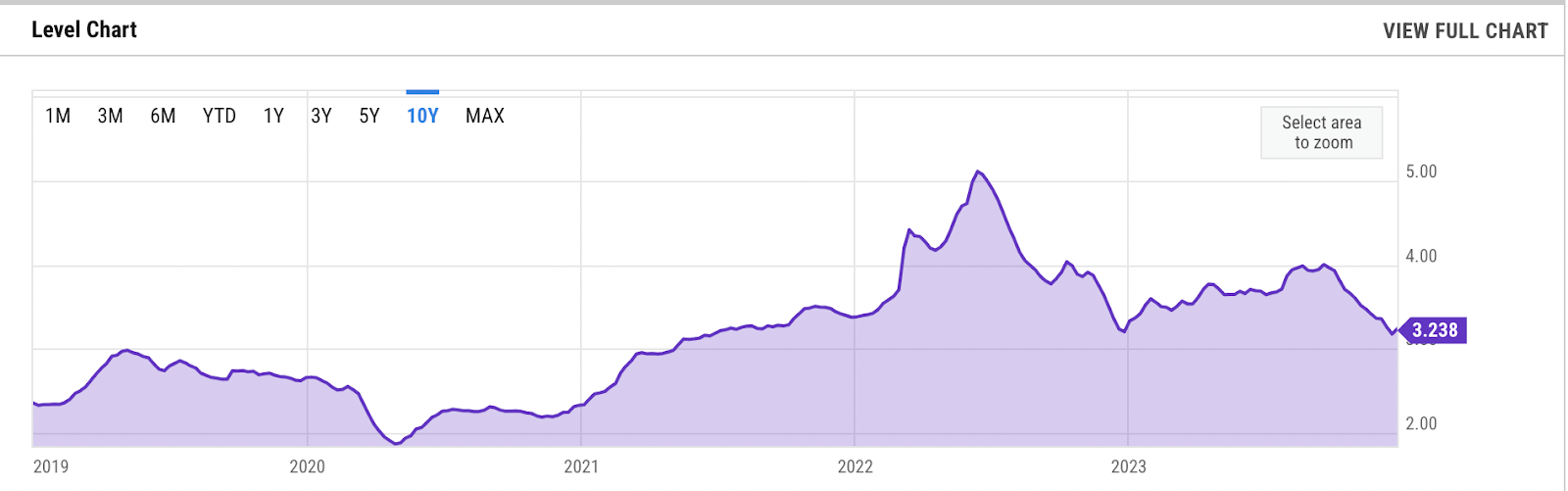

Another risk that is facing JBHT is elevated gas prices . Seeing as the company is a delivery company, having favorable gas prices will make earnings better. The chart above here showcases a pretty steady decline in prices from the highs last year. I do think there is a risk present that prices may rise going into the summer as demand picks up. It also of course depends on US production levels as well. The US oil industry has been on fire the last several quarters as a means of offsetting the cuts OPEC is doing and stabilizing prices in the US. It seems to be working as the largest basin the Permian continues to produce very well. My fear is that should US production levels decline it might very well send gas prices higher and harm the earnings of JBHT and other delivery companies. For the moment it seems to be heading in the right direction, but it's an area I will be monitoring in 2024 very closely.

Final Words

I have covered JBHT before, but my last article was close to 6 months ago so I figured an update was in order now. the stock price has grown nearly 10% since then and the results I think continue to be robust for the business. Rate cuts this year will send more demand JBHT way I think and result in 2025 or 2026 netting them record sales results. As I anticipate that to be the case it means there is a decent upside potential until then should the company be valued more in line with the rest of the sector based on p/s, which I think it will. It all concludes with me continuing to be bullish on the business and sticking with my initial buy rating.

For further details see:

J.B. Hunt Transport: I Remain Confident That Sales And Margin Will Recover In 2024