JJSF - J&J Snack Foods: Too Rich For Our Liking

2023-09-14 23:00:20 ET

Summary

- JJSF’s revenue has grown at a CAGR of 6%, reflecting the lucrative nature of the snacking industry, due to high prices and consumer behavior leaning toward recurring purchases.

- JJSF’s portfolio of brands is strong, with good diversification and exposure nationally. We see scope for greater M&A, expansion into healthier alternatives, and international expansion.

- Inflationary pressures have contributed to margin erosion, creating significant execution risk associated with returning to pre-pandemic levels.

- JJSF looks unattractive relative to its peers while trading at a premium. This is unjustified in our view.

Investment thesis

Our current investment thesis is:

- JJSF provides investors with good exposure to a growing industry, with robust demand. The company’s portfolio of brands is attractive, although lacks the international exposure and brand heights of many of its peers.

- We believe growth can continue to outperform, owing to M&A and commercial developments in line with what has been achieved historically. Further, we do suspect margins will continue to improve, although it remains uncertain as to where they will normalize.

- With JJSF underperforming its peers and the various uncertainties currently, we do not think it is attractively priced.

Company description

J&J Snack Foods Corp. ( JJSF ) is a well-established American snack food manufacturer headquartered in Pennsauken, New Jersey. Founded in 1971, the company specializes in producing and distributing a diverse range of snack foods and frozen beverages. J&J Snack Foods' product portfolio includes soft pretzels, churros, frozen lemonades, fruit bars, and more. These products are sold to various market segments, including foodservice providers, convenience stores, schools, entertainment venues, and supermarkets.

Share price

JJSF’s share price performance has been strong, returning a comparable amount to the wider market. This has been delivered through financial progress but also bullish investor attitudes, which we will look to assess.

Financial analysis

{kind=link}

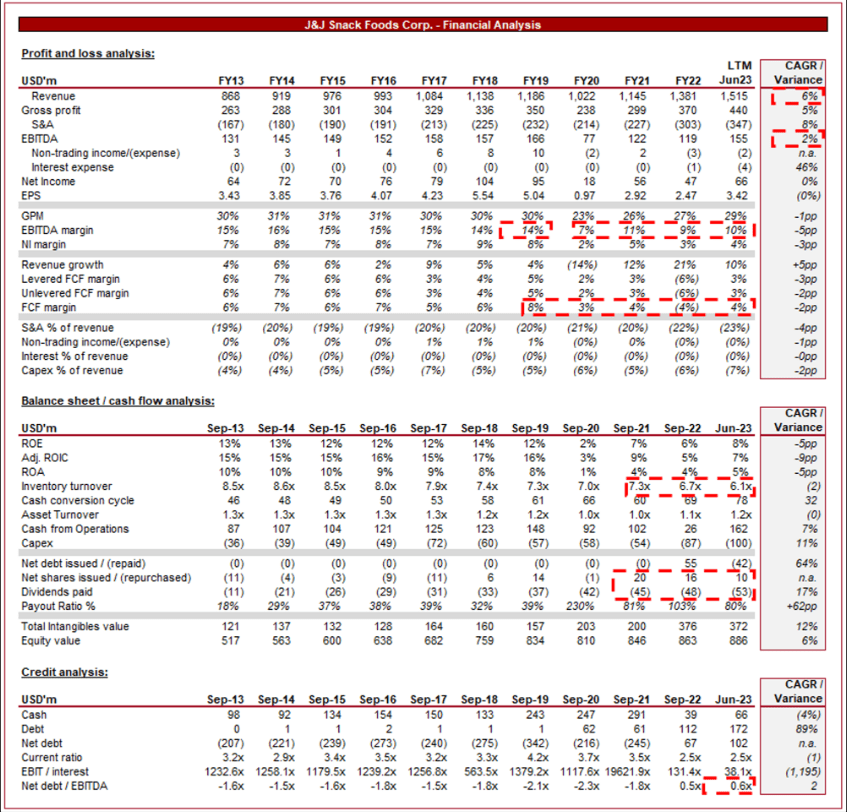

Presented above are JJSF's financial results.

Revenue & Commercial Factors

Business Model

JJSF offers a diverse portfolio of snack products, including soft pretzels, frozen beverages, churros, bakery products, and more. These products are sold under various brand names and distribution channels. The company operates as a fast-moving consumer goods business (FMCG), seeking to achieve scale and reach throughout its portfolio via a quality product and the development of its brand.

The company distributes its products through multiple channels, including convenience stores, supermarkets, foodservice operators, schools, and entertainment venues. This diversified distribution strategy reduces risk and increases market reach.

JJSF continually focuses on product innovation and development. It introduces new flavors, variations, and formats to cater to changing consumer preferences and create constant interest in its brands. As an example, Superpretzel launched the “Bavarian Soft Pretzel Sticks” nationally.

The company has grown through strategic acquisitions, adding well-known brands like Dippin’ Dots and ICEE to its portfolio. These acquisitions have expanded its product offerings and market presence. We believe there is an opportunity for consolidation within the snacking industry, representing scope for further acquisitions to achieve increased scale.

Snacking Industry

JJSF faces competition from various players in the snack and frozen beverage industry, including major corporations like Conagra Brands ( CAG ), Utz Brands ( UTZ ), and General Mills ( GIS ), as well as smaller regional competitors. Additionally, the company contends with alternatives to traditional snacks, such as fresh fruits and yogurt.

The US snacking industry is substantial, valued at an estimated $110b in 2023. The industry is expected to grow at a CAGR of 3.8% into 2028 , driven by strong demand, economic development, and pricing. Given the maturity of the industry, this rate is considered attractive, as it exceeds the long-term GDP target of the US.

The attractiveness of snacking is attributable to the “typical American diet” (similar case for most Western nations). Essentially, it is an industry that reaches most of the populous, with recurring sales (& loyalty), resilient demand, the ability to price and market aggressively, and attractive economics. This is one of the primary reasons Kellogg ( K ) is spinning off its Snacking segment into a standalone “growth” business, expected to grow at 3-5% on an organic basis.

JJSF has been heavily reliant on the North American market, particularly the United States. The snack food market in the U.S. is highly competitive and saturated, limiting opportunities for significant growth. Thus far, JJSF has managed to outperform the market as a whole but the risk is that its growth rate is pulled down toward the average.

Consumer preferences have shifted towards healthier snack options. This is part of a broader trend of increased awareness of physical and mental health factors, contributing to reduced/changing snacking habits. JJSF’s product portfolio, which includes many indulgent and calorie-dense items, may not align with these health-conscious trends. The healthy segment is forecast to grow by 6.6% into 2030, illustrating the shift in demand. For this reason, it is critical for JJSF to explore opportunities to diversify its product portfolio by introducing healthier snack options or entering new food categories that align with changing consumer preferences. This could represent a segment to expand into via M&A.

Additionally, consumer spending patterns are changing, with increased e-commerce usage, such as through websites like Amazon (AMZN), to improve convenience and receive better pricing. Investing in e-commerce capabilities and exploring direct-to-consumer sales could allow the business to improve its economics on sales.

The company's international presence is relatively small compared to its domestic operations. Expanding into new international markets could provide growth opportunities but its lack of brand visibility could make this difficult. If the company did attempt this organically, expanding into the anglosphere or LatAm is likely the best opportunity.

Competitive Positioning

We consider the following factors to be JJSF’s competitive advantages:

- Brands - JJSF operates a range of well-regarded brands, allowing the business to price above private labels successfully and enjoy outsized demand.

- Operational capabilities - JJSF has a strong supply chain and distribution channel, allowing for consistently strong margins and maximum reach, which is critical in a highly competitive industry where shelf space is key.

Broadly, we are concerned by the extent to which the company is attractive. It has strong brands and a national presence but we struggle to see the value drivers for outperformance. Its brands are not global and the extent of product diversification is limited.

Margins

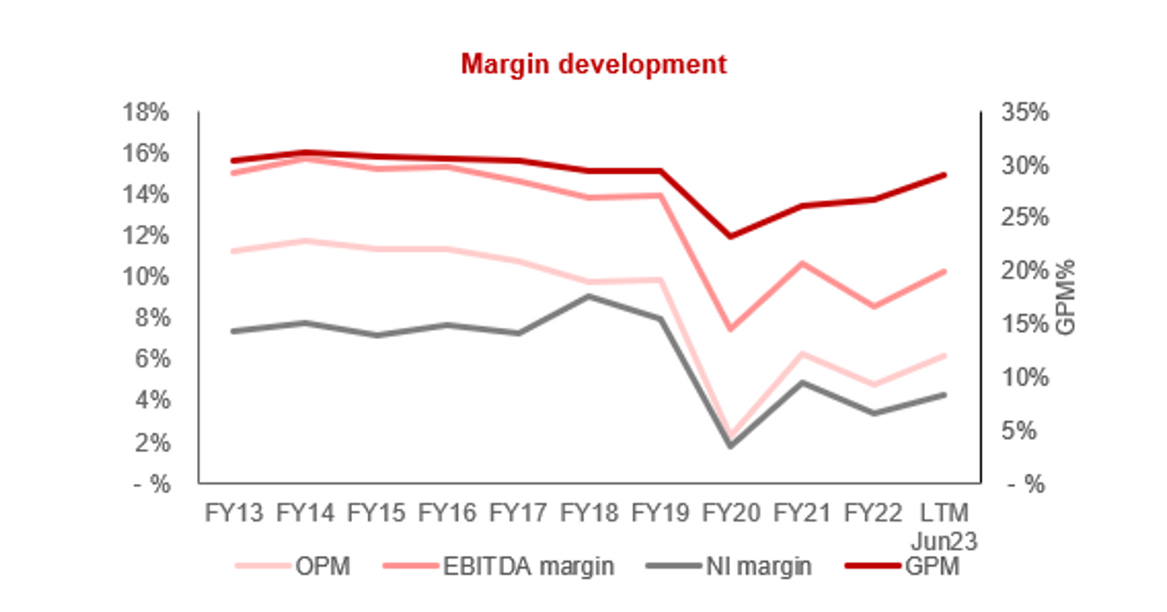

{kind=link}

JJSF’s margins have declined during the post-pandemic period, with EBITDA-M falling to 10% and NIM to 4%. The company has faced rising costs of raw materials, labor, and transportation, contributing to a squeeze on both GPM% and EBITDA-M (rising S&A).

Management believes we are beginning to see cost inflation stabilize, contributing to margin improvement during the LTM. In combination, there is an effort to improve efficiency in the production process and logistics (which led to a share price rally). Further, improvements are required.

Historical evidence suggests there is upside available but we are not certain this is deliverable due to the competition in the market. An EBITDA-M of at least 12% should be targeted by Management.

Balance sheet & Cash Flows

JJSF’s inventory turnover has declined in recent periods, compounding the negative impact of declining margins. This is acting as a drag on cash flows and appears an unusual development given the strong demand during the LTM.

JJSF is conservatively financed despite the various acquisitions, suggesting a continuation is possible should opportunities present themselves.

Industry analysis

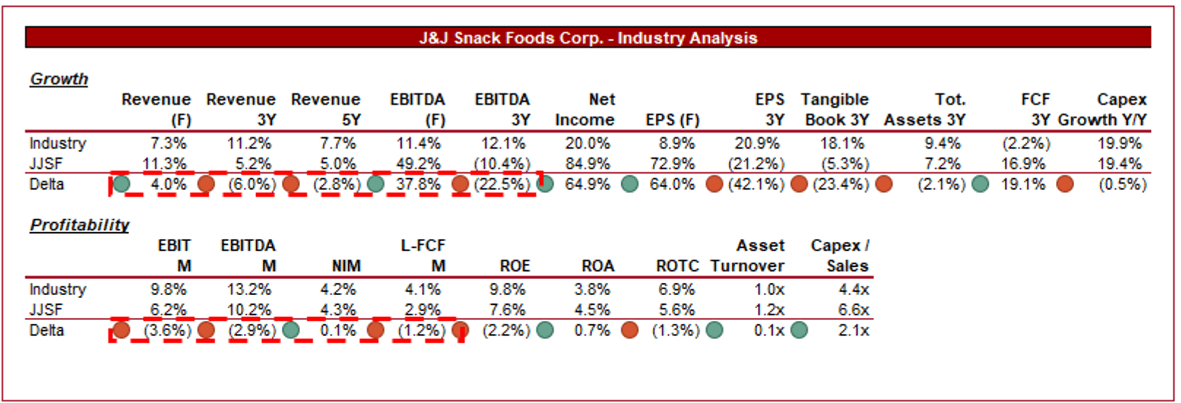

{kind=link}

Presented above is a comparison of JJSF's growth and profitability to the average of its industry, as defined by Seeking Alpha (35 companies).

JJSF performs modestly relative to peers, acknowledging that it is currently underperforming its normalized level. The company’s growth has lagged behind the industry average, only held up by recent acquisitions. This to us a reflection of the “position” of its brands, which are strong in the US but face high competition.

JJSF’s historical margins would have it placed around the average but at its current levels, the company is significantly underperforming. This gap closes at a FCF level which is positive but is nevertheless, unimpressive.

Valuation

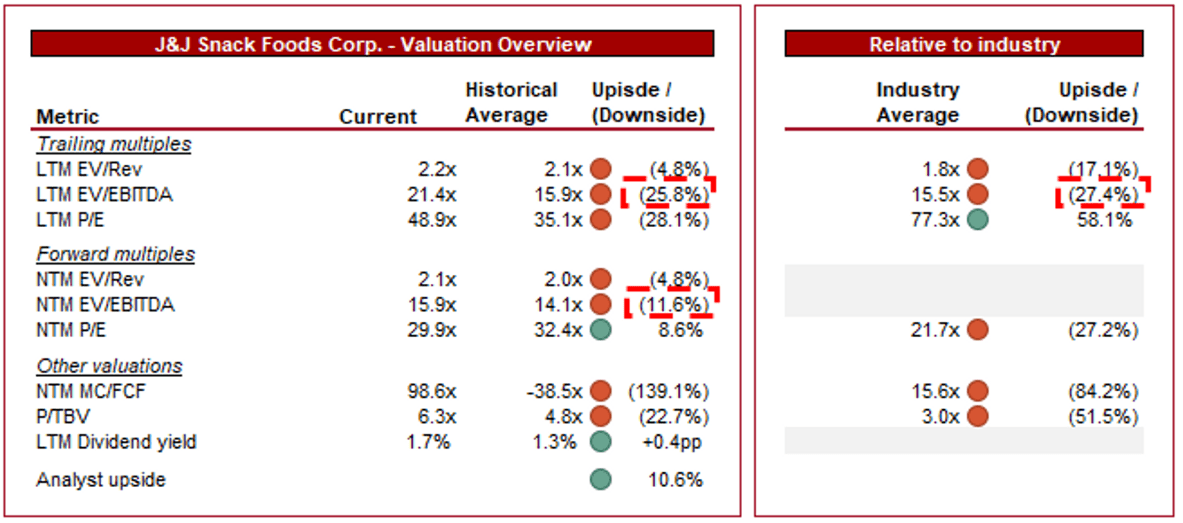

{kind=link}

JJSF is currently trading at 21x LTM EBITDA and 16x NTM EBITDA. This is a premium to its historical average.

JJSF’s premium to its historical average is unjustifiable in our view, given the deterioration in margins and the unchanged commercial positioning. This likely suggests investors are pricing in a high chance of margins returning to prior levels, which we are unconvinced about.

Further, the company is trading at a larger premium to its peer group (27% LTM EBITDA, 27% NTM PE). This again appears unreasonable in our view, for the reasons discussed, as well as the company’s elasticity to a decline in conditions. Most FMCGs have seen their margins remain broadly robust, with small erosion. This is not the cast for JJSF.

For these reasons, we do not consider JJSF attractively priced.

Final thoughts

JJSF is a solid business. The company owns a range of valuable brands that have a strong presence in the US. The snacking segment is highly lucrative due to consumer behaviors, with a good growth forecast. We see several opportunities for outsized returns in the coming years, including launching healthier alternatives to its current products.

Our struggles with this business are that it is clearly susceptible in macro conditions, as illustrated by its margins, and also does not own brands to the level of its peers (who are international). JJSF’s valuation does not price in any of the risks associated with these factors.

For further details see:

J&J Snack Foods: Too Rich For Our Liking