SJM - J. M. Smucker: Hostess Acquisition Benefit Has Been Priced In

2023-10-13 11:21:22 ET

Summary

- SJM has shown remarkable growth in 2023, driven by the easing of the COVID-19 pandemic.

- SJM's acquisition of Hostess has the potential to drive future revenue growth and strengthen its position in the snack segment.

- The company's wide range of products and commitment to expansion position it well to capitalize on industry trends.

Investment action

Based on my current outlook and analysis of J. M. Smucker ( SJM ), I recommend a hold rating. SJM has shown remarkable growth in 2023, driven by the easing of the COVID-19 pandemic. Even amidst COVID-19 challenges, SJM maintained its margins well, reflecting its robust cost management. The acquisition of Hostess emerges as a pivotal strategic decision with the potential to drive future revenue growth. However, it seems the broader market has already accounted for the anticipated benefits of this move in the stock's present valuation.

Basic Information

SJM boasts a diverse portfolio that encompasses a wide range of products, including fruit spreads, coffee, pet foods, peanut butter, and oils. With a steadfast commitment to quality and innovation, the company has introduced some of the most beloved brands to households across the globe. Their dedication to sustainability, ethical sourcing, and community engagement further solidifies their reputation as a company that cares about its consumers, partners, and the environment. As SJM continues its journey, it remains deeply rooted in its core values, ensuring that every product delivered resonates with its tradition of excellence.

The implications of COVID-19 significantly altered the global economic landscape in 2020, and SJM was not exempt from its effects. The challenges of that year led to a slight dip in the company's revenue. However, showcasing resilience and strategic adaptability, SJM began its recovery journey as the pandemic's grip started to ease. By 2023, the company's revenue growth rate was on an upward trajectory of 7%, surpassing the pre-pandemic growth rate observed in 2019. Furthermore, the company's operating margin has been consistent, hovering around its six-year historical mean of 19%. This consistency underscores SJM's operational efficiency and its ability to sustain profitability even amidst challenges.

Review

In the first quarter , SJM reported strong numbers. Although they experienced a 4% dip in net sales, it was counterbalanced by a 9% uplift from Jif peanut butter, a reflection of the previous year's product recall, which affected year-on-year comparisons. When adjusted for the one-off net sales of $374.1 million from brands they've since divested and accounting for a $3.8 million setback from foreign currency changes, there emerges a significant net sales boost of $310.1 million, marking a 21% increase.

The acquisition of Hostess by SJM is a strategic move that goes beyond a mere expansion of product lines. Hostess, with its iconic snack offerings like Twinkies and Ding Dongs, holds a nostalgic value for many consumers and has a strong foothold in the snack market. By integrating Hostess into its portfolio, SJM not only taps into this established brand equity but also gains access to a broader consumer base. This move underscores SJM's plan to diversify and strengthen its position in the snack segment, a market that continues to grow as consumers increasingly seek convenient and indulgent snack options. Moreover, the merger promises synergies in operations, distribution, and marketing, setting the stage for enhanced profitability and market reach. By bringing Hostess under its umbrella, SJM is poised to leverage its combined expertise and potentially introduce innovative products that cater to the evolving tastes and preferences of consumers.

Mark Smucker, the CEO, has emphasized SJM's continued interest in further strategic acquisitions, indicating a proactive and forward-looking approach to growth in the food industry. The company's wide range of products further emphasizes this commitment to expansion. Products like Jif peanut butter, Milk-Bone, and Uncrustables have been spotlighted for their growth, showcasing SJM's ability to innovate and cater to evolving consumer preferences.

Looking ahead, the future of the packaged food segment is promising. Factors such as urbanization, the increasing demand for convenience foods, diverse taste preferences influenced by global exposure, and a growing emphasis on health and wellness are shaping the industry's trajectory. SJM, with its strategic initiatives and diverse product range, is well-positioned to capitalize on these trends. Additionally, the company's pet portfolio, which continues to show positive momentum, indicates SJM's adaptability and focus on long-term growth.

Valuation

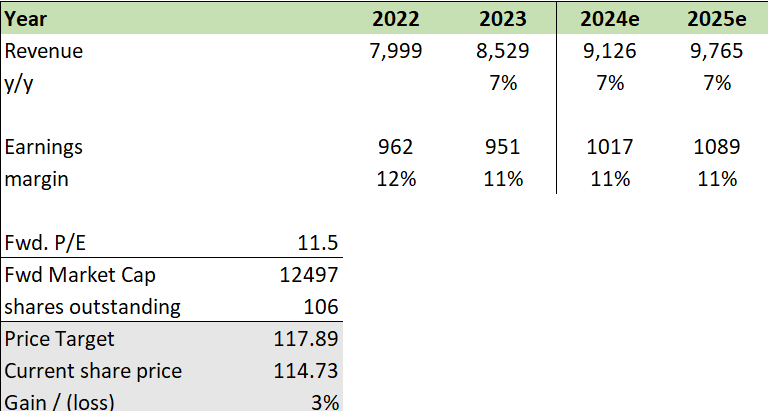

I forecast 7% revenue growth for SJM in both FY24 and FY25, which is above the general market consensus for FY24 of 3% while FY23 is in line. While the broader market is taking a cautious stance on the immediate returns from the Hostess acquisition, highlighting concerns about potential integration challenges, short-term costs, and the time needed for full benefits to materialize, I hold a more optimistic view. I'm confident that the synergies between the two companies can be harnessed swiftly, given that they operate within the same sector and offer products that are analogous in nature. On the topic of margins, I expect them to stay in line with the 2023 figures, a perspective that resonates with the prevailing market consensus. Considering the Hostess acquisition is centered around a business that mirrors SJM's core operations, I remain unconvinced that it will have any adverse effect on SJM's margins.

{kind=link}

Currently, SJM is trading at ~11.5X forward P/E, while its peers have a median of 12.7x. SJM boasts a higher gross margin of 33.2%, outpacing the peer median of 27%. However, its net margin stands at 9.5%, which is slightly behind the peer group's median of 11%. Taking these into account, I believe that SJM's present valuation is justified.

In light of my optimistic outlook, the price target for SJM is ~ $118, offering a relatively low 3% upside. The acquisition of Hostess undoubtedly introduces a favourable dynamic, yet it seems the market has already priced in the anticipated benefits of this acquisition. With such a limited margin of safety, I recommend a hold rating on the stock.

Risk and final thoughts

One of the inherent risks to the hold rating on SJM is the possibility that the Hostess acquisition may yield benefits beyond expectations. Acquisitions, while fraught with challenges, can sometimes unlock unforeseen synergies and growth opportunities. If the integration of Hostess into SJM's operations proves to be more seamless than anticipated and the combined entity is able to rapidly capitalize on cross-selling opportunities, operational efficiencies, and expanded market reach, revenue, and profit growth could surpass current projections. Additionally, the combined expertise might lead to faster-than-expected product innovations that resonate with consumers. If the market starts to recognize these unexpected benefits and adjusts its valuation metrics accordingly, SJM's stock could experience an upward re-rating.

In evaluating SJM's prospects, the strategic acquisition of Hostess emerges as a significant move, aiming to enhance the company's foothold in the food industry. Yet, it seems the market has already factored in the anticipated benefits of this merger into the stock's valuation. Despite my optimistic outlook, the anticipated upside appears modest. This low single-digit growth rate, even amidst such positive sentiment, highlights the intricate challenges and competitive landscape of the food sector. The lack of a margin of safety further accentuates the need for a cautious approach. Weighing all these considerations, while SJM demonstrates promise with its strategic initiatives and growth potential, its prevailing valuation suggests a hold recommendation for the stock.

For further details see:

J. M. Smucker: Hostess Acquisition Benefit Has Been Priced In