JSNSF - J Sainsbury Stock: Trading At Fair Value

2023-04-07 02:45:24 ET

Summary

- Sainsbury's operates supermarkets in the UK.

- Competition has been fierce due to Aldi and Lidl, as well as e-commerce retailers.

- Inflationary pressures have allowed the business to increase sales, while margins have been maintained.

- Management has been aggressively deleveraging, which could mean improved dividend payments in the coming years.

- The company is less profitable than M&S and Tesco while trading at a similar valuation.

Company description

J Sainsbury's plc ( JSNSF / JSAIY ) operates in the retail and financial services industries. The company has three segments, including Retail-Food, Retail-General Merchandise and Clothing, and Financial Services. It offers various store formats, including supermarkets and convenience stores, and is also involved in online grocery and general merchandise operations.

Additionally, J Sainsbury's plc provides financial services such as credit cards, scorecards, personal loans, and insurance products for home, car, pet, travel, and life.

Sainsbury's is one of the largest supermarket chains in the UK and is considered to be one of the "Big Three" alongside Tesco ( TSCDY ) and Asda.

Share price

Sainsbury's share price has trended down in the last decade as greater competition and market conditions have made the company unattractive to investors.

Financial analysis

{kind=link}

Presented above is Sainsbury's financial performance for the last decade.

Revenue has grown at a CAGR of 3%, driven by consistently improving performance across the historical period. As the data shows, revenue has only spiked above 5% twice, when Sainsbury's acquired Argos and Habitat .

The growth of online retailers like Amazon has put pressure on traditional supermarket chains like Sainsbury's. Online shopping has increased substantially in the last decade, with this trend transferring slowly to groceries also. This has contributed to greater competition for Sainsbury's as it could rely on a certain level of footfall, allowing for cross-selling to other departments such as apparel, but this is less of a benefit now. Overarchingly, this is the main reason why the Argos/Habitat acquisition has been unable to produce outsized returns for the business, they are both facing tough competition from the likes of Amazon.

Price competition has become a key feature of the UK grocery market, with supermarket chains regularly engaging in price wars to attract customers. This has been exacerbated by Aldi and Lidl entering the UK market, as they have offered consumers low prices with comparable quality. These factors have made it very difficult to trade in the market, with most players accepting low single-digit growth for this reason.

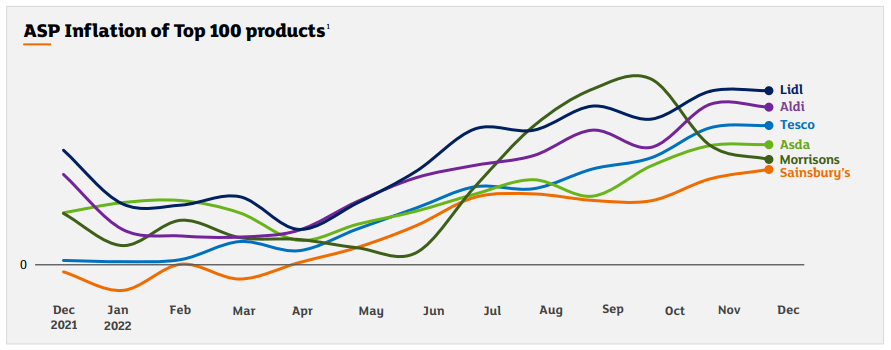

Current economic conditions have had a significant impact on supermarkets due to the pressures of inflation. Food inflation has been high in the UK, forcing supermarkets to follow suit to maintain margins. As the following graph shows, the increase in the last year has been more than all of the last decade.

Sainsbury's strategy has been to slowly increase prices, purposely doing so after their competitors have. This has the scope to be beneficial as it increases the chances of consumers switching to them but importantly discourages consumers from departing. As the following graph shows, Sainsbury's remains behind its peers.

{kind=link}

Surprisingly, this strategy has worked according to volume data. As the following graph shows, Sainsbury's volume has actually increased, whereas the average of its big 4 peers is a decline. Consumers generally look to avoid switching and so this is a noticeable change in market dynamics, with gains toward Sainsbury's.

Volume change (Sainsbury's)

Despite this strategy, GPM and EBITDA-M have remained flat across the last 2 years, suggesting this lag is not impacting the business negatively.

Margins

Sainsbury's margins have remained relatively flat across the historical period, with some small fluctuations but always reverting to the mean. The key growth area for Sainsbury's is GP, which has grown at a far higher rate than revenue. This is likely driven by greater pricing pressures on its supply chain, justified by greater competition. Unfortunately, this has been offset by an 11% growth rate in S&A expenses, which is why the GP gains have not translated to an improvement in EBITDA-M. Management has done well in recent years to improve efficiency in this regard, with the expense falling to 4% of revenue. The target should be 3%, with realistic scope for the company to reach this level.

Balance sheet

Management has been utilizing its FCF to aggressively deleverage the business, primarily because it is overleveraged, at least in our view. A 3x ND/EBITDA ratio is the maximum in our view but does not necessarily give a company the flexibility it desires. Sainsbury's has been trading at above this level, in large part due to leases on properties rather than traditional debt, which is less of a risk. Nevertheless, Management has been deleveraging to the extent that this ratio has reached 3.06x, which we believe to be good.

With this deleveraging process in full swing, dividend payments have remained constrained. Payments have essentially not grown, which is a noticeable underperformance against many other established businesses. We can see deleveraging slowing in the near term, which could mean we see dividend payments increase. Sainsbury's current yield is 5%, which is already quite attractive.

Investors should be aware that Sainsbury's' net asset value excluding goodwill is £6,908m, compared to a market cap of £6,323m. This means that the company is trading below its minimum liquidation value, which could signal a bottom for the stock price.

Outlook

{kind=link}

Presented above is Wall Street's consensus outlook for the coming 5 years.

Revenue growth is expected to be mild, with only a 1% growth rate. With economic conditions uncertain, this looks to be a conservative view of the business. We would expect growth at the normalized economic rate, which should exceed 1% over the long term.

EBITDA-M is expected to expand slightly, driven in large part by continued scale benefits as the business grows larger. Interestingly FCF and NI are expected to decline, which the evidence does not support. This could be a conservative view of the business but we would expect more of the same.

Peer comparison

{kind=link}

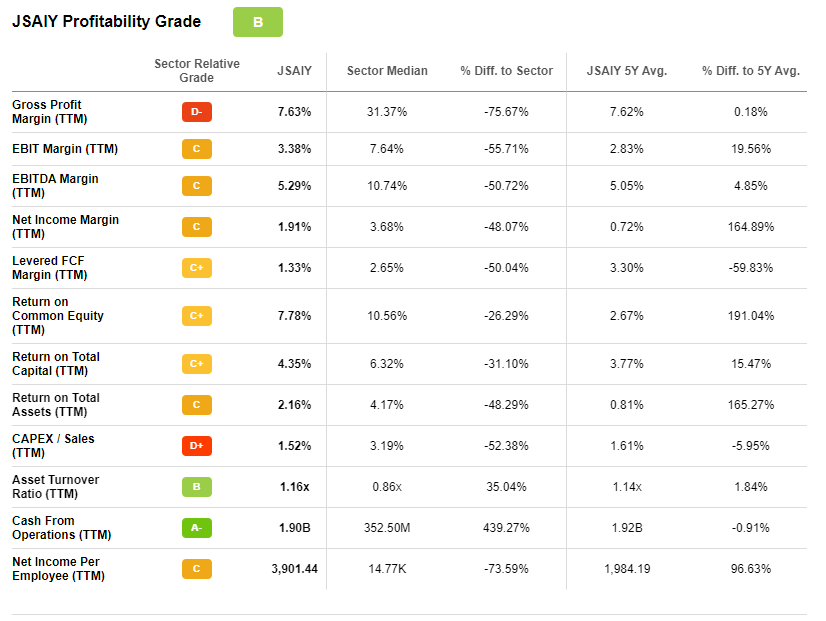

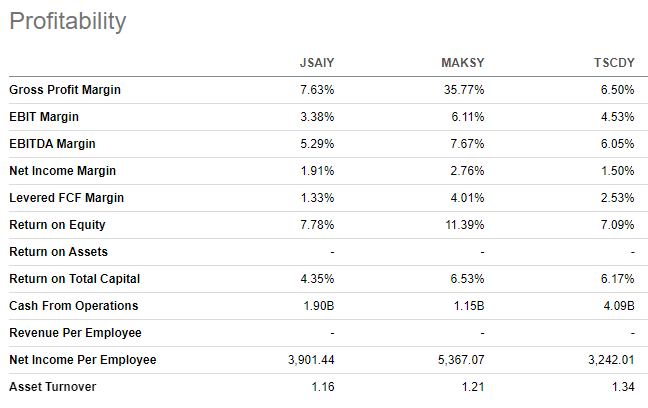

Presented above is a comparison of Sainsbury's to a cohort of consumer staple businesses.

Surprising to us, Sainsbury's scores well, receiving a B rating. Our view is that the company is not that attractive, however, as it underperforms on the metrics we care about. Sainsbury's is noticeably lower on an EBITDA and NI level, which is not compensated for in any other metrics. Sainsbury's is essentially a marketplace and so will always be held back by tight margins, with no ability to justify pricing superiority.

{kind=link}

Sainsbury's also performs poorly from a growth perspective, as the business is wholly tied to economic development. As a supermarket, the company does not have scope to price beyond the market and it is evident that the retail segments of Argos/Habitat cannot move the needle.

Valuation

{kind=link}

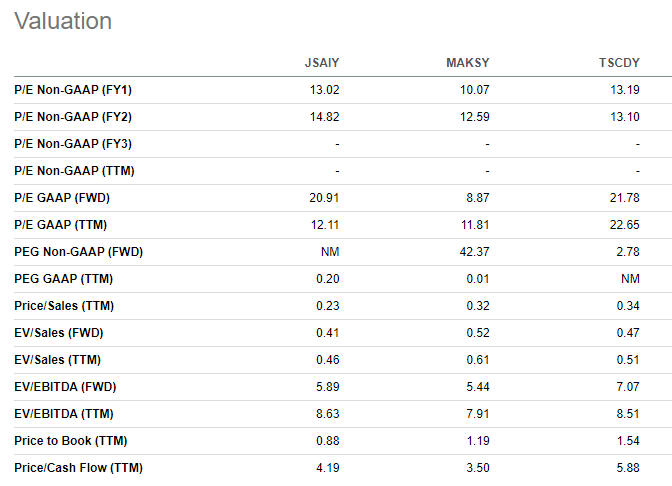

Sainsbury's valuation is given an A rating, owing to the fact the company is trading at a sharp discount to its peers. On a forward EBITDA basis, the discount is over 50%, which looks substantial. This issue is that Sainsbury's is less profitable and growing slower, which means a discount is appropriate.

The degree to which a discount should be applied is based on the comparable businesses in our view, those being Tesco and Marks and Spencer ( MAKSF ). Both businesses are UK retailers with a substantial supermarket footprint.

Both businesses are more profitable than Sainsbury's but not by a significant level. This to us suggests Sainsbury's should trade at a slight discount to these businesses, otherwise, investors would be better off with them.

{kind=link}

Sainsbury's looks to be trading at a similar valuation to these businesses, with a slight discount or premium based on the metric considered. The key metrics we care about are NTM P/E and EBITDA, both of which suggest little upside.

{kind=link}

Final thoughts

Sainsbury's has faced additional competition and changing consumer trends, growing sustainably despite this. Unfortunately, the market dynamics mean the company is just not very attractive. Margins are low and the businesses focus is primarily on achieving inflation-linked growth. Sainsbury's current valuation does not suggest any substantial upside, although we can see dividends increasing in the coming years following additional debt repayments.

For further details see:

J Sainsbury Stock: Trading At Fair Value