JBL - Jabil: Beyond The Surface Value And Growth At Your Fingertips

2023-10-20 04:14:30 ET

Summary

- Jabil is a leading provider of worldwide manufacturing services and solutions in the semiconductor industry.

- The company is well-positioned to benefit from the trend of re-shoring manufacturing operations to the US and the increasing demand for outsourcing.

- Jabil's involvement in secular growth segments, such as electric vehicles and healthcare, promises substantial expansion and profitability.

- Our fundamental and valuation analysis leads us to believe that Jabil represent a very interesting mix between Value and Growth.

- We initiate on Jabil with a Strong Buy recommendation and a $170.10 Target Price.

Introduction

The year 2023 has been marked by a strong rally on Equity. In this context, many Tech players have strongly performed.

Bloomberg

Pushed by potential secular trends narratives such as A.I. disruption and E.V. adoption, many names reached high valuation levels putting some investors into uncomfortable positions. For these reasons, we have been trying to look at names with strong potential without being too expensive. Through this investment case, we'll explain what makes Jabil Inc. (JBL) such an interesting play.

Company Presentation

Founded in 1966, JBL is one of the leading providers of worldwide manufacturing services and solutions. The firm is specialized in electronics design, production and product management services to companies in various industries and end markets such as Automotive Electronics Manufacturer, Semi-Cap Equipment's, Cloud Data centers, Defense & Aerospace, Telecommunication Healthcare and more.

Operations

JBL operations are divided into two major business segments namely:

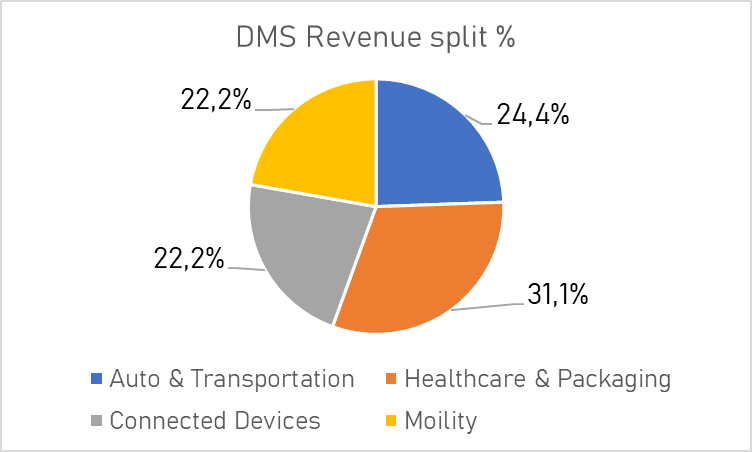

- Diversified Manufacturing Services ((DMS)) focuses on manufacturing services for material sciences, technologies, and healthcare. It works with customers to develop and manufacture products in the automotive and transportation, connected devices, healthcare and packaging, and mobility industries.

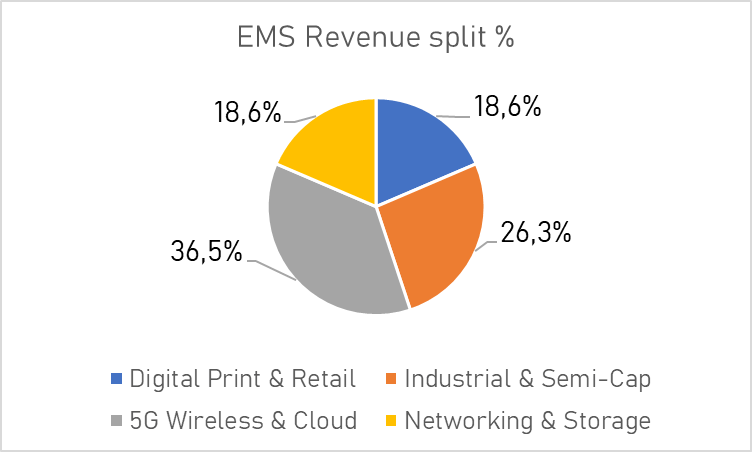

- Electronics Manufacturing Services ((EMS)) focuses on IT, supply chain design, and engineering, technologies largely centered on core electronics. The products Jabil makes for its customers are used in the 5G, wireless and cloud, digital print and retail, industrial and semi-cap, and networking and storage industries.

Both of these segments account for 50% of revenues.

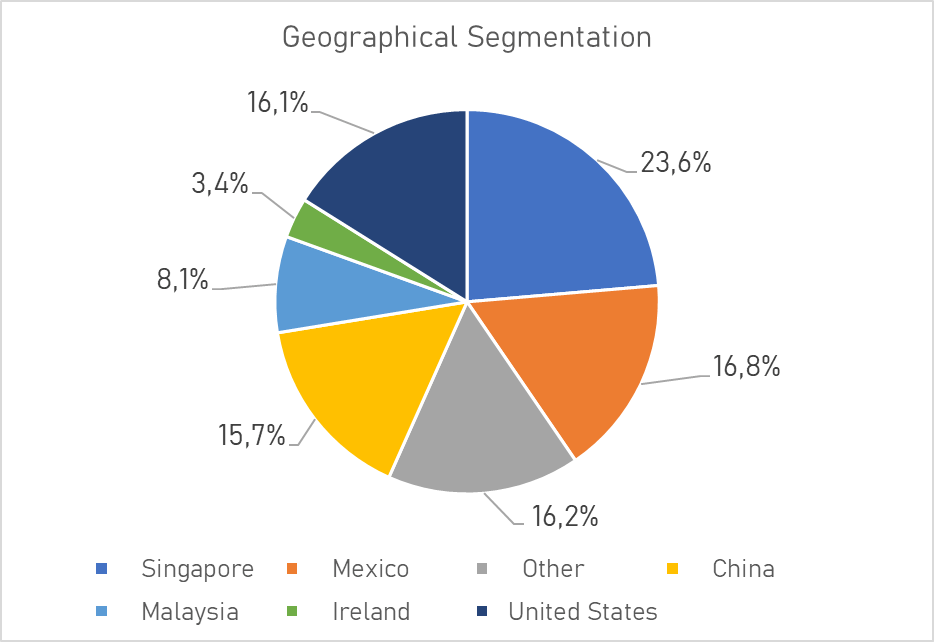

Geographical Segmentation And Main Clients

JBL's geographical reach is concentrated, 6 countries account for 83.8% of sales, the top 3 end markets being Malaysia (23.6%); Mexico (16.8%), and the U.S. (16.1%).

{kind=link}

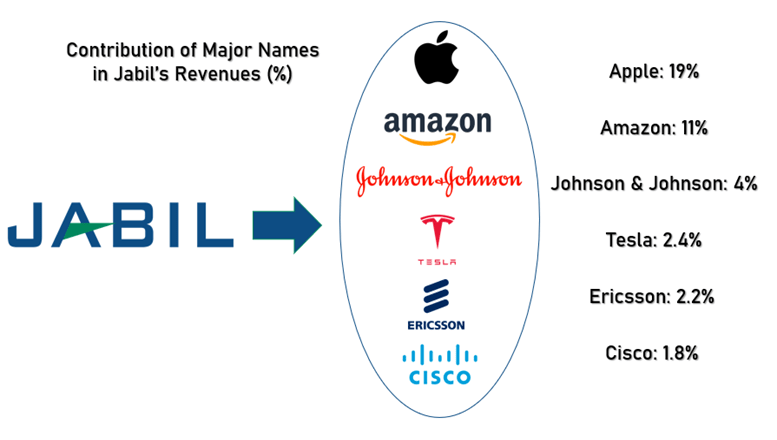

In terms of client reach, JBL is also very concentrated as few customers account for a very important portion of revenues. The company's five largest customers account for 45% of the company's revenue and 80 customers account for approximately 90% of the company's revenue. However, this concentration in revenue should not offset the prestige of the clients trusting JBL.

{kind=link}

End Market Segmentation

In terms of End Market, JBL is way more diversified. We decided to represent separately the EMS and the DMS segment to give you more visibility. Remember, these two segments account for 50% of revenues. JBL is well exposed to various sectors the 3 mains being 5G Wireless & Cloud (36.5% of EMS), Healthcare & Packaging (31.1% of DMS), Industrial & Semi-Cap (31.1% of DMS)

Company presentation Company presentation

{kind=link}

{kind=link}

Now that we have presented the company in detail, let's dive into what we believe could represent major growth drivers for JBL.

Re-shoring On The Way

Re-shoring has become one of the major subjects in the U.S. To mitigate supply chain elevated logistic costs and geopolitical risks, especially after the Covid-19 crisis and tensions experienced with China, manufacturers across many industries are issuing plans and strategies to re-shore their activities within the U.S. This is particularly true for the semiconductors and pharma players whose are for many JBL clients. These initiatives are supported by massive government plans. First, on the Healthcare side, The American Jobs Plan ((AJP)), allocates $130 billion to bolster supply chains and encourage the return of manufacturing operations to the United States. On the Semiconductor side, following the Chip Act, many semiconductor manufacturers announced they would invest around $200 billion into building new fabrication facilities in the US.

For these reasons, we expect JBL to benefit first from re-shoring possibilities as more and more companies are moving property plants, and equipment away from China to the US.

Outsourcing As An Undeniable Trend

Demand for outsourcing could also be a major growth driver for JBL. As the semiconductor (supported by A.I. notably) and healthcare industries are evolving toward more and more complex products, many customers want to reduce their manufacturing costs and thus externalize several steps of their production process. Also, we expect the rise in demand for complex medical devices to support JBL's growth. The company is particularly well positioned in this sector, especially after the acquisition of Nypro Healthcare in 2013.

The group's long-term partnership with Johnson & Johnson (JNJ) signed in 2019 (representing $1 billion in revenues) is in our view proof of the quality and trustworthiness of the firm expertise. This puts the firm in a very good position to obtain more outsourcing deals of this kind in the future.

Reminder: In 2018, JBL announced a long-term strategic collaboration with Johnson & Johnson Medical Devices. Under the terms of this agreement, Jabil took over 14 Johnson & Johnson Medical Devices sites in the United States and increased its capacity in the medical equipment sector, one of the key areas of its diversification strategy.

Segments Exposed To Secular Growth Supporting The Case

Aside from its « lower value added » businesses, JBL is also involved in very specific and disruptive tasks linked to secular growth markets, especially in the Electric Vehicles ((EV)) and Health care sectors. These themes are very interesting and make the investment case even more compelling as it represents an exposure to longer life cycles characterized by major technological investments and Capex in A.I. / Machine learning (M.L.) / Quantum computing, cloud but also robotics. All these activities in these specific sectors will be crucial in helping the firm to expand its margins and improve its profitability over the long term.

The EV Segment As A Key Growth Driver

As part of all these segments, we identify the EV segment as one of the most important growth drivers. According to the IAE , EVs are expected to represent by 2030 EVs more than 60% of vehicles sold globally reaching a total fleet of nearly 250m. of electric vehicles achieving an average annual growth rate of about 30%.

International Energy Agency (IAE)

JBL management has anticipated this massive shift towards E.V. Thanks to this proactivity and vision, JBL has been able to build through the years, solid relations with some of the largest and most renowned EV companies such as Tesla (TSLA). JBL is working with 8 of the top 10 EV companies in terms of market cap. As legislation is pushing towards the adoption of EVs, we expect JBL to benefit from this shift. Indeed, both in Europe with the 2035 objectives and in the U.S. with the Inflation Reduction Act ((IRA)), EV adoption is being pushed. As this trend seems to be made to last, we expect this segment to experience mid-double-digit growth for the five upcoming years supported also by technological evolutions, the creation of new models, and more. Finally, we see the IRS credits and Tesla's significant role in advancing electric vehicle ((EV)) adoption as very positive for JBL. We hold the belief that JBL, being a supplier to TSLA, is strategically positioned to capitalize on the expanding domestic EV market. Moreover, JBL stands to benefit also in the EV industry from the domestic manufacturing requirements imposed by the IRS, as companies are likely to continue outsourcing production from US-based facilities.

JBL - AMZN Relationship Is Truly Appreciable

In our opinion, there is also an important upside possibly linked to the strong relation with Amazon (AMZN) which now accounts for 11% of sales. JBL has been operating in the cloud segment for many years and is now working with many leading firms strengthening its reputation in a fast-growing market. In our opinion, it's truly appreciable to have AMZN as an important client as it is known for being the company with the highest CAPEX In the world (near $50 b. in 2023).

Bloomberg

A.I.: The Cherry On The Cake

A.I. and machine learning could also be a major driver for the firm allowing it to both reduce costs and increase its top line. A.I. is not new and has already been used in factory automation processes. Even if JBL has been using A.I. for many years, we believe that the current acceleration in A.I. development could help the firm to improve its automation process thus contributing to margin improvements but also increasing potential revenues.

A Value Opportunity Within The Manufacturing Industry

We decided to compare JBL to several peers operating on the same industry namely: Flex (FLEX), Celestica (CLS), Plexus Corp (PLXS), CTS Corp (CTS).

Bloomberg

At first glance, the contrast might be mitigated as the firm trades at a slight premium in terms of P/E and at a huge premium in terms of P/B. This is in our view not necessarily negative. In fact, it shows JBL's capacity to deliver with fewer assets than its peers. Note that it trades at discounts when looking at the Price/Sales ratio and EV/EBITDA.

When comparing JBL to three major Indexes namely the S&P500 (SPX), the Nasdaq100 (NDX) and the Russell 2000 (RTY) the cheapness of JBL is more evident. Its "asset light" model still makes it expensive on a P/B basis.

Bloomberg

These elements lead us to consider JBL as a value play that could attract investors seeking exposure to Growth names without getting into names with very expensive valuations.

Get Value For Money

At Growth Arcane, we appreciate when companies employ well their capital to run their business. In that matter, JBL does not disappoint and is well above its peers as shown by strong ROCE and ROIC, a welcome sight for investors.

Bloomberg

DCF Analysis

For the first 3 years, we use the consensus numbers of revenue growth. We then use the 5-year average growth for the final 3 years. Thanks to supply chain investments and A.I. optimization we expect an improvement on the operating margin resulting in an EBITDA margin of approximately 9% reached by year end of 2027.

{kind=link}

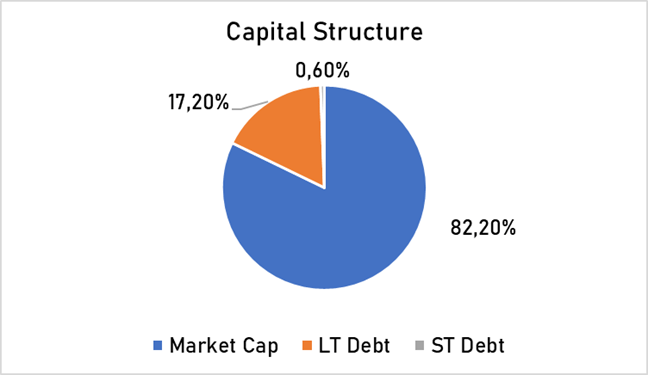

For our WACC calculations, we considered the firm current capital structure which is the following:

{kind=link}

Our assumptions also consider Cost of Equity of 4.71% due to US notes rates and an ERP of 6.30%.

6.30% being the combination of EMR of 10.50% - RF and a Beta of 1.09.

Cost of Debt is calculated with the Notes outstanding and a tax rate of 35%

Company data

Here's what we got:

Bloomberg, Authors forecasts

We reach an Equity Value of 22.2B$ which converts into a price per share of 170.10$

An attractive upside of 24% on JBL at the time we are making this exercise.

Bloomberg, Authors forecasts

You can find above our sensitivity analysis. In our view, it is very supportive as it shows that in the vast majority of scenarios, JBL stands out as a robust bull case. Finally, we have the conviction that rates have made a plateau and that they are more likely now to go downward than upward. This would put even less pressure on valuation.

Risks To The Investment Thesis

The first risk we identified is linked to the customer concentration we mentioned earlier. Indeed, JBL faces a notable risk due to its heavy reliance on two major customers, AAPL and AMZN, constituting over 10% of total revenue each. Apple alone represents 19% of the revenue, while Amazon accounts for 11%. Despite this, JBL's dependency is somewhat mitigated by its diversified involvement across Apples's product range. However, JBL management is in our view aware of that and should already be anticipating a reduction in the Apple mix over time.

The firm might also face persistent supply chain shortages. Even though improvements have been observed recently, this remains a major risk to consider especially in the EV segment where demand is growing faster and faster.

Tougher economic conditions or higher interest rates might also have a negative impact on our forecast.

Conclusion

In conclusion, we believe that JBL offers a compelling investment opportunity that we consider attractive. The company is well-positioned to benefit from the growing trend of re-shoring, driven by supply chain concerns and government initiatives. Additionally, the increasing demand for outsourcing in industries like semiconductors and healthcare, along with its strong partnership with Johnson & Johnson, positions JBL for continued growth. Furthermore, the company's involvement in secular growth segments, particularly in Electric Vehicles, promises substantial expansion. JBL's strategic relations with Amazon and its focus on AI and machine learning add further appeal to its investment thesis. In summary, JBL's diversification, technological expertise, and established client relationships make it a compelling choice for potential investors. We initiate on JBL with a Strong Buy recommendation and a $170.10 Target Price.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Jabil: Beyond The Surface, Value And Growth At Your Fingertips