VOO - Jabil: Despite The Rip Higher More Is Yet To Come

2023-10-17 11:23:50 ET

Summary

- JBL stock is up 123% over the past year. While investors may be tempted to take profits, I say "not so fast".

- The $2.2 billion divestiture of its (low-margin) China Mobility segment to BYD is going to enable JBL to accelerate its stock buyback plan to invest in higher-margin higher-growth businesses.

- The current $2.5 billion share buyback authorization equates to ~14% of the company's current market-cap.

- By FY25, JBL expects core earnings of $10.65/share. With a P/E of only 15x, the stock could easily reach $160/share (+15% from here).

The stock of Florida-based Jabil (JBL), a top-tier diversified and electronics manufacturing services ("EMS") provider, is up 23% since my last BUY-rated article on August 28th (see What The $2.2 Billion BYD Deal Means For Jabil Shareholders ). However, despite the nice rip, in my opinion, JBL is still undervalued. Today, I will update investors on the BYD deal, Jabil's prospects, and guidance going forward, and take a look at the stock's current and future valuation.

Investment Thesis

Diversified electronics and manufacturing services companies have traditionally traded at relatively low valuation levels as compared to the broad S&P500 - primarily because they operate relatively low-margin businesses:

As can be seen in the graphic above, JBL has traditionally traded at roughly half the P/E of the S&P500. So, despite the stock rising +128% over the past year, JBL's current P/E of 23x is still slightly below that of the S&P500's P/E of 25x . Now, some investors might look at that chart and be tempted to take profits. However, there are likely more gains to come - here's why.

Earnings

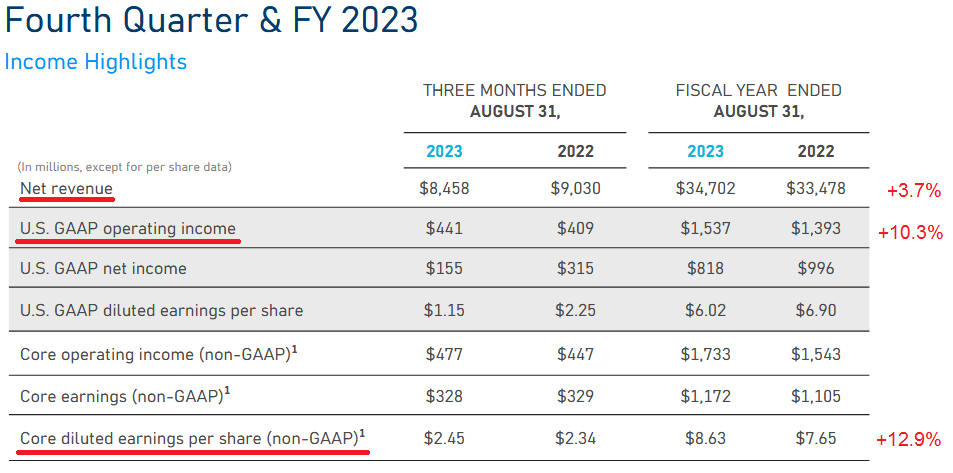

Since my last article on Jabil (see reference above), the company released its Q4 and FY2023 earnings report in late September. The FY23 summary below was taken from the Q4 Presentation :

{kind=link}

As can be seen, and as I have been reporting in my Seeking Alpha articles on JBL, despite relatively modest revenue growth during FY23, the combination of margin expansion and a reduced outstanding share count due to the company's use of strong free-cash-flow to execute a meaningful stock buyback plan, GAAP operating income and core diluted EPS growth grew substantially faster than top-line growth.

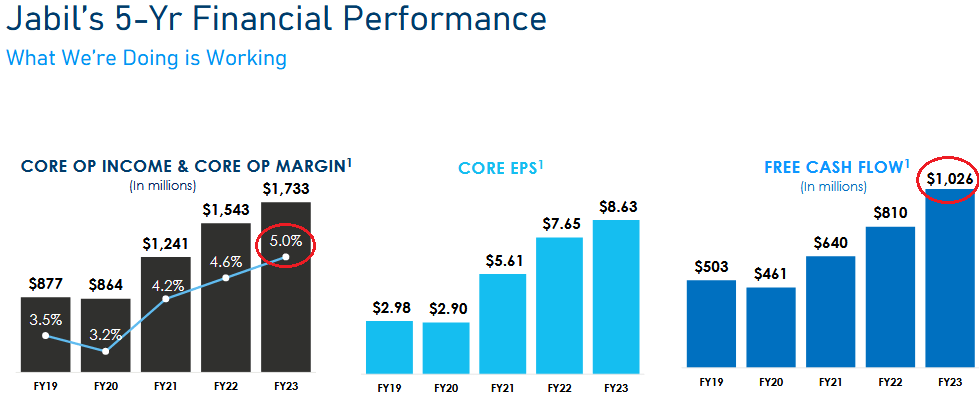

Indeed, as the graphic below shows, in FY23 Jabil's operating margin grew 40 basis points yoy. Better yet, FCF grew to over $1 billion (+26.7% yoy) - or an estimated $7.82/share based on the average of 131.2 million fully diluted shares outstanding at the end of Q4 (which were -4.2% yoy):

{kind=link}

The combination of higher margins, strong free cash flow generation, and a lower outstanding share count continues to be the primary investment catalysts for investors going forward. Note that Jabil was able to achieve the financial results shown above despite the pandemic supply-chain shocks. This is a testament to the ability of Jabil's management team and the strength of the company's planning and logistics.

The $2.2 Billion BYD Deal

Along with the earnings report, Jabil clarified and updated details on the pending $2.2 billion sale of its China Mobility segment to BYD Electronics (BYDDY) (BYDDF). First of all, on September 26th, Jabil announced the two companies had reached a definitive agreement to complete the transaction on a fully cash basis. The deal is expected to close in the first two quarters of Jabil's FY24 (i.e. before the end of February 2024).

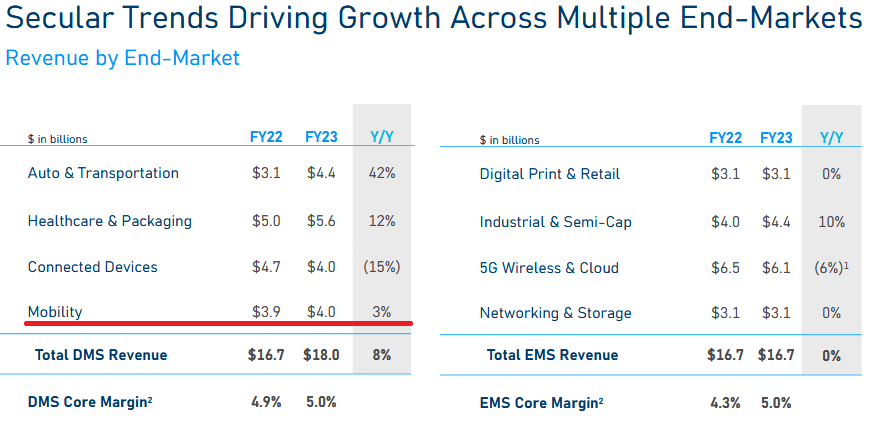

Secondly, the company clarified that the divestment consists of the entirety of Jabil's Mobility Segment, which represented $4 billion in revenue in FY23 (or ~11.5% of total revenue):

{kind=link}

Now, some investors would question why the stock has ripped higher despite the pending loss of some 11.5% of total revenue. As I suggested in my previous article, there are numerous reasons why the market responded so bullishly to this news:

- The Mobility segment consists of high-volume low-margin Apple business (primarily making iPhone cases and circuit boards). As a result, Jabil has further reduced its dependence on Apple (something the company has been successfully working on for years now).

- Growth in the Mobility segment has significantly lagged several of JBL's other segments such as Automotive (EVs), Healthcare & Packaging, and Industrial & Semi-Cap.

- The divestiture reduces Jabil's exposure to Chinese supply-chain risks.

- The divestiture will enable Jabil to fund investments in faster growing higher-margin businesses like EVs, renewable energy, AI, and data centers (review the Q4 presentation for more details on growth prospects).

- The $2.2 billion cash windfall has enabled Jabil to accelerate its already substantial stock-buyback plan.

Buybacks

Indeed, on point #5 above, note that Jabil announced in the Q4 report that the Board of Directors has increased Jabil's stock buyback authorization to $2.5 billion. It is important for investors to understand that $2.5 billion equates to 14% of Jabil's current market cap of $17.8 billion. This follows a $1 billion share buyback plan announced in September of 2022 (of which $776 million remained outstanding as of end of Q4).

On the Q4 conference call , Jabil CFO Mark Dastoor gave investors additional insight into the buyback plan:

We expect to begin executing on this upsized authorization immediately. You heard Adam say that we were unable to complete our Q4 share repurchases due to restrictions around the Mobility transaction. We plan to launch a $500 million accelerated share repurchase transaction in October prior to the close of our Mobility transaction. Post-closing of the Mobility transaction, we intend to execute a series of additional accelerated buybacks throughout FY '24 and FY '25 with the intent of optimizing share repurchases and interest expense, thereby maximizing the EPS impact.

My opinion is that it was the $500 million of accelerated buybacks that started this month that led to the stock's recent jump higher.

Lastly, note that in FY23, Jabil repurchased 6.7 million shares at an average price of $72.82. The stock is currently trading north of $138. Now that is a successful stock buyback plan!

Valuation

Some investors might say that the current P/E=23x is rich for a diversified electronic & manufacturing company like Jabil. However, let's take a look at Jabil's guidance going forward and consider that the company has traditionally under-promised and over-delivered.

First off, of the $2.2 billion in proceeds from the divestiture, the company expects total costs and taxes will equate to ~$300 million while restructuring costs are expected to be ~$200 million. That leaves total "net" proceeds of $1.7 billion.

The midpoint of FY24 revenue guidance, driven by continued strong growth in the Automotive, Healthcare & Packaging (which will become JBL's largest operating segment), and Industrial & Semi-cap segments is for $33.5 billion. The point here is that despite selling a segment that consisted of 11.5% of FY revenue, JBL expects FY24 revenue to dip by only an estimated $1.2 billion (or -3.5%).

For FY24 core operating margin, Jabil is expecting another 40 basis point increase to ~5.4%. Consider then an extra 40 basis points on an estimated $33.5 billion in revenue equates to $13.4 million in additional incremental operating margin on a yoy basis.

Meantime, Jabil is expecting FCF of $1 billion+ again in FY24 as cap-ex investment stays relatively flat at less than 2.5% of revenue.

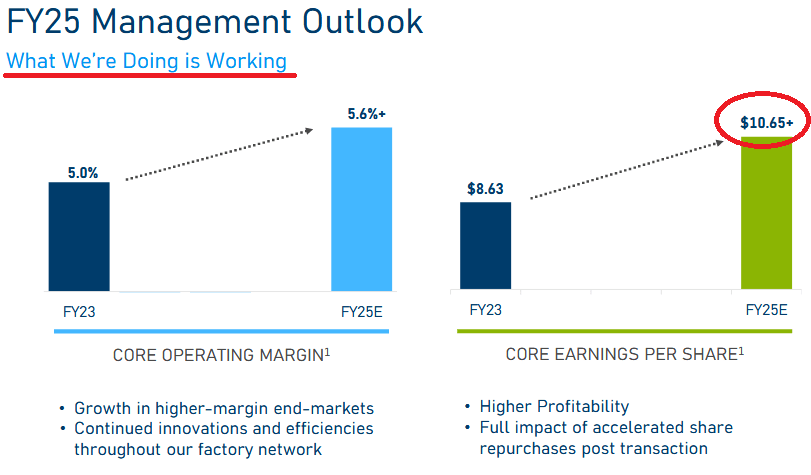

Looking out to FY25, investors will see the big payoff:

{kind=link}

As can be seen in the slide, core operating margin is expected to reach 5.6% in FY25 with core EPS growing to $10.65/share.

Now I wouldn't expect JBL's P/E to reach parity with the S&P500. However, I don't think it is a stretch or unreasonable to expect Jabil's long-term P/E to reach 15x... and 15 times core EPS of $10.65 equates to a stock price of $160.

Risks

At the end of Q4, the balance sheet was strong: total debt was $2.9 billion while cash and cash equivalents amounted to $1.8 billion, for a net debt of only $1.1 billion. That equates to a total debt to core EBITDA ratio of only ~1.1x.

Revenue in 3 of Jabil's 7 remaining segments (Networking & Storage, 5G Wireless & Cloud, and Connected Devices) is expected to decline in FY24. I suspect much of this decline is by choice as JBL management is clearly moving toward a higher-margin business model. That said, growth in the other segments needs to materialize as expected in order for the overall revenue estimates noted earlier to come to fruition.

Upside risks included faster growth in the growing segments and/or better-than-expected margin expansion.

Summary & Conclusions

Despite the recent rip higher in JBL's stock price (see chart below), investors would be wise to resist taking profits here. The combination of a strong stock buyback plan and margin expansion is going to lead to strong growth in earnings and FCF/share. Even a modest increase in P/E valuation to 15x could easily lead to a stock price of $155 next year. As a result, I reiterate my BUY on JBL and increase my price target from $125 to $155.

As seen in the chart above, Jabil stock has absolutely creamed the performance of the S&P500 and Nasdaq-100 as represented by the Vanguard S&P500 ETF ( VOO ) and the Invesco Nasdaq-100 Trust ( QQQ ), respectively. While I don't expect that level of out-performance to continue going forward, investors are advised to hold onto Jabil stock for at least another year (or two).

For further details see:

Jabil: Despite The Rip Higher, More Is Yet To Come